West Reading, Pa.-based Tower Health has turned down a $706 million offer from StoneBridge Healthcare, a hospital turnaround firm, making this the fourth purchase offer rejected by the system since 2021.

StoneBridge received an email from Andrew Turnbull, a managing director at Houlihan Lokey, an investment bank that works with Tower Health, saying that there had been a board meeting and the firm’s offer had been rejected, Joshua Nemzoff, CEO of StoneBridge Healthcare, told Becker’s.

“I’m not sure what they’re thinking. We have requested multiple board meetings, but we’ve never had a chance to meet with the board. We’ve just gotten emails back saying they’re rejecting the offer,” Mr. Nemzoff said.

WoodBridge, a nonprofit sister organization to StoneBridge, initially shared a nonbinding agreement in principle with Tower Health, which included the intent to purchase the system’s assets.

“We’ve given them a number of other offers. I think the last one was more than a year ago. They’ve lost $400 million in operations in the last two years, and they’re $1.8 billion in revenue and $1.5 billion in debt, and 30 days of cash,” Mr. Nemzoff told Becker’s.

Tower Health initially turned down a $675 million offer from StoneBridge in November 2022. In partnership with Allentown, Pa.-based Lehigh Valley Health Network, the firm also made two conditional offers to acquire the system’s assets for $600 million in 2021, which were also rejected.

“Given their cash position and given their extraordinary amount of debt, I think our plan is just to frankly to wait for them to go bankrupt and show up in court for the auction. I think that’s going to happen next year,” Mr. Nemzoff said.

StoneBridge was formed in 2020. The firm currently does not own or operate any hospitals. Like StoneBridge, WoodBridge has also not completed any hospital deals, Mr. Nemzoff told Becker’s.

Three Philadelphia-based hospitals are reportedly up for sale, according to an email notice from Los Angeles-based investment bank Xnergy, The Philadelphia Inquirer reported Dec. 19.

The names of three hospitals are not confirmed. And the notice, which was obtained by the publication, did not name an owner of the hospitals. However, it did describe the hospitals’ owner as one that has acute care facilities with an average of 136 beds.

Three Philadelphia-area hospitals fit the bed parameters in the notice: Bristol-based Lower Bucks Hospital, Philadelphia-based Roxborough Memorial Hospital, and Norristown-based Suburban Community Hospital. All three are owned by Ontario, Calif.-based Prime Healthcare Services, The Philadelphia Inquirer reported.

Roxborough and Lower Bucks were acquired by Prime in 2012, with Suburban acquired by Prime’s nonprofit affiliate Prime Healthcare Foundation in 2016. The hospitals have also seen significant annual operating loss over the last five years with a 43% combined inpatient volume drop, from 3,795 discharges in 2018 to 2,250 discharges in 2022, the publication shared.

Members of the Pennsylvania Association of Staff Nurses & Allied Professionals at both Suburban and Lower Bucks are also set to launch five-day strikes Dec. 22 due to ongoing labor contract negotiations for things like increased wages and important benefits, a union spokesperson told Becker’s.

“Prime Healthcare’s mission is to always do what’s best for our communities and patients, however, we do not comment on strategic merger and acquisition initiatives,” Elizabeth Nikels, vice president of communications and public relations for Prime Healthcare, said in an email response to Becker’s regarding the sale.

