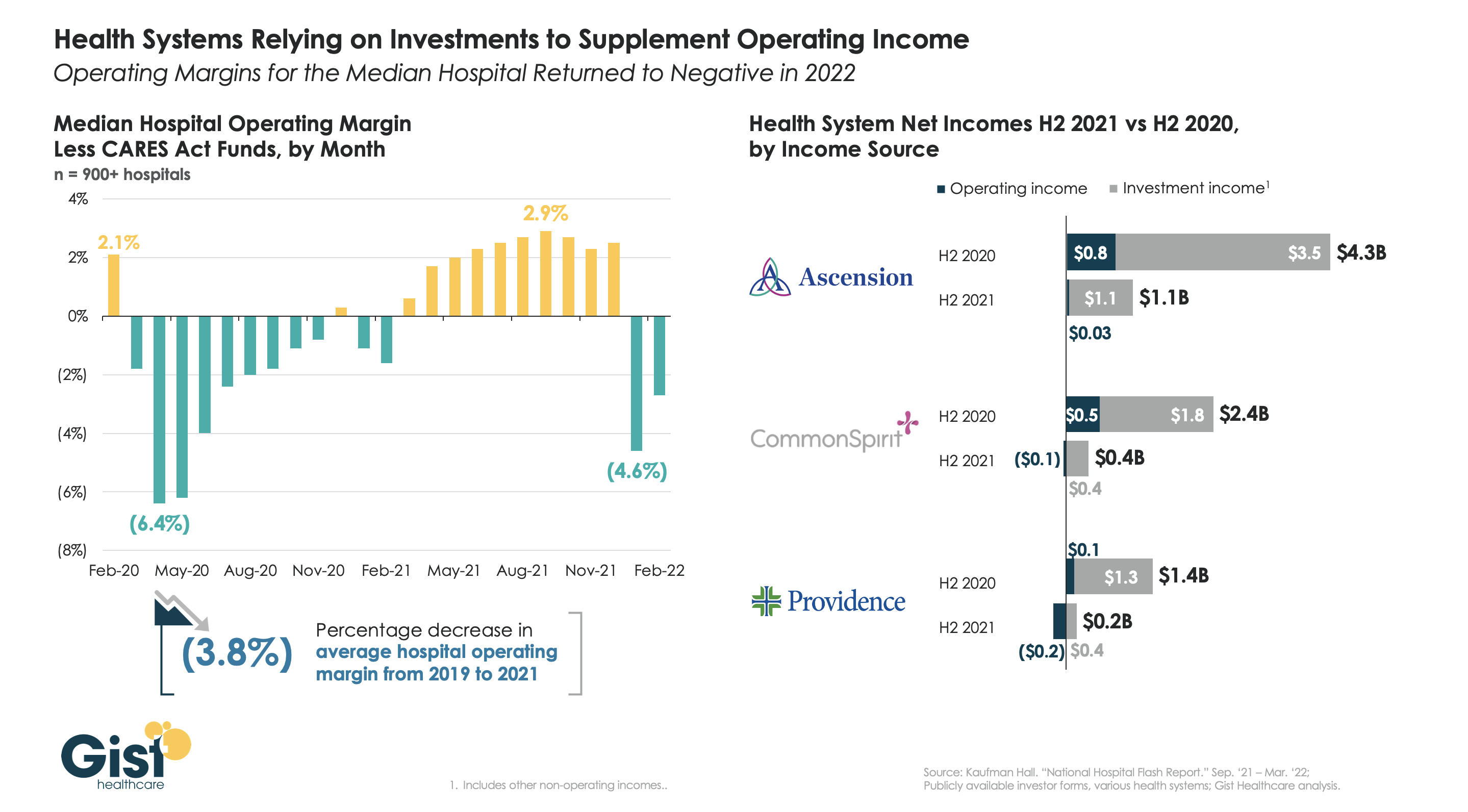

The combination of the Omicron surge, lackluster volume recovery, and rising expenses have contributed to a poor financial start of the year for most health systems. The graphic above shows that, after a healthier-than-expected 2021,the average hospital’s operating margin fell back into the red in early 2022, clocking in more than four percent lower than pre-pandemic levels.

Despite operational challenges, however, many of the largest health systems continue to garner headlines for their sizable profits, thanks to significant returns on their investment portfolios in 2021.

