Five recent Supreme Court rulings have reset the context for U.S. jurisprudence for years to come and open a can of worms for healthcare operators.

Last year’s SCOTUS decision ruling in Dobbs v. Jackson Women’s Health (June 24, 2022) set the tone: in its 6-3 decision, the high court determined that that access to abortion is a state issue, not federal thus nullifying the 50-year-old legal precedent in Roe v. Wade and reversing 2 lower court rulings.

On June 1, 2023, in the United States v. Supervalu, petitioners sued SuperValu and Safeway under the False Claims Act (FCA) alleging they defrauded the Medicare and Medicaid by knowingly filing false claims. Essentially, the plaintiffs sought financial remedy because the retailers’ prices were not explicitly and specifically “usual and customary” prices. In its unanimous ruling, SCOTUS agreed that “the phrase ‘usual and customary’ is open to interpretation, but reasoned that “such facial ambiguity alone is not sufficient to preclude a finding that respondents knew their claims were false.”

On June 29, 2023, in Students for Fair Admissions, Inc. v. President and Fellows of Harvard College, the court ruled 6-3 that affirmative action policies at Harvard and the University of NC that consider an applicant’s race in college admissions are unconstitutional.

On June 30, 2023, in 303 Creative LLC v. Elenis (June 30, 2023) By a vote of 6-3, SCOTUS ruled that the First Amendment right of free speech prohibits Colorado from forcing a website designer to create expressive designs speaking messages with which the designer disagrees.

On June 30, 2023, in Department of Education v. Brown: By a unanimous vote, SCOTUS ruled that the 2 plaintiffs lacked standing to “Article III standing to assert a procedural challenge to the student-loan debt-forgiveness plan adopted by the Secretary of Education pursuant to Higher Education Relief Opportunities for Students Act of 2003 (HEROES Act).” In effect, the court vacated and remanded the judgment of the United States Court of Appeals for the 5th Circuit because it felt Myra Brown and Alexander Taylor (plaintiffs) did not prove that any injury suffered from not having their loans forgiven. Therefore, the court had no jurisdiction to address their procedural claim.

Each of these is specific to a circumstance but collectively they expose industries like healthcare to greater compliance risk, potential court challenges and operational complexity. Here’s an example:

The 58-year-old Kennedy-era legal precedent of affirmative action to redress racial inequity was the focus in Students for Fair Admissions, Inc. v. President and Fellows of Harvard College. SCOTUS essentially sided with plaintiffs who argued affirmative action violates the 14th Amendment’s Equal Protection guarantee. In healthcare, research shows access to the healthcare system is disproportionately inaccessible to persons of color, especially if they’re poor. They improve when individuals are treated by clinicians of the same race but only about 5% of doctors in America are Black, compared to 12% of the general population and only 6% of doctors in the U.S. are Hispanic while the group accounts for nearly almost 20% of the general population.

Notwithstanding the uncanny similarities between higher education and healthcare (both have raised prices above GDP and overall inflation rates for 2 decades, both jealously protect their reputations against outside transparency and unflattering report cards, both feature competition between public and private institutions and both face questions about the value of their efforts), the issue of diversity is central in both. Affirmative action is a means to that end, but at least for now and in higher education, it’s not constitutional.

Might workforce diversity and clinician training efforts be stymied by the prospect of court challenges? Might “affirmative action” in healthcare be replaced by “holistic review” to enable consideration of an applicant’s life or quality of character as some conservative jurists have suggested?

My take:

Affirmative action per the example above is only one of many constructs widely accepted in healthcare today where court challenges may alter the future. Individual rights and free speech including online medical advice, the role of state governments, fraud and abuse and other domains are equally exposed.

It’s clear this court is not threatened by legal precedent nor cautious about public opinion on touchy issues. Thus, immediate imperatives for healthcare organizations are these:

Revisit legal precedents on which the ways we operate are based: Roles and responsibilities in US healthcare are sacrosanct and protected by legal precedent: Physicians diagnose and treat; others don’t. Insurers pay claims but don’t practice medicine. Not for profit hospitals serve community needs in exchange for tax-exemption. Public health programs that serve the poor are funded by local and state governments. Employer sponsored benefits underwrite the system’s profitability and fund its hospital Part A obligations and so on. Might a conservative court revisit these in the context of the constitution’s “general welfare” purpose and redirect its focus, roles and structure?

Revisit terms and phrases where consensus is presumed but specific definition is lacking: Just as SCOTUS recognized ambiguity in applying terms like “usual and customary” in its Supervalu-Safeway ruling, it is likely to challenge other widely used phrases used in healthcare that often lack specific referents i.e., quality, safety, efficacy, effectiveness, community benefit, charity care, evