A few weeks ago The Commonwealth Fund, a philanthropic organization in New York City, which keeps tabs on health care trends, released an ominous study signaling that the bedrock of the U.S. health system is in trouble.

The study found that the employer insurance market, where millions of Americans have received good, affordable coverage since the end of World War II, could be in jeopardy. The continuing rise in the costs of medical care, and the insurance premiums to pay for it, may well cause employers to make cutbacks, leaving millions of workers uninsured or underinsured, often with no way to pay for their care and the prospect of debt for the rest of their lives.

Indeed the Fund revealed that 23% of adults in the U.S. are underinsured, meaning that though they were covered by health insurance, high deductibles and coinsurance made it difficult or impossible to pay for the care they needed.

“They have health plans that don’t provide affordable access to care,” said Sara Collins, senior adviser and vice president at the Fund. “They have out-of-pocket costs and deductibles that are high relative to their income.”

This predicament has forced many to assume medical debt or skip needed care. The Fund found that as many as one-third of people with chronic conditions like heart failure and diabetes reported they don’t take their medication or fill prescriptions because they cost too much.

Others did not go to a doctor when they were sick, skipping a recommended follow-up visit or test, and did not see a specialist when one was recommended. Nearly half of the respondents reported they did not get care for an ongoing condition because of the cost. Two out of five working-age adults who reported a delay or skipped care told researchers their health problem had gotten worse. Those findings belie the narrative, deployed when changes to the system are discussed, that America has the best health care in the world, and we dare not change it.

The seeds of today’s underinsurance predicament were planted in the 1990s when the system’s players decided remedies were needed to curb Americans’ appetite for medical interventions.

They devised managed care, with its HMOs, PPOs, insurance company approvals, and other restrictions that are with us today. But health care is far more expensive than it was in the ’90s, leaving patients to struggle to pay the higher prices, or, as the study shows, go without needed care.

Perhaps one of the study’s most striking findings is that a vast majority of underinsured workers had employer insurance plans, which over the decades had provided good coverage. Researchers concluded that recent cost containment measures were simply shifting more costs to workers through higher deductibles and coinsurance.

I checked in with Richard Master, the CEO of MCS Industries in Easton, Pennsylvania. We’ve talked over the years about the rising cost of health insurance for his 91 workers who make picture frames and wall decorations. This year, he was expecting a 5 to 6% increase in insurance rates.

A family plan now costs more than $39,000, he said, adding that “29% of people with employee plans are underinsured and have high out-of-pocket costs.”

To help reduce his own costs, he told me he has put in place a high-deductible plan and was setting up health saving accounts that allow him to give a sum of money to each worker to use for their medical expenses.

As health insurance premiums continue to rise, more employers will likely heap more of those rising costs onto workers, many of whom will inevitably have a tough time paying for them.

Every time there has been a hint in the air that maybe, just maybe, America might embrace a universal system like peer nations across the globe that offer health care to all their citizens, the special interests—doctors, hospitals, insurers, employers, and others that benefit financially from the current system have snuffed out any possibility that might happen, worried that such a system could affect their profits.

For as long as I can remember, the public has been told America has the best health care system in the world. Major holes in our system exposed by The Commonwealth Fund belie that assumption.

Tomorrow night, the Presidential candidates square off in Philadelphia. Per polling from last week by the New York Times-Siena, NBC News-Wall Street Journal, Ipsos-ABC News and CBS News, the two head into the debate neck and neck in what is being called the “chaos election.”

Polls also show the economy, abortion and immigration are the issues of most concern to voters. And large majorities express dissatisfaction with the direction the country is heading and concern about their household finances.

The healthcare system per se is not a major concern to voters this year, but its affordability is. Out-of-pocket costs for prescription drugs, insurance premiums and co-pays and deductibles for hospitals and physician services are considered unreasonable and inexplicably high. They contribute to public anxiety about their financial security alongside housing and food costs. And majorities think the government should do more by imposing price controls and limiting corporate consolidation.

That’s where we are heading into this debate. And here’s what we know for sure about the 90-minute production as it relates to health issues and policies:

Each candidate will rail against healthcare prices, costs, and consolidation taking special aim at price gouging by drug companies and corporate monopolies that limit competition for consumers.

Each will promise protections for abortion services: Trump will defer to states to arbitrate those rights while Harris will assert federal protection is necessary.

Each will opine to the Affordable Care Act’s future: Trump will promise its repeal replacing it “with something better” and Harris will promise its protection and expansion.

Each will promise increased access to behavioral health services as memories of last week’s 26-minute shooting tirade at Apalachee High School fade and the circumstances of Colt Gray’s mental collapse are studied.

And each will promise adequate funding for their health priorities based on the effectiveness of their proposed economic plans for which specifics are unavailable.

That’s it in all likelihood. They’re unlikely to wade into root causes of declining life expectancy in the U.S. or the complicated supply-chain and workforce dynamics of the industry. And the moderators are unlikely to ask probative questions like these to discover the candidate’s forethought on matters of significant long-term gravity…

What are the most important features of health systems in the world that deliver better results at lower costs to their citizens that could be effectively implemented in the U.S. system?