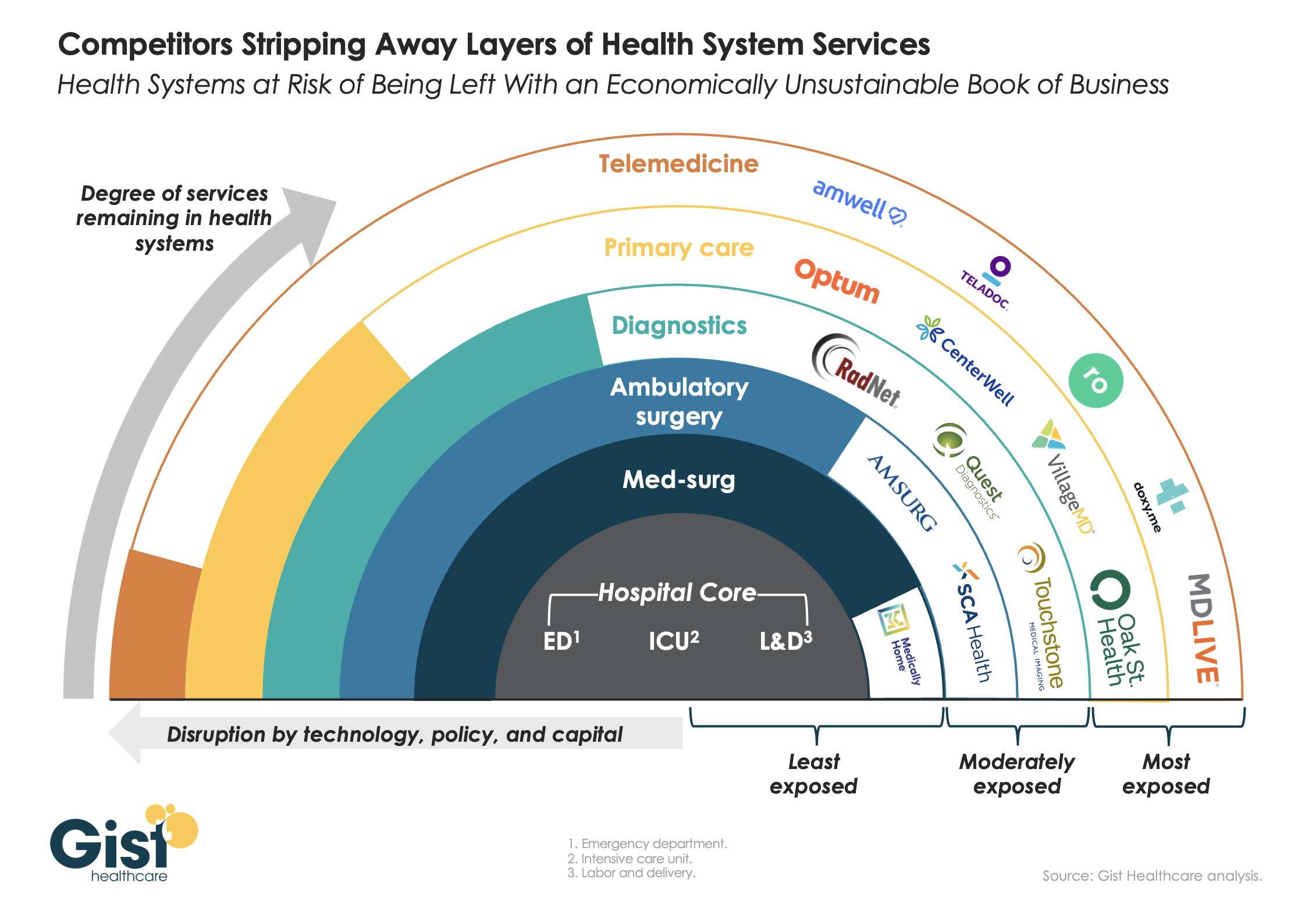

This week’s graphic features our assessment of the many emerging competitive challenges to traditional health systems.

Beyond inflation and high labor costs, health systems are struggling because competitors—ranging from vertically integrated payers to PE-backed physician groups—are effectively stripping away profitable services and moving them to lower-cost care sites. The tandem forces of technological advancement, policy changes, and capital investment have unlocked the ability of disruptors to enter market segments once considered safely within health system control.

While health systems’ most-exposed services, like telemedicine and primary care, were never key revenue sources (although they are key referral drivers), there are now more competitors than ever providing diagnostics and ambulatory surgery, which health systems have relied on to maintain their margins.

Moving forward, traditional systems run the risk of being “crammed down” into a smaller portfolio of (largely unprofitable) services: the emergency department, intensive care unit, and labor and delivery.

Health systems cannot support their operations by solely providing these core services, yet this is the future many will face if they don’temulate the strategies of disruptors by embracing the site-of-care shift, prioritizing high-margin procedures, rethinking care delivery within the hospital, and implementing lower-cost care models that enable them to compete on price.

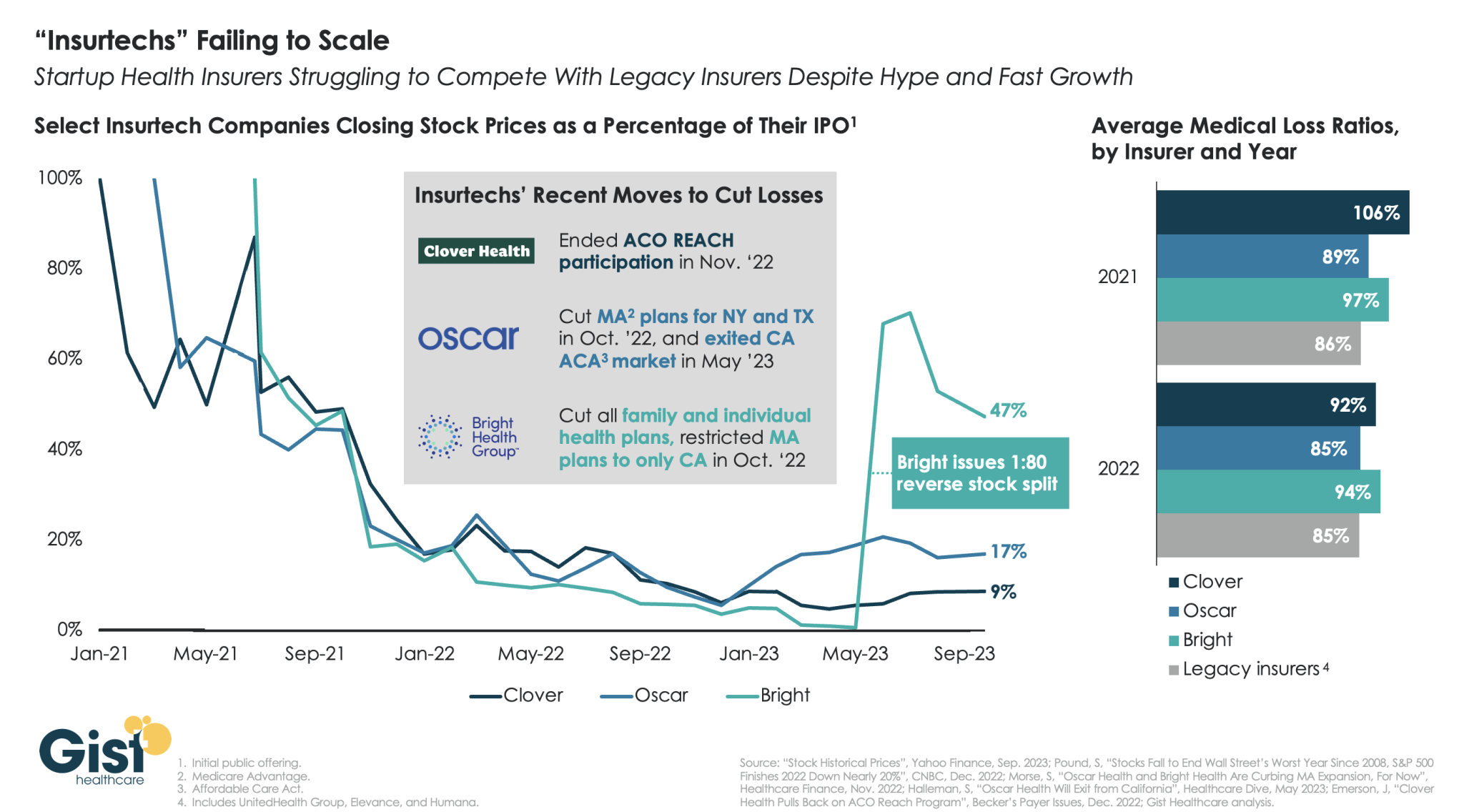

“Insurtechs” Clover Health, Oscar Health, and Bright Health all went public in the midst of the hot equity market of 2021. Investors were excited by the fast growth of these health insurer startups, and their potential to revolutionize an industry dominated by a few large players.

However, the hype has dissipated as financial performance has deteriorated. After growing at all costs during a period of low interest rates, changing market conditions directed investors to demand a pivot to profitability,which the companies have struggled to deliver—twoyears later,none of the three has turned a profit.

Oscar and Bright have cut back their market presence significantly, while Clover has mostly carried on while sustaining high losses. In the last two years, only Oscar has posted a medical loss ratio in line with other major payers, who meanwhile are reporting expectation-beating profits. While Oscar has shown signs of righting the ship since the appointment of former Aetna CEO Mark Bertolini,

the future of these small insurers remains uncertain. As their losses mount and they exit markets, they may become less desirable as acquisition targets for large payers.

Politicians, economists, auto industry analysts and main street business owners are closely watching the UAW strike that began at midnight last Thursday. Healthcare should also pay attention, especially hospitals. medical groups and facility operators where workforce issues are mounting.

Auto manufacturing accounts for 3% of America’s GDP and employs 2.2 million including 923,000 in frontline production. It’s high-profile sector industry in the U.S. with its most prominent operators aka “the Big Three” operating globally. Some stats:

The US automakers sold an estimated 13.75 million new and 36.2 million used vehicles in 2022.

The total value of the US car and automobile manufacturing market is $104.1 billion in 2023:

9.2 million US vehicles were produced in 2021–a 4.5% increase from 2020 and 11.8% of the global total ranking only behind China in total vehicle production.

As of 2020, 91.5% of households report having access to at least one vehicle.

There were 290.8 million registered vehicles in the United States in 2022—21% of the global market.

Americans spend $698 billion annually on the combination of automobile loans and insurance.

By comparison, the healthcare services industry in the U.S.—those that operate facilities and services serving patients—employs 9 times more workers, is 29 times bigger ($104 Billion vs. $2.99 trillion/65% of total spend) and 6 times more integral in the overall economy (3% vs. 18.3% of GDP).

Surprisingly, average hourly wages are similar ($31.07 in auto manufacturing vs. $33.12 in healthcare per BLS) though the range is wider in healthcare since it encompasses licensed professionals to unskilled support roles. There are other similarities:

Each industry enjoys ubiquitous presence in American household’ discretionary. spending.

Each faces workforce issues focused on pay parity and job security.

Each is threatened by unwelcome competitors, disruptive technologies and shifting demand complicating growth strategies.

Each is dependent on capital to remain competitive.

And each faces heightened media scrutiny and vulnerability to misinformation/disinformation as special interests seek redress or non-traditional competitors seek advantage.

Ironically, the genesis of the UAW dispute is not about wages; it is about job security as electric-powered vehicles that require fewer parts and fewer laborers become the mainstay of the sector. CEO compensation and the corporate profits of the Big Three are talking points used by union leaders to galvanize sympathizer antipathy of “corporate greed” and unfair treatment of frontline workers.

But the real issue is uncertainty about the future: will auto workers have jobs and health benefits in their new normal?

In healthcare services sectors—hospitals, medical groups, post-acute care facilities, home-care et al—the scenario is similar: workers face an uncertain future but significantly more complicated. Corporate greed, CEO compensation and workforce discontent are popular targets in healthcare services media coverage but the prominence of not-for-profit organizations in healthcare services obfuscates direct comparisons to for-profit organizations which represents less than a third of the services economy. For example, CEO compensation in NFPs—a prominent target of worker attention—is accounted differently for CEOs in investor-owned operations in which stock ownership is not treated as income until in options are exercised or shares sold. Annual 990 filings by NFPs tell an incomplete story nonetheless fodder for misinformation.

The competitive landscape and regulatory scrutiny for healthcare services are also more complicated for healthcare services. Unlike auto manufacturing where electric vehicles are forcing incumbents to change, there’s no consensus about what the new normal in U.S. healthcare services will be nor a meaningful industry-wide effort to define it. Each sector is defining its own “future state” based on questionable assumptions about competitors, demand, affordability, workforce requirements and more. Imagine an environmental scan in automakers strategy that’s mute on Tesla, or mass transit, Zoom, pandemic lock-downs or energy costs?

While the outlook for U.S. automakers is guardedly favorable, per Moody’s and Fitch, for not-for-profit health services operators it’s “unsustainable” and “deteriorating.”

Nonetheless, the parallels between the current state of worker sentiment in the U.S. auto manufacturing and healthcare services sectors are instructive. Auto and healthcare workers want job security and higher pay, believing their company executives and boards but corporate profit above their interests and all else. And polls suggest the public’s increasingly sympathetic to worker issues and strikes like the UAW more frequent.

Ultimately, the UAW dispute with the Big Three will be settled. Ultimately, both sides will make concessions. Ultimately, the automakers will pass on their concession costs to their customers while continuing their transitions to electric vehicles.

In health services, operators are unable to pass thru concession costs due to reimbursement constraints that, along with supply chain cost inflation, wipe out earnings and heighten labor tension.

So, the immediate imperatives for healthcare services organizations seem clear as labor issues mount and economics erode:

Educate workers—all workers—is a priority. That includes industry trends and issues in sectors outside the organization’s current focus.

Define the future. In healthcare services, innovators will leverage technology and data to re-define including how health is defined, where it’s delivered and by whom. Investments in future-state scenario planning is urgently needed.

Address issues head-on: Forthrightness about issues like access, prices, executive compensation, affordability and more is essential to trustworthiness.

Stay tuned to the UAW strike and consider fresh approaches to labor issues. It’s not a matter of if, but when.

PS: I drive an electric car—my step into the auto industry future state. It took me 9 hours last Thursday to drive 275 miles to my son’s wedding because the infrastructure to support timely battery charges in route was non-existent. Ironically, after one of three self-charges for which I paid more than equivalent gas, I was prompted to “add a tip”. So, the transition to electric vehicles seems certain, but it will be bumpy and workers will be impacted.

The future state for healthcare is equally frought with inadequate charging stations aka “systemness” but it’s inevitable those issues will be settled. And worker job security and labor costs will be significantly impacted in the process.

So far, 2023 is shaping up to be a slightly better year for hospital performance, but it comes on the heels of unprecedented financial difficulties for the sector.

In the graphic above, we evaluated nearly 30 years of historical data from Kaufman Hall and the American Hospital Association to provide a broader perspective on hospital operating margins over time. 2020 and 2022 have been the only years in which a majority of hospitals—53 percent—posted a negative operating margin.

During the most comparable periods of recent economic hardship, the “dot-com bubble burst” of the late 1990s and the 2009 Great Recession, the share of hospitals with negative operating margins amounted to only 42 and 32 percent, respectively.

With this context, hospitals’ current financial distress is more severe than anything we’ve seen in the past three decades.

Healthcare is clearly no longer recession-proof: a four percent operating margin—the level needed for health systems to not only sustain operations but also invest in growth—feels even more elusive as labor costs remain high, surgical care continues to shift to outpatient settings, the second half of the Baby-Boom generation ages into Medicare, and deep-pocketed competitors compete for profitable services.

That’s the amount you arrive at if you multiply the number of physicians employed by hospitals and health systems (approximately 341,200 as of January 2022, according to data from the Physicians Advocacy Institute and Avalere) by the median $306,362 subsidy—or loss—reported in our Q1 2023 Physician Flash Report.

Subsidizing physician employment has been around for a long time and such subsidies were historically justified as a loss leader for improved clinical services, the potential for increased market share, and the strengthening of traditionally profitable services.

But I am pretty sure the industry did not have $104 billion in losses in mind when the physician employment model first became a key strategic element in the hospital operating model. However, the upward reset in expenses brought on by the pandemic and post-pandemic inflation has made many downstream hospital services that historically operated at a profit now operate at breakeven or even at a loss. The loss leader physician employment model obviously no longer works when it mostly leads to more losses.

This model is clearly broken and in demand of a near-term fix. Perhaps the critical question then is how to begin? How to reconsider physician employment within the hospital operating plan?

Out of the box, rethink the physician productivity model. Our most recent Physician Flash Report data shows that for surgical specialties, there was a median $77 net patient revenue per provider wRVU. For the same specialties, there was a median $80 provider paid compensation per provider wRVU. In other words, before any other expenses are factored in, these specialties are losing $3 per wRVU on paid compensation alone. Getting providers to produce more wRVUs only makes the loss bigger.

It’s the classic business school 101 problem.

If a factory is losing $5 on every widget it produces, the answer is not to produce more widgets. Rather, expenses need to come down, whether that is through a readjustment of compensation, new compensation models that reward efficiency, or the more effective use of advanced practice providers.

Second, a number of hospital CEOs have suggested to me that the current employed physician model is quite past its prime. That model was built for a system of care that included generally higher revenues, more inpatient care, and a greater proportion of surgical vs. medical admissions. But overall, these trends were changing and then were accelerated by the Covid pandemic. Inpatient revenue has been flat to down. More clinical work continues to shift to the outpatient setting and, at least for the time being, medical admissions have been more prominent than before the pandemic.

Taking all this into account suggests that in many places the employed physician organizational and operating model is entirely out of balance. One would offer the calculated guess that there are too many coaches on the team and not enough players on the field. This administrative overhead was seemingly justified in a different loss leader environment but now it is a major contributor to that $104 billion industry-wide loss previously calculated.

Finally, perhaps the very idea of physician employment needs to be rethought.

My colleagues Matthew Bates and John Anderson have commented that the “owner” model is more appealing to physicians who remain independent then the “renter” model. The current employment model offers physicians stability of practice and income but appears to come at the cost of both a loss of enthusiasm and lost entrepreneurship. The massive losses currently experienced strongly suggest that new models are essential to reclaim physician interest and establish physician incentives that result in lower practice expenses, higher practice revenues, and steadily reduced overall subsidies.

