Kreidler took action against Aliera and its partner, Trinity Healthshare, Inc. (Trinity) in May 2019 after an investigation revealed that since August 2018, the companies sold 3,058 policies to Washington consumers and collected $3.8 million in premium. Trinity agreed to Kreidler’s order.

“Aliera and Trinity promised to provide people with coverage when they needed it only to leave consumers with huge medical bills,” said Kreidler. “I’m taking action today to send a message to all scam artists – if you harm our consumers, you will pay heavily.

“Shopping for health insurance can be very stressful – especially if you have to worry about being ripped off. True insurance companies have to meet rigorous standards before they can sell coverage to consumers. These companies are hiding behind a federal and state exemption that exists for legitimate health care sharing ministries and using it to rake in profit across the country on the backs of vulnerable consumers.”

Aliera, an unlicensed insurance producer in Washington, administered and marketed health coverage on behalf of Trinity HealthShare. Trinity represents itself as a health care sharing ministry.Such ministries are exempt from state insurance regulation only if they meet statutory requirements. If so, they do not have to meet the same consumer protections guaranteed under the Affordable Care Act. This includes providing coverage for anyone with a pre-existing medical condition.

A legal health care sharing ministry is a nonprofit organization whose members share a common set of ethical or religious beliefs and share medical expenses consistent with those beliefs.

Kreidler’s office has received more than 20 complaints from consumers. Some believed they were buying health insurance without knowing they had joined a health care sharing ministry. Many discovered this when the company denied their claims because their medical conditions were considered pre-existing under the plan.

“Real health care sharing ministries can offer a valuable service to their members,” Kreidler said. “Unfortunately, we’re seeing players out there trying to use the exemptions for legitimate ministries to skirt insurance regulation and mislead trusting consumers. I want these outfits to know we’re on to them and we will hold them accountable.”

Sold insurance without a Washington insurance producer license.

Represented an unauthorized insurer, Trinity.

Operated an unlicensed discount plan organization.

Kreidler’s investigation into Trinity found that it failed to meet key federal and state requirements:

Trinity was formed on June 27, 2018, without any members. Federal and state laws require that health care sharing ministries be formed before Dec. 31, 1999, and their members to have been actively sharing medical costs.