How should the U.S. allocate its spending to improve the overall health and well-being of the entire population?

How should the system be funded?

My take:

I will be watching along with an audience likely to exceed 60 million. Invariably, I will be frustrated by well-rehearsed “gotcha” lines used by each candidate to spark reaction from the other. And I will hope for more attention to healthcare and likely be disappointed.

Misinformation, disinformation and AI derived social media messaging are standard fare in winner-take-all politics.

When used in addressing health issues and policies, they’re effective because the public’s basic level of understanding of the health system is embarrassingly low: studies show 4 in 5 American’s confess to confusion citing the system’s complexity and, regrettably, the inadequacy of efforts to mitigate their ignorance is widely acknowledged.

Thus, terms like affordability, value, quality, not-for-profit healthcare and many others can be used liberally by politicians, trade groups and journalists without fear of challenge since they’re defined differently by every user.

Given the significance of healthcare to the economy (17.6% of the GDP),

the total workforce (18.6 million of the 164 million) and individual consumers and households (41% have outstanding medical debt and all fear financial ruin from surprise medical bills or an expensive health issue), it’s incumbent that health policy for the long-term sustainability of the health system be developed before the system collapses. The impetus for that effort must come from trade groups and policymakers willing to invest in meaningful deliberation.

The dust from this election cycle will settle for healthcare later this year and in early 2025. States are certain to play a bigger role in policymaking: the likely partisan impasse in Congress coupled with uncertainty about federal agency authority due to SCOTUS; Chevron ruling will disable major policy changes and leave much in limbo for the near-term.

Long-term, the system will proceed incrementally. Bigger players will fare OK and others will fail. I remain hopeful thoughtful leaders will address the near and long-term future with equal energy and attention.

Regrettably, the tyranny of the urgent owns the U.S. health system’s attention these days: its long-term destination is out-of-sight, out-of-mind to most. And the complexity of its short-term issues lend to magnification of misinformation, disinformation and public ignorance.

That’s why this debate will frustrate healthcare voters.

PS: Congress returns this week to tackle the October 1 deadline for passing 12 FY2025 appropriations bills thus avoiding a shutdown. It’s election season, so a continuing resolution to fund the government into 2025 will pass at the last minute so politicians can play partisan brinksmanship and enjoy media coverage through September. In the same period, the Fed will announce its much anticipated interest rate cut decision on the heals of growing fear of an economic slowdown. It’s a serious time for healthcare!

Cigna, my former employer, disclosed this morning that during the first seven months of this year, it spent $5 billion of the money it took from its health plan and pharmacy benefit customers to buy back shares of its own stock, a gimmick that rewards shareholders at the expense of those customers.

Cigna also disclosed that its revenues increased a stunning 25% – to $60.5 billion – during the second quarter of this year compared to the same period in 2023. Profits also grew, from $1.8 billion to $1.9 billion.

One of the ways Cigna made so much money was by purging health plan enrollees it decided were not profitable enough to meet Wall Street’s profit expectations.

Enrollment in its U.S. health plans fell by nearly half a million people – from 17.9 million to 17.4 million – over the past year. The company signaled to investors that it was more than OK with that decline, noting that it ran off those customers through “targeted pricing actions in certain geographies.” What that means is that Cigna increased premiums so much for those folks that they either found other insurers or joined the ranks of the uninsured.

It was an entirely different story in Cigna’s pharmacy benefit (PBM) business, which saw a 24% increase in total pharmacy customers. The vast majority of Cigna’s revenues now come from its role as one of the country’s largest middlemen in the pharmacy supply chain. Revenue from Cigna’s pharmacy operations totaled nearly $50 billion in the second quarter of this year, up from $38.2 billion last year. By contrast, revenue from its health plan business increased modestly, from $12.7 billion to $13.1 billion.

But by purging 478,000 men, women and children from its rolls, Cigna reported a profit margin of 9.2% for its health plan operations. That, folks, is exceedingly high in the health insurance business.

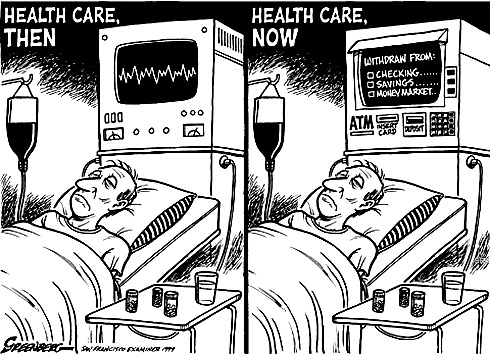

One way Cigna and the other industry giants can reward their shareholders so handsomely is by making their health plan and pharmacy customers pay more and more out of their own pockets before the insurers pay a dime.

The Affordable Care Act made it illegal for insurers to refuse to sell coverage to people with preexisting conditions or to set premiums based on someone’s health status.

But that law kept open a big back door that enables insurers like Cigna to make people with health problems pay huge sums of money for their care through deductibles and copayments. As a consequence, millions of Americans are walking away from the pharmacy counter without their medications, and many others who simply cannot live without their meds often wind up buried under a mountain of medical debt.

