Health insurers licensed by the Blue Cross Blue Shield Association face steep financial penalties from that organization if they merge with a competitor that doesn’t sell BCBS insurance, Axios’ Bob Herman writes.

Why it matters: Blue Cross Blue Shield is one of the most recognizable health insurance names in the country, and the powerful association behind that brand wants to keep its dominance in local markets.

Case in point: Triple-S Management, a BCBS affiliate in Puerto Rico, sold itself in August to the parent company of the Florida Blues for $900 million.

If Triple-S sold itself to a non-BCBS company, therefore terminating its license with the BCBSA, Triple-S would have faced a $96 million surcharge, according to merger documents filed by Triple-S.

The $96 million charge, based on a fee of $98.33 per member, was called a “re-establishment fee.”

What they’re saying: “The license agreements between the Blue Cross Blue Shield Association and its licensees include various financial and other provisions that apply to terminations, mergers and sales of licensees,” BCBSA said in a statement.

“BCBSA is unable to confirm the financial implications of any other transactions that Triple-S may have considered in deciding to enter into this transaction.”

Operating cash flow margins for nonprofit hospitals fell to a median 7% in 2020.

A shortage of nurses and other workers will continue to erode hospital financial performance into 2022, according to a new Healthcare Quarterly report from Moody’s.

A rise in COVID-19 cases in various regions of the United States has contributed to a wave of nurses, often burned out, resigning to take care of family, to work in less acute healthcare settings such as ambulatory care or to pursue higher-paying contract opportunities, such as becoming a travel nurse.

Hospitals are also having difficulty finding other types of healthcare workers, such as respiratory therapists and imaging technicians, as well as nonclinical workers in areas such as dietary, housekeeping and environmental services.

WHY THIS MATTERS

The report holds no surprises for hospital executives, who already know the financial affect labor shortages are having on revenue. But Moody’s confirms projections that rising costs will make it difficult for hospitals to rebuild margins to pre-COVID-19 levels.

Labor shortages are driving up costs and also may be limiting the number of lucrative elective procedures, resulting in lost revenue. Not-for-profit hospitals saw operating cash flow margins fall to a median 7% in 2020, from 8.3% in the three prior years, according to Moody’s median data.

Hospitals using contract nurses report that hourly wages are very high, in some cases higher now with the Delta variant than during earlier COVID-19 surges. Many hospitals and health systems have also increased minimum wages for nonclinical workers and are finding they must compete with other service sectors, such as the food industry, to attract nonclinical staff.

Given their substantial reliance on government reimbursement from Medicare and Medicaid, most healthcare providers maintain limited pricing flexibility to offset the costs of higher wages. While there are opportunities for more lucrative commercial insurance contracts, rates are the subject of intense negotiations, limiting providers’ pricing power, Moody’s said.

Providers with strong liquidity and diversified cash flow will remain better positioned to manage stress from cost constraints. Hospitals are taking steps to retain nurses, including developing “float pools” of nurses who can work in multiple departments, increasing retention and merit pay, and expanding healthcare benefits such as mental health and child care services.

LifeBridge Health, a not-for-profit health system operating in Baltimore and Carroll County, Maryland, paid its nursing staff retention bonuses in December 2020 as the labor market tightened. To recruit nurses, many systems are offering signing bonuses in exchange for multi-year work commitments as well as scholarship and loan forgiveness programs with local nursing schools.

While these strategies will ease the effect of labor shortages over the long term, they will cause hospitals’ costs to increase in 2022 as salaries and benefits typically represent at least half of a hospital’s expenses. Labor shortages will also likely spark an increase in unionization efforts or lead to more difficult negotiations between unions and providers, potentially increasing costs via new contracts.

THE LARGER TREND

The quarterly report focused on the impact of labor shortages and cost pressures for various sectors, including hospitals, insurers, pharmaceuticals, healthcare services such as staffing firms and health insurers.

Health insurers are less affected by labor shortages, wage pressure and potentially burgeoning inflation than many other healthcare sectors, Moody’s said. Insurers reset premiums each year, which helps them to offset inflation. But if the government does not keep up with payment, providers will look to insurers to make up the shortfall.

Large physician staffing companies, such as Envision Healthcare Corporation and Team Health Holdings, will experience pressure on their profitability as it becomes harder and more expensive to fill open positions as burnout and retirements decrease the number of doctors available to work.