Please see this blog as an extension of my last blog, “America’s Hospitals Need a Makeover.”It should be obvious that by analogy we are not talking about a coat of paint here or even new appliances in the kitchen.

The financial performance of America’s hospitals has exposed real structural flaws in the healthcare house. A makeover of this magnitude is going to require a few prerequisites:

Don’t start designing the renovation unless you know specifically where profitability has changed within your service lines and by explicitly how much. Right now is the time to know how big the problem is, where those problems are located, and what is the total magnitude of the fix.

The Board must be brought into the discussion of the nature of the physician employment problem and the depth of its proposed solutions. Physicians are not just “any employees.” They are often the engine that runs the hospital and must be afforded a level of communication that is equal to the size of the financial problem. All of this will demand the Board’s knowledge and participation as solutions to the physician employment dilemma are proposed, considered, and eventually acted upon.

The basic rule of home renovation applies here as well: the longer the fix to this problem is delayed the harder and more expensive the project becomes. The losses set out here certainly suggest that physician employment is a significant contributing factor to hospitals’ current financial problems overall. It would be an understatement to say that the time to get after all of this is right now.

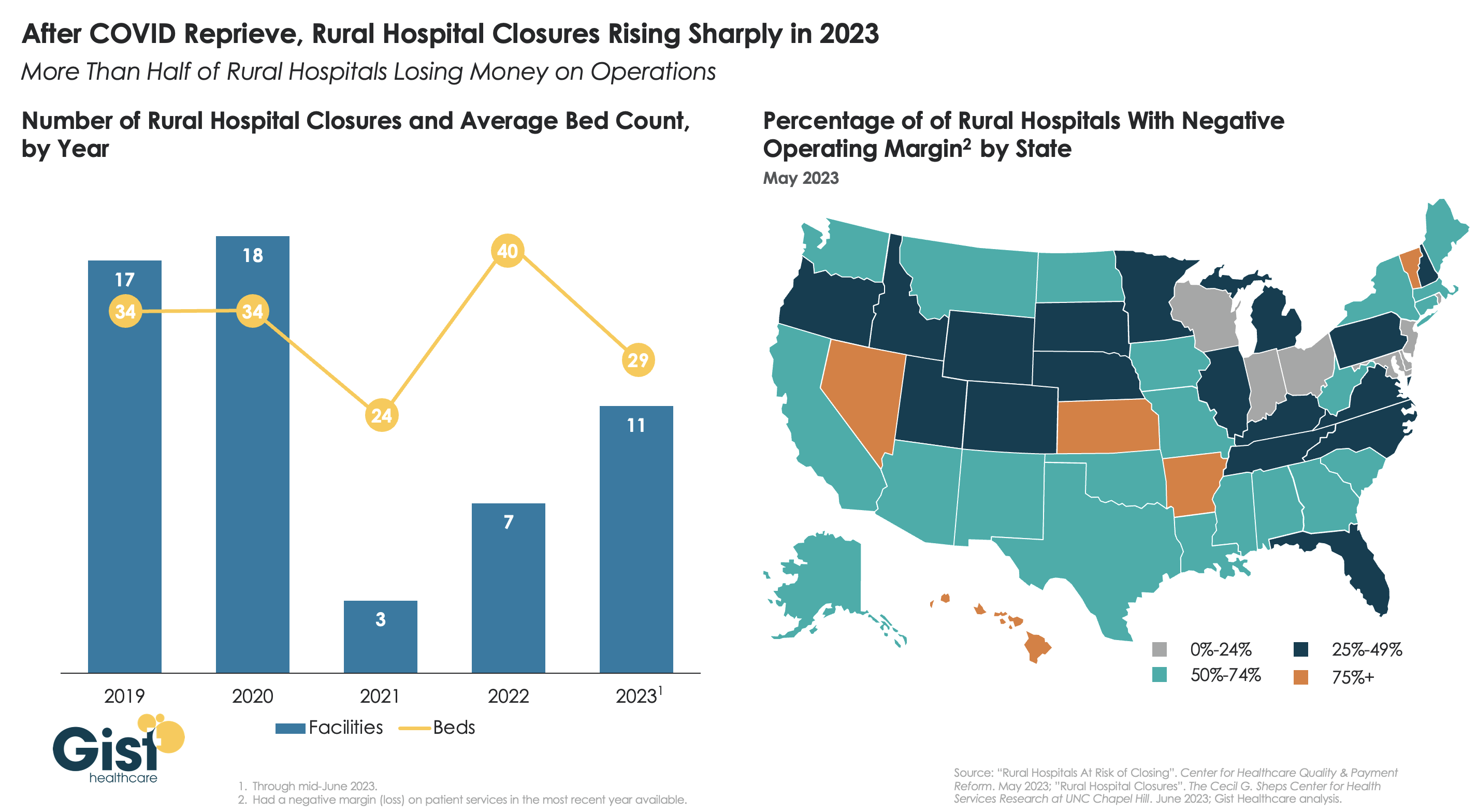

After a brief reprieve thanks to COVID relief funds, rural hospital closures are once again on the rise, with 11 facilities already closing in the first half of this year.

More rural facilities have already closed in 2023 than the previous two years combined, and this year is on pace to be the second-highest number of rural hospital beds lost since 2005.

And the majority of rural hospitals that haven’t closed are experiencing negative operating margins, with almost one in three at immediate or high risk of closure due to declining volumes, shifting payer mix, and increased labor and supply costs.

Leaders at rural hospitals now face difficult decisions including drastically cutting services, merging with a larger system, or closing their doors altogether. The Centers for Medicare and Medicaid Services (CMS) launched the Rural Emergency Hospital Program recently, designed to financially support small rural hospitals that convert to providing emergency services only, but so far program uptake has been limited.

While efforts to prop up hospitals will help to sustain access to care in the near term, rural communities ultimately need a new model for care, with reimagined facilities, supported by enhanced virtual connections to specialists and higher-acuity services.

On October 1, 1908, Ford produced the first Model T automobile. More than 60 years later, this affordable, mass produced, gasoline-powered car was still the top-selling automobile of all time. The Model T was geared to the broadest possible market, produced with the most efficient methods, and used the most modern technology—core elements of Ford’s business strategy and corporate DNA.

On April 25, 2018, almost 100 years later, Ford announced that it would stop making all U.S. internal-combustion sedans except the Mustang.

The world had changed. The Taurus, Fusion, and Fiesta were hardly exciting the imaginations of car-buyers. Ford no longer produced its U.S. cars efficiently enough to return a suitable profit. And the internal combustion technology was far from modern, with electronic vehicles widely seen as the future of automobiles.

Ford’s core strategy, and many of its accompanying products, had aged out. But not all was doom and gloom; Ford was doing big and profitable business in its line of pickups, SUVs, and -utility vehicles, led by the popular F-150.

It’s hard to imagine the level of strategic soul-searching and cultural angst that went into making the decision to stop producing the cars that had been the basis of Ford’s history. Yet, change was necessary for survival. At the time, Ford’s then-CEO Jim Hackett said, “We’re going to feed the healthy parts of our business and deal decisively with the areas that destroy value.”

So Ford took several bold steps designed to update—and in many ways upend—its strategy. The company got rid of large chunks of the portfolio that would not be relevant going forward, particularly internal combustion sedans. Ford also reorganized the company into separate divisions for electric and internal combustion vehicles. And Ford pivoted to the future by electrifying its fleet.

Ford did not fully abandon its existing strategies. Rather, it took what was relevant and successful, and added that to the future-focused pivot, placing the F-150 as the lead vehicle in its new electric fleet.

This need for strategic change happens to all large organizations. All organizations, including America’s hospitals and health systems, need to confront the fact that no strategic plan lasts forever.

Over the past 25-30 years, America’s hospitals and health systems based their strategies on the provision of a high-quality clinical care, largely in inpatient settings. Over time, physicians and clinics were brought into the fold to strengthen referral channels, but the strategic focus remained on driving volume to higher-acuity services.

More recently, the longstanding traditional patient-physician-referral relationship began to change. A smarter, internet-savvy, and self-interested patient population was looking for different aspects of service in different situations. In some cases, patients’ priority was convenience. In other cases, their priority was affordability. In other cases, patients began going to great lengths to find the best doctors for high-end care regardless of geographic location. In other cases, patients wanted care as close as their phone.

Around the country, hospitals and health systems have seen these environmental changes and adjusted their strategies, but for the most part only incrementally. The strategic focus remains centered on clinical quality delivered on campus, while convenience, access, value, affordability, efficiency, and many virtual innovations remain on the strategic periphery.

Health system leaders need to ask themselves whether their long-time, traditional strategy is beginning to age out. And if so, what is the “Ford strategy” for America’s health systems?

