One in every five workers is now collecting unemployment benefits as the country struggles to get the COVID-19 outbreak under control. A recent Families USA study estimates a quarter of the 21.9M workers that were furloughed or laid off between February and May lost their health insurance. And the payer mix will continue to change as the pandemic wears on.

The graphic below highlights a study from consultancy Oliver Wyman, looking at the impact of rising unemployment (at 15, 20 and 30 percent) on insurance coverage. With each five to ten percent rise in unemployment, the commercially insured population decreases by three to five percent. Those who lose employer-sponsored insurance either remain uninsured, buy coverage on the Obamacare marketplaces, or qualify for Medicaid.

Surprisingly, Washington State and California are reporting little to no enrollment growth in Medicaid programs thus far. Experts point to lack of outreach and consumer awareness as key contributors to the slow growth—but Medicaid enrollment will likely begin to rise quickly in coming months as temporary furloughs convert to more permanent layoffs.

The right side of the graphic spotlights the growing number of uninsured individuals in those states with the highest uninsured rates. The previous record for the largest increase in uninsured adults was between 2008 and 2009, when nearly 4M lost coverage.The current pandemic-driven increase has crushed that record by 39 percent.

On average, states are seeing uninsured populations increase by two percent, with some as high as five percent. And the two states with the highest uninsured rates, Florida and Texas, are also dealing with the largest surge in COVID-19 cases and deaths. The ranks of the uninsured will continue to climb as states reimpose shutdowns, government assistance ends, and layoffs grow.

This perfect storm of a shift in payer mix, the impending insolvency of Medicare and the inability of states to absorb the growing costs of Medicaid represent a tsunami of challenges.

With COVID-19 there has been unprecedented stress placed upon the healthcare system. The human and financial toll of the current crisis has been extraordinary. Yet, little attention has been focused on the impact of this virus on the viability of our healthcare financing system.

Three significant shifts in healthcare financing are occurring as a result of the pandemic’s economic impact. First, as a result of job losses, there will be a shift in commercial insurance to government-funded insurance programs. Second, revenue for funding Medicare, based on payroll taxes, will be significantly decreased. Finally, states will have less tax revenue to pay for Medicaid, threatening the viability of this program as well.

More than 30 million Americans have filed for unemployment since the start of the COVID-19 pandemic. According to a recent report, about 27 million people may lose their employer-sponsored insurance.

This will result in millions of people seeking coverage through Medicaid programs, the individual marketplace or simply becoming uninsured. Healthcare providers have relied upon margins from commercial insurance to offset costs from poorer reimbursing government funded programs and uncompensated care.

With more than 156 million Americans receiving employer sponsored insurance at the start of this year, and given recent projected job losses, providers may see a 17% shift in payer mix. The reliance on commercial insurance and cost shifting has become a necessary way for providers to financially sustain operations.

With a 35% margin with commercial insurance compared to Medicare, a 17% shift in payer mix on a trillion dollar spend would result in a substantial reduction in financial resources available to hospitals.

Almost half of healthcare expenditures already come from government programs. Medicare, the largest of these programs, is principally supported by taxes on payroll and social security benefits. With COVID-related job losses there will be a corresponding reduction in payroll tax revenues to the Medicare system. Reports from the Congressional Research Service submitted to Congress in May, with data used prior to COVID-19, projected that Medicare would become insolvent in 2026.

Analyses performed show that there will be a gap in Medicare revenues during the next three years (from the pre-COVID projections) of close to $150 billion. The result is that Medicare will become insolvent as early as 2022. Even by applying more conservative projections, such as recovering all job losses by the end of 2020 and payroll tax revenue holding steady at pre-COVID levels, Medicare still becomes insolvent in 2023.

State revenues, too, will be under real pressure with reduced tax revenues resulting from the current economic downturn. Medicaid programs are supported in part by federal funds, but also from general funds from the state.

On average, states are projecting about a 10% reduction in revenues in 2020, rising to almost a 25% reduction in 2021. Even without considering the growth in Medicaid enrollment hitting states, this reduced tax revenue will make sustaining current Medicaid program funding increasingly difficult.

