Walmart Health opened three new clinics in Jacksonville, Fla., starting June 6 as the company continues its push into retail healthcare, the Florida Times-Union reported.

The retail giant now has more than 30 Walmart Health centers across Florida, Arkansas, Georgia, Illinois and Texas, with plans to grow to 77 by the end of 2024 and expand into Arizona and Missouri.

Florida is one of Walmart Health’s biggest markets, with 22 coming to the state by fall 2023. They are also located in the Orlando and Tampa metro areas. They include medical, dental, vision, hearing and behavioral health services.

“With only one primary care doctor per 1,380 Florida residents, these Walmart Health centers will help address the demand for care in three major cities in the Sunshine State,” David Carmouche, MD, senior vice president of omnichannel care offerings for Walmart, said in a 2022 Times-Unionstory. “We are part of these communities, and we are excited to bring more options for in-person and telehealth care services to our neighbors. We’re making healthcare available when and where you may need it.”

Academic medicine combines healthcare with higher education, the two sectors of the American economy that have exhibited outsized cost growth during the past 50 years. The result is a stunning disconnection between the business practices of academic medical centers (AMCs) and the supply-demand dynamics reshaping healthcare delivery.

Market, technological and regulatory forces are pushing the healthcare industry to deliver higher-value care that generates better outcomes at lower costs. A parallel movement is shifting resources out of specialty and acute care services into primary, preventive, behavioral health and chronic disease care services. In the process, care delivery is decentralizing and becoming more consumer-centric.

AMCs Double Down

Counter to these trends, academic medicine is doubling down on high-cost, centralized, specialty-focused care delivery. Privilege has its price. Several AMCs — including Mass General Brigham, IU Health, UCSF, Ohio State and UPMC — are undertaking multibillion-dollar expansions of their existing campuses. Collectively, AMCs expect American society to fund their continued growth and profitability irrespective of cost, effectiveness and contribution to health status.

Despite being tax-exempt and having access to a large pool of free labor (residents), AMCs charge the highest treatment prices in most markets. [1] Archaic formulas allocate residency “slots” and lucrative Graduate Medical Education payments (over $20 billion annually) disproportionately into specialty care and more-established AMCs. Given their cushy funding arrangements, it’s no wonder AMCs fight vigorously to maintain an out-of-date status quo.

Legacy practices from the early 1900s still dominate medical education, medical research and clinical care. Like tenured faculty, academic physicians manage their practices with little interference. Clinical deans rule their departments with a free hand. With few exceptions, interdisciplinary coordination is an oxymoron. The result is fragmented care delivery that tolerates duplication, medical error and poor patient service.

Irresistible consumerism confronts immovable institutional inertia. As exhibited by substantial operating losses at many AMCs, their foundations are beginning to crack. [2]

Medicine’s Rise from Poverty to Prosperity

In his 1984 Pulitzer Prize-winning work, Paul Starr chronicles the social transformation of American medicine during the 19th and 20th centuries. Prior to the 1900s, doctors had low social status. Most care took place in the home. Pay was low. The profession lacked professional standards. There were too many quacks. Most doctors lived hand-to-mouth.

As the century turned, several cultural, economic, scientific and legal developments converged to elevate the profession’s status in American society. Stricter licensing reduced the supply of physicians and closed most existing medical schools. Legislation and legal rulings restricted corporate ownership of medical practices and enshrined physicians’ operating autonomy. Scientific breakthroughs gave medicine more healing power.

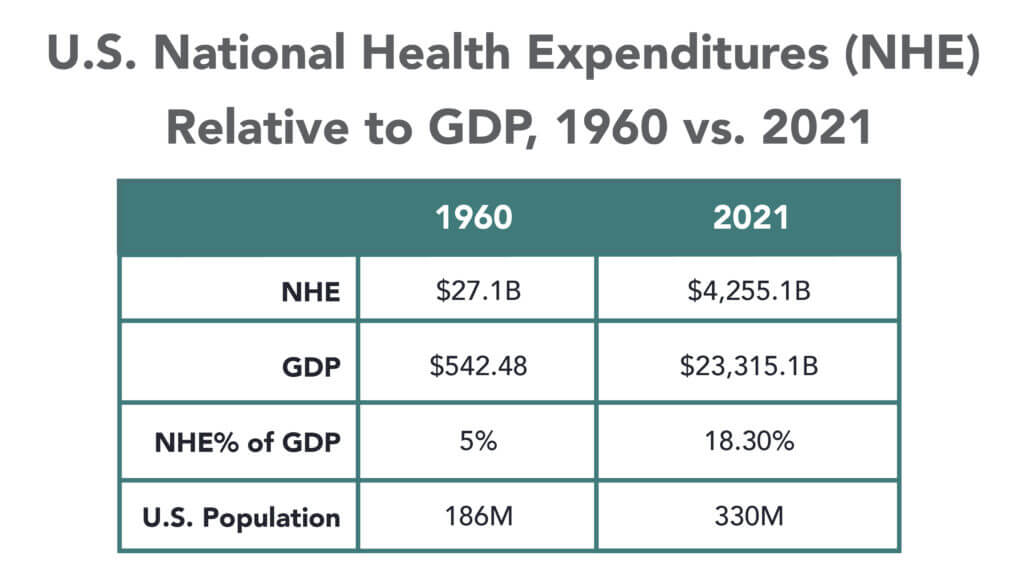

Through the decades that followed, the American Medical Association and state medical societies frustrated external attempts to control medical delivery externally and institute national health insurance. They insisted on fee-for-service payment and the absolute right of patients to choose their doctors. These are causal factors underlying healthcare’s skyrocketing cost increases, growing from 5% of the U.S. gross domestic product (GDP) in 1960 to over 18% in 2021.

Academic and community-based physicians have always had a tenuous relationship. Status and prestige accompany academic affiliations. Academic practices require referrals from community physicians but rarely consult with them on treatment protocols. For their part, community physicians marvel at the lack of market awareness exhibited by academic practices. They have tolerated one another to perpetuate collective physician control over healthcare operations.

Incomes and prestige for both community and academic physicians rose as the medical profession limited practitioner supply, established payment guidelines, encouraged specialization, controlled service delivery and socialized capital investment. One hundred years later, the business of healthcare still exhibits these characteristics. Gleaming new medical centers testify to the profession’s success in socializing capital investment and maintaining autonomy over hospital operations.

Entrenched beliefs and behaviors explain why most hospitals, despite their high construction costs, are largely deserted after 4 p.m. and on weekends. They explain the maldistribution of facilities and practitioners. They explain the overdevelopment of specialty care. They explain the underinvestment in preventive care, mental health services and public health.

Value-Focused Backlash Portends Reckoning

These beliefs and behaviors are contributing to AMC’s current economic dislocation. Dependent upon public subsidies and premium treatment payments to maintain financial sustainability, high-cost AMCs are particularly vulnerable to value-based competitors.

The marketplace is attacking inefficient clinical care with tech-savvy, consumer-friendly business models. Care delivery is decentralizing even as many AMCs invest more heavily in campus-based medicine. A market-based reckoning confronts academic medicine.

A visit up north illustrates the general unwillingness of academic physicians to accept market realities and their continued insistence on maintaining full control over the academic medical enterprise. It’s like watching a train wreck occur in slow motion.

Minnesota Madness

After experiencing severe economic distress, the University of Minnesota sold its University of Minnesota Medical Center (UMMC) to Fairview Health in 1997. Fairview currently operates UMMC in partnership with the University of Minnesota Physicians (UMP) under the banner of M Health Fairview.

In September 2022, Sanford Health and Fairview Health signed a letter of intent to merge. The new combined company would bear the Sanford name with its headquarters in Sioux Falls, South Dakota. Despite the opportunity to double its catchment area for specialty referrals, the University and UMP oppose the merger with Sanford. They fear out-of-state ownership could compromise the integrity of UMMC’s operations.

Fairview wants the Sanford merger to help it address massive operating losses resulting, in part, from its contractual arrangements with UMP. Negotiations between the parties have become acrimonious. Amid the turmoil, the University and UMP announced in January 2023 their intention to acquire UMMC from Fairview and build a new state-of-the-art medical center on the University’s Minneapolis campus.

The University has named this proposal “MPact Health Care Innovation.” It calls for the Minnesota state legislature to fund the multibillion-dollar cost of acquiring, building and operating the new medical enterprise. Typical of academic medical practices, UMP expects external sources to pony up the funding to support their high-cost centralized business model while they continue to call the shots.

The arrogance and obliviousness of the University’s proposal is staggering. Minnesota struggles with rising rates of chronic disease and inequitable healthcare access for low-income urban and rural communities. The idea that a massive governmental investment in academic medicine will “bridge the past and future for a healthier Minnesota” as the MPact tagline proclaims is ludicrous.

Out of Touch

Like the rest of the country, Minnesota is experiencing declining life expectancy. Despite spending more than double the average per-capita healthcare cost of other wealthy countries, the United States scores among the worst in health status measures. Spending more on high-end academic medicine won’t change these dismal health outcomes. Spending more on preventive care, health promotion and social determinants of health could.

The real gem in the University of Minnesota’s medical enterprise is its medical school. It has trained 70% of the state’s physicians. It ranks third and fourth nationally in primary care and family medicine. It is advancing a progressive approach to interdisciplinary and multi-professional care.

If the Minnesota state legislature really wants to advance health in Minnesota, it should expand funding for the University’s aligned health schools and community-based programs without funding the acquisition and expansion of the University’s clinical facilities.

No Privilege Without Performance

Our nation must stop enabling academic medicine’s excesses. Funding AMCs’ insatiable appetite for facilities and specialized care delivery is counterproductive. It is time for academic medicine to embrace preventive health, holistic care delivery and affordable care access.

Privilege comes with responsibility. AMCs that resist the pivot to value-based care and healthier communities deserve to lose market relevance.

America has the means to create a healthier society. It requires shifting resources out of healthcare into public health. We must have the will to make community-based health networks a reality. It starts by saying no to needless expansion of acute care facilities.

In the mid-1980’s, managed care advocate Dr. Paul Ellwood predicted that eventually, US healthcare would be dominated by perhaps a dozen vast national firms he called SuperMeds that would combine managed care based health insurance with care delivery systems. Ellwood was a leader of the “managed competition” movement which advocated for a private sector alternative to a federal government-run National Health Insurance system. Ellwood and colleagues believed that Kaiser Foundation Health Plans and other HMOs would be able to stabilize health costs and thus affordably extend care to the uninsured.

The US political system and market dynamics would not co-operate with Ellwood and his Jackson Hole Group’s vision. In the ensuing thirty-five years, healthcare has remained both highly fragmented and regional in focus. However, unbeknownst to most, during the past decade, as a result of a major merger and relentless smaller acquisitions, two SuperMeds were born- CVS/Aetna and UnitedHealth Group, that whose combined revenues comprise 14% of total US health spending.

CVS/Aetna is slightly larger than United, by dint of grocery sales in its drugstores and its vast Caremark pharmacy benefits management business. However, CVS’s Aetna health insurance arm is one third the size of United’s, and though CVS is rapidly scaling up its care delivery apparatus through its in-store Health Hubs, it remains is a tiny fraction of United’s care footprint. Despite being slightly smaller at the top line, United’s market capitalization is more than 3.5 times that of CVS.

United’s vast scope is difficult to comprehend because much of it is not visible to the naked eye, and the most rapidly growing businesses are partly nested inside United’s health insurance business.

United employs over 300 thousand people. At $287.6 billion total revenues in 2021, United exceeded 7% of total US health spending (though $8.3 billion are from overseas operations).

In 2021, United was $100 billion larger than the British National Health Service. It is more than three times the size of Kaiser Permanente, and five times the size of HCA, the nation’s largest hospital chain. United is both larger and richer than energy giant Exxon Mobil. United has over $70 billion in cash and investments, and is generating about $2 billion a month in operating cash flow.

Its highly regulated health insurance business is the visible tip of a rapidly growing iceberg. Revenue from United’s core health insurance business grew at 11% in 2021, compared to 14% growth in United’s diversified Optum subsidiary. Optum generated $155.6 billion in 2021 (of which 60% were from INSIDE United’s health insurance business). You can see the relationship of Optum’s three major businesses to United’s health insurance operations in Exhibit I.

Optum is the Key to United’s Growth

Understanding the role of Optum is key to understanding United’s business. It is remarkable how few of my veteran health care colleagues have any idea what Optum is or what it does. Optum was once a sort of dumping ground for assorted United acquisitions without a seeming core purpose. A private equity colleague once derided Optum as “The Island of Lost Toys”. Now, however, Optum is driving United’s growth, and generates billions of dollars in unregulated profits both from inside the highly regulated core health insurance business and from external customers.

Optum consists of three parts:Optum Health, its care delivery enterprise ($54 billion revenues in 2021), Optum Rx, its pharmacy benefits management enterprise ($91 billion revenues in 2021) and Optum Insight, a diversified business services enterprise ($12.2 billion in 2021). Virtually all of United’s acquisitions join one of these three businesses.

Optum Health: The Third Largest Care Delivery Enterprise in the US

By itself, Optum Health is almost the size of HCA ($54 billion in 2021 vs HCA’s $58.7 billion) and consists of a vast national portfolio of care delivery entities: large physician groups, urgent care centers, surgicenters, imaging centers, and now by dint of the recently announced $5.7 billion acquisition of LHC, home health agencies. Optum Health has studiously avoided acquiring beds of any kind: hospitals, nursing homes, etc. and likely will continue to do so. Optum Health’s physician groups not only generate profits on their own, but also provide powerful leverage for United to control health costs for its own subscribers, pushing down United’s highly visible and regulated Medical Loss Ratio (MLR), and increasing health plan profits.

Optum Health began in 2007 when United acquired Nevada-based Sierra Health, and thus became the new owner of a small multispecialty physician group which Sierra owned. The group did not belong in United’s health insurance business and came to rest over in Optum. Over the past twelve years, Optum Health has acquired an impressive percentage of the major capitated medical groups in the US- Texas’ WellMed, California’s HealthCare Partners (from DaVita), as well as Monarch, AppleCare and North American Medical Management, Massachusetts’ Reliant (formerly Fallon Clinic) and Atrius in Massachusetts (pending) , Kelsey Seybold Clinic (also pending) in Houston, TX and Everett Clinic and PolyClinic in Seattle.

Optum Health claims over 60 thousand physicians, though many of these are actually independent physicians participating in “wrap around” risk contracting networks. By comparison, Kaiser Permanente’s Medical Groups employ about 23 thousand physicians. United’s management claims that Optum Health provides continuing care to about 20 million patients, of whom 3 million are covered by some form of so-called “value based” contracts. Perhaps half of this smaller number are covered by capitated (percentage of premium-PMPM) contracts.

Optum Health straddles fierce competitive relationships between United’s health insurance business and competing health plans in well more than a dozen metropolitan areas. Almost half (44%) of Optum Health’s revenues come from providing care for health plans other than United.

When Optum acquires a large physician group, it acquires those groups’ contracts with United’s health insurance competitors, some of which contracts have been in place for decades. Premium revenues from other health plans, presumably capitation or per member per month (PMPM) revenues, are one-quarter of Optum Health’s $54 billion total revenues. These “external” premium revenues have quadrupled since 2018, largely for Medicare Advantage subscribers. Optum Health contributes about $4.5 billion in operating profit to United. It is impossible to determine from United’s disclosures how much of this profit comes from Optum Health’s services provided to United’s insured lives and how much from its medical groups’ extensive contracts with competing health plans.

Optum Health’s surgicenters and urgent care centers provide affordable alternatives to using expensive hospital outpatient services and emergency departments, potentially further reducing United medical expense. This creates obvious tensions with United’s hospital networks, since Optum Health can use its large medical practices and virtual care offerings to divert patients from hospitals to its own services, or else render those services unnecessary.

Though some observers have termed Optum/United’s business model “vertical integration”-ownership of the suppliers to and distributors of a firm’s product– Optum Health has actually grown less vertical since 2018, with revenues from competing health plans growing from 36% of total revenues in 2018 to 44% in 2021. A 2018 analysis by ReCon Strategy found at best a sketchy matchup between United’s health plan enrollment by market and its Optum Health assets (https://reconstrategy.com/2018/04/uniteds-medicare-advantage-footprint-and-optumcare-network-do-not-overlap-much-so-far/.

Optum Rx: The Nation’s Third Largest Pharmacy Benefits Management Business

Optum’s largest business in revenues is its Optum Rx pharmaceutical benefits management (PBM) business, which generates $91 billion in revenues, and processes over a billion pharmacy claims not only for United but also many competing insurers and employer groups. Pharmaceutical costs are a rapidly growing piece of total medical expenses, and controlling them is yet another source of largely unregulated profits for United; Optum Rx generated over $4.1 billion of operating profit in 2021.

Optum Rx is the nation’s third largest PBM business after Caremark, owned by CVS/Aetna and Express Scripts, owned by CIGNA, and processes about 21% of all scripts written in the US. Pharmacy benefits management firms developed more than two decades ago to speed the conversion of patients from expensive branded drugs to generics on behalf of insurers and self-funded employers. They were given a big boost by George Bush’s 2004 Medicare Part D Prescription Drug benefit, as a “pro-competitive” private sector alternative to Medicare directly negotiating prices with pharmaceutical firms.

Reducing drug spending is one key to United’s profitability. Since generics represent almost 90% of all prescriptions written, Optum Rx now relies on fees generated by processing prescriptions and on rebates from pharmaceutical firms to promote their costly branded drugs as preferred drugs on Optum Rx’s formularies. These rebates are determined based on “list” prices for those drugs vs. the contracted price for the PBMs, and are actual cash payments from manufacturers to PBMs.

Drug rebates represent a significant fraction of operating profits for health insurers that own PBMs, particularly for their older Medicare Advantage patients that use a lot of expensive drugs. Unfortunately, PBMs have incentives to inflate the list price, because rebates are caculated based on the spread between list prices and the contract pricel Unfortunately, this increases subscribers’ cash outlays, because patient cost shares are based on list prices.

Optum Rx generates about 39% of its revenues (and an undeterminable percentage of its profits) serving other health insurers and self-funded employers. Many of those self-funded employers demand that Optum pass through the rebates directly to them (even if it means being charged higher administrative fees!).

Unlike the situation with Optum Health, the “verticality” of Optum’s PBM business-the percentage of Optum revenues derived from serving United subscribers- has increased in the last seven years, to more than 60% of Optum Rx’s total business. What happens to the billions of dollars in rebates generated by Optum Rx is impossible to determine from United’s disclosures. However, our best guess is that pharmaceutical rebates represent as much as a quarter of United’s total corporate profits.

Optum Insight: “Intelligent” Business Solutions

The fastest growing and by far the most profitable Optum business is its business intelligence/business services/consulting subsidiary. Optum Insight was generated $12.2 billion in revenues in 2021, but a 27.9% operating margin, five times that of United’s health insurance business. Optum Insight is strategically vital to enhancing the profitability of United’s health insurance activities, but also generates outside revenues selling services to United’s health insurance competitors and hospital networks.

The core of Optum Insight is a business intelligence enterprise formerly known as Ingenix, which provided “big data” to United and other insurers about hospital and pricing behavior and utilization-crucial both for benefits design and administration. In 2009, Ingenix was accused by New York State of under reporting prices for out of network health services for itself and its clients, which had the effect of reducing its own medical reimbursements, and increasing patient cost shares. United signed a consent decree to alter Ingenix business practices and settled a raft of lawsuits filed on behalf of patients, physicians and employers. Its name was subsequently changed to Optum Insight.

By dint of aggressive acquisitions, Optum Insight has dramatically increased its medical claims management business, consulting services and business process outsourcing activities. . Most of United’s investment in artificial intelligence can be found inside Optum Insight. Big data plays a crucial role in United’s overall strategy. Optum Insight’s claims management software uses vast medical claims data bases and artificial intelligence/machine learning software to spot and deny medical claims for which documentation is inadequate or where services are either “inappropriate” or else not covered by an individual’s health plan. Providers also claim that the same software rejects as many as 20% of their claims, often for problems as tiny as a mis-spelled word or a missing data field.

Optum Insight software plays a crucial role in helping United’s health insurance plans manage their medical expense. Traditional health plan profitability is generated by reducing medical expense relative to collected premiums to increase underwriting profit. These profits are regulated, with highly variable degrees of rigor by state health insurance commissioners, and also by provisions of ObamaCare enacted in 2010.

Though its acquisition of Equian in 2019 and the proposed $13 billion acquisition of health information technology conglomerate Change Healthcare in 2021, United came within an eyelash of a near monopoly on “intelligent” medical claims processing software. The Justice Department challenged this latter acquisition and United may agree to divest Change’s claims processing software business as a condition of closing the deal. Even without the Change acquisition, Optum Insight processes hundreds of millions of medical claims annually not only for United’s health insurance business but for many of United’s competitors.

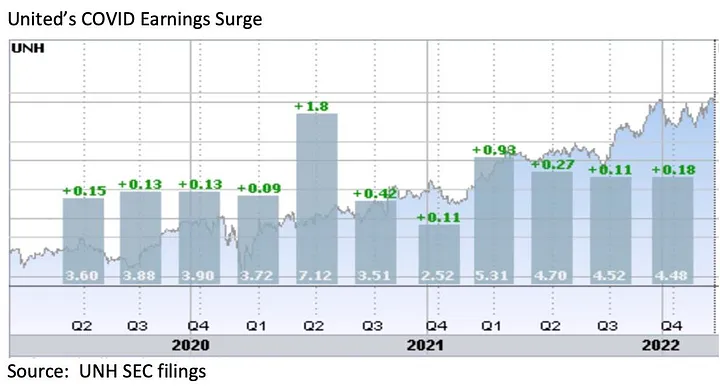

However, Optum Insight’s claims management system can also be used to increase MLR if medical expense unexpectedly declines, exposing the firm to federal requirement that it rebate excessive ‘savings’ to subscribers. This happened in 2020, when the COVID pandemic dramatically and unexpectedly added billions to United’s earnings due to hospitals suspending elective care. The chart below shows United’s 2Q2020 earnings per share almost doubling due to the precipitous drop in its medical claims expenses!

Hospital finance colleagues reported an immediate and substantial drop in medical claims denials from United and other carriers in the summer and fall of 2020. United’s quarterly profits dutifully and steeply declined in the subsequent two quarters, because its medical expenses sharply rebounded. The rise in

United’s medical expenses helped the firm avoid premium rebates to patients required by provisions of the ObamaCare legislation passed in 2010. The firm did voluntarily rebate about $1.5 billion to many of its customers in June, 2020.

However the most rapidly growing part of Optum Insight is its Optum 360 business process outsourcing business, which helps hospitals manage their billing and collections revenue cycle, as well as information technology operations, supply chain (purchasing and materials management) and other services. Through Optum 360, Optum Insight has signed five long term master contracts in the past two years’ worth many billions of dollars with care providers in California, Missouri and other states to provide a broad range of business services.

With all these different businesses, it is theoretically possible for one piece of Optum to be reducing a hospital’s cash flow by denying medical claims for United subscribers, while United’s health insurance network managers bargain aggressively to reduce the hospital’s reimbursement rates while yet another piece of Optum runs the billing and collection services for the same hospital and its employed physicians, while yet another piece of Optum competes with the hospital’s physicians and ambulatory services, diverting patients from its ERs and clinics, reducing the hospital’s revenues.

It is not difficult to imagine a future in which Optum/United offers hospital systems an Optum 360 outsourcing contract that run most of the business operations of a hospital system in exchange for preferred United health plan rates, an AI-enabled EZ pass on its medical claims denials and inpatient referrals from Optum physician groups and urgent care centers, at the expense of competing hospitals.

Managing these potential conflicts will be an increasing challenge as these various businesses grow, placing intense pressure on United’s leadership to get the various pieces of United to work together. To many anxious hospital executives, United resembles nothing so much as the Kraken, rising up out of the sea, surrounding and engulfing them- a powerful friend perhaps or a fearsome foe. As you might expect, United’s growing market power and growth has generated a fierce backlash in the hospital management community.

What Business is United Healthcare In?

United Healthcare is the most successful business in the history of American healthcare. The rapid growth of Optum and continued health insurance enrollment growth from government programs like Medicaid and Medicare has created a cash engine which generates nearly $2 billion a month in free cash flow. Optum’s portfolio has given United an impressive array of tools, unequalled in the industry, to improve its profitability and to reach into every corner of the US health system. United Healthcare is managed care on steroids.

United’s diversified portfolio of businesses gives the firm what a finance-savvy colleague termed “optionality”- the ability to redirect capital and management attention to areas of growth and away from areas that have ceased to grow, in the US or overseas. With its substantial investable capital, it will have the pick of the litter of the 11 thousand digital health companies as the overextended digital health market consolidates. United will be able to use its vast resources to build state-of-the-art digital infrastructure to reach and retain patients and manage their care.

United’s main short term business risks seem to be running out of accretive transactions effectively to deploy its growing horde of capital and managing the firm’s rising political exposure. United has had tremendous business discipline and has shied away from speculative acquisitions that are not immediately accretive to earnings. If its earnings growth falters, however, it will also encounter pressure from the investment community to increase dividends (presently about 1.2%) or share buybacks to bolster its share price, or else divest some or all of Optum in order to “maximize shareholder value”.

Answering the question, “What Business is United In” is simple: just about everything in health but hospitals and nursing homes.

Answering the questions- who are its customers and what do they want? — is a great deal harder. The customers United serves are in a sort of cold war with one another. United’s original business was protecting employers from health cost growth , and tempering the influence of hospitals and doctors by reducing their rates and utilization. By fostering so-called Consumer Directed Health Plans that expose many of their subscribers to very high front-end copayments, United and its health insurance brethren, have also increased their out-of-pocket costs, whether they have the savings to pay them or not.

There are also some ironies in United’s development. Optum Insight’s suite of hospital business services are designed to reduce administrative costs created in major part by United and other insurers’ medical claims data requirements. Its PBM business, originally intended to reduce drug spending by bargaining aggressively with pharmaceutical manufacturers has ended up pushing up drug list prices and consumer cost shares.

While presumably everybody benefits if United can somehow help patients become and remain healthy, it is still far from obvious how to do this. Managing all these markedly divergent customer needs will be a tremendous management challenge for whoever succeeds United’s reclusive (and very effective) 70 year old Chairman Stephen Hemsley.

What Does Society Get from this Vast Enterprise?

However, as Peter Drucker told a different generation of business giants, businesses are not entities unto themselves, accountable only to shareholders and customers. They are organs of society, and are expected to create social value. Americans are suspicious of vast enterprises, as businesses from Standard Oil, US Steel and ATT to Microsoft and Facebook have learned. As businesses grow and become more successful, public suspicion grows.

Private health insurers already face strident opposition from progressive Democrats, who believe that health coverage ought to be a public good, a right of citizenship provided publicly; in other words, that private health insurers have no business being in business. And large insurers like United also face intense opposition from hospitals and many physicians because they reduce their incomes and impose major administrative burdens upon them.

In the age of Twitter and TikTok, United is highly vulnerable to “event risks” that confirm the hostile narratives of the firm’s detractors that United is mainly about maximizing its own profits, not about improving the health of its subscribers or the communities it serves. It is not clear how many the tens of millions of United subscribers have warm and fuzzy feelings about their giant health insurer. Memories of the HMO backlash of the 1990’s reside in the firm’s corporate memory.

United has grown to its present immense scale largely without public knowledge. United has within its reach the capability of constraining overall health cost growth across dozens of metropolitan areas and regions, not merely cost growth for its own beneficiaries (roughly one in seven US citizens already get their health insurance through United). With its expanding digital health operations, it can deploy state of the art tools for helping United’s 50 million subscribers avoid illness and live healthier lives.

United also has the ability to damage the financial operations of beloved local hospitals and deny coverage to families, raising their out of pocket expenses. How United frames and defends its social mission and how it manages all the delicate and increasingly fraught customer relationships will determine its future, and in important ways, ours as well.

As care continues to shift to lower cost ambulatory surgery centers (ASCs), the graphic above looks at recent growth and consolidation in the ASC market.

From 2012 to 2022, the five largest operators increased their collective ownership of ASC facilities from 17 to 21 percent, and were responsible for over 50 percent of total facility growth in that period.

While physicians still fully own over half of the nation’s ASCs, the national chains tend to run larger, multispecialty facilities responsible for an outsized proportion of procedures and revenue.

The likes of Tenet, Optum, and HCA are betting big on ASCs, banking on projections that the market will grow by over 60 percent in the next seven years.

(Though AmSurg’s parent company, Envision Healthcare, filed for bankruptcy, AmSurg is buying Envision’s remaining ASCs to retain its significant foothold in the market.)

While many high-revenue specialties, notably orthopedics and gastroenterology, have already seen a significant shift to ASCs, cardiology is one of the most promising service lines for ASC growth, with some predicting that a third of cardiology procedures will be performed in ambulatory settings in the next few years.

The shift of surgeries from hospitals to ASCs is daunting for health systems, who stand to lose half or more of the revenue from each case—if they’re able keep the procedure within the system.

In the meantime, low-cost ASC operators will continue to add new facilities that deliver high margins to fuel their growth.

Last month, Eric Jordahl, Managing Director of Kaufman Hall’s Treasury and Capital Markets practice, blogged about the dangers of nonprofit healthcare providers’ extremely conservative risk management in today’s uncertain economy.

Healthcare public debt issuance in the first quarter of 2023 was down almost 70 percent compared to the first quarter of 2022. While not the only funding channel for not-for-profit healthcare organizations,

the level of public debt issuance is a bellwether for the ambition of the sector’s capital formation strategies.

While health systems have plenty of reasons to be cautious about credit management right now, it’s important not to underrate the dangers of being too risk averse. As Jordahl puts it: “Retrenchment might be the right risk management choice in times of crisis, but once that crisis moderates that same strategy can quickly become a risk driver.”

The Gist: Given current market conditions, there are a host of good reasons why caution reigns among nonprofit health systems, but this current holding pattern for capital spending endangers their future competitiveness and potentially even their survival.

Nonprofit systems aren’t just at risk of losing a competitive edge to vertically integrated payers, whom the pandemic market treated far more kindly in financial terms, but also to for-profit national systems, like HCA and Tenet, who have been flywheeling strong quarterly results into revamped growth and expansion plans.

Health systems should be wary of becoming stuck on defense while the competition is running up the score.

Retail giant Walmart announced the 2024 opening of four new health centers in Oklahoma.

Oklahoma joins Missouri and Arizona as the third state Walmart Health will enter in 2024.

The 5,570-square-foot centers will be located next to Walmart retail locations and will include primary care, labs, X-rays, EKG, behavioral health, dental, hearing and telehealth services, according to an April 26 Walmart news release.

The health centers will use the Epic EHR system. The new locations will be in the Oklahoma City area, according to the release.

After 18 years as CEO in Kaiser Permanente, I set my sights on improving the heatlh of the nation, hoping to find a way to achieve the same quality, technology and affordability our medical group delivered to 5 million patients on both coasts.

That quest launched the Fixing Healthcare podcast in 2018, and it inspired interviews with dozens of leaders, thinkers and doers, both in and around medicine. These experts shared innovative ideas and proven solutions for achieving (a) superior quality, (b) improved patient access, (c) lower overall costs, and (d) greater patient and clinician satisfaction.

Which of the hundreds of ideas presented remain most promising?

Why, after five years and so many excellent solutions, has our nation experienced such limited improvements in healthcare?

And finally, how will these great ideas become reality?

To answer the first question, I offer 15 of the best Fixing Healthcare recommendations so far. Some quotes have been modified for clarity with links to all original episodes (and transcripts) included.

Fixing the business of medicine

1. Malcolm Gladwell, journalist and five-time bestselling author: “In other professions, when people break rules and bring greater economic efficiency or value, we reward them. In medicine, we need to demonstrate a consistent pattern of rewarding the person who does things better.”

2. Richard Pollack, CEO of the American Hospital Association (AHA): “I hope in 10 years we have more integrated delivery systems providing care, not bouncing people around from one unconnected facility to the next. I would hope that we’re in a position where there’s a real focus on ensuring that people get care in a very convenient way.”