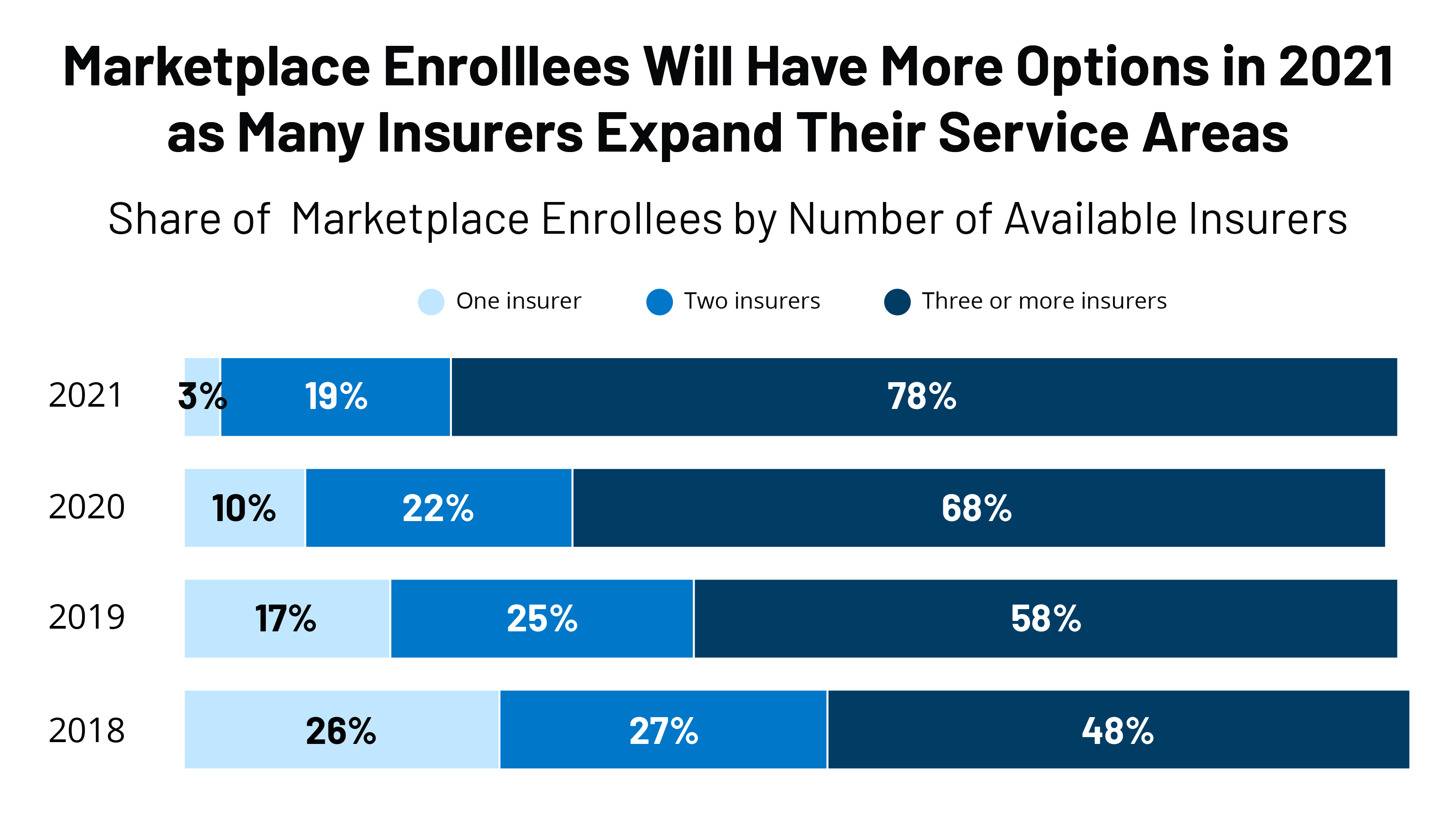

Some 30 insurers are entering the individual market, and an additional 61 are expanding their service area within states, a KFF report says.

Insurer participation in the Affordable Care Act marketplace in 2021 is seeing a third straight year of growth as several insurers are entering the market or expanding their service area, according to a recent Kaiser Family Foundationreport.

For instance, in 2020, UnitedHealthcare, the nation’s largest insurer, became a new entrant in five states, according to the report: Arizona, Maryland, North Carolina, Tennessee and Virginia. Twenty states had new entrants to the market.

For 2021, 30 insurers are entering the individual market, and an additional 61 are expanding their service area within states.

There will be an average of five insurers per state in 2021, up from a low of 3.5 in 2018, but still below the peak of six in 2015. Only 10% of counties will have a single insurer offering in 2021, down from 52% of counties in 2018, the report said. Rural areas tend to have fewer insurers in the ACA market.

Often, when there is only one insurer participating on the exchange, that company is a Blue Cross Blue Shield or Anthem plan, the report said. Before the ACA, state individual markets were often dominated by a single Blue Cross Blue Shield plan.

WHY THIS MATTERS

Despite uncertainties surrounding the ongoing pandemic, the end of the individual mandate and the question of whether the Supreme Court will rule next year to invalidate the entire ACA, the numbers show that insurers appear bullish on participation.

Insurers remained profitable during the pandemic due to decreases in healthcare utilization and claims costs. They are on track yet again to owe substantial rebates to consumers based on low medical loss ratios in 2021.

Even with the lack of a mandate, individuals continue to enroll in ACA plans, with enrollment this year more than keeping pace with last year’s figures. Premiums for 2021 are 1-4% below the average.

THE LARGER TREND

The enrollment numbers continue a trend of rising insurer participation in the ACA going into the 2020 market, and lower premiums.

Insurer participation next year equals the average participation levels at the outset of the marketplaces in 2014, according to the KFF report.

Since 2014, the number of insurers participating on the exchanges has been in flux. Going into the 2018 plan year, many insurers left the market or reduced their footprint due to losses in the market.

Millions of Americans are in danger of losing their homes when federal and local limits on evictions expire at the end of the year, a growing body of research shows.

A report issued this month from the National Low Income Housing Coalition (NLIHC) and the University of Arizona estimates that 6.7 million households could be evicted in the coming months. That amounts to 19 million people potentially losing their homes, rivaling the dislocation that foreclosures caused after the subprime housing bust.

Apart from being a humanitarian disaster, the crisis threatens to exacerbate the coronavirus pandemic, according to a forthcoming study in the Journal of Urban Health.

