The nonprofit health system narrowed its operating loss while continuing to grapple with financial and policy pressures as it progresses towards profitability.

KEY TAKEAWAYS

Providence cut its operating loss in the second quarter to $21 million, improving from a $123 million loss a year ago.

Revenue rose 3% year-over-year to $7.91 billion, driven by higher patient volumes and better commercial rates.

The health system faces ongoing “polycrisis” challenges, including rising supply costs, staffing mandates, insurer denials, and looming Medicaid cuts, which have already prompted layoffs, hiring pauses, and leadership restructuring.

Providence made promising strides toward financial sustainability in the second quarter as higher patient volumes helped trim an operating loss that has weighed heavily on its balance sheet.

Yet the Renton, Washington-based health system warned that a compounding set of external pressures, which it labeled a “polycrisis,” still poses formidable challenges to its mission and future.

For the three months ended June 30, the nonprofit reported an operating loss of $21 million, equating to an operating margin of –0.3%, representing a marked improvement from the $123 million loss (–1.6%) posted over the same period in 2024. Compared with the previous quarter, the gain was even starker as Providence trimmed its deficit by $223 million. Through the first six months of the year, the health system had an operating loss of $265 million (-1.7%).

Revenue growth was fueled by higher patient volumes and improved commercial rates, Providence highlighted. Operating revenue rose 3% year-over-year to $7.91 billion as inpatient admissions (up 3%), outpatient visits (up 3%), case mix–adjusted admissions (up 3%), physician visits (up 8%), and outpatient surgeries (up 5%) all contributed.

On the expense side, Providence managed a 2% rise in operating costs to $7.93 billion, thanks largely to productivity gains, including a 43% reduction in agency contract labor. However, supply costs swelled by 9% and pharmacy expenses jumped by 12% year-over-year.

Providence, along with the healthcare industry at large, faces what CEO Erik Wexler called a “polycrisis” due to a mix of inflation, tariff-driven supply pressures, new state laws on staffing and charity care, insurer reimbursement delays and denials, and looming federal Medicaid cuts, especially from the One Big Beautiful Bill Act, which the health system said “threatens to intensify health care pressures.”

Those factors are significantly influencing hospitals’ and health systems’ decision-making. Providence has made staffing adjustments that include cutting 128 jobs in Oregon earlier this month, a restructuring in June that eliminated 600 full-time equivalent positions, apause on nonclinical hiring in April, and leadership reorganization since Wexler took over as CEO in January.

Accounts receivable is another area that has been indicative of headwinds, with Providence noting that while it improved in the second quarter, it “remains elevated compared to historical trends.”

Even with the roadblocks in its path, Providence is working towards profitability after being in the red for several years running.

“I’m incredibly proud of the progress we’ve made and grateful to our caregivers and teams across Providence St. Joseph Health for their continued dedication,” Wexler said in the news release. “The strain remains, especially with emerging challenges like H.R.1, but we will continue to respond to the times and answer the call while transforming for the future.”