This perfect storm of a shift in payer mix, the impending insolvency of Medicare by 2022 and the inability of states to absorb the growing costs of Medicaid represent a tsunami of challenges for the health system. Looking at this new reality, it is clear that our system for financing healthcare is severely broken and we must identify solutions to sustain access to medical care for our citizens.

This will be a challenge of a generation and we will need strength, courage and bold ideas to get through this. Pandemics have a way of changing a society’s political, economic and sociologic outlooks, and COVID-19 will be no different.

If there’s one state in the U.S. where you don’t want a pandemic, it’s Florida. Florida is an international crossroads, a magnet for tourists and retirees, and its population is older, sicker and more likely to be exposed to COVID-19 on the job than the country as a whole.

When the coronavirus struck, the conditions there made it a perfect storm.

Despite these strains, Disney World reopened two theme parks on July 11, and Florida Gov. Ron DeSantis announced schools would reopen in August. The governor had shut down alcohol sales in bars in late June as case numbers skyrocketed, but he hasn’t made face masks mandatory or moved to shut down other businesses where the virus can easily spread.

As public healthresearchers, we have been studying how states respond to the pandemic. Florida stands out, both for its absence of statewide policies that could have stemmed the spread of COVID-19 and for some unique challenges that make those policies both more necessary and more difficult to implement than in many other states.

The challenges of economic pressures

Florida is one of nine states with no income tax on wages, so its tax base relies heavily on tourism and property in its high-density coastal areas. That puts more pressure on the government to keep businesses and social venues open longer and reopen them faster after shutdowns.

If you look closely at Florida’s economy, its vulnerabilities to the pandemic become evident.

The state depends on international trade, tourism and agriculture – sectors that rely heavily on lower-wage, often seasonal, workers. These workers can’t do their jobs from home, and they face financial barriers to getting tested, unless it’s provided through their employer or government testing sites. They also struggle with health care – Florida has a higher-than-average rate of people without health insurance, and it chose not to expand Medicaid.

In the tourism industry, even young, healthy employees typically at lower risk from COVID-19 can unknowingly spread the virus to visitors or vice versa. The tourism industry also encourages crowded bar and club scenes, where the governor has blamed young people for spreading the coronavirus.

The past few weeks have been emblematic of the economic battles facing a state that depends on tourism for both jobs and state revenues.

Even as the public health risks were quickly rising, businesses continued to open their doors. Major cruise lines planned to resume their itineraries in the fall. A note on the Universal Studios website read: “Exposure to COVID-19 is an inherent risk in any public location where people are present; we cannot guarantee you will not be exposed during your visit.”

The Governor’s Re-open Florida Taskforce issued guidelines in late April meant to lower the state’s coronavirus risk, but those guidelines have been largely ignored in practice.

No county in Florida has reduced cases or maintained the health care resources recommended by the task force. The data needed to fully assess progress are also questionable, given a recent scandal regarding the state data’s accuracy, availability and transparency.

Florida’s patchwork of local rules also makes it hard to contain the virus’s spread.

With no statewide mask rules or plans to reverse reopening, other than for bars, communities and businesses have taken their own actions to implement public health precautions. The result is varying mask ordinances and restrictions on large gatherings in some cities but not those surrounding them. Though the Florida Department of Health has issued an advisory recommending face coverings, some local areas have voted down mask mandates.

More warning signs ahead

Late summer and fall will bring new challenges for Florida in terms of the virus’s spread and the state’s response to it.

That’s when Florida’s risk of hurricanes grows, and while Floridians are well-versed in hurricane preparedness, storm shelters aren’t designed for social distancing and will need careful plans for protecting nursing home residents. Storm cleanup could mean lots of people working in close proximity while protective gear is in short supply.

If Florida’s schools reopen fully, the risk of the virus rapidly spreading to teachers, parents and children who are more vulnerable is a real concern being weighed against the costs of keeping schools closed.

Colleges that reopen to classes and sporting events also raise the risk of spreading the virus in Florida communities. And the possible return of retirees who spend their winters in Florida would increase the high-risk population by late fall. One in five Florida residents is over age 65, giving the state one of the nation’s oldest populations – a risk factor, along with chronic illnesses, for severe symptoms with COVID-19.