Eliminating burnout

3. Zubin Damania, aka ZDoggMD, hospitalist and healthcare satirist: “In the culture of medicine, specialists view primary care as the weak medical students, the people who couldn’t get the board scores or rotation honors to become a specialist. Because why would you do primary care? It’s miserable. You don’t get paid enough. It’s drudgery. We must change these perceptions.”

4. Devi Shetty, India’s leading heart surgeon and founder of Narayana Health: “When you strive to work for a purpose, which is not about profiting yourself, the purpose of our action is to help society, mankind on a large scale. When that happens, cosmic forces ensure that all the required components come in place and your dream becomes a reality.”

5. Jonathan Fisher, cardiologist and clinician advocate: “The problem we’re facing in healthcare is that clinicians are all siloed. We may be siloed in our own institution thinking that we’re doing it best. We may be siloed in our own specialty thinking that we’re better than others. All of these divides need to be bridged. We need to begin the bridging.”

Making medicine equitable

6. Jen Gunter, women’s health advocate and “the internet’s OB-GYN”: “Women are not listened to by doctors in the way that men are. They have a harder time navigating the system because of that. Many times, they’re told their pain isn’t that serious or their bleeding isn’t that heavy. We must do better at teaching women’s health in medicine.”

7. Amanda Calhoun, activist, researcher and anti-racism educator: “A 2015 survey showed that white residents and medical students still thought Black people feel less pain, which is wild to me because Black is a race. It’s not biological. This is actually an historical belief that persists. One of the biggest things we can do as the medical system is work on rebuilding trust with the Black community.”

Addressing social determinants of health

8. Don Berwick, former CMS administrator and head of 100,000 Lives campaign: “We know where the money should go if we really want to be a healthy nation: early childhood development, workplaces that thrive, support to the lonely, to elders, to community infrastructures like food security and transportation security and housing security, to anti-racism and criminal-justice reform. But we starve the infrastructures that could produce health to support the massive architecture of intervention.”

9. David T. Feinberg, chairman of Oracle Health: “Twenty percent of whether we live or die, whether we have life in our years and years in our life, is based on going to good doctors and good hospitals. We should put the majority of effort on the stuff that really impacts your health: your genetic code, your zip code, your social environment, your access to clean food, your access to transportation, how much loneliness you have or don’t have.”

Empowering patients

10. Elisabeth Rosenthal, physician, author and editor-in-chief of KHN: “To patients, I say write about your surprise medical bills. Write to a journalist, write to your local newspaper. Hospitals today are very sensitive about their reputations and they do not want to be shamed by some of these charges.”

11. Gordon Chen, ChenMed CMO: “If you think about what leadership really is, it’s influence. Nothing more, nothing less. And the only way to achieve better health in patients is to get them to change their behaviors in a positive way. That behavior change takes influence. It requires primary care physicians to build relationship and earn trust with patients. That is how both doctors and patients can drive better health outcomes.”

Utilizing technology

12. Vinod Khosla, entrepreneur, investor, technologist: “The most expensive part of the U.S. healthcare system is expertise, and expertise can relatively be tamed with technology and AI. We can capture some of that expertise, so each oncologist can do 10 times more patient care than they would on their own without that help.”

13. Rod Rohrich, influential plastic surgeon and social media proponent: “Doctors, use social media to empower your audience, to educate them, and not to overwhelm them. If you approach social media by educating patients about their own health, how they can be better, how can they do things better, how they can find doctors better, that’s a good thing.”

Rethinking medical education

14. Marty Makary, surgeon and public policy researcher: “I would get rid of all the useless sh*t we teach our medical students and residents and fellows. In the 16 years of education that I went through, I learned stuff that has nothing to do with patient care, stuff that nobody needs to memorize.”

15. Eric Topol, cardiologist, scientist and AI expert: “It’s pretty embarrassing. If you go across 150 medical schools, not one has AI as a core curriculum. Patients will get well versed in AI. It’s important that physicians stay ahead, as well.”

Great ideas, but little progress

Since 2018, our nation has spent $20 trillion on medical care, navigated the largest global pandemic in a century and developed an effective mRNA vaccine, nearly from scratch. And yet, despite all this spending and scientific innovation, American medicine has lost ground.

American life expectancy has dropped while maternal mortality rates have worsened. Clinician burnout has accelerated amid a growing shortage of primary care and emergency medicine physicians. And compared to 12 of its wealthiest global peers, the United States spends nearly twice as much per person on medical care, but ranks last in clinical outcomes.

Guests on Fixing Healthcare generally agree on the causes of stagnating national progress.

Healthcare system giants, including those in the drug, insurance and hospital industries, find it easier to drive up prices than to prevent disease or make care-delivery more efficient. Over the past decade, they’ve formed a conglomerate of monopolies that prosper from the existing rules, leaving them little incentive to innovate on behalf of patients. And in this era of deep partisan divide, meaningful healthcare reforms have not (and won’t) come from Congress.

Then who will lead the way?

Industry change never happens because it should. It happens when demand and opportunity collide, creating space for new entrants and outsiders to push past the established incumbents. In healthcare, I see two possibilities:

1. Providers will rally and reform healthcare

Doctors and hospitals are struggling. They’re struggling with declining morale and decreasing revenue. Clinicians are exiting the profession and hospitals are shuttering their doors. As the pain intensifies, medical group leaders may be the ones who decide to begin the process of change.