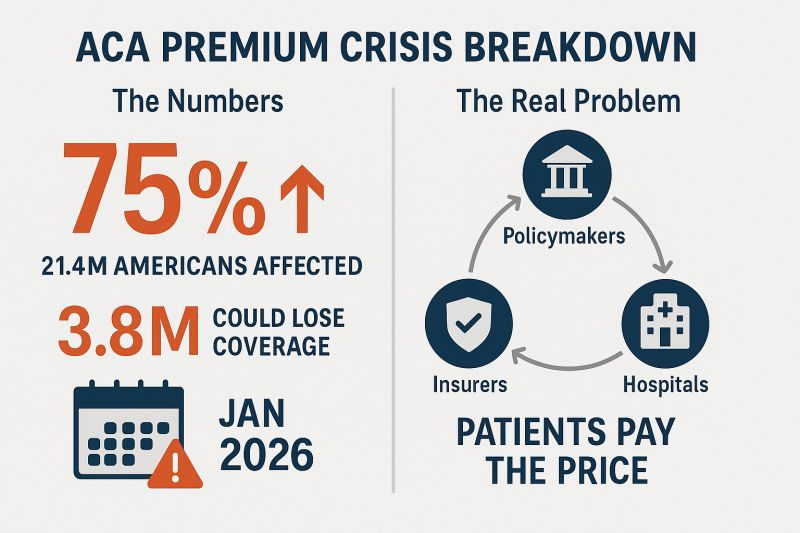

When Congress passed pandemic-era enhancements to Affordable Care Act (ACA) premium subsidies in 2021, it wasn’t just a policy tweak — it was a lifeline. But unless lawmakers act, those subsidies will vanish on January 1, 2026.

According to KFF, the average ACA enrollee could see premiums spike 75% overnight. For many, that will mean a choice between things like their health coverage and rent or food. The Congressional Budget Office estimates more than 4.2 million people could lose coverage over the next decade as a result. Below is where the expired subsidies will hurt the hardest:

1. Young adults… and their parents’ wallets

Young people who’ve aged out of their parents’ plans and buy coverage through the ACA marketplaces will see some of the steepest jumps.

If they decide to forgo coverage, as KFF Health News warns: The so-called “‘insurance cliff’ at age 26 can send young adults tumbling into being uninsured.”

The ACA is the only real option for many small-business owners, freelancers and gig workers. These are the folks that conservatives say we should encourage to build and grow their own businesses who make up the backbone of Main Street. Losing the enhanced subsidies means many will face premiums hundreds of dollars higher per month. Some will be forced to close shop and turn to jobs at out-of-town corporations flush enough to afford to offer subsidized coverage to their workers, a direct hit to local economies.

3. States already in crisis

States aren’t in a position to plug the gap.Politico reports that California, Colorado, Maryland, Washington, and others are scrambling to soften the blow, but even the most ambitious state-level plans can’t replace hundreds of millions in lost federal funding.

And this comes right after Medicaid cuts in the One Big Beautiful Bill Act that will hit hospitals, clinics and low-income communities. In Washington state alone, officials expect premiums to jump 75% when the subsidies expire, with one in four marketplace enrollees dropping coverage. That means more uninsured patients showing up in ERs, less preventive care, and more strain on already struggling rural hospitals.

4. (Already) disappearing alternatives to Big Insurance

The ACA marketplaces aren’t just a safety net for individuals but also home to smaller non-profit and regional health plans that give Americans an alternative to the “Big 7” Wall Street-run insurance conglomerates. These community-rooted plans are already facing financial headwinds from shrinking enrollment and Medicaid funding cuts. When premiums spike in 2026, many could lose enough members to be forced out of the market entirely.

And here’s the real danger: The Big 7 can weather this storm. Their huge market capitalizations, government contracts, pharmacy benefit manager (PBM) divisions and sprawling care delivery businesses give them insulation from ACA marketplace losses. In fact, they may see this as an opportunity to buy up the smaller competitors that fail, which would further consolidate their dominance over our health care system. Or they could just decide to flee the ACA marketplace entirely because the population will skewer sicker and older, creating a death spiral that the big insurers will not want to touch. What little consumer choice exists outside the big corporate insurers could vanish, and even that could disappear.

5. <65 year olds

Perhaps the most vulnerable group will be Americans in their 50s and early 60s who lose their jobs or retire early (often not by choice) and find themselves too young for Medicare but facing incredibly high premiums on the individual market. Under ACA rules, insurers can charge older enrollees up to three times more than younger adults for the same coverage. The enhanced subsidies have been the only thing keeping many of these premiums within reach.

Take those subsidies away, and a 60-year-old who loses employer coverage could see their monthly premium shoot into four figures. For those living off severance, savings or reduced income, choosing to gamble with their health and wait it out until 65 may be the only option.

Congress knows the stakes. Will they act?

Making the subsidies permanent would cost $383 billion over 10 years, which would be a political hurdle for a Congress intent on deep budget cuts. But the cost of inaction is far higher, both in human and economic terms. These subsidies have kept coverage affordable for millions, fueled small business growth, and stabilized state health systems during one of the most turbulent economic periods in recent memory. Without them, the hit to many folks could be a Frazier-level K.O.

But let’s face it — what I’m advocating for isn’t perfect either. The prospect of extending these subsidies raises a question: Should taxpayers be footing the bill for health insurance premiums when insurance corporations are reporting tens of billions in annual profits and paying hefty dividends to shareholders?

The short answer, for now, unfortunately, is yes. Because this is the deck we’ve been dealt and we can’t let Americans fall into medical debt, lose their homes – or their lives. Extending the ACA subsidies is not pretty. But for Americans, it’s just a bob and weave.

Self-dealing is illegal in banks, real estate, and investment firms, but in health insurance, it’s not only legal, it’s widespread. Large insurers have spent decades consolidating the U.S. health care system, acquiring medical practices, pharmacies, and pharmacy benefit managers, all while sidestepping rules meant to protect patients and taxpayers.

For example, UnitedHealth Group has 2,694 subsidiaries, as documented in the Center for Health and Democracy’s Sunlight Report on UnitedHealth Group. Within this conglomerate, there are 589 clinician practice locations across 32 states acquired between 2007 and 2023. UnitedHealth Group also has 24 subsidiary pharmacy benefit managers and over 30 subsidiary pharmacies. Data and insider accounts suggest that UnitedHealth Group and other vertically integrated insurers engage in self-dealing to increase profits. The ways these subsidiaries interact closely resembles self-dealing practices that are prohibited by law in other industries, such as banking, real estate, and investment firms.

As Dr. Seth Glickman and I have explained in earlier pieces, when a health insurer owns or controls medical practices, pharmacy benefit managers, or pharmacies, it can circumvent medical loss ratio (MLR) regulations. MLR rules require insurance companies to spend 80–85% of premium dollars on medical costs, leaving the remainder for administrative fees and profits. Unitedhealth Group, for instance, reportedly pays its own subsidiary providers above-market rates for medical services. These payments count as “medical costs” under MLR rules, yet the subsidiaries retain the excess as profit. Similarly, when a patient uses Optum Rx, a UnitedHealth Group subsidiary, or a subsidiary pharmacy, the fees added by the PBM are counted as medical costs, even though they are retained as profit by the parent company.

In banking, such actions are expressly prohibited. Consider a bank CEO who owns a real estate development company and seeks a loan for a risky project. If the bank lends to the CEO’s company at a below-market interest rate, the loan violates federal law and could trigger millions in fines as well as civil and criminal charges for both the CEO and the bank. This scenario parallels UnitedHealth Group’s current operations. In both cases, customer money (depositor funds in a bank; premium dollars in insurance) is used to funnel profit to insiders or affiliates, bypassing the market discipline that governs arm’s-length transactions.

Real estate law similarly prohibits self-dealing. Imagine a real estate agent hired to sell a client’s home who secretly buys the property through an affiliate at a lower price than the market reflects. By underrepresenting the home’s value, the agent enriches themselves at the client’s expense. This violates state real estate laws and common law fiduciary duties. The parallel in Insurance is clear: insurers pay inflated prices to their owned practices, driving up care costs and premiums. In both cases, the fiduciary is using client assets (property or premium dollars) to generate hidden profits for themselves or their affiliates, avoiding fair-market competition.

Investment advisers are also prohibited from similar practices. If you hire a broker to get the best price for a stock trade, the broker cannot quietly route the trade to an affiliate at a worse price so the affiliate profits. Even small losses per trade scale into substantial gains for the broker’s affiliate, all at the client’s expense. These actions violate the Investment Advisers Act of 1940, the Securities Exchange Act of 1934, and SEC rules when proper disclosure or consent is not obtained. Similarly, insurers use premium dollars to channel profits to subsidiaries instead of relying on competitive market pricing.