Florida is also a battleground state for the upcoming presidential election, and that’s likely to mean campaign rallies and more close contact. The Republican National Convention was moved to Jacksonville after President Donald Trump complained that North Carolina might not let the GOP fill a Charlotte arena to capacity due to coronavirus restrictions. Florida organizers recently said they were considering holding parts of the convention outdoors.

The high number of cases being reported in Florida will lead to even more hospitalizations and fatalities in coming weeks and months. Without clear public health messages and precautions implemented and enforced across the state, the coronavirus forecast for the Sunshine State will remain stormy.

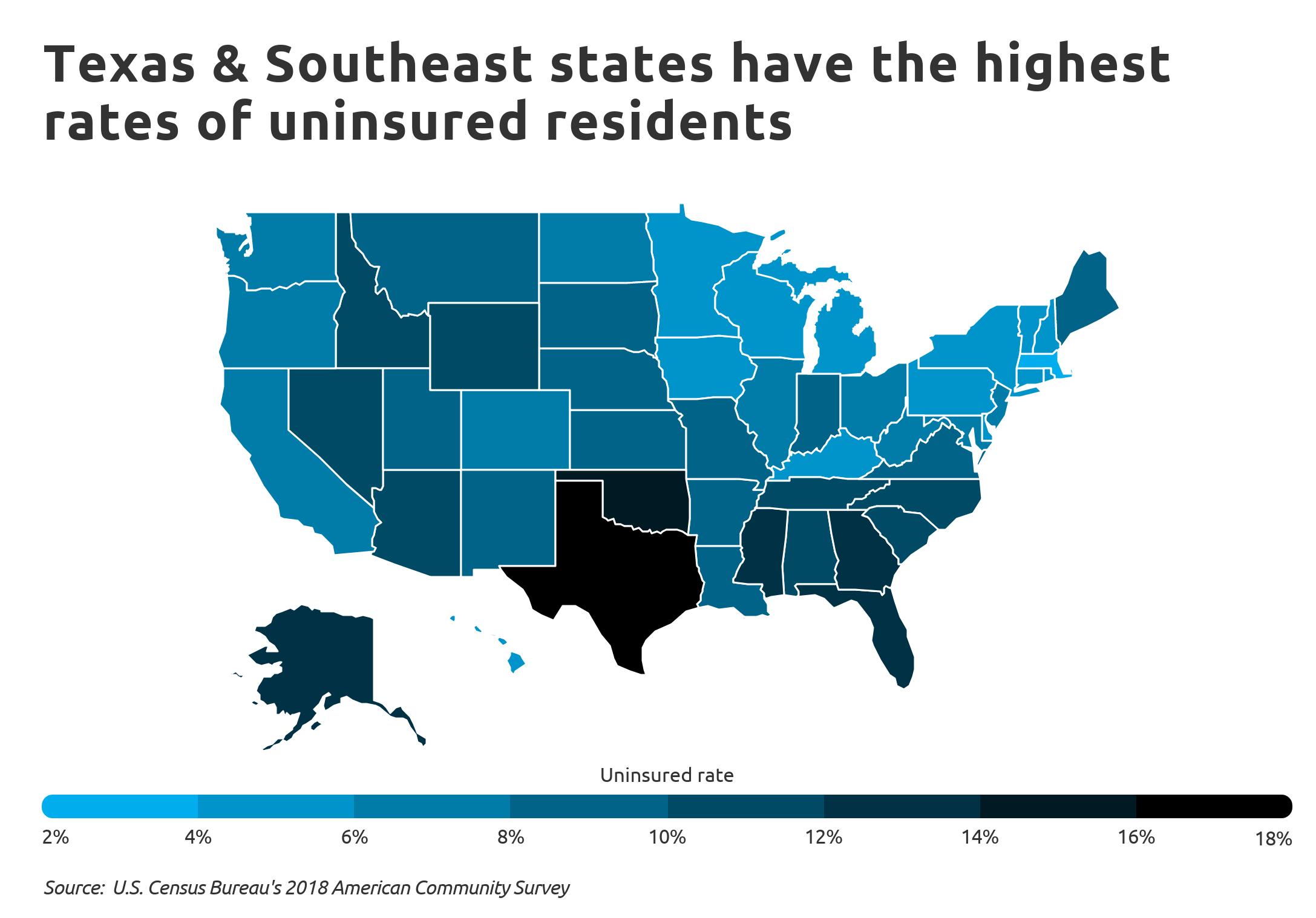

Texas has the highest uninsured rate in the U.S., with 29 percent of adults uninsured as of May, according to a report from Families USA.