Travel nurse staffing has higher profit margin resilience compared to physician staffing, the report said.

For real estate investment trusts, worker shortages are slowing net operating income growth for REITs to invest in senior housing and skilled nursing facilities.

Growth in salaries and benefits has exceeded hospitals’ expense growth, a trend likely to continue for the remainder of 2021 andinto 2022, Moody’s said in an earlier October report.

In one bright spot in the earlier report, Moody’s noted recent rises in nursing school enrollment indicating a more robust long-term staffing pipeline. However, the aging population, combined with a healthcare workforce that may be retiring from their jobs or quitting due to burnout, represent long-term healthcare staffing challenges nationwide.

Health economists study the economic determinants of health. They also analyze how health care resources are utilized and allocated, and how health care policies and quality of care can be improved. In this episode, we discuss what exactly a healthcare system would look like if these professionals were calling all the shots.

Labor shortages from the COVID-19 pandemic will continue to worsen the financial performance of nonprofit and for-profit hospitals into 2022, an October Moody’s quarterly report found.

As nurses and other workers deal with burnout and resign from positions, some hospitals are limiting elective procedures, which is reducing revenue. They’re also increasing minimum wage and using contract nurses with much higher hourly wages.

Physician staffing companies like Envision Healthcare Corp. and TeamHealth will also struggle with profitability as it becomes more difficult to fill open positions because of fewer available physicians, the report said.

An Association of American Medical Colleges study in 2020 found that more than 2 out of 5 physicians will be 65 or older by 2030; COVID-19 is accelerating retirement.

Meanwhile, health insurers are not as affected by labor shortages, wage pressure and inflation, according to the report. Because their product is more short-term and premiums reset every year, they have more flexibility when it comes to inflation.

Cost-sharing is the practice of making individuals responsible for part of their health insurance costs beyond the monthly premiums they pay for health insurance – think things like deductibles and copayments. The practice is meant to inspire more thoughtful choices among consumers when it comes to healthcare decisions. However, the choices it inspires can often be more harmful than good.

We recently shared an updated perspective on the independent physician landscape. Notably absent from this map, but an important player in this space, are entities, like health plans, private equity, and health systems, who partially or wholly fund some independent physician groups.

We intentionally left these funders off the map because they don’t work in a uniform way with all physician groups. The reality is that funders have their handprints all over this map—and just knowing what type of funder you’re working with doesn’t necessarily tell you how they work with physician groups.

Funders work across the physician landscape because they recognize two things:

First, in order to play in today’s physician market, funders need to be flexible in how they work with physicians in order to appeal to the wide variety of groups and build a bigger market presence.

Second, building or buying these physician group archetypes outright is not the only way to work with them. Many funders instead opt to invest in them—either through dollars or resources.

Key funders to watch

There are three key funders we track the closest: private equity, health plans, and health systems. Below are brief overviews of how they commonly work with independent groups and our predictions for where you might see them go next.

Private equity (PE): Consistent approach with still to be proven outcomes

The goal of PE firms is to make money on their investments. To do this, these firms buy shares of practices in order to have partial ownership. In return, physician groups get the capital they need to make investments—investments that in theory drive profits for both the physician shareholders and the PE investors. Unlike other funders, PE is rarely associated with full acquisition.

Two of the places we’ve seen the most private equity investment are in consolidation of specialty practices (usually at the national level) or value-based care investments in primary care practices (across all archetypes).

Private equity is gaining traction as a physician group partner because they often try to preserve some degree of physician autonomy and they’ve learned to nuance their investments and pitches based on the group they’re seeking to work with.

We predict: PE will continue to back the full range of archetypes on this map—investing in both independent groups directly and the national archetypes.

What we’ll be watching:

What will happen to the handful of major PE investments in the independent physician group space that will be reaching their 5-7 year mark

What level of physician autonomy will PE firms continue to preserve as PE gains stronger footholds in the physician landscape

Health plans: The most eager to transform (incrementally)

Health plans are often predominantly associated with a single physician archetype for a given plan. For example, when you think about UnitedHealthcare, you might think of their sister company, OptumCare, and an aggregation strategy. Or, you might think of Blues plans most commonly as service partners.