The questions asked and answered by Ford in the past five years are highly relevant to health system strategic planning at a time of changing demand, economic and clinical uncertainty, and rapid innovation. For example, as you view your organization in its entirety, what must be preserved from the existing structure and operations, and what operations, costs, and strategies must leave? And which competencies and capabilities must be woven into a going-forward structure?

America’s hospitals and health systems have an extremely long history—in some cases, longer than Ford’s. With that history comes a natural tendency to stick with deeply entrenched strategies. Now is the time for health systems to ask themselves, what is our Ford F150? And how do we “electrify” our strategic plan going forward?

A couple of months ago, I got a call from a CEO of a regional health system—a long-time client and one of the smartest and most committed executives I know. This health system lost tens of millions of dollars in fiscal year 2022 and the CEO told me that he had come to the conclusion that he could not solve a problem of this magnitude with the usual and traditional solutions. Pushing the pre-Covid managerial buttons was just not getting the job done.

This organization is fiercely independent. It has been very successful in almost every respect for many years. It has had an effective and stable board and management team over the past 30 to 40 years.

But when the CEO looked at the current situation—economic, social, financial, operational, clinical—he saw that everything has changed and he knew that his healthcare organization needed to change as well. The system would not be able to return to profitability just by doing the same things it would have done five years or 10 years ago. Instead of looking at a small number of factors and making incremental improvements, he wanted to look across the total enterprise all at once. And to look at all aspects of the enterprise with an eye toward organizational renovation.

I said, “So, you want a makeover.”

The CEO is right. In an environment unlike anything any of us have experienced, and in an industry of complex interdependencies, the only way to get back to financial equilibrium is to take a comprehensive, holistic view of our organizations and environments, and to be open to an outcome in which we do things very differently.

In other words, a makeover.

Consider just a few areas that the hospital makeover could and should address:

There’s the REVENUE SIDE: Getting paid for what you are doing and the severity of the patient you are treating—which requires a focus on clinical documentation improvement and core revenue cycle delivery—and looking for any material revenue diversification opportunities.

There is the relationship with payers: Involving a mix of growth, disruption, and optimization strategies to increase payments, grow share of wallet, or develop new revenue streams.

There’s the EXPENSE SIDE: Optimizing workforce performance, focusing on care management and patient throughput, rethinking the shared services infrastructure, and realizing opportunities for savings in administrative services, purchased services, and the supply chain. While these have been historic areas of focus, organizations must move from an episodic to a constant, ongoing approach.

There’s the BALANCE SHEET: Establishing a parallel balance sheet strategy that will create the bridge across the operational makeover by reconfiguring invested assets and capital structure, repositioning the real estate portfolio, and optimizing liquidity management and treasury operations.

There is NETWORK REDESIGN: Ensuring that the services offered across the network are delivered efficiently and that each market and asset is optimized; reducing redundancy, increasing quality, and improving financial performance.

There is a whole concept around PORTFOLIO OPTIMIZATION: Developing a deep understanding of how the various components of your business perform, and how to optimize, scale back, or partner to drive further value and operational performance.

Incrementalism is a long-held business approach in healthcare, and for good reason. Any prominent change has the potential to affect the health of communities and those changes must be considered carefully to ensure that any outcome of those changes is a positive one. Any ill-considered action could have unintended consequences for any of a hospital’s many constituencies.

But today, incrementalism is both unrealistic and insufficient.

Just for starters, healthcare executive teams must recognize that back-office expenses are having a significant and negative impact on the ability of hospitals to make a sufficient operating margin. And also, healthcare executive teams must further realize that the old concept of “all things to all people” is literally bringing parts of the hospital industry toward bankruptcy.

As I described in a previous blog post, healthcare comprises some of the most wicked problems in our society—problems that are complex, that have no clear solution, and for which a solution intended to fix one aspect of a problem may well make other aspects worse.

The very nature of wicked problems argues for the kind of comprehensive approach that the CEO of this organization is taking—not tackling one issue at a time in linear fashion but making a sophisticated assessment of multiple solutions and studying their potential interdependencies, interactions, and intertwined effects.

My colleague Eric Jordahl has noted that “reverting to a 2019 world is not going to happen, which means that restructuring is the only option. . . . Where we are is not sustainable and waiting for a reversion is a rapidly decaying option.”

The very nature of the socioeconomic environment makes doing nothing or taking an incremental approach untenable. It is clearly beyond time for the hospital industry makeover.