The report compared uninsured rates in 2018 to rates in May 2020 using data from the U.S. Bureau of Labor Statistics and the Urban Institute. Every state saw an increase in the number of uninsured, and the total number of uninsured in the U.S. climbed 21 percent.

The increase was due in part to layoffs tied to the COVID-19 pandemic in recent months. Nearly 5.4 million Americans lost health insurance coverage from February to May of this year due to job losses, according to the report.

Below is the total percentage of all uninsured adults in each state and the District of Columbia as of May.

Sound familiar? Just like President Trump, these Republican senators say they support coverage guarantees for patients with preexisting health conditions. And just like Trump, their records show the opposite.

It’s a classic case of buyer beware: Look under the hood of what Daines, Gardner and McSally are selling, and you’ll find a car without an engine.

THE FACTS

Republicans for a decade have tried to repeal the Affordable Care Act, President Barack Obama’s signature health-care legislation. The Supreme Court has upheld the law twice in the face of challenges from conservative groups. As coronavirus cases reached a new high in the United States, the Trump administration filed a legal brief on June 25 asking the Supreme Court to strike down the entire law, joining with a group of GOP state attorneys general who argue that the ACA is unconstitutional.

Before the ACA, insurance companies could factor in a person’s health status while setting premiums, a practice that sometimes made coverage unaffordable or unavailable for those in need of expensive treatment or facing a serious illness such as cancer.

The ACA PROHIBITED THIS PRACTICE through two provisions: “guaranteed issue,” which means insurance companies must sell insurance to anyone who wants it, and “community rating,” which means people in the same age group and geographic area who buy similar insurance pay similar prices. The changes made insurance affordable for people with serious diseases or even those with minor health problems, who also could have been denied coverage before the law’s passage.

Now, about 20 million people covered through the ACA could lose their health insurance if the Supreme Court strikes down the law, among many other consequences bearing directly on the U.S. response to the coronavirus pandemic.

In addition to the coverage guarantee, the ACA established online health insurance marketplaces and subsidies for participating buyers. The law also directs billions of dollars a year in federal funding to states that have chosen to expand their Medicaid programs under the Obamacare law. Millions of Americans have gained coverage through those provisions.

We asked the Daines, Gardner and McSally campaigns whether the senators support or oppose the GOP lawsuit at the Supreme Court and how they would address affordability issues for patients with preexisting conditions if the ACA falls. None of their campaigns responded to our questions.

“Steve Daines will protect Montanans with preexisting conditions.”

Daines voted to repeal the ACA in 2013 and has supported efforts to repeal and replace the law more recently during the Trump administration.

Regarding the GOP lawsuit, a Daines spokesperson was quoted in the Billings Gazette saying the senator “supports whatever mechanism will protect Montanans from this failed law, lower health care costs, protect those with preexisting conditions and expand access to health care for Montanans.”

“What I look forward to working on is a plan that protects people with preexisting conditions.” (Gardner)

Gardner has been voting to repeal, defund or replace the ACA since 2011, the year after its passage. This year, his campaign website says nothing about the law, but his official Senate website says, “Fixing our healthcare system will require repealing the Affordable Care Act and replacing it with patient-centered solutions, which empower Americans and their doctors.”

Asked by the Hill whether he supported the GOP lawsuit, Gardner said: “That’s the court’s decision. If the Democrats want to stand for an unconstitutional law, I guess that’s their choice.” In an interview with Colorado Public Radio, Gardner evaded the question six times in a row.

“Of course I will always protect those with preexisting conditions. Always.” (McSally)

In 2015, McSally voted to repeal the ACA when she served in the House. In 2017, she voted to replace the ACA with the American Health Care Act, which would have allowed insurers to charge higher premiums to patients with complicated medical histories.

McSally, now in the Senate, has declined to comment on the GOP lawsuit pending before the Supreme Court. When asked by PolitiFact, “the campaign didn’t specifically answer, but pointed to her general disapproval of the ACA.”