“Our concern is we’re going to see a huge increase in evictions after the CDC moratorium is lifted,” said Andrew Aurand, vice president of research at the NLIHC and a co-author of the report.

The number of Americans struggling to pay rent has steadily risen since this summer, according to the Census Bureau’s Household Pulse Survey. In the latest survey, from early November, 11.6 million people indicated they wouldn’t be able to pay the rent or mortgage next month.

Meanwhile, some renters who are still paying rent are relying on “unsustainable” income to make ends meet. Among those who report trouble making rent, “More than half are borrowing from family and friends to meet their spending needs, one-third are using credit cards, and one-third are spending down savings,” the NLIHC report found.

Approaching a “payment cliff”

In early September, the U.S. Centers for Disease Control and Prevention barred evictions through year-end, describing the move as a public health measure to reduce spread of the coronavirus. The CDC order protects renters earning less than $99,000 if they have lost income during the pandemic and are likely to become homeless if they’re evicted.

Many states and cities also imposed renter protections during the spring and summer, and others established rental assistance programs to help tenants make ends meet. However, both types of programs are quickly expiring.

Once the CDC moratorium expires,Aurand said, “We expect to see a jump in [eviction] filings, and we know that even now, filings are already occurring. Come January, sadly, for a number of tenants, the next step is the landlord will evict them.”

The situation could reach crisis levels in the new year. With Congress yet to pass another coronavirus relief package, about 12 million Americans are set to lose their unemployment benefits the day after Christmas, a sharp fall in income that would make it harder for many people to pay rent. An abrupt cutoff would slash income by about $19 billion per month, Nancy Vanden Houten, lead economist at Oxford Economics, said in a research note.

Although the Trump Administration has restricted evictions for most households through the end of the year, it did not relieve renters of the need to pay rent. That means many renters may face a “payment cliff” at year’s end, when they must pay several months’ worth of back rent or face eviction.

“If renters are required to quickly repay past due rent or face eviction, the hardship will fall predominantly on lower-income families who have already been disproportionately affected by the coronavirus crisis,” Vanden Houten wrote.

Said Aurand, “If you were a low-income renter before the pandemic and you were hit financially, even if your income starts to recover, you’re going to have a very hard time paying back that rental debt.”

“What we really need is rental assistance,” he noted. “The underlying problem is renters struggling to pay their rent because we’re in an economic crisis, and the moratorium doesn’t address that.”

Long-term impact

Academics have also pushed for direct aid to renters and homeowners, citing the extreme economic fallout from the coronavirus and related shutdowns. In Los Angeles, where 1 in 5 renters were late on rent at some point this summer, residents are facing “an income crisis layered atop of a housing crisis,” researchers at the University of California – Los Angeles have said.

“Delivering assistance to renters now can not just stave off looming evictions, but also prevent quieter and longer-term problems that are no less serious, such as renters struggling to pay back credit card or other debt, struggling to manage a repayment plan, or emerging from the pandemic with little savings left,” they wrote in August report. “Renter assistance can also help the smaller landlords who are disproportionately seeing tenants unable to pay.”

A groundswell of evictions would cause enormous financial hardship. Losing a home is one of the most traumatic events a family can experience, with research showing that people who have experienced eviction are more likely to lose their jobs, fall ill or suffer from mental-health consequences. Children whose families are evicted are more likely to drop out of school, while evictions also contribute to the spread of COVID-19, according to a forthcoming study from UCLA viewed by “60 Minutes.“

“We’ve got a country that’s about to witness evictions like they’ve never witnessed before,” Laura Tucker, a social worker for Florida’s Hillsborough County School District, told “60 Minutes.”

“An eviction can impact a family’s ability to re-house for more than 10 years,” she said.

For that reason, housing and public health experts have said that rental aid now

“Now is the time for action to provide emergency rental assistance. A failure to do so will result in millions of renters spiraling deeper into debt and housing poverty, while public costs and public health risks of eviction-related homelessness increase,” the NLIHC report says. “These outcomes are preventable.”

Of his many plans to expand insurance coverage, President-elect Joe Biden’s simplest strategy is lowering the eligibility age for Medicare from 65 to 60.

But the plan is sure to face long odds, even if the Democrats can snag control of the Senate in January by winning two runoff elections in Georgia.

Republicans, who fought the creation of Medicare in the 1960s and typically oppose expanding government entitlement programs, are not the biggest obstacle.Instead, the nation’s hospitals — a powerful political force — are poised to derail any effort. Hospitals fear adding millions of people to Medicare will cost them billions of dollars in revenue.