A growing number of bills have been or soon will be introduced by members of Congress to fulfill Biden’s pledge, but you can expect Cigna and other big insurers to insist that doing so will mean premiums will have to go up.

That’s bullshit.

It might mean that Cigna and the other giants might have to curtail their stock buyback programs and accept slimmer profit margins, but it does not mean premiums will have to go up.

Wall Street will howl if one of the tools insurers use to gouge their customers is taken away – just as investors are punishing Cigna today for the sin of not predicting even higher profits for the rest of the year –

but reducing out-of-pocket requirements would put a significant dent in the enormous and ongoing transfer of wealth by middlemen like Cigna from middle-class Americans, especially those struggling with health issues, to fat cat investors and corporate executives.

Over the weekend, President Biden called it quits and Democrats seemingly coalesced around Vice President Harris as the Party’s candidate for the White House. While speculation about her running mate swirls, the stakes for healthcare just got higher. Here’s why:

A GOP View of U.S. Healthcare

Republicans were mute on their plans for healthcare during last week’s nominating convention in Milwaukee. The RNC healthcare platform boils down to two aims: ‘protecting Medicare’ and ‘granting states oversight of abortion services. Promises to repeal and replace the Affordable Care Act, once the staple of GOP health policy, are long-gone as polls show the majority (even in Red states (like Texas and Florida) favor keeping it. The addition of Ohio Senator JD Vance to the ticket reinforces the party’s pro-capitalism, pro-competition, pro-states’ rights pitch.

To core Trump voters and right leaning Republicans, the healthcare industry is a juggernaut that’s over-regulated, wasteful and in need of discipline. Excesses in spending for illegal immigrant medical services ($8 billion in 2023), high priced drugs, lack of price transparency, increased out-of-pocket costs and insurer red tape stoke voter resentment. Healthcare, after all, is an industry that benefits from capitalism and market forces: its abuses and weaknesses should be corrected through private-sector innovation and pro-competition, pro-consumer policies.

A Dem View of Healthcare

By contrast, healthcare is more prominent in the Democrat’s platform as the party convenes for its convention in Chicago August 19. Women’s health and access to abortion, excess profitability by “corporate” drug manufacturers, hospitals and insurers, inadequate price transparency, uneven access and household affordability will be core themes in speeches and ads, with a promise to reverse the Dobb’s ruling by the Supreme Court punctuating every voter outreach.

Healthcare, to the Democratic-leaning voters is a right, not a privilege.

Its majority think it should be universally accessible, affordable, and comprehensive akin to Medicare. They believe the status quo isn’t working: the federal government should steward something better.

Here’s what we know for sure:

Foreign policy will be a secondary focus. The campaigns will credential their teams as world-savvy diplomats who seek peace and avoid conflicts. Nationalism vs. globalism will be key differentiator for the White House aspirants but domestic policies will be more important to most voters.

Healthcare reform will be a more significant theme in Campaign 2024 in races for the White House, U.S. Senate, U.S. House of Representatives and Governors. Dissatisfaction with the status quo and disappointment with its performance will be accentuated.

The White House campaigns will be hyper-negative and disinformation used widely (especially on healthcare issues). A prosecutorial tone is certain.

Given the consequence of the SCOTUS’ Chevron ruling limiting the role and scope of agency authority (HHS, CMS, FDA, CDC, et al), campaigns will feature proposed federal & state policy changes and potential Cabinet appointments in positioning their teams. Media speculation will swirl around ideologues mentioned as appointees while outside influencers will push for fresh faces and new ideas.

Consumer prices and inflation will be hot-button issues for pocketbook voters: the health industry, especially insurers, hospitals and drug companies, will be attacked for inattention to affordability.

Substantive changes in health policies and funding will be suspended until 2025 or later. Court decisions, Executive Orders from the White House/Governors, and appointments to Cabinet and health agency roles will be the stimuli for changes. Major legislative and regulatory policy shifts will become reality in 2026 and beyond. Temporary adjustments to physician pay, ‘blame and shame’ litigation and Congressional inquiries targeting high profile bad actors, excess executive compensation et al and state level referenda or executive actions (i.e. abortion coverage, price-containment councils, CON revisions et al) will increase.

Total healthcare spending, its role in the economy and a long-term vision for the entire system will not be discussed beneath platitudes and promises. Per the Congressional Budget Office, healthcare as a share of the U.S. GDP will increase from 17.6% today to 19.7% in 2032. Spending is forecast to increase 5.6% annually—higher than wages and overall inflation. But it’s too risky for most politicians to opine beyond acknowledgment that “they feel their pain.”

My take:

Regardless of the election outcome November 5, the U.S. healthcare industry will be under intense scrutiny in 2025 and beyond. It’s unavoidable.

Discontent is palpable. No sector in U.S. healthcare can afford complacency. And every stakeholder in the system faces threats that require new solutions and fresh voices.

Last week, 2 important economic reports were released that provide a retrospective and prospective assessment of the U.S. health economy:

The CBO National Health Expenditure Forecast to 2032:

“Health care spending growth is expected to outpace that of the gross domestic product (GDP) during the coming decade, resulting in a health share of GDP that reaches 19.7% by 2032 (up from 17.3% in 2022). National health expenditures are projected to have grown 7.5% in 2023, when the COVID-19 public health emergency ended. This reflects broad increases in the use of health care, which is associated with an estimated 93.1% of the population being insured that year… During 2027–32, personal health care price inflation and growth in the use of health care services and goods contribute to projected health spending that grows at a faster rate than the rest of the economy.”

The Congressional Budget Office forecast that from 2024 to 2032:

National Health Expenditures will increase 52.6%: $5.048 trillion (17.6% of GDP) to $7,705 trillion (19.7% of GDP) based on average annual growth of: +5.2% in 2024 increasing to +5.6% in 2032

NHE/Capita will increase 45.6%: from $15,054 in 2024 to $21,927 in 2032

Physician services spending will increase 51.2%: from $1006.5 trillion (19.9% of NHE) to $1522.1 trillion (19.7% of total NHE)

Hospital spending will increase 51.6%: from $1559.6 trillion (30.9% of total NHE) in 2024 to $2366.3 trillion (30.7% of total NHE) in 2032.

Prescription drug spending will increase 57.1%: from 463.6 billion (9.2% of total NHE) to 728.5 billion (9.4% of total NHE)

The net cost of insurance will increase 62.9%: from 328.2 billion (6.5% of total NHE) to 534.7 billion (6.9% of total NHE).

The U.S. Population will increase 4.9%: from 334.9 million in 2024 to 351.4 million in 2032.

The Bureau of Labor Statistics CPI Report for May 2024 and Last 12 Months (May 2023-May2024):

“The Consumer Price Index for All Urban Consumers (CPI-U) was unchanged in May on a seasonally adjusted basis, after rising 0.3% in April… Over the last 12 months, the all-items index increased 3.3% before seasonal adjustment. More than offsetting a decline in gasoline, the index for shelter rose in May, up 0.4% for the fourth consecutive month. The index for food increased 0.1% in May. … The index for all items less food and energy rose 0.2% in May, after rising 0.3 % the preceding month… The all-items index rose 3.3% for the 12 months ending May, a smaller increase than the 3.4% increase for the 12 months ending April. The all items less food and energy index rose 3.4 % over the last 12 months. The energy index increased 3.7%for the 12 months ending May. The food index increased 2.1%over the last year.

Medical care services, which represents 6.5% of the overall CPI, increased 3.1%–lower than the overall CPI. Key elements included in this category reflect wide variance: hospital and OTC prices exceeded the overall CPI while insurance, prescription drugs and physician services were lower.

Physicians’ services CPI (1.8% of total impact): LTM: +1.4%

Hospital services CPI (1.0% of total impact): LTM: +7.3%

Prescription drugs (.9% of total impact) LTM +2.4%

Over the Counter Products (.4% of total impact) LTM 5.9%

Health insurance (.6% of total) LTM -7.7%

Other categories of greater impact on the overall CPI than medical services are Shelter (36.1%), Commodities (18.6%), Food (13.4%), Energy (7.0%) and Transportation (6.5%).

Three key takeaways from these reports:

The health economy is big and getting bigger. But it’s less obvious to consumers in the prices they experience than to employers, state and federal government who fund the majority of its spending. Notably, OTC products are an exception: they’re a direct OOP expense for most consumers. To consumers, especially renters and young adults hoping to purchase homes, the escalating costs of housing have considerably more impact than health prices today but directly impact on their ability to afford coverage and services. Per Redfin, mortgage rates will hover at 6-7% through next year and rents will increase 10% or more.

Proportionate to National Health Expenditure growth, spending for hospitals and physician services will remain at current levels while spending for prescription drugs and health insurance will increase. That’s certain to increase attention to price controls and heighten tension between insurers and providers.

There’s scant evidence the value agenda aka value-based purchases, alternative payment models et al has lowered spending nor considered significant in forecasts.

The health economy is expanding above the overall rates of population growth, overall inflation and the U.S. economy. GDP. Its long-term sustainability is in question unless monetary policies enable other industries to grow proportionately and/or taxpayers agree to pay more for its services. These data confirm its unit costs and prices are problematic.

As Campaign 2024 heats up with the economy as its key issue, promises to contain health spending, impose price controls, limit consolidation and increase competition will be prominent.

Public sector actions

will likely feature state initiatives to lower cost and spend taxpayer money more effectively.

Private sector actions

will center on employer and insurer initiatives to increase out of pocket payments for enrollees and reduce their choices of providers.

Thus, these reports paint a cautionary picture for the health economy going forward. Each sector will feel cost-containment pressure and each will claim it is responding appropriately. Some actually will.

PS: The issue of tax exemptions for not-for-profit hospitals reared itself again last week.

The Committee for a Responsible Federal Budget—a conservative leaning think tank—issued a report arguing the exemption needs to be ended or cut. In response,

the American Hospital Association issued a testy reply claiming the report’s math misleading and motivation ill-conceived.

This issue is not going away: it requires objective analysis, fresh thinking and new voices. For a recap, see the Hospital Section below.

As campaigns for November elections gear up for early voting and Congress considers bipartisan reforms to limit consolidation and enhance competition in U.S. healthcare, prospective voters are sending a cleat message to would-be office holders:

Healthcare Affordability must be addressed directly, transparently and now.

Polling by Gallup, Kaiser Family Foundation and Pew have consistently shown healthcare affordability among top concerns to voters alongside inflation, immigration and access to abortion. It is higher among Democratic-leaning voters but represents the majority in every socio-economic cohort–young and old, low and middle income and households with/without health insurance coverage., urban and rural and so on.

It’s understandable: household economic security is declining: per the Federal Reserve’s latest household finances report:

72% of US adults say they are doing well financially (down from 78% in 2021)

54% say they have emergency savings to cover 3 months expenses ($400)—down from high of 59% in 2015.

69% say their finances deteriorated in 2023. They’re paying more for groceries, fuel, insurance premiums and childcare.

Renters absorbed a 10% increase last year and mortgage interest spike has put home ownership beyond reach for 6 in 10 households

Thus, household financial security is the issue and healthcare expenses play a key role. Drug prices, hospital consolidation, price transparency and corporate greed will get frequent recognition in candidate rhetoric. “Reform” will be promised. And each sector in the industry will offer solutions that place the blame on others.

Granted, the U.S. health system lacks a uniform definition of healthcare affordability. It’s a flaw. In the Affordable Care Act, it was framed in the context of an individual’s eligibility for government-subsidized insurance coverage (8.39% adjusted gross income for households between 100% and 400% of the federal poverty level). But a broader application to the entire population was overlooked. Nonetheless, economists, regulators and consumers recognize the central role healthcare affordability plays in household financial security.

Handicapping the major players potential to win the hearts and minds of voters about healthcare affordability is tricky:

Each major sector has seen the ranks of its membership decrease and the influence (and visibility) of its bigger players increase. They’re easy targets for industry critics.

Each sector is seeing private equity and non-traditional players play bigger roles. The healthcare landscape is expanding beyond the traditional players.

Each sector is struggling to make their cases for incremental reforms while employers, legislators and consumers want more. Bipartisan support for anything is a rarity: an exception is antipathy toward healthcare consolidation and lack of price transparency.

All recognize that affordability is complicated. Unit cost and price increases for goods and services are the culprit: excess utilization is secondary.

Against this backdrop, here’s a scorecard on the current state of preparedness as each navigates affordability going into Campaign 2024:

Sector

Advantages

Disadvantages

Handicap Score1=Unprepared to5=Well Prepared

Hospitals

Community presence (employer, safety net) Economic impact Influence in Congress Scale: 30% of spending + direct employment of 52% of physicians Access to capital

Lack of costs & price transparency Unit costs inflation due to wage, supply chain & admin Shifting demand for core services. Low entry barriers for key services Regulator headwind (state, federal). Operating, governing culture Value proposition erosion with employers, pre-Medicare populations Consumer orientation

3

Physicians

Consumer trust Influence in Congress Shared savings (Medicare) Essentiality Specialization Access to technology

Care continuity Inadequacy of primary care Disorganization (fragmentation) Value of shared savings to general population (beyond Medicare) Culture: change-averse (education, licensing performance measurement, et al) Data: costs, outcomes

2

Drug Manufacturers

Increasing product demand Influence in Congress Public trust in drug efficacy Insurance structure that limits consumer price sensitivity to OOP Potential for AI -enabled discovery, market access Access to private capital Congress’ constraint on PBMs

Unit cost escalation Lack of price transparency Growing disaffection for FDA Long-term Basic Research Funding State Price Control Momentum Market access Restrictive Formulary Growth Transparency in Distributor-PBM business relationships Public perception of corporate greed

2

Health Insurers

Availability of claims, cost data Employer tax exemptions Growing government market Plan design: OOP, provider access Public association: coverage = financial security Access to private capital

Escalating premiums Declining group market Growing regulatory scrutiny (consolidation, data protection) Tension with health systems Value proposition erosion among government, employers, consumers

4

Retail Health

Non-incumbrance of restrictive regulatory framework Consumer acceptance Breadth of product opportunities Access to private capital Opportunity for care management (i.e. CVS- Epic) Operational orientation to consumers (convenience, pricing, et al) Potential with employers,

Lack of access, coordination with needed specialty care Threat of regulatory restraint on growth Risks associated with care management models

3

The biggest, investor-owned health insurers own the advantage today. As in other sectors, they’re growing faster than their smaller peers and enjoy advantages of scale and private capital access to fund their growth. A handful of big players in the other sectors stand-out, but their affordability solutions are, to date, not readily active.

In each sector above, there is consensus that a fundamental change in the structure, function and oversight of the U.S. health is eminent. In all, tribalism is an issue: publicly-owned, not for profits vs. investor-owned, independent vs. affiliated, big vs. small and so on.