While CommonSpirit and Providence each posted negative operating margins for the second half of 2021, and Ascension managed a small operating profit, all three were able to use investment income to cushion their performance.

A growing number of health systems are doubling down on investment strategies in an effort to diversify revenue streams, and capture the kind of returns from investments generated by venture capital firms. However, it is unlikely that revenue diversification will be a sustainable long-term strategy.

To succeed, health systems must look to reconfigure elements of the legacy business model that are proving financially unsustainable amid rising expenses, shifts of care to lower-cost settings, and an evolving, consumer-centric landscape.

Judging from our recent conversations with health system executives, we’d guess CEOs across the industry woke up this morning glad to see the first quarter in the rearview mirror.

Almost everyone we’ve spoken to has told us that the past three months have been miserable from an operating margin perspective—skyrocketing labor costs, rising drug and supply prices, and stubbornly long length of stay, particularly among Medicare patients.

In the words of one CFO, “I’ve never seen anything like this. For the first time, we budgeted for a negative margin, and still didn’t hit our target. I’m not sure how long our board will let us stay on this trajectory before things change.”

Yet few of the drivers of poor financial performance appear to be temporary. Perhaps the over-reliance on agency nursing staff will wane as COVID volumes bottom out (for how long remains unknown), but overall labor costs will remain high, there’s no immediate relief for supply chain issues, and COVID-related delays in care have left many patients sicker—and thus in need of more costly care. Plus, the lifeline of federal relief funds is rapidly dwindling, if not already gone.

Expect the next three quarters (and beyond) to bring a greater focus on cost cutting, especially as not-for-profit systems struggle to defend their bond ratings in the face of rising interest rates.

Moody’s Investors Service has downgraded the ratings on Providence’s revenue bond debt to “A1” from “Aa3.”

“The downgrade to ‘A1’ is driven by the disaffiliation with Hoag Hospital, and the expectation that weaker operating, balance sheet, and debt measures will continue for the time being,” Moody’s said in an April 5 release.

Renton, Wash.-based Providence and Newport Beach, Calif.-based Hoag ended their affiliation Jan. 31. The two organizations cut ties at a time when Providence is facing several challenges, including operating pressures, variable utilization and reliance on temporary labor, Moody’s said.

The “A1” rating and stable outlook also reflect Providence’s strengths, including a large service area, a large revenue base of more than $25 billion and a leading market share in all of its markets.

Moody’s said it expects Providence to continue to grow its operating platform and generate additional revenue growth.

Hospitals across the U.S. saw their operating margins remain negative for the second consecutive month in February as they continued to feel the repercussions of the winter omicron surge, according to Kaufman Hall’s “National Hospital Flash Report: March 2022” posted March 28.

The median operating margin in February was -3.45 percent, up from -4.52 percent in January, but “still well below sustainable levels,” Kaufman Hall said.

Kaufman Hall said the improvement in hospital margin was driven by disproportionate increases among several hospitals that saw margin gains, but most hospitals reported margin declines in February. Specifically, the median operating margin was down 11.8 percent month over month.

“The second month of 2022 brought further challenges for the nation’s hospitals and health systems,” Kaufman Hall said. “Overall, the year is off to a difficult start.”

Kaufman Hall noted that patient days were down 13.3 percent month over month, and fewer severely ill COVID-19 patients also contributed to shorter hospital stays as the average length of stay dropped 5.3 percent month over month.

Hospitals’ gross operating revenue also decreased 7.4 percent compared to January 2022, with outpatient revenue falling 5 percent and inpatient revenue declining 19.3 percent.

Kaufman Hall noted that hospitals saw some improvement month over month in terms of expenses. Total expenses per adjusted discharge fell 4.5 percent compared to January, labor expense per adjusted discharge fell 6.1 percent and non-labor expenses per adjusted discharge was down 3.6 percent. However, Kaufman Hall noted that year over year, expenses are still up significantly, with total adjusted expense per adjusted discharge rising 10.4 percent compared to February 2021.

Insurers, retailers, and other healthcare companies vastly exceed health system scale, dwarfing even the largest hospital systems. The graphic above illustrates how the largest “mega-systems” lag other healthcare industry giants, in terms of gross annual revenue.