The stark parallels between self-dealing in banks, real estate, and investment brokerages, which Congress regulated decades ago, and health insurance are damning. Health insurance conglomerates have built empires on paying themselves to the detriment of patients and taxpayers. Congress must act to regulate this type of self-dealing in insurance as it does in other industries.

Moreover, the depth of insurer control over the patient care system necessitates regulations to prevent vertical monopolies, where insurers dominate every stage of care delivery.

People who buy health insurance through the Affordable Care Act (ACA) are set to see a median premium increase of 18 percent, more than double last year’s 7 percent median proposed increase, according to an analysis of preliminary filings by KFF.

The proposed rates are preliminary and could change before being finalized in late summer. The analysis includes proposed rate changes from 312 insurers in all 50 states and DC.

It’s the largest rate change insurers have requested since 2018, the last time that policy uncertainty contributed to sharp premium increases. On average, ACA marketplace insurers are raising premiums by about 20 percent in 2026, KFF found.

Insurers said they wanted higher premiums to cover rising health care costs, like hospitalizations and physician care, as well as prescription drug costs. Tariffs on imported goods could play a role in rising medical costs, but insurers said there was a lot of uncertainty around implementation, and not many insurers were citing tariffs as a reason for higher rates.

But they are adding in higher increases due to changes being made by the Trump administration and Republicans in Congress. For instance, the majority of insurers said they are taking into account the potential expiration of enhanced premium tax credits.

Those subsidies, put in place during the COVID-19 pandemic, are set to expire at the end of the year, and there are few signs that Republicans are interested in tackling the issue at all.

If Congress takes no action, premiums for subsidized enrollees are projected to increase by over 75 percent starting in January 2026, according to KFF.

But some states are pushing back.

Arkansas Gov. Sarah Huckabee Sanders (R) on Wednesday called on the state’s insurance commissioner to disapprove the proposed increases from Centene and Blue Cross Blue Shield. The companies filed increases of up to 54 percent and 25.5 percent, respectively, she said.

“Arkansas’ Insurance Commissioner is required to disapprove of proposed rate increases if they are excessive or discriminatory, and these are both,” Huckabee Sanders said in a statement.

“I’m calling on my Commissioner to follow the law, reject these insane rate increases, and protect Arkansans.”

Ahead of my Congressional testimony last week before the Senate HELP committee, I compiled data on the profits, revenues and CEO compensations of big health insurers in 2024. The curiosity from senators on both sides of the aisle signaled, to me, that lawmakers are as interested as I’ve ever seen in the industry’s rampant profiteering.

What I found was that the seven biggest publicly traded health insurance companies collectively made $71.3 billion in profits, up more than half a billion dollars from 2023. All while millions of Americans continued to skip their medications, rationed insulin and delayed care due to insurers’ out-of-pocket demands.

Let’s break it down.

You won’t be surprised to learn that shareholders are not the only ones benefiting from the care-restricting barriers insurers have erected to boost profits. The CEOs of those seven companies took home a combined $146.1 million in 2024 compensation. That’s enough to cover annual premiums for thousands of American families.

Here’s what the top brass made:

Meanwhile, patients across the country report increasing out-of-pocket costs, more aggressive prior authorizations and narrower provider networks. But for these executives, the real measure of success is how high they can push their stock prices and not how many people can afford to see a doctor.

So, What’s Driving the Revenue Surge?

One word: Gouging.

Insurers continued to jack up premiums for their commercial customers and overcharge the government. Despite watchdog warnings, Uncle Sam continues to pour money into private Medicare Advantage plans even as audits and investigations uncover widespread fraud and upcoding. And Medicaid managed care is a gold mine, too. These insurers now dominate state Medicaid contracts and can quietly extract billions through behind-the-scenes ownership of pharmacies, PBMs and providers.

It’s not just health insurance anymore — it’s a monopolized empire.

All that said, to the dismay of shareholders, the big seven insurers have had to admit that so far in 2025, they’ve paid more medical claims than they had expected, which means their profits were down somewhat during the first months of the year. I’ll shed more light on that in a future post. No need for you to shed any tears for them, though, because we’re still talking billions and billions in profits.

So if you’re wondering why your premiums, deductibles and costs at the pharmacy counter keep going up — just look at those 2024 numbers. We all paid more for health insurance and got less for the hard-earned money we had to shovel out for our “coverage.”

And expect even more financial pain (and difficulty getting the care you need) as these companies do all they can to get their profit margins back to where Wall Street wants them.

President Donald Trump has made big promises about fixing American healthcare. Now comes the moment that separates talk from action.

With the 2026 midterms fast approaching and congressional attention soon shifting to electoral strategy, the window for legislative results is closing quickly. This summer will determine whether the administration turns promises into policy or lets the opportunity slip away.

Trump and his handpicked healthcare leaders — HHS Secretary Robert F. Kennedy Jr. and FDA Commissioner Dr. Marty Makary — have identified three major priorities: lowering drug prices, reversing chronic disease and unleashing generative AI. Each one, if achieved, would save tens of thousands of lives and reduce costs.

But promises are easy. Real change requires political will and congressional action. Here are three tests that Americans can use to gauge whether the Trump administration succeeds or fails in delivering on its healthcare agenda.

Test No. 1: Have Drug Prices Come Down?

Americans pay two to four times more for prescription drugs than citizens in other wealthy nations. This price gap has persisted for more than 20 years and continues to widen as pharmaceutical companies launch new medications with average list prices exceeding $370,000 per year.

One key reason for the disparity is a 2003 law that prohibits Medicare from negotiating prices directly with drug manufacturers. Although the Inflation Reduction Act of 2022 granted limited negotiation rights, the initial round of price reductions did little to close the gap with other high-income nations.

President Trump has repeatedly promised to change that. In his first term, and again in May 2025, he condemned foreign “free riders,” promising, “The United States will no longer subsidize the healthcare of foreign countries and will no longer tolerate profiteering and price gouging.”

To support these commitments, the president signed an executive order titled “Delivering Most-Favored-Nation (MFN) Prescription Drug Pricing to American Patients.” The order directs HHS to develop and communicate MFN price targets to pharmaceutical manufacturers, with the hope that they will voluntarily align U.S. drug prices with those in other developed nations. Should manufacturers fail to make significant progress toward these targets, the administration said it plans to pursue additional measures, such as facilitating drug importation and imposing tariffs. However, implementing these measures will most likely require congressional legislation and will encounter substantial legal and political challenges.

The pharmaceutical industry knows that without congressional action, there is no way for the president to force them to lower prices. And they are likely to continue to appeal to Americans by arguing that lower prices will restrict innovation and lifesaving drug development.

But the truth about drug “innovation” is in the numbers: According to a study by America’s Health Insurance Plans, seven out of 10 of the largest pharmaceutical companies spend more on sales and marketing than on research and development. And if drugmakers want to invest more in R&D, they can start by requiring peer nations to pay their fair share — rather than depending so heavily on U.S. patients to foot the bill.

If Congress fails to act, the president has other tools at his disposal. One effective step would be for the FDA to redefine “drug shortages” to include medications priced beyond the reach of most Americans. That change would enable compounding pharmacies to produce lower-cost alternatives just as they did recently with GLP-1 weight-loss injections.

If no action is taken, however, and Americans continue paying more than twice as much as citizens in other wealthy nations, the administration will fail this crucial test.

Test No. 2: Did Food Health, Quality Improve?

Obesity has become a leading health threat in the United States, surpassing smoking and opioid addiction as a cause of death.

Since 1980, adult obesity rates have surged from 15% to over 40%, contributing significantly to chronic diseases, including type 2 diabetes, heart disease and multiple types of cancers.