Getting consensus to address affordability head on is hard, so not much is done by the sectors themselves. And none is approaching the solution in its necessary context—the financial security of a households facing unprecedented pressures to make ends meet. In all likelihood, the bigger, more prominent organizations in their ranks of these sectors will deliver affordability solutions well-above the lowest common denominators that are comfortable for most Thus, health care affordability will be associated with organizational brands and differentiated services, not the sectors from which their trace their origins. And it will be based on specified utilization, costs, outcome and spending guarantees to consumers and employers that are reasonable and transparent.

Abuses by payers are myriad, but these five areas could bear the most fruit for federal antitrust investigators.

Earlier this month, the U.S. Department of Justice announced it has haunched an investigation into “issues regarding payer-provider consolidation” along with other problems associated with mergers and acquisitions in health care. This is significant. For years Washington has trained its oversight authority on pharmaceutical manufacturers, private equity investments in health care and, more recently, pharmacy benefits managers controlled by big insurers. This has held bad actors like Martin Skhreli and Steward Healthcare accountable. But, it has also let insurers grow ever larger, under the radar.

No longer.

This task force will specifically evaluate the following, as an example: “A health insurance company buys several medical practices that compete with each other. It also prohibits its medical practices from contracting with rival health insurance companies.” The government will also dig into “anticompetitive uses of health care data,” “preventing transparency,” “price fixing,” and other areas that could drag nefarious activities of insurers into the spotlight.

I applaud the Department of Justice’s continued focus on these issues, building on the Department’s action announced in February to begin an antitrust investigation into UnitedHealth Group. (If you haven’t read the piece we published in February on UnitedHealth’s self-dealing that helped lead DOJ to open that antitrust inquiry, you can do so here.) The following are a few areas of low-hanging fruit that I hope the task force will focus on as they consider the impact insurers’ ongoing vertical integration has had on the overall health care system.

1. Insurers purchasing physician practices

Once a low-profile issue, Congress and the Biden administration alike have increasingly turned their focus to insurance companies – often referred to as payers – that now own and operate physician practices and clinics – those being paid. Even for someone without a law degree, it is easy to see the conflict this creates, particularly at scale.

There is the oft-cited statistic that UnitedHealth has said that through its Optum division, the company employs or otherwise controls about 10 percent of doctors in the U.S. – around 130,000 physicians and other practitioners in 16 states. This prompted me to take a closer look at publicly available information on the number of doctors employed by other insurers to get a better handle on how much control of physician practices payers now have.

It is difficult to put a percentage on physicians employed by each insurer, but it is clear that the others are following UnitedHealth’s lead. CVS/Aetna purchased Signify Health in 2023, adding 10,000 clinicians to its portfolio. The company says it supports “more than 40,000 physicians, pharmacists, nurses and nurse practitioners.”

Clearly taking a page out of UnitedHealth’s playbook, Elevance (formerly Anthem), which owns Blue Cross Blue Shield plans in 14 states announced last month a “strategic partnership” with 900 providers across several states. Elevance did not disclose the terms of the deal except to say it, “will primarily be through a combination of cash and our equity interest in certain care delivery and enablement assets of Carelon Health.”

As insurers have acquired physician practices, they also have created a rinse-and-repeat strategy associated with kicking physicians they don’t own out of network, and in some cases targeting those same practices for acquisition. Aetna and Humana recently told investors they will be reviewing their networks of physicians, signaling they’ll soon be further narrowing their networks. A good question for this task force: when insurers review those contracts with doctors, do they ever kick the doctors they employ out of network? (Doubtful.) This could specifically draw attention from the task force’s focus on “health care contract language and other practices that restrict competition,” such as contract provisions that require or encourage patients to seek care from doctors directly employed or closely controlled by patients’ insurers.

Additionally, UnitedHealth CEO Andrew Witty recently told analysts, “As I think you see some of the funding changes play out across the — across the next few years, I suspect that may also create new opportunities for us as different companies assess their positions.” My translation:UnitedHealth’s burdensome business practices and the way it shortchanges doctors (those “funding changes” he referenced) contribute to the financial distress that is forcing many health care providers to “assess their positions.”

As the task force continues to consider the impact of private equity in health care monopolies, transactions like this one should receive equal consideration for their lack of transparency and overall impact on market consolidation.

2. Co-mingling of middlemen

I have watched with interest for over the past year as both Democrats and Republicans in Washington increasingly trained their fire on pharmacy benefit managers. The natural next area of focus in that space, which this new task force could advance, should be around how the

three PBMs that control 80 percent of market share are all combined with health insurance companies – namely CVS/Aetna (Caremark), UnitedHealth (Optum Rx), and Cigna (Express Scripts).

An important, and politically popular, area where this consolidation has played out is in the squeeze placed on small, independent pharmacists across the country. More than 300 community pharmacies have closed in the past year alone, out of an inability to operate or push back on unfair margins pushed by these PBM-insurer monopolies. As we have written here, the fees these PBMs charge have increased more than 100,000 percent over the past decade, and are quietly contributing significantly to the profits of the largest health insurers.

