It may be time to update your inflation narrative.

The ultra-hot readings that defined the first half of 2022 appear to be firmly in the rearview mirror, improving the odds that price pressures can dissipate further without excessive economic pain.

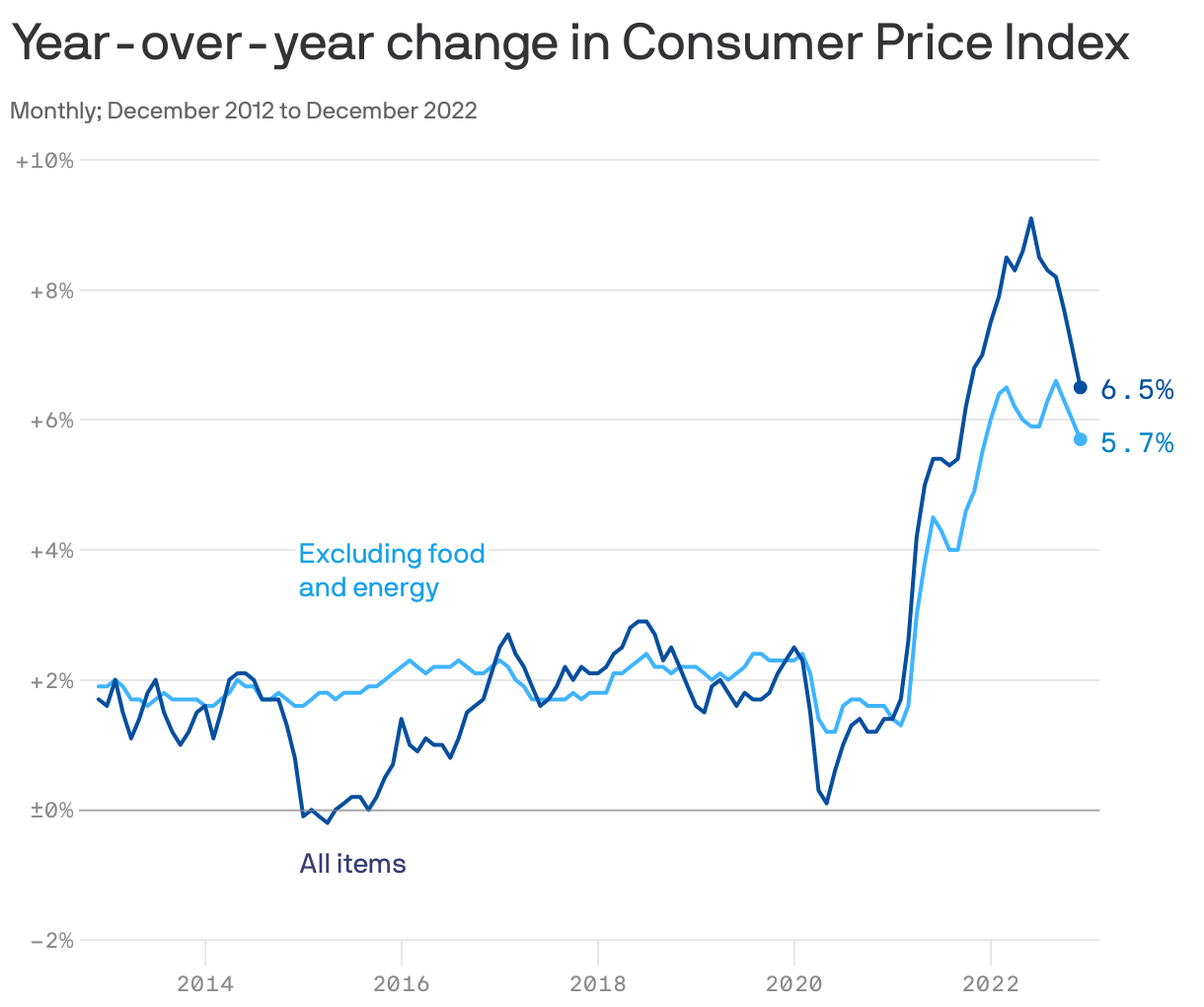

- That’s the key takeaway from the December Consumer Price Index released this morning, which confirmed notably cooler inflation as the year came to a close.

Why it matters:

The nation’s inflation problem isn’t over, but so far inflation is slowing while the job market is still healthy, an enviable combination.

- As Princeton economist Alan Blinder put it in an op-ed last week, inflation was “vastly lower” in the second half of 2022 than the first; yet, “hardly anyone seems to have noticed.”

By the numbers:

In the final three months of 2022, core inflation (which excludes food and fuel costs) came in at an annualized 3.1% — higher than the Fed aims for, but hardly crisis levels. In the second quarter of the year, that number was 7.9%.

- It’s a stunning decline, occurring alongside a labor market that by nearly all measures is still flourishing. Just this morning, the Labor Department announced that jobless claims fell to an ultra-low 205,000 last week.

State of play:

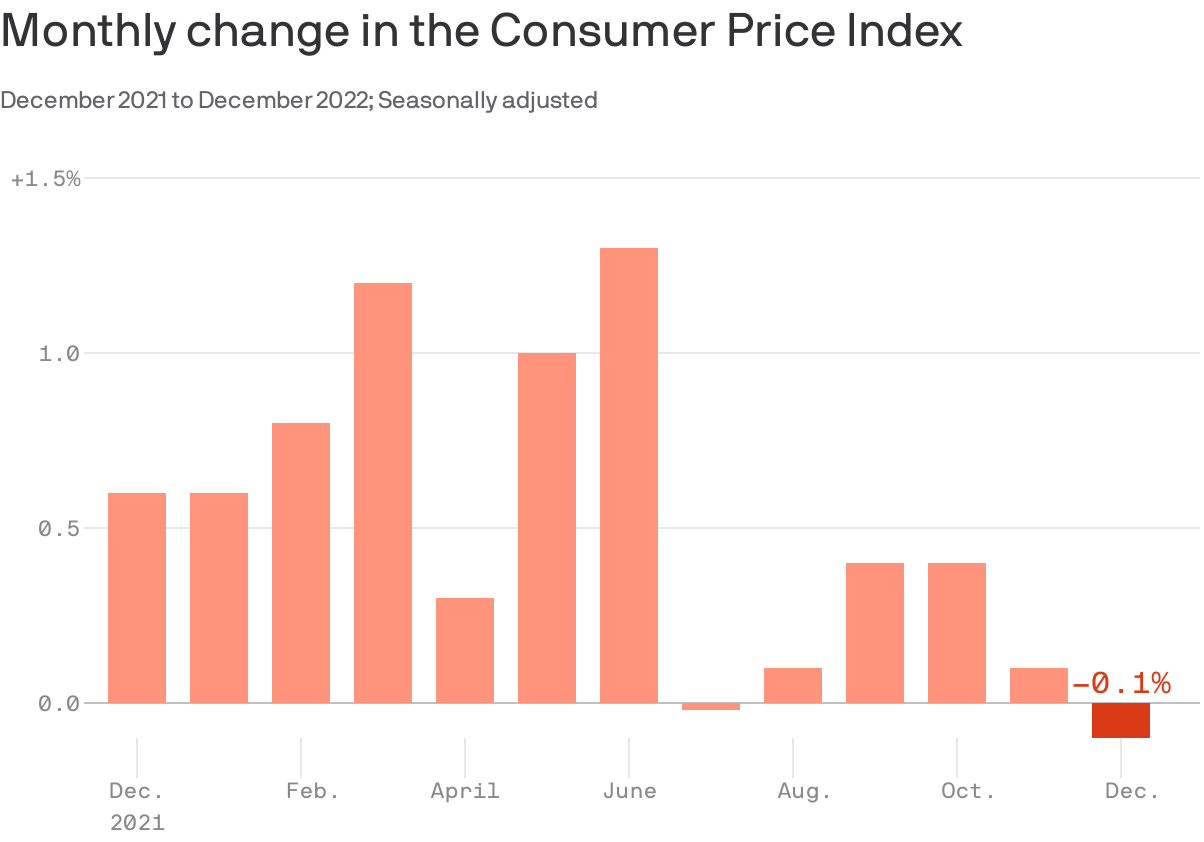

Grocery prices rose 1.1% in the final three months of the year, an uncomfortably high rate, but not as extreme as the rates seen earlier in 2022.

- Gasoline prices, pushed up by Russia’s invasion of Ukraine, were once the crucial reason why inflation was rising. In recent months, the opposite has been true: December pump prices slid 9.4%, helping drag the overall index into negative territory.

- Disinflation was at work for many other goods, including used cars (-2.5%) and new vehicles (-0.1%) where prices have reversed, helped by easing supply chain bottlenecks.

- Shelter costs pushed inflation upward, surging 0.8% in December. But private-sector data points to rents on new leases falling in recent months, which would only filter into the CPI data over time. That makes for a more benign inflation outlook in 2023.

What to watch:

That’s not to say there aren’t risks ahead. The war in Ukraine is ongoing, and another energy price shock could occur.

- The Fed has also focused in on the services sector, where price increases have slowed from last summer but remain frothy. The risk is that business costs associated with the still-tight labor market (like higher wages) will pass through to prices for consumers.

The bottom line:

Inflation will still be a worry in 2023, but much less so than it seemed a few months ago.