The first step would be to demand payment reform.

Today’s reimbursement model, fee-for-service, pays doctors and hospitals based on the quantity of care they provide—not the quality of care. This methodology pushes physicians to see more patients, spend less time with them, and perform ever-more administrative (billing) tasks. Physicians liken it to being in a hamster wheel: running faster and faster just to stay in place.

Instead, providers of care could be paid by insurers, the government and self-funded businesses directly, through a model called “capitation.” With capitation, groups of providers receive a fixed amount of money per year. That sum depends on the number of enrollees they care for and the amount of care those individuals are expected to need based on their age and underlying diseases.

This model puts most of the financial risk on providers, encouraging them to deliver high-quality, effective medical care. With capitation, doctors and hospitals have strong financial incentives to prevent illnesses through timely and recommended preventive screenings and a focus on lifestyle-medicine (which includes diet, exercise and stress reduction). They’re rewarded for managing patients’ health and helping them avoid costly complications from chronic diseases, such as heart attacks, strokes and cancer.

Capitation encourages doctors from all specialties to collaborate and work together on behalf of patients, thus reducing the isolation physicians experience while ensuring fewer patients fall through the cracks of our dysfunctional healthcare system. The payment methodology aligns the needs of patients with the interests of providers, which has the power to restore the sense of mission and purpose medicine has lost.

Capitation at the delivery-system level eliminates the need for prior authorization from insurers (a key cause of clinician burnout) and elevates the esteem accorded to primary care doctors (who focus on disease prevention and care coordination). And because the financial benefits are tied to better health outcomes, the capitated model rewards clinicians who eliminate racial and gender disparities in medical care and organizations that take steps to address the social determinants of health.

2. Major retailers will take over

If clinicians don’t lead the way, corporate behemoths like Amazon, CVS and Walmart will disrupt the healthcare system as we know it. These retailers are acquiring the insurance, pharmacy and direct-patient-care pieces needed to squeeze out the incumbents and take over American healthcare.

Each is investing in new ways to empower patients, provide in-home care and radically improve access to both in-person and virtual medicine. Once generative AI solutions like ChatGPT gain enough computing power and users, tech-savvy retailers will apply this tool to monitor patients, enable healthier lifestyles and improve the quality of medical care compared to today.

When Fixing Healthcare debuted five years ago, none of the show’s guests could have foreseen a pandemic that left more than a million dead. But, had our nation embraced their ideas from the outset, many of those lives would have been saved. The pandemic rocked an already unstable and underperforming healthcare system. Our nation’s failure to prevent and control chronic disease resulted in hundreds of thousands of unnecessary deaths from Covid-19. Outdated information technology systems, medical errors and disparities in care caused hundreds of thousands more. As a nation, we could have done much better.

With the cracks in the system widening and the foundation eroding, disruption in healthcare is inevitable. What remains to be seen is whether it will come from inside or outside the U.S. healthcare system.

On Tuesday, Milwaukee, WI-based Froedtert Health and Neenah, WI-based ThedaCare shared they have signed a letter of intent to form a $5B, 18-hospital system.

The merger would unite Froedtert’s southeast Wisconsin service area with ThedaCare’s northeast and central Wisconsin footprint, linking tertiary care patients in ThedaCare’s high-growth service areas in the Fox Valley to Froedtert’s Medical College of Wisconsin in Milwaukee. As the systems serve non-overlapping markets, the merger is not expected to receive challenge from federal regulators.

The Gist: These two systems have partnered previously, striking a joint venture last fall to build two health campuses with micro-hospitals, which likely served as the operational test case for merger plans already in the works.

The pace of consolidation has quickened in the Badger State, with Gundersen Health System and Bellin Health completing a merger last fall to form an 11-hospital system.

While interstate mega-mergers have defined recent health system M&A trends, these types of regional mergers, which bring together systems in adjacent but non-overlapping markets, could serve to bolster the combined system’s value proposition as a partner to employers and other healthcare entities in the state and beyond.

On today’s episode of Gist Healthcare Daily, Kaufman Hall co-founder and Chair Ken Kaufman joins the podcast to discuss his recent blog that examines Ford Motor Company’s decision to stop producing internal-combustion sedans, and talk about whether there are parallels for health system leaders to ponder about whether their traditional strategies are beginning to age out.

On Monday, the Mark Cuban Cost Plus Drugs Company (MCCPDC) announced via Twitter that it will begin to offer two branded diabetes drugs, Invokana and Invokamet, produced by Janssen, a Johnson & Johnson subsidiary. A month’s supply of these drugs, the first non-generics it has offered, will cost patients around $244, over 60 percent less than average retail prices. Prescriptions for these diabetes drugs fell from nearly 2M in 2020 to under 1M in 2022, and a key Invokama patent will expire next year, both factors that may have influenced Janssen’s decision to partner with MCCPDC.

The Gist: MCCPDC estimates that as many as 1M people who use these or similar drugs could benefit from the lower prices—not only the uninsured but also those considered “underinsured” due to high deductibles.

Even though the deal is for two drugs with declining revenues, selling brand-name drugs from a pharmaceutical heavyweight is a notable step for the company.

As Congress continues to investigate PBMs for driving up drug spending through their pricing tactics, MCCPDC’s move offers a path to PBM disruption through direct competition. By cutting out the rebates retained by health plans and PBMs, MCCDPC can potentially offerbetter net payments to pharmaceutical companies, as well as reduced cost-sharing for patients—an arrangement that benefits both parties at the expense of traditional PBMs.