We still have little insight into how these business lines interact with each other, and the ultimate impact that has on patients. Given the enormous influence just three insurance companies have over what prescriptions Americans can receive, and how much should be paid for each prescription, the task force would do well to focus on what insurers and PBMs are doing behind the scenes to maximize profits and limit patient access to prescription drugs. It’s already gaining traction on Capitol Hill, with one Congressman recently saying, “I’ll continue to bust this up … this vertical integration in health care.”

3. Prior authorization requests

CVS/Aetna shares were hammered after the company reported a significant increase in payment of Medicare Advantage claims during the first three month is of this year. Expect all insurers to notice. And as they have seen their forecasts fall short of Wall Street’s expectations – particularly because of increasing scrutiny in Washington of Medicare Advantage – these corporations will look to increase their already aggressive use of prior authorization to limit claims payments.

It is not as though insurers make seeking the care you need easy. Far from it. Prior authorization has become “medical injustice disguised as paperwork,” as the New York Times said in a recent, excellent video detailing the widespread nature of this profiteering practice.

While not a stated direct focus of this task force, the increased impact of prior authorization in care delivery is a direct outgrowth of a few large health insurers effectively controlling the marketplace. As insurers directly employ more doctors and enroll more Americans in their plans, they can use prior authorization to increasingly determine whether a patient can get care, period.

Scrutiny in this space could add momentum to increasing activity in state legislatures and Washington to rein in excessive prior authorization. As of early March, nine states and the District of Columbia had passed bills to limit how far insurers could go with prior authorization. And earlier this year, the Centers for Medicare and Medicaid released a final rule that is expected to save physicians $15 billion over the next decade by putting limits on insurer prior authorization tactics.

4. Rising out-of-pocket costs

Regular readers of this newsletter know one of my crusades is to ensure folks who pay good money for health insurance – out of their paychecks or through their tax dollars – can use it when they need it. It was a big win earlier this year for the Lower Out of Pockets Now coalition (which I lead) when President Biden called for a cap on prescription drug out-of-pocket costs of $2,000 annually for everybody, not just Medicare beneficiaries.

If there was true competition and real consumer choice in health insurance, payers wouldn’t be able to get away with increasingly shifting patients into high-deductible plans. But the fact that a few big players control the health insurance market has allowed the oligopoly of payers to do just that, with ever-rising deductibles alongside ever-rising premiums.

The task force’s focus on price fixing, collusion, and transparency in health care costs will, I hope, include some focus on how insurers use their size and clout to drive up out-of-pocket costs and premiums simultaneously – with little recourse to employers or their employees.

5. Implementing crystal clear laws and rules in health care

You know you’re a monopoly or close to it when you can pretty much do whatever you want and get away with it. Look no further than America’s health insurance companies and implementation of the No Surprises Act.

As I wrote earlier this year, Congress and CMS have been clear about how out-of-network hospital bills should be negotiated between insurers and physicians. Yet in case after case, including many that have become the basis of lawsuits, insurers are clearly flouting the Act passed by Congress and the rules promulgated by CMS. Payers are doing this, doctors have said, simply because of their size and ability to weather criticism from physicians, regulators, and the courts – while doctors struggle to pay their bills with significant payments still owed pending out-of-network negotiations with insurers.

One would hope, at a minimum, this task force, focused on rooting out the ills of monopolies, would document how insurers are well aware of how they are supposed to implement legislation like the No Surprises Act, but flout it anyway.

ALSO: We’re premiering our Magic Translation Box to help you decipher corporate jargon and understand what’s coming down the pike.

If you are enrolled in an Aetna Medicare Advantage plan, now might be a good time to get more nervous than usual.

Wall Street is not happy with Aetna’s parent, CVS Health. In response to that unhappiness, triggered by the company’s admission that it has been paying more claims than usual, CVS execs have promised to do whatever it takes to get profit margins back to a level investors deem suitable.

That means the odds have increased that Aetna will refuse to cover the treatments and medications your doctor says you need. It also means CVS/Aetna likely will increase your premiums next year and might dump you altogether. The company has a long history of doing just that, as you’ll see below.

Medicare Advantage companies in general are facing what Wall Street financial analysts call headwinds, and those winds are now coming from several sources: increased Congressional scrutiny of insurers’ business practices, Biden administration efforts to end years of overpayments that have cost taxpayers hundreds of billions of dollars, enrollee discontent, and a gathering storm of negative press.

To understand the pressures CVS CEO Karen Lynch and her C-Suite team are under to satisfy the company’s remaining shareholders (many have fled), you need to know and understand what they told them in recent weeks–and what she undoubtedly will have to say again, with conviction, this coming Thursday when CVS holds its annual meeting of shareholders. You can be certain Lynch’s staff has prepared a binder chock full of the rudest questions she could face from rich folks (mostly institutional investors) who’ve become a little less rich in recent months as the golden calf calf called Medicare Advantage has lost some of its luster. (My former colleagues and I used to put together such a CEO-briefing binder during my Cigna days, which coincided with Lynch’s years at Cigna.)