“Hospitals certainly are not going to be happy with it,” said Jonathan Oberlander, professor of health policy and management at the University of North Carolina at Chapel Hill.

Medicare reimbursement rates for patients admitted to hospitals are on average half what commercial or employer-sponsored insurance plans pay.

“It will be a huge lift [in Congress] as the realities of lower Medicare reimbursement rates will activate some powerful interests against this,” said Josh Archambault, a senior fellow with the conservative Foundation for Government Accountability.

Biden, who turns 78 this month, said his plan will help Americans who retire early and those who are unemployed or can’t find jobs with health benefits.

“It reflects the reality that, even after the current crisis ends, older Americans are likely to find it difficult to secure jobs,” Biden wrote in April.

Lowering the Medicare eligibility age is popular. About 85% of Democrats and 69% of Republicans favor allowing those as young as 50 to buy into Medicare, according to a Kaiser Family Foundation tracking poll from January 2019. (Kaiser Health News is an editorially independent program of the Kaiser Family Foundation.)

Although opposition from the hospital industry is expected to be fierce, it is not the only obstacle to Biden’s plan.

Critics, especially Republicans on Capitol Hill, will point to the nation’s $3 trillion budget deficit as well as the dim outlook for the Medicare Hospital Insurance Trust Fund. That fund is on track to reach insolvency in 2024. That means there won’t be enough money to pay hospitals and nursing homes fully for inpatient care for Medicare beneficiaries.

It’s also unclear whether expanding Medicare will fit on the Democrats’ crowded health agenda, which includes dealing with the COVID-19 pandemic, possibly rescuing the Affordable Care Act (if the Supreme Court strikes down part or all of the law in a current case), expanding Obamacare subsidies and lowering drug costs.

Biden’s proposal is a nod to the liberal wing of the Democratic Party, which has advocated for Sen. Bernie Sanders’ government-run “Medicare for All” health system that would provide universal coverage. Biden opposed that effort, saying the nation could not afford it. He wanted to retain the private health insurance system, which covers 180 million people.

To expand coverage, Biden has proposed two major initiatives. In addition to the Medicare eligibility change, he wants Congress to approve a government-run health plan that people could buy into instead of purchasing coverage from insurance companies on their own or through the Obamacare marketplaces. Insurers helped beat back this “public option” initiative in 2009 during the congressional debate over the ACA.

The appeal of lowering Medicare eligibility to help those without insurance lies with leveraging a popular government program that has low administrative costs.

“It is hard to find a reform idea that is more popular than opening up Medicare” to people as young as 60, Oberlander said. He said early retirees would like the concept, as would employers, who could save on their health costs as workers gravitate to Medicare.

The eligibility age has been set at 65 since Medicare was created in 1965 as part of President Lyndon Johnson’s Great Society reform package. It was designed to coincide with the age when people at that time qualified for Social Security. Today, people generally qualify for early, reduced Social Security benefits at age 62, but full benefits depend on the year you were born, ranging from age 66 to 67.

While people can qualify on the basis of other criteria, such as having a disability or end-stage renal disease, 85% of the 57 million Medicare enrollees are in the program simply because they’re old enough.

Lowering the age to 60 could add as many as 23 million people to Medicare, according to an analysis by the consulting firm Avalere Health. It’s unclear, however, if everyone who would be eligible would sign up or if Biden would limit the expansion to the 1.7 million people in that age range who are uninsured and the 3.2 million who buy coverage on their own.

Avalere says 3.2 million people in that age group buy coverage on the individual market.

While the 60-to-65 group has the lowest uninsured rate (8%) among adults, it has the highest health costs and pays the highest rates for individual coverage, said Cristina Boccuti, director of health policy at West Health, a nonpartisan research group.

About 13 million of those between 60 and 65 have coverage through their employer, according to Avalere. While they would not have to drop coverage to join Medicare, they could possibly opt to pay to join the federal program and use it as a wraparound for their existing coverage. Medicare might then pick up costs for some services that the consumers would have to shoulder out of pocket.

Some 4 million people between 60 and 65 are enrolled in Medicaid, the state-federal health insurance program for low-income people. Shifting them to Medicare would make that their primary health insurer, a move that would save states money since they split Medicaid costs with the federal government.