However, when you dig deeper, the story is much more nuanced. Plans and their parent companies like UnitedHealth Group do often aggregate practices, but they also sell and integrate services via service partner models. And several Blues plans are now building practices from the ground up. To top it off, some plans are even adopting an investment strategy like Anthem with Privia.

Perhaps more than any other funder, health plans often adopt a range of strategies to develop their physician strategy and maintain their existing networks. And even cases where plans aren’t funding entities themselves, they’re thinking of new ways to work with the growing range of physician groups.

We predict: Health plans will move away from a uniform approach to physician practice partnership and towards more multifaceted approaches to appeal to a wide range of providers.

What we’ll be watching:

Will health plans diversify their suite of approaches based on the groups they’re pursuing

Will health plans tailor their value proposition for each partnership approach

Health systems: Playing catch up to evolve

We often tend to think about health systems as aggregators—they buy independent physician groups and add them to their employed medical groups. But we’re seeing two physician market shifts that are causing health systems to move away from a one-size-fits-all approach.

One, the remaining independent groups are growing in size and, two, they are less willing to be acquired. On top of that, as private equity firms and payers continue to diversify their strategies, health systems must adapt to keep pace—or risk being seen as the least attractive partner.

As a result, more health systems are telling us about their new approaches to physician partnerships, like starting an MSO to act as a service partner or convening coalitions between themselves and independent groups.

We predict: Health systems will face increasing pressure to diversify how they are operating with physician groups. Similar to health plans, we expect to see a pivot away from an aggregation-only approach. To learn more, read our take on how health systems and independent groups should think about partnership.

What we’ll be watching:

How quickly will health systems stand up additional partnership approaches

Will health systems in markets where they’re the dominant partner proactively adjust their partnership approach versus wait for the market to shift first

Your checklist to work successfully with today’s physician groups

As you evaluate your partnership strategy, here’s our starter list of questions to ask yourself:

Clarify your partnership goals:

What are my organization’s goals for physician partnership broadly?

What are the archetypes I currently fund or partner with?

Do these archetypes serve my organization’s stated goals?

Identify the right partnership approaches for your organization

What new archetypes should I build or work with to advance my organization’s goals and target new physician groups?

Do I need to build this archetype myself or is it better to fund one that exists?

If funding, should I wholly own or invest in the archetype?

Define your value proposition to physicians

Have I adjusted my value proposition for each of the archetypes I fund or partner with?

Am I clearly articulating my value proposition in a way that speaks to physicians’ needs and wants?

Does my value proposition align with what I’m actually delivering? For example, if I say I’m preserving autonomy, how am I doing that?

How does my value proposition compare and compete with others in the market?

Map out the power dynamics of the archetypes you want to work with

Who has the ultimate decision-making power in the organization? (Hint: Decision-making power gets more diffuse as you move from right to left, national chain to service partner.)

Who are the key stakeholders who influence decision-making?

About 73% of health insurance markets are highly concentrated, and in 46% of markets, one insurer had a share of 50% or more, a new report from the American Medical Association shows. The report comes a few months after President Joe Biden directed federal agencies to ramp up oversight of healthcare consolidation.

The majority of health insurance markets in the U.S. are highly concentrated, curbing competition, according to a report released by the American Medical Association.

For the report, researchers reviewed market share and market concentration data for the 50 states and District of Columbia, and each of the 384 metropolitan statistical areas in the country.

They found that 73% of the metropolitan statistical area-level payer markets were highly concentrated in 2020. In 91% of markets, at least one insurer had a market share of 30%, and in 46% of markets, one insurer had a share of 50% or more.

Further, the share of markets that are highly concentrated rose from 71% in 2014 to 73% last year. Of those markets that were not highly concentrated in 2014, 26% experienced an increase large enough to enter the category by 2020.

In terms of national-level market shares of the 10 largest U.S. health insurers, UnitedHealth Group comes out on top with the largest market share in both 2014 and 2020, reporting 16% and 15% market share, respectively. Anthem comes in second with shares of 13% in 2014 and 12% in 2020.

But the picture looks different when it comes to the market share of health insurers participating in the Affordable Care Act individual exchanges. In 2014, Anthem held the largest market share among the top 10 insurers on the exchanges, with a share of 14%. By 2020, Centene had taken the top spot, with a share of 18%, while Anthem had slipped to fifth place, with a share of just 4%.

Another key entrant into the top 10 list in 2020 was insurance technology company Oscar Health, with 3% of the market share in the exchanges at the national level.

“These [concentrated] markets are ripe for the exercise of health insurer market power, which harms consumers and providers of care,” the report authors wrote. “Our findings should prompt federal and state antitrust authorities to vigorously examine the competitive effects of proposed mergers involving health insurers.”

The payer industry hit back. In a statement provided to MedCity News, America’s Health Insurance Plans, a national payer association, said that Americans have many affordable choices for their coverage, pointing to the fact that CMS announced average premiums for Medicare Advantage plans will drop to $19 per month in 2022 from $21.22 this year.

“Health insurance providers are an advocate for Americans, fighting for lower prices and more choices for them,” said Kristine Grow, senior vice president of communications at America’s Health Insurance Plans, in an email. “We negotiate lower prices with doctors, hospitals and drug companies, and consumers benefit from lower premiums as a result.”

Further, the report does not mention the provider consolidation that also contributes to higher healthcare prices. Mergers and acquisitions among hospitals and health systems have continued steadily over the past decade, remaining relatively impervious to even the Covid-19 pandemic.

Scrutiny around consolidation in the healthcare industry may grow. In July, President Joe Biden issued an executive order urging federal agencies to review and revise their merger guidelines through the lens of preventing patient harm.

The Federal Trade Commission has already said that healthcare businesses will be one of its priority targets for antitrust enforcement actions.

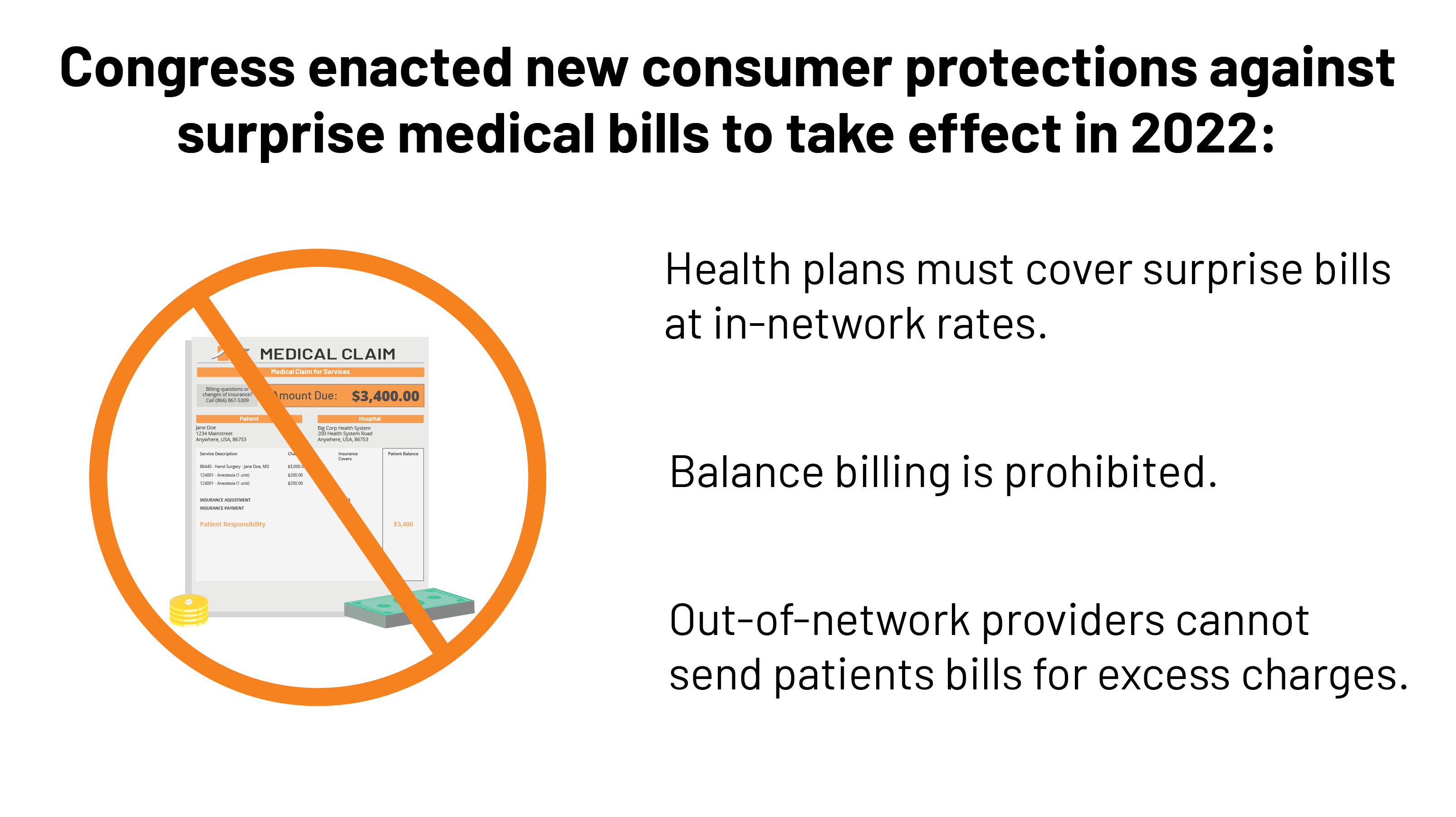

On Thursday the Department of Health and Human Services (HHS), along with other federal agencies, released the long-awaited second half of its proposed regulations implementing the No Surprises Act, passed by Congress at the end of last year, which bans “surprise billing” of patients who unsuspectingly receive care from out-of-network providers.

The interim final rule, which will take effect on January 1st after a comment and review period, lays out a process for addressing disputed patient bills, first through a 30-day “open negotiation” between the patient’s insurer and the out-of-network provider, and then through a federally-managed arbitration process.

Of most interest to insurers and providers who have lobbied fiercely for months to ensure a favorable interpretation of the law, the new regulation specifies that the outsider arbitrator, to be agreed upon by both parties, must begin with the presumption that the median in-network rate for services in the local market is the correct one. The arbitrator can then modify that price based on the specific circumstances of the case.

That method was broadly favored by insurers, and AHIP strongly endorsed the proposed approach, saying in a press release that “this is the right approach to encourage hospitals, healthcare providers, and health insurance providers to work together and negotiate in good faith.” Predictably, the hospital lobby felt otherwise; the American Hospital Association reacted by calling the rule “a windfall for insurers”, saying that it “unfairly favors insurers to the detriment of hospitals and physicians who actually care for patients.”

The ultimate winners here are patients, who will gain important new protections against the potentially crippling financial implications of surprise billing. We’d agree with HHS Secretary Xavier Becerra, who told the New York Times that the new rule would “[take] patients out of the middle of the food fight,” and provide “a clear road map on how you can resolve that food fight between the provider and the insurer.” It’s about time.

Still unresolved: the high cost of out-of-network ambulance services, left out of the No Surprises Act altogether. Let’s hope Congress circles back to address that issue soon.

Prime Healthcare’s New Jersey hospitals announced this week they would terminate their contracts with major insurer UnitedHealthcare, citing significant underpayment compared to the rates of neighboring facilities, and lower reimbursement rates than those offered by Medicaid.

The decision impacts Saint Clare’s Health in Denville, Dover and Boonton, Saint Michael’s Medical Center in Newark, and Saint Mary’s General Hospital in Passaic.

Dr. Sonia Mehta, regional CEO and chief medical officer of Prime Healthcare New Jersey, said in a statement that the hospitals have been underpaid for years, including some rates well below that of Medicaid, and added that UnitedHealthcare’s contract proposal jeopardizes the organization’s ability to deliver quality care.

WHAT’S THE IMPACT?

Due to new disclosure requirements by the Centers for Medicare and Medicaid Services, all hospitals must now disclose their contracted rates. Prime Healthcare said it learned it had been underpaid compared to what United has been paying neighboring hospitals.

The New Jersey Hospital Association reported that Prime Healthcare hospitals provide quality healthcare services and that its cost of care is among the lowest in the State of New Jersey.

“We are patient-focused and are committed to delivering the most compassionate care by exceptional physicians using state-of-the-art technology,” said Mehta. “Undercutting our payments is unacceptable, and so we are taking the necessary step of providing notice of our intent to provide care out-of-network. We realize it is a bold move, but a necessary one to separate our hospitals from organizations that work contrary to our mission and commitment to our patients.”

Prime’s New Jersey hospitals will continue to honor the rates and services in the agreements until the end of the cooling off period, which is December 16 for the Medicaid product and December 31 for the commercial and Medicare products.

All patients can continue to use Prime’s emergency services at its New Jersey hospitals, regardless of insurance, and the hospitals are willing to negotiate single patient agreements for elective services. The hospitals will also honor all continuity of care services for United members.

UnitedHealthcare told Healthcare Finance News that Prime’s demands are unreasonable.

“Prime is demanding a 14% price hike in just one year for our employer-sponsored and individual plans, which is unsustainable and would increase healthcare costs for New Jersey residents and employers,” said spokesperson Cole Manbeck. “We hope Prime will work with us to ensure the people we serve have continued access to Prime’s hospitals at an affordable cost.

“While we have agreement on rates for our Medicare Advantage and Medicaid plans and proposed to Prime that we finalize the contract for these plans, Prime refused unless we accepted its 14% price hike demands for our employer-sponsored and individual plans,” he said.

“This unnecessarily puts thousands of New Jersey residents in the middle of our negotiation, presumably because Prime hopes the potential disruption in care for our most vulnerable members would pressure us to give in to its price hike demands.”

THE LARGER TREND

Prime Healthcare New Jersey is part of Prime Healthcare, a health system operating 45 hospitals and more than 300 outpatient locations in 14 states. In 2020, Prime successfully completed its acquisition of St. Francis Medical Center, a 384-bed Los Angeles County medical facility that had previously been owned by Verity Health.

Prime acquired St. Francis for a net of more than $350 million, including a $200 million base cash price and $60 million for accounts receivable.

Just last week, CMS blocked four Medicare Advantage plans from enrolling new members in 2022 because they didn’t spend the minimum threshold on medical benefits, with three UnitedHealthcare plans and one Anthem plan failing to hit the required 85% mark three years in a row. Medicare Advantage plans are required to spend a minimum of 85% of premium dollars on medical expenses; failure to do so for three consecutive years triggers the sanctions.

In June, UnitedHealthcare backtracked on a proposed policy retroactively rejecting emergency department claims. The policy, which was slated to take effect on July 1, meant UHC would evaluate ED claims to determine if the visits were truly necessary for commercially insured members. Claims deemed non-emergent would have been subject to “no coverage or limited coverage,” according to the insurer.

UHC rolled back the policy – for now. The insurer told The New York Times that the policy would be stalled until the end of the ongoing COVID-19 pandemic, whenever that might be.

The pharmaceutical industry is on the verge of defeating a major Democratic proposal that would allow the federal government to negotiate drug prices.

Speaker Nancy Pelosi (D-Calif.) can afford only three defections when the House votes on a sweeping $3.5 trillion spending package, but Reps. Scott Peters (D-Calif.), Kurt Schrader (D-Ore.) and Kathleen Rice (D-N.Y.) last week voted to block the drug pricing bill from advancing out of the Energy and Commerce Committee. Rep. Stephanie Murphy (D-Fla.) voted against advancing the tax portion of the legislation in the House Ways and Means Committee.

All told, the number of House Democrats who have concerns about the drug pricing bill is in the double digits, and several Democrats in the 50-50 Senate would not vote for the measure in its current form, according to industry lobbyists.

The holdouts mark a sharp contrast to just two years ago, when every House Democrat voted for the same drug pricing bill, underscoring the inroads pharmaceutical manufacturers have made with the caucus on a measure that would narrow corporate profit margins.

“The House markups on health care demonstrate there are real concerns with Speaker Pelosi’s extreme drug pricing plan and those concerns are shared by thoughtful lawmakers on both sides of the aisle,” the Pharmaceutical Research and Manufacturers of America (PhRMA), the industry’s top trade group, said in a statement following the committee votes.

The reversal follows the industry’s multimillion-dollar ad campaigns opposing the bill, timely political donations and an extensive lobbying effort stressing drugmakers’ success in swiftly developing lifesaving COVID-19 vaccines.

The bill at the center of the fight, H.R. 3, would allow Medicare to negotiate the price of prescription drugs by tying them to the lower prices paid by other high-income countries. The measure is projected to free up around $700 billion through the money it saves on drug purchases — covering a big chunk of the Democrats’ $3.5 trillion spending plan.

Drugmakers say the measure would reduce innovation, pointing to a Congressional Budget Office estimate that found it would lead to nearly 60 fewer new drugs over the next three decades.

Peters and other Democrats have proposed an alternative bill that would limit price negotiation to a fraction of the prescription drugs included in H.R. 3, focusing instead on drugs like insulin, the diabetes treatment that has seen its price rise dramatically over the last decade. The alternative measure also would set a yearly out-of-pocket spending limit for lower-income Medicare recipients.

The proposal foreshadows a less aggressive drug pricing compromise that uneasy Senate Democrats are more likely to get behind.

“You’re going to see something pass, but it probably won’t be H.R. 3,” said a lobbyist who represents pharmaceutical companies.

Pharmaceutical manufacturers oppose any efforts to control the price of prescription drugs, but the alternative bill is more favorable to the industry than the broader Democratic bill.

“Any kind of artificial price controls will have an impact on both new scientific investment as well as access to medicines,” said Rich Masters, chief public affairs and advocacy officer at the Biotechnology Innovation Organization, a trade group that represents pharmaceutical giants such as Sanofi, Merck and Johnson & Johnson.

“We appreciate the focus on patient out of pocket costs, which we know is a critical component to any reform efforts and something that BIO and our member companies have long supported,” he added.

Progressive lawmakers, who have long bemoaned rising drug prices, blasted the three House Democrats who voted to block H.R. 3, saying they succumbed to industry donations and lobbying efforts.

“What the pharmaceutical industry has done, year after year, is pour huge amounts of money into lobbying and campaign contributions … the result is that they can raise their prices to any level they want,” Sen. Bernie Sanders (I-Vt.) said in a video message Friday.

The pharmaceutical industry spent $171 million on lobbying through the first half of the year, more than any other industry, to deploy nearly 1,500 lobbyists, according to money-in-politics watchdog OpenSecrets. That’s up from around $160 million at the same point last year, when the industry broke its own lobbying spending record.

Peters announced his opposition to Pelosi’s drug pricing proposal in May and shortly after was showered with donations from pharmaceutical industry executives and lobbyists, STAT News reported.

Peters is the No. 1 House recipient of pharmaceutical industry donations this year, bringing in $88,550 from pharmaceutical executives and PACs, according to OpenSecrets. Over his congressional career, Peters has received in excess of $860,000 from drugmakers, more than any other private industry.

The California Democrat told The Hill last week that accusations of his vote being guided by donations are “flat wrong” and noted that his San Diego congressional district employs roughly 27,000 pharmaceutical industry workers consisting mostly of researchers.

“It’s always going to be the attack because it’s simple and it’s easier than engaging on the merits,” he said.

Schrader received nearly $615,000 from the industry. He inherited a fortune from his grandfather, a former top executive at Pfizer, and had between $50,000 and $100,000 invested in Pfizer, in addition to other pharmaceutical holdings as of last year, according to his most recent annual financial disclosure.

Schrader tweeted last week that he is “committed to lowering prescription drug costs,” while arguing that the House bill would not pass the Senate in its current form.

Rep. Lou Correa (D-Calif.) another supporter of Peters’s more industry friendly bill, received an influx of pharmaceutical donations in recent months, including a $2,000 check from Pfizer’s PAC in mid-August, according to Federal Election Commission filings.

In meetings with lawmakers, lobbyists have argued that now is not the time to go after drugmakers, which developed highly effective COVID-19 vaccines and are developing booster shots and other treatments to fight the virus.

The U.S. Chamber of Commerce, which represents several major pharmaceutical manufacturers, said last month that Democratic drug pricing efforts will leave the U.S. “unprepared for the next public health crisis.”

PhRMA last week launched a seven-figure ad campaign to oppose H.R. 3. That’s after pharmaceutical groups and conservative organizations bankrolled by drugmakers spent $18 million on ads attacking the proposal through late August, according to an analysis from Patients for Affordable Drugs, a group that launched its own ads backing H.R. 3 last week.

The ad buys are meant to sway both lawmakers and the general public. A June Kaiser Family Foundation poll found that 90 percent of Americans approve of the drug pricing measure, but that support dropped to 32 percent when they were told that the proposal “could lead to less research and development of new drugs.”