To help with that understanding, we’re introducing the HEALTH CARE un-covered Magic Translation Box (MTB). We’ll fire it up occasionally to decipher the coded language executives use when they have to deal with analysts and investors in a public setting. We’ll start with what Lynch and her team told analysts on May 1 when CVS announced first-quarter 2024 results that caused a stampede at the New York Stock Exchange.

Lynch: We recently received the final 2025 (Medicare Advantage) rate notice (from the Center for Medicare and Medicaid Services), and when combined with the Part D changes prescribed by the Inflation Reduction Act, we believe the rate is insufficient. This update will result in significant added disruption to benefit levels and choice for seniors across the country. While we strive to deliver benefit stability to seniors, we will be adjusting plan-level benefits and exiting counties as we construct our bid for 2025. We are committed to improving margins.

Magic Translation Box: Can you believe it? CMS did not bend to industry pressure to pay MA plans what we demanded for next year. We only got a modest increase, not enough, in our opinion, to protect our profit margins. To make matters worse, starting next year we won’t be able to make people enrolled in Medicare prescription drug plans (Part D) pay more than $2,000 out of their own pockets, thanks to the Inflation Reduction Act President Biden signed in 2022. So, to make sure you, our most important stakeholder, once again have a good return on your investment, we will notify CMS next month that we will slash the value of Medicare Advantage plans by reducing or eliminating some benefits, like dental, hearing and vision, that attract people to MA plans in the first place. And, for good measure, we’ll be dumping Medicare Advantage enrollees who live in zip codes where we can’t make as much money as we’d like. For them: too bad, so sad. For you: more money in your bank account. And for extra good measure, to keep seniors from blaming greedy us for what we have in store for them, our industry will be bankrolling dark money ads to persuade voters that Biden and the Democrats are the bad guys cutting Medicare.

Later during CVS’s earnings call, CFO Thomas Cowhey reiterated Lynch’s remarks about reducing benefits.

Cowhey:So, we’ve given you all the pieces to kind of understand why we think it (Medicare Advantage) will lose a significant amount of money this year. But as you think about improvement there, obviously there’s a lot of work that we still need to do to understand what benefits we’re going to adjust and what ones we can and can’t…To the extent that we don’t believe we can credibly recapture margin in a reasonable period of time, we will exit those counties…(And) as we’ve all mentioned we’re going to be taking significant pricing actions and really it’s going to depend on what our competitors do.

Magic Translation Box: We’re under the gun to figure this out because we have to notify CMS by June 3 how much we will increase Medicare Advantage premiums and cut benefits next year and which counties we’ll abandon altogether. We’ll also be watching what our competitors do, but we know from what they’ve been telling you guys that they, too, will be dumping enrollees, hiking premiums and slashing benefits.

To make sure investors couldn’t miss what they were saying, Lynch jumped back into the conversation to make clear they knew they were #1 in her book:

Lynch: I’m just going to reiterate what I said in my prepared remarks. (You can bet what follows were prepared, too.) We are committed to improving margin in Medicare Advantage [emphasis added] and we will do so by pricing for the expected trends. We will do so by adjusting benefits and exiting service counties. And we are committed to doing that.

Magic Translation Box: Have I made myself clear? We will do whatever it takes to deliver the profits you expect. We will keep a closer eye on how much care people are trying to get and we’ll swing into action faster next time if we see evidence of an uptick. There will be carnage, but you guys rule. You mean a lot more to us than those old and disabled people who don’t have nearly as much money as you do in their bank accounts.

This will not be the first time Aetna has dumped health plan enrollees who were a drain on profits. In 2000, when Medicare Advantage was called Medicare+Choice, Aetna notified the Clinton administration it would stop offering Medicare plans in 14 states, affecting 355,000 people, more than half of Aetna’s total Medicare enrollment at the time. Other companies, including Cigna, did the same thing. My team and I wrote a press release to announce that Cigna would be bailing from almost all the markets where we sold private Medicare plans.

We of course blamed the federal government (i.e., the Democrats) for being the skinflints that made it necessary to bail. Our CEO at the time, Ed Hanway, said the government just couldn’t be relied upon to be a reliable “partner.”

Back then, just a relatively small percentage of Medicare beneficiaries were in private plans. Today, more than half of Medicare-eligible Americans are enrolled in a Medicare Advantage plan, which means the disruption could be much worse this time. Some people in counties where Aetna and other companies stop offering plans likely will not find a replacement plan with the same provider network, premiums and benefits.

But in most places, those who get dumped will be stuck in the volatile, often nightmarish Medicare Advantage world, unable to return to traditional Medicare and buy a Medicare supplement policy to cover their out-of-pocket obligations.

That’s because in all but a handful of states, seniors and disabled people will not be able to buy a Medicare supplement policy as cheaply as they could within six months of becoming eligible for Medicare benefits. After that, Medicare supplement insurers, including Aetna, get their underwriters involved. If your health isn’t excellent, expect to pay a king’s ransom for a Medigap policy.