Chris Pope, a senior fellow with the conservative Manhattan Institute, said getting health industry support, particularly from hospitals, will be vital for any health coverage expansion. “Hospitals are very aware about generous commercial rates being replaced by lower Medicare rates,” he said.

“Members of Congress, a lot of them are close to their hospitals and do not want to see them with a revenue hole,” he said.

President Barack Obama made a deal with the industry on the way to passing the ACA. In exchange for gaining millions of paying customers and lowering their uncompensated care by billions of dollars, the hospital industry agreed to give up future Medicare funds designed to help them cope with the uninsured. Showing the industry’s prowess on Capitol Hill, Congress has delayed those funding cuts for more than six years.

Jacob Hacker, a Yale University political scientist, noted that expanding Medicare would reduce the number of Americans who rely on employer-sponsored coverage. The pitfalls of the employer system were highlighted in 2020 as millions lost their jobs and their workplace health coverage.

Even if they can win the two Georgia seats and take control of the Senate with the vice president breaking any ties, Democrats would be unlikely to pass major legislation without GOP support — unless they are willing to jettison the long-standing filibuster rule so they can pass most legislation with a simple 51-vote majority instead of 60 votes.

Hacker said that slim margin would make it difficult for Democrats to deal with many health issues all at once.

“Congress is not good at parallel processing,” Hacker said, referring to handling multiple priorities at the same time. “And the window is relatively short.”

Even a solidly conservative Supreme Court could find a pretty easy path to preserve most of the Affordable Care Act — if it wants to.

The big picture: It’s too early to make any predictions about what the court will do, and no ACA lawsuit is ever entirely about the law. They have all been colored by the bitter political battles surrounding the ACA.

Even so, a handful of factors — the specifics of this case, the court’s recent precedents, even a few threads from Amy Coney Barrett’s Supreme Court confirmation hearings — can at least help draw a roadmap for a conservative ruling that would leave most of the ACA intact.

How it works: There are two steps to the current ACA case. First, the justices will have to decide whether the law’s individual mandate has become unconstitutional. If it has, they’ll then have to decide how many other provisions have to fall along with it.

The real action is in the second step — whether the mandate is “severable” from the rest of the law.

“If you picture severability being like a Jenga game — it’s kind of, if you pull one out, can you pull it out while it all stands? Or if you pull two out, will it still stand?” Barrett explained during Wednesday’s questioning.

“The presumption is always in favor of severability,” she said.

Severability is a question of congressional intent — whether Congress still would have passed the rest of a law if it knew it couldn’t have the piece the courts are striking down. And conservative judges make a point of relying only on a law’s text when determining congressional intent.

That should make the current case easy, the blue states defending the ACA argue: Congress zeroed out the mandate and left the rest of the law intact — a pretty clear sign that it intended for the rest of the law to operate in the absence of the mandate.

“It is abundantly clear that Congress wanted to keep the hundreds of other ACA provisions … without an enforceable minimum coverage provision, because that is the scheme Congress created,” Democratic attorneys general said in a brief.

The other side:The red states challenging the law, on the other hand, get further away from straight textualism.

They say the courts should instead look to Congress’ initial belief, when it passed the ACA in 2010, that the mandate was inextricably tied to protections for pre-existing conditions.

What we’re watching: Barrett acknowledged in this week’s hearings that the law has changed since it was first passed — a potentially encouraging sign, if you’re an ACA defender hoping the conservative justices will look at legislative text Congress wrote in 2017 instead of expert statements from 2010.

“Congress has amended the statute since” the 2012 Supreme Court ruling upholding the ACA, Barrett said Wednesday. “It has zeroed out the mandate, so now California v. Texas involves a different provision.”

A case from earlier this year— tied to another big-ticket Obama policy — might also help illuminate the current court’s approach to severability.

The court’s conservative majority ruled in June that the leadership structure of the Consumer Financial Protection Bureau was unconstitutional.

But a combination of four liberals and three conservatives then held that the whole agency didn’t have to be struck down because of it.

Yes, but: None of this means that the threat to the entire ACA, or to its protections for people with pre-existing conditions, has been exaggerated.

The Republican attorneys general who brought the case are asking the court to invalidate the entire statute. So is the Justice Department.

A federal judge ruled that the entire law had to fall. An appeals court couldn’t decide how much to strike, but said it would probably need to be more than just the mandate — and protections for pre-existing conditions would be next in line.