Amazon and Walmart, retail behemoths that continue to elbow into the healthcare space, posted 2021 revenue that more than quintuples that of the largest health system, Kaiser Permanente. The largest health systems reported increased year-over-year revenue in 2021, largely driven by higher volumes, as elective procedures recovered from the previous year’s dip.

However, according to a recent Kaufman Hall report, while health systems, on average, grew topline revenue by 15 percent year-over-year, they face rising expenses, and have yet to return to pre-pandemic operating margins.

Meanwhile, the larger companies depicted above, including Walmart, Amazon, CVS Health, and UnitedHealth Group, are emerging from the pandemic in a position of financial strength, and continue to double down on vertical integration strategies, configuring an array of healthcare assets into platform businesses focused on delivering value directly to consumers.

While many hospitals face financial hardships and rising expenses from the COVID-19 pandemic, several large health systems ended 2021 with profits above $1 billion.

These big health systems attributed the financial performance to several factors, including bigger investment gains and higher-acuity patients.

Seven health systems that posted net income of $1 billion last year:

1. Pittsburgh-based UPMC, an integrated delivery system with 40 hospitals, recorded a net income of $1.1 billion in 2021, driven by an operating income of $843 million and nonoperating gains of $810 million.

2. AdventHealth, a 48-hospital system based in Altamonte Springs, Fla., recorded a net income of $1.5 billion in 2021. The net income included an operating income of $994.6 million and investment gains of $517.7 million. In 2020, the health system’s net income was $914.8 million.

3. Cleveland Clinicreported a 66.7 percent increase in net income for the 12 months ended Dec. 31. The 19-hospital system saw its net income hit $2.2 billion, including an operating income of $746.3 million and investment gains of $1.4 billion.

4. Rochester, Minn.-based Mayo Clinic’s net income for 2021 was $3.6 billion, up from $2.5 billion a year earlier. The results included an operating income of $1.2 billion.

5. Driven by strong investment gains, Oakland, Calif.-based Kaiser Permanenterecorded a net income of $8.1 billion in 2021, an increase of $1.7 billion from 2020. The sharp rise in net income from the integrated delivery system with 39 hospitals included $7.5 billion in other income, including investment gains, and $611 million in operating income for 2021.

6. Nashville, Tenn.-based HCA Healthcare, a 182-hospital system, reported a net income of $7.7 billion in 2021, including investment gains and operating profits.

7. Tenet Healthcare, a 60-hospital system based in Dallas, reported net income of $1.5 billion on revenues of $19.5 billion in 2021. Tenet ended the 12-month period with an operating income of $2.9 billion, up from $2 billion recorded one year before. It also recorded losses on nonoperating activities and said its results for the year ending Dec. 31 included a pretax gain of $406 million associated with the divestiture of five Miami area hospitals, as well as stimulus funds totaling $205 million.

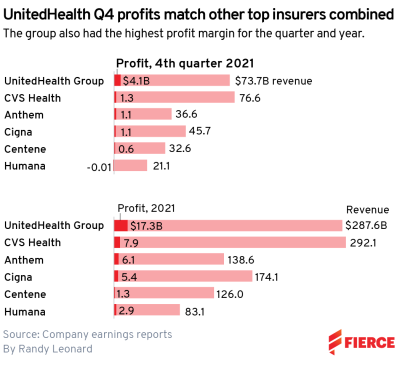

UnitedHealth Group was the most profitable payer in 2021, bringing in more than double the profit of itsnext-closest competitor with $17.3 billion in earnings.

CVS Health recorded the second-highest profit for the year among six major national insurers, earning $7.9 billion. CVS did bring in the highest revenue for the year, though, edging out UnitedHealth with $292.1 billion.

UHG reported $287.6 billion in revenue for 2021, according to the company’s earnings report.

Both healthcare giants expect to top $300 billion in revenue this year, according to their forecasts.

UnitedHealth was also the fourth quarter’s most profitable company, raking in $4.1 billion, which matched what its competitors earned combined, according to the filings.

UnitedHealth Group’s results represented significant growth over both the full-year and fourth quarter of 2020. According to its earnings report, this was driven in part by gains in Medicare Advantage and Medicaid at UnitedHealthcare as well as another quarter of double-digit growth at Optum.

CVS was also the next-highest earner in Q4, with $1.3 billion in profit on $76.6 billion in revenue. UHG was just behind on revenue with $73.7 billion.