WHAT HAPPENS IF THE GOP LAWSUIT SUCCEEDS?

Trump told The Washington Post days before his inauguration in 2017 that he was nearly done with his plan to replace the ACA. Three and a half years later, no replacement plan has emerged from the administration and Republicans in Congress hardly agree on what it would look like — or how to preserve the protections for preexisting health conditions.

Sen. Thom Tillis (R-N.C.), who is also running for reelection this year, has introduced a 24-page bill calledthe Protect Act that includes language guaranteeing coverage for preexisting conditions. Daines signed on as a co-sponsor on June 24, the day before the Justice Department filed its brief in the Supreme Court. McSally signed on in April 2019. Gardner is not listed as a co-sponsor.

Experts say the Tillis proposal does not offer the same level of protection for preexisting conditions as the ACA, and they warn that millions of Americans could lose their health coverage if the ACA falls and the Protect Act is the only replacement.

“Insurers before the Affordable Care Act had multiple and redundant ways that they could avoid people who had preexisting conditions,” said Karen Pollitz, a senior fellow at the Kaiser Family Foundation. The Protect Act prevents some of those practices, but it “leaves enough other loopholes that it would make it very possible and likely for insurers to be able to avoid paying benefits for the conditions they most worry about,” she said.

Before the ACA, an insurance company could reject an application outright, say, after reviewing a patient’s medical history. The Protect Act has language barring that practice.

“The second thing they could do is, they could sell you coverage, but they could exclude your preexisting condition. ‘Oh, you have diabetes? I’m not going to pay for any of those benefits,’” Pollitz said. “The Tillis bill says you can’t do that, so that’s good.”

In the days before the ACA, insurers were allowed to charge higher premiums based on a patient’s health status. To prevent this, the Protect Act takes language from the Health Insurance Portability and Accountability Act (HIPAA), rather than the newer ACA.

“The Protect Act inserts old HIPAA nondiscrimination language that prevents employers from varying worker premium contributions based on health status,” Pollitz said. “But the Protect Act also includes the old rule of construction that says nothing limits what the insurance company can charge the employer or individual.”

Pollitz said the “community rating” language in the ACA provides clearer protections in this area. The Protect Act says “nothing … shall be construed to restrict the amount that an employer or individual may be charged for coverage under a group health plan.”

“The bill would reinstate three protections at risk in the Texas case — prohibiting insurers from denying applicants based on pre-existing conditions, charging higher premiums due to a person’s health status, and excluding pre-existing conditions from coverage,” Sarah Lueck, a senior policy analyst at the left-leaning Center on Budget and Policy Priorities, wrote in an analysis.

“But it would leave many others on the cutting room floor,” she wrote, because insurers would be able to exclude coverage of benefits such as maternity care, mental health and substance-use treatment; set annual and lifetime limits on insurance payouts; and charge older patients more than younger patients at greater levels than the ACA allows, among other changes.

It’s important to keep in mind that the Protect Act would not replace other parts of Obamacare, such as the online marketplaces and subsidies. Neither would it continue the ACA’s Medicaid expansion, which 37 states and D.C. have now adopted. That includes Arizona, Colorado and Montana.

The Pinocchio Test

Voters deserve straight answers when their health care is on the line, especially in the middle of a deadly pandemic.

Daines, Gardner and McSally have voted to end the Affordable Care Act. People with preexisting conditions would have been left exposed because of those votes; insurers could have denied coverage or jacked up prices for sick patients.

The three senators’ comments about the GOP lawsuit are woefully vague, but they can all be interpreted as tacit support. Asked about the case, a Daines spokesperson said “whatever mechanism” to get rid of the ACA would do. McSally’s campaign “didn’t specifically answer, but pointed to her general disapproval of the ACA.” Gardner avoided the question six times in one interview, but in another, he said: “That’s the court’s decision. If the Democrats want to stand for an unconstitutional law, I guess that’s their choice.”

Roughly 5.4 million adults in the U.S. lost their health insurance from February to May after losing their jobs, according to a new estimate from Families USA, a group that favors the Affordable Care Act.

Why it matters: There are more adults under 65 without insurance in Southern states, which are the same states setting new records for single-day coronavirus infections along with risinghospitalizations, Axios’ Orion Rummler writes.