A major driver of this epidemic is the widespread consumption of ultra-processed foods: products high in added sugar, unhealthy fats and artificial additives. These foods are engineered to be hyper-palatable and calorie-dense, promoting overconsumption and, in some cases, addictive eating behaviors.

RFK Jr. has publicly condemned artificial additives as “poison” and spotlighted their impact on children’s health. In May 2025, he led the release of the White House’s Make America Healthy Again (MAHA) report, which identifies ultra-processed foods, chemical exposures, lack of exercise and excessive prescription drug use as primary contributors to America’s chronic disease epidemic.

But while the report raises valid concerns, it has yet to produce concrete reforms.

To move from rhetoric to results, the administration will need to implement tangible policies.

Here are three approaches (from least difficult to most) that, if enacted, would signify meaningful progress:

Front-of-package labeling. Implement clear and aggressive labeling to inform consumers about the nutritional content of food products, using symbols to indicate healthy versus unhealthy options.

Taxation and subsidization. Impose taxes on unhealthy food items and use the revenue to subsidize healthier food options, especially for socio-economically disadvantaged populations.

Regulation of food composition. Restrict the use of harmful additives and limit the total amount of fat and sugar included, particularly for foods aimed at kids.

These measures will doubtlessly face fierce opposition from the food and agriculture industries. But if the Trump administration and Congress manage to enact even one of these options — or an equivalent reform — they can claim success.

If, instead, they preserve the status quo, leaving Americans to decipher nutritional fine print on the back of the box, obesity will continue to rise, and the administration will have failed.

Test No. 3: Are Patients Using Generative AI To Improve Health?

The Trump administration has signaled a strong commitment to using generative AI across various industries, including healthcare. At the AI Action Summit in Paris, Vice President JD Vance made the administration’s agenda clear: “I’m not here this morning to talk about AI safety … I’m here to talk about AI opportunity.”

FDA Commissioner Dr. Marty Makary has echoed that message with internal action. After an AI-assisted scientific review pilot program, he announced plans to integrate generative AI across all FDA centers by June 30.

But internal efficiency alone won’t improve the nation’s health. The real test is whether the administration will help develop and approve GenAI tools that expand clinical access, improve outcomes and reduce costs.

To these ends, generative AI holds enormous promise:

Managing chronic disease: By analyzing real-time data from wearables, GenAI can empower patients to better control their blood pressure, blood sugar and heart failure. Instead of waiting months between doctor visits for a checkup, patients could receive personalized analyzes of their data, recommendations for medication adjustments and warnings about potential risk in real time.

Improving diagnoses: AI can identify clinical patterns missed by humans, reducing the 400,000 deaths each year caused by misdiagnoses.

Personalizing treatment: Using patient history and genetics, GenAI can help physicians tailor care to individual needs, improving outcomes and reducing side effects.

These breakthroughs aren’t theoretical. They’re achievable. But they won’t happen unless federal leaders facilitate broad adoption.

That will require investing in innovation. The NIH must provide funding for next-generation GenAI tools designed for patient empowerment, and the FDA will need to facilitate approval for broad implementation. That will require modernizing current regulations. The FDA’s approval process wasn’t built for probabilistic AI models that rely on continuous application training and include patient-provided prompts. Americans need a new, fit-for-purpose framework that protects patients without paralyzing progress.

Most important, federal leaders must abandon the illusion of zero risk. If American healthcare were delivering superior clinical outcomes, managing chronic disease effectively and keeping patients safe, that would be one thing. But medical care in the United States is far from that reality. Hundreds of thousands of Americans die annually from poorly controlled chronic diseases, medical errors and misdiagnoses.

If generative AI technology remains confined to billing support and back-office automation, the opportunity to transform American healthcare will be lost. And the administration will have failed to deliver on this promise.