CVS Health executives said that the retail business outperformed expectations in the fourth quarter amid increased demand for COVID-19 tests and booster shots.

The healthcare giant performed 32 million tests and 59 million vaccine doses over the course of the year, with 8 million tests and 20 million vaccinations reported in the fourth quarter alone.

While CVS and UnitedHealth duked it out for the top spot, all six of the big national payers were profitable for 2021, though Humana did post a $14 million loss for the fourth quarter.

Centene Corporation lands in sixth place for the year in profitability, bringing in $1.3 billion in profit on $126 billion in revenue. It also reported $599 million in profit for Q4.

Humana earned $2.9 billion for the year and $83.1 billion in revenue despite the Q4 loss, according to the company’s earnings report. Executives said the insurer braced for headwinds related to COVID-19 during the year and also saw disappointing growth in new Medicare Advantage members.

Anthem and Cigna fall in the middle of the pack, according to our review. They both reported about $1.1 billion in profit for Q4, though Cigna was ahead with $45.7 billion in revenue.

Anthemearned $6.1 billion in profit on $138.6 billion in revenue for the year, and executives shrugged off concerns about the Medicare Advantage market, saying its performance in open enrollment met expectations. In addition, it’s seeing growth at its in-house pharmacy benefit manager, IngenioRx, as it expands clientele.

Driven by strong investment gains, Oakland, Calif.-based Kaiser Permanente recorded a net income of $8.1 billion in 2021, an increase of $1.7 billion from 2020, according to its financial results released Feb. 11. However, its operating income fell sharply.

For the 12 months ended Dec. 31, the integrated healthcare provider with 39 hospitals recorded an operating revenue of $93.1 billion, up from $88.7 billion recorded last year. Additionally, Kaiser saw its expenses rise 6.9 percent to $92.5 billion in 2021.

In 2021, Kaiser saw its operating income fall to $611 million, an operating margin of 0.7 percent. This compares to a $2.2 billion operating income in 2020 and an operating margin of 2.5 percent.

Kaiser attributed the sharp decrease in operating income to an increase in care delivery expenses due to COVID-19 surges.

Total other income and expenses, which includes investment income, reached $7.5 billion in 2021. In 2020, Kaiser saw a gain of $4.1 billion.

“Our financial performance underscores the strength of our integrated model, which allows us to weather unexpected challenges such as the COVID-19 pandemic while continuing to serve our members,” said Kathy Lancaster, Kaiser Permanente executive vice president and CFO.

In 2021, Kaiser also said its health plan membership grew by 185,000 members. It now has more than 12.5 million members.

The second year of the pandemic did not dampen UnitedHealth Group’s finances, and the company actually surpassed its initial 2021 revenue and profit projections, Bob writes.

The big picture: UnitedHealth’s revenue has tripled from 2010 to 2021, and profit has almost quadrupled. The company continues to make more of its money from owning doctor groups and controlling pharmacy benefits instead of relying on health insurance.

Attending a recent executive retreat with one of our member health systems, we heard the CEO make a statement that really resonated with us. Referring to the current workforce crisis—pervasive shortages, pressure to increase compensation, outsized reliance on contract labor to fill critical gaps—the CEO made the assertion that this situation isn’t temporary. Rather, it’s the “new normal”, at least for the next several years.

The Great Resignation that’s swept across the American economy in the wake of COVID has not spared healthcare; every system we talk to is facing alarmingly high vacancy rates as nurses, technicians, and other staff head for the exits. The CEO made a compelling case that the labor cost structure of the system has reset at a level between 20 and 30 percent more expensive than before the pandemic, and executives should begin to turn attention away from stop-gap measures (retention bonuses and the like) to more permanent solutions (rethinking care models, adjusting staffing ratios upward, implementing process automation).

That seemed like an important insight to us. It’s increasingly clear as we approach a third year of the pandemic: there is no “post-COVID world” in which things will go back to normal. Rather, we’ll have to learn to live in the “new normal,” revisiting basic assumptions about how, where, and by whom care is delivered.

If hospital labor costs have indeed permanently reset at a higher level, that implies the need for a radical restructuring of the fundamental economic model of the health system—razor-thin margins won’t allow for business to continue as usual. Long overdue, perhaps, and a painful evolution for sure—but one that could bring the industry closer to the vision of “right care, right place, right time” promised by population health advocates for over a decade.