What they found: 3.9 million adults lost health insurance over one year during the Great Recession, per Families USA’s analysis. It only took four months in this current crisis for an estimated 5.4 million Americans to lose health insurance.

More than 20% of adults in Georgia, Florida, South Carolina, North Carolina, Mississippi, Oklahoma and Texas were without insurance as of May.

All of these states have set new records in the past two weeks for their highest number of coronavirus infections in a single day, per data from the COVID Tracking Project.

46% of adults who lost coverage due to the pandemic came from five states: Florida, New York, Texas, California and North Carolina.

The backdrop: 21 million Americans were unemployed in May, according to the Bureau of Labor Statistics’ nonfarm payrolls report.

The Trump administration proposed a rule Friday to allow some group health plans grandfathered under the Affordable Care Act to raise out-of-pocket costs for enrollees but still allow them to have health savings accounts. Such plans must not discriminate against enrollees with pre-existing conditions, but are exempt from many other ACA regulations. If they violate any rules regarding costs or structure they lose their grandfathered status and are required to follow all the mandates of the landmark 2010 law.

The proposed rule, issued by the U.S. Department of Labor, would relax some of the complex inflation and pricing calculations grandfathered plans must follow. The department admitted that the change could lead to higher deductibles and other out-of-pocket costs for the estimated 23.1 million enrollees in such grandfathered plans.

The rule stems from a 2017 executive order issued by President Donald Trump that allows regulatory changes to be made in response to perceived economic burdens imposed by the ACA. However, the Labor Department conceded in its Federal Register publication of the proposed rule that the current rules for grandfathered health plans probably weren’t that burdensome.

Dive Insight:

The administration has made no secret of its ire for the ACA and is actively trying to overturn it at the U.S. Supreme Court. A release explaining the changes notes fixed cost-sharing for high-deductible health plans would be raised, and “an alternative method of measuring permitted increases in fixed-amount cost sharing” has been introduced that “would allow plans and issuers to better account for changes in the costs of health coverage over time.”

The formal 76-page proposal, published in the Federal Register on Sunday, said premiums might go down as a result of the changes, but there were no estimates provided or circumstances where that might occur.

Moreover, the proposed rule also noted that the change could lead to more people foregoing healthcare because their out-of-pocket costs might become unaffordable.

The Labor Department also noted that there have been so few fluctuations in the state of grandfathered health plans in recent years that it was likely the current regulations were not overly burdensome in the first place.

Public comments will be solicited until mid-August before a final rule is issued.

Sen. Patty Murray, D-Wash., and ranking member of the Senate Health, Education, Labor, and Pensions Committee, wasted little time late last week blasting the proposal.

“Regardless of what the president wants to believe, we’re in the middle of a pandemic that is devastating families’ health and finances,” Murray said in a statement.

Promising that “we are going to at last build the health care system the American people have always deserved”, a joint task force of health policy advisors from the Biden and Sanders campaigns this week released a unified set of proposals that will serve as part of the former Vice President’s campaign platform for the November election.

While the document does not include Sanders’ signature “Medicare for All” proposal, it does support a government-run public insurance option that would be available to all Americans, at income-adjusted, subsidized rates—including free coverage for those with low incomes. It also promises to expand Medicare benefits to include dental, vision, and hearing coverage, and to extend Medicare eligibility to those age 60 and above.

For those who lose their health coverage due to the COVID pandemic, the unity document endorses having the government pick up the tab for COBRA benefits and shifting enrollees into premium-free coverage on the Obamacare exchanges when their COBRA eligibility expires.

It also promises greater investment in public health resources, including increased funding for the CDC, and funding to recruit 100,000 contact tracers nationwide.

Other key components of the proposal include eliminating “surprise billing”, reducing drug costs, addressing racial and gender-based health inequities, and bolstering investment in scientific research.

This week’s document represents an important step in unifying the progressive and moderate wings of the Democratic party around key health policy principles. Should Biden win in November, and if Democrats gain control of the Senate, we’d expect quick action on many of these proposals.