The bottom line: The ACA’s allies may not be able to save the remains of the individual mandate, but that’s a loss they can live with. And there is at least a clear path to a ruling, even from a conservative court, that would leave the rest of the law intact.

Two conservative justices on the Supreme Court appeared prepared to preserve at least some of the major components of ObamaCare, including its protections for people with preexisting conditions, as they heard arguments Tuesday in a suit challenging the law.

Chief Justice John Roberts and Justice Brett Kavanaugh seemed to express the view that if the court were to strike down the provision of the law mandating the purchase of health insurance, the rest of the law should be allowed to survive.

“Looking at our severability precedents, it does seem fairly clear that the proper remedy would be to sever the mandate provision and leave the rest of the act in place, the provisions regarding preexisting conditions and the rest,” Kavanaugh said.

The U.S. Supreme Court is set to hear a case questioning the legality of the ACA on Nov. 10.

Five things to know:

1. At the center of the case is whether the health law should be struck down. In a brief filed June 25 in Texas v. United States, the Trump administration argues the entire ACA is invalid because in December 2017, Congress eliminated the ACA’s tax penalty for failing to purchase health insurance. The administration argues the individual mandate is inseverable from the rest of the law and became unconstitutional when the tax penalty was eliminated; therefore, the entire health law should be struck down.

2. The administration’s brief was filed in support of a group of Republican-led states seeking to undo the ACA. Meanwhile, California Attorney General Xavier Becerra is leading a coalition of more Democratic states to defend the ACA before the Supreme Court.

3. The case goes before the Supreme Court days after media outlets projected Joe Biden as the next president of the U.S. President-elect Biden has said he seeks to expand government-subsidized insurance coverage and wants to the bring back the ACA’s tax penalty for failing to purchase health insurance, according to The Wall Street Journal. If a change regarding the tax penalty did occur, the publication notes that Republicans’ argument on severability would no longer apply.

4. The case also goes before the Supreme Court about two weeks after the Senate voted Oct. 26 to confirm Amy Coney Barrett to the Supreme Court. Ms. Barrett previously criticized Chief Justice John Roberts’ 2012 opinion sustaining the law’s individual mandate, The New York Times reported, but she said during her confirmation hearings in October that “the issue in the case is this doctrine of severability, and that’s not something that I have ever talked about with respect to the Affordable Care Act.”

5. According to the Journal, the Supreme Court is not expected to make a decision in the case until the end of June.

President-elect Joe Biden’s healthcare agenda: building on the ACA, value-based care, and bringing down drug prices.

In many ways, Joe Biden is promising a return to the Obama administration’s approach to healthcare:

Building on the Affordable Care Act (ACA) through incremental expansions in government-subsidized coverage

Continuing CMS’ progress toward value-based care

Bringing down drug prices

Supporting modernization of the FDA

Bolder ideas, such as developing a public option, resolving “surprise billing,” allowing for negotiation of drug prices by Medicare, handing power to a third party to help set prices for some life sciences products, and raising the corporate tax rate, could be more challenging to achieve without overwhelming majorities in both the House and the Senate.

Biden is likely to mount an intensified federal response to the COVID-19 pandemic, enlisting the Defense Production Act to compel companies to produce large quantities of tests and personal protective equipment as well as supporting ongoing deregulation around telehealth. The Biden administration also will likely return to global partnerships and groups such as the World Health Organization, especially in the area of vaccine development, production and distribution.

What can health industry executives expect from Biden’s healthcare proposals?

Broadly, healthcare executives can expect an administration with an expansionary agenda, looking to patch gaps in coverage for Americans, scrutinize proposed healthcare mergers and acquisitions more aggressively and use more of the government’s power to address the pandemic. Executives also can expect, in the event the ACA is struck down, moves by the Biden administration and Democratic lawmakers to develop a replacement. Healthcare executives should scenario plan for this unlikely yet potentially highly disruptive event, and plan for an administration marked by more certainty and continuity with the Obama years.

All healthcare organizations should prepare for the possibility that millions more Americans could gain insurance under Biden. His proposals, if enacted, would mean coverage for 97% of Americans, according to his campaign website. This could mean millions of new ACA customers for payers selling plans on the exchanges, millions of new Medicaid beneficiaries for managed care organizations, millions of newly insured patients for providers, and millions of covered customers for pharmaceutical and life sciences companies. The surge in insured consumers could mirror the swift uptake in the years following the passage of the ACA.