When I teach strategy at Stanford’s Graduate School of Business, I tell students that the best leaders focus on a few high-priority goals with clear definitions of success — and a refusal to accept failure. Based on the administration’s own words, grading the administration on these three healthcare tests will fulfill those criteria.

However, with Labor Day just months away, the window for action will soon close. The time for presidential action is now.

July 2025 will be the month U.S. healthcare leaders recognize as the industry’s modern turning point. Consider…

On July 4, the One Big Beautiful Bill Act was signed into law setting in motion $960 billion in Medicaid cuts over the decade and massive uncertainty among those most adversely impacted—low income and under-served populations dependent on public programs, 8 to 11 million who used now-suspended marketplace subsidies to buy insurance coverage, and hundreds of state and local health agencies left in funding limbo.

On July 15, the Bureau of Labor Statistics reported the June Consumer Price Index rose .3% bumping the LTM to 2.7% (lower than LTM of 3.4% for medical services). Prices have edged up.

On July 31, President Trump issued an Executive Order to 17 drug companies ordering them to reduce prices on their drugs by September 29 or else. And CMS issued final rules for FY2026 Medicare payments to hospitals, rehab and other providers reflecting increases ranging from 2.5-3.3% effective October 1.

And on the same day, the Bureau of Labor issued its July 2025 jobs report that showed a disappointing net gain of 73,000 jobs plus downward revisions for May and June of 258,000 sparking Wall Street anxiety and President Trump to call the results “rigged” before firing BLS head Erika McEntarfer. Note: healthcare added 55,000 in July—the biggest of any sector and more than its 42,000 average monthly increase.

Collectively, these actions reflect rejection of the health industry by the GOP-led Congress.

It follows 15 years of support vis a vis the Affordable Care Act (2010) and pandemic recovery emergency funding (2020-2021). In that 15-year period, the bigger players got bigger in each sector, investment of private equity in each sector became more prevalent, costs increased, affordability for consumers and employers decreased, and the public’s overall satisfaction with the health system declined precipitously.

For the four major players in the system, the passage of the “big, beautiful bill” was a disappointment. Their primary concerns were not addressed:

Physicians wanted relieffrom annual payment cuts by Medicare preferring reimbursement tied directly to medical inflation. And insurer’ prior authorization and provider reimbursement was a top issue. Status: Not much has changed though adjustments are promised.

Hospitals wanted continuation of federal Medicaid funding, protection of the 340B drug purchasing program, rejection of site-neutral payment policies, higher Medicare reimbursement and relief from insurer prior authorization frustrations. Status: Medicaid funding is being cut forcing the issue for states. CMS payment increases for 2026 are lower than operating cost increases. Insurers have promised prior-auth relief but details about how and when are unknown. And Congress posture toward hospitals seems harsh: price transparency compliance, safety event reporting, and cost concerns are bipartisan issues.

Insurers wanted sustained funding for state Medicaid and Medicare Advantage programs and federal pushback against drug prices and hospital consolidation. Status: Congress appears sympathetic to enrollee complaints and anxious to address insurer “waste, fraud and abuse” including overpayments in Medicare Advantage.

Drug companies oppose “Most Favored Nation” pricing and want protections of their patents and limits on how much insurers, pharmacy benefits managers, wholesalers, online distributors and other “middlemen” earn at their expense. Status: to date, little action despite sympathetic rhetoric by lawmakers. Status: to date, Congress has taken nominal action beyond the Inflation Reduction Act (2022) though 23 states have passed legislation requiring PBMs, insurers and manufacturers to disclose drug prices and 12 states have established Prescription Drug Affordability Boards to monitor prices.

My take:

The landscape for U.S. healthcare is fundamentally changed as a result of the July actions noted above. It is compounded by public anxiety about the economy at home and global tensions abroad.

These July actions were a turning point for the industry: responding appropriately will require fresh ideas and statesmanship. Transparency about prices, costs, incentives and performance is table stakes. Leaders dedicated to the greater good will be the difference.