Clearly the most difficult would be the public option and Medicare expansion, which would require lengthy negotiation with various industry groups to garner sufficient political support. Similar to the 2009 process that led to the Affordable Care Act, we would likely see a year’s worth of political horse-trading, leading to passage of some compromise legislation before the midterm elections in 2022.

All of that in the midst of an ongoing pandemic and likely prolonged economic downturn—both of which will probably allow for the passage of more far-reaching legislation than might otherwise be possible.

The Supreme Court ruled Wednesday that the Trump administration may allow employers and universities to opt out of the Affordable Care Act requirement to provide contraceptive care because of religious or moral objections.

The decision seems to greatly expand an exception approved by the Obama administration, and the government estimates that it could mean that 70,000 to 126,000 women could lose access to cost-free birth control.

“We hold that the [administration] had the authority to provide exemptions from the regulatory contraceptive requirements for employers with religious and conscientious objections,” wrote Justice Clarence Thomas, who was joined by Chief Justice John G. Roberts Jr., and Justices Samuel A. Alito Jr., Neil M. Gorsuch and Brett M. Kavanaugh.

The decision sent the case back to a lower court and instructed it to dissolve a nationwide injunction that had kept the exception from being implemented.

Liberal Justices Elena Kagan and Stephen G. Breyer agreed with the court conservatives’ decision to send the case back to lower courts, but they did not join the majority opinion. Justices Ruth Bader Ginsburg and Sonia Sotomayor dissented.

At issue is the Trump administration’s decision in 2018 to expand the types of organizations that could opt out of providing cost-free access to birth control and the extent to which the government should create exemptions to the law for religious groups and nonreligious employers with moral and religious objections.

The Obama administration had narrower exceptions for churches and other houses of worship, and it created a system of “accommodations,” or workarounds, for religiously affiliated organizations such as hospitals and universities. Those accommodations would provide the contraceptive care but avoid having the objecting organizations directly cover the cost.

Under the Trump administration rules, the employers able to opt out include essentially all nongovernmental workplaces, from small businesses to Fortune 500 companies. And the employer has the choice of whether to permit the workaround.

The states of Pennsylvania and New Jersey initially challenged the rules, noting that when women lose coverage from their employers, they seek state-funded programs and services. Last summer, a unanimous panel of the U.S. Court of Appeals for the 3rd Circuit blocked the rules from taking effect nationwide. The court said the administration probably lacked authority to issue such broad exemptions and did not comply with requirements to provide notice and allow public comment on the rules.

In addition to the Trump administration, a charity called Little Sisters of the Poor defended the rules. The order of nuns, which runs homes for the elderly and employs about 2,700 people, points out that the government provided exemptions from the beginning for religious organizations such as churches. They say the accommodation provision violates the 1993 Religious Freedom Restoration Act, the law that says the government must have a compelling reason for programs that substantially burden religious beliefs.

In 2014, the Supreme Court in Burwell v. Hobby Lobby Stores ruled that certain closely held businesses do not have to offer birth control coverage that conflicts with the owners’ religious beliefs. But the court did not take a position on the accommodation provision, which requires objecting organizations to notify the government.

Two years later, a shorthanded court of eight justices declined to rule on the merits of another challenge to the contraceptive-coverage requirement and sent the case back to the lower courts. The unusual, unsigned decision was viewed as a punt by a court then equally divided along ideological lines.

Oklahoma voters approved a state question to expand Medicaid to more low-income residents, according to The Oklahoman.

The June 30 vote makes Oklahoma the first state to amend its constitution to expand Medicaid. Adding Medicaid expansion to Oklahoma’s constitution effectively limits the state’s GOP-controlled legislature and Republican governor from rolling back the measure.

The vote narrowly passed, with most of Oklahoma’s counties opposing the expansion. Just seven of the state’s 77 counties, including more populated ones such as Oklahoma and Tulsa Counties, voted in favor.

Oklahoma has until July 1, 2021, to expand Medicaid under the ACA. The expansion is expected to affect about 200,000 Oklahomans and cost about $164 million annually. The cost was a sticking point for Gov. Kevin Stitt, as the state may face a $1 billion shortfall in 2022. The Oklahoma Hospital Association supports the expansion.

/cdn.vox-cdn.com/uploads/chorus_asset/file/13249599/GettyImages_984402230.jpg)