Biden’s plan to address the COVID-19 pandemic

Biden is expected to draw on his experience from H1N1 and the Ebola outbreaks to address the COVID-19 pandemic with a more active role for the federal government, which many Americans support. These actions could shore up the nation’s response in which the federal government largely served in a support role to local, state and private efforts.

Three notable exceptions have been the substantial federal funding for development of vaccines against the SARS-CoV-2 virus, Congress’ aid packages and the rapid deregulatory actions taken by the FDA and CMS to clear a path for medical products to be enlisted for the pandemic and for providers, in particular, to be able to respond to it.

Implications of Biden’s 2020 health agenda on healthcare payers, providers and pharmaceutical and life sciences companies

The US health system has been slowly transforming for years into a New Health Economy that is more consumer-oriented, digital, virtual, open to new players from outside the industry and focused on wellness and prevention. The COVID-19 pandemic has accelerated some of those trends. Once the dust from the election settles, companies that have invested in capabilities for growth and are moving forcefully toward the New Health Economy stand to gain disproportionately.

Shortages of clinicians and foreign medical students may continue to be an issue for a while

The Trump administration made limiting the flow of immigrants to the US a priority. The associated policy changes have the potential to exacerbate shortages of physicians, nurses and other healthcare workers, including medical students. These consequences have been aggravated by the pandemic, which dramatically curtailed travel into the US.

Healthcare organizations, especially rural ones heavily dependent on foreign-born employees, may find themselves competing fiercely for workers, paying higher salaries and having to rethink the structure of their workforces.

Providers should consider reengineering primary care teams to reflect the patients’ health status and preferences, along with the realities of the workforce on the ground and new opportunities in remote care.

Focus on modernizing the supply chain

Biden and lawmakers from both parties have been raising questions about life sciences’ supply chains. This focus has only intensified because of the pandemic and resulting shortages of personal protective equipment (PPE), pharmaceuticals, diagnostic tests and other medical products.

Investment in advanced analytics and cybersecurity could allow manufacturers to avoid disruptive stockouts and shortages, and deliver on the promise of the right treatment to the right patient at the right time in the right place.

Drug pricing needs a long-term strategy

Presidents and lawmakers have been talking about drug prices for decades; few truly meaningful actions have been implemented. Biden has made drug pricing reform a priority.

Drug manufacturers may need to start looking past the next quarter to create a new pricing strategy that maximizes access in local markets through the use of data and analytics to engage in more value-based pricing arrangements.

New financing models may help patients get access to drugs, such as subscription models that provide unlimited access to a therapy at a flat rate.

Companies that prepare now to establish performance metrics and data analytics tools to track patient outcomes will be well prepared to offer payers more sustainable payment models, such as mortgage or payment over time contracts, avoiding the sticker shock that comes with these treatments and improving uptake at launch.

Pharmaceutical and life sciences companies will likely have to continue to offer tools for consumers like co-pay calculators and use the contracting process where possible to minimize out-of-pocket costs, which can improve adherence rates and health outcomes.

View interoperability as an opportunity to embrace, not a threat to avoid or ignore

While the pandemic delayed many of the federal interoperability rule deadlines, payers and providers should use the extra time to plan strategically for an interoperable future.

Payers should review business partnerships in this new regulatory environment.

Digital health companies and new entrants may help organizations take advantage of the opportunities that achieving interoperability may present.

Companies should consider the legal risks and take steps to protect their reputations and relationships with customers by thinking through issues of consent and data privacy.

Health organizations should review their policies and consider whether they offer protections for customers under the new processes and what data security risks may emerge. They should also consider whether business associate agreements are due in more situations.

Plan for revitalized ACA exchanges and a booming Medicare Advantage market

The pandemic has thrown millions out of work, generating many new customers for ACA plans just as the incoming Biden administration plans to enrich subsidies, making more generous plans within reach of more Americans.

Payers in this market should consider how and where to expand their membership and appeal to those newly eligible for Medicare. Payers not in this market should consider partnerships or acquisitions as a quick way to enter the market, with the creation of a new Medicare Advantage plan as a slower but possibly less capital-intensive entry into this market.

Payers and health systems should use this opportunity to design more tailored plan options and consumer experiences to enhance margins and improve health outcomes.

Payers with cash from deferred care and low utilization due to the pandemic could turn to vertical integration with providers as a means of investing that cash in a manner that helps struggling providers in the short term while positioning payers to improve care and reduce its cost in the long term.

Under the Trump administration, the FDA has approved historic numbers of generic drugs, with the aim of making more affordable pharmaceuticals available to consumers. Despite increased FDA generics approvals, generics dispensed remain high but flat, according to HRI analysis of FDA data.

Pharmaceutical company stocks, on average, have climbed under the Trump administration, with a few notable dips due to presidential speeches criticizing the industry and the pandemic.

Providers have faced some revenue cuts, particularly in the 340B program, and many entered the pandemic in a relatively weak liquidity position. The pandemic has led to layoffs, pay cuts and even closures. HRI expects consolidation as the pandemic continues to curb the flow of patients seeking care in emergency departments, orthopedic surgeons’ offices, dermatology suites and more.

Lawmakers and politicians often use bold language, and propose bold solutions to problems, but the government and the industry itself resists sudden, dramatic change, even in the face of sudden, dramatic events such as a global pandemic. One notable exception to this would be a decision by the US Supreme Court to strike down the ACA, an event that would generate a great deal of uncertainty and disruption for Americans, the US health industry and employers.

The financial challenges caused by the COVID-19 pandemic have forced hundreds of hospitals across the nation to furlough, lay off or reduce pay for workers, and others have had to scale back services or close.

Lower patient volumes, canceled elective procedures and higher expenses tied to the pandemic have created a cash crunch for hospitals. U.S. hospitals are estimated to lose more than $323 billion this year, according to a report from the American Hospital Association. The total includes $120.5 billion in financial losses the AHA predicts hospitals will see from July to December.

Hospitals are taking a number of steps to offset financial damage. Executives, clinicians and other staff are taking pay cuts, capital projects are being put on hold, and some employees are losing their jobs. More than 260 hospitals and health systems furloughed workers this year and dozens of others have implemented layoffs.

Below are 11 hospitals and health systems that announced layoffs since Sept. 1, most of which were attributed to financial strain caused by the pandemic.

1. NorthBay Healthcare, a nonprofit health system based in Fairfield, Calif., is laying off 31 of its 2,863 employees as part of its pandemic recovery plan, the system announced Nov. 2.

2. Minneapolis-based Children’s Minnesota is laying off 150 employees, or about 3 percent of its workforce. Children’s Minnesota cited several reasons for the layoffs, including the financial hit from the COVID-19 pandemic. Affected employees will end their employment either Dec. 31 or March 31.

3. Brattleboro Retreat, a psychiatric and addiction treatment hospital in Vermont, notified 85 employees in late October that they would be laid off within 60 days.

4. Citing a need to offset financial losses, Minneapolis-basedM Health Fairview said it plans to downsize its hospital and clinic operations. As a result of the changes, 900 employees, about 3 percent of its 34,000-person workforce, will be laid off.

5. Lake Charles (La.) Memorial Health Systemlaid off 205 workers, or about 8 percent of its workforce, as a result of damage sustained from Hurricane Laura. The health system laid off employees at Moss Memorial Health Clinic and the Archer Institute, two facilities in Lake Charles that sustained damage from the hurricane.

6. Burlington, Mass.-based Wellforce laid off 232 employees as a result of operating losses linked to the COVID-19 pandemic. The health system, comprising Tufts Medical Center, Lowell General Hospital and MelroseWakefield Healthcare,experienced a drastic drop in patient volume earlier this year due to the suspension of outpatient visits and elective surgeries. In the nine months ended June 30, the health system reported a $32.2 million operating loss.

7. Baptist Health Floyd in New Albany, Ind., part of Louisville, Ky.-based Baptist Health, eliminated 36 positions. The hospital said the cuts, which primarily affected administrative and nonclinical roles, are due to restructuring that is “necessary to meet financial challenges compounded by COVID-19.”

8. Cincinnati-based UC Health laid off about 100 employees. The job cuts affected both clinical and non-clinical staff. A spokesperson for the health system said no physicians were laid off.

9. Mercy Iowa City(Iowa) announced in September that it will lay off 29 employees to address financial strain tied to the COVID-19 pandemic.

10. Springfield, Ill.-based Memorial Health Systemlaid off 143 employees, or about 1.5 percent of the five-hospital system’s workforce. The health system cited financial pressures tied to the pandemic as the reason for the layoffs.

11. Watertown, N.Y.-based Samaritan Healthannounced Sept. 8 that it laid off 51 employees and will make other cost-cutting moves to offset financial stress tied to the COVID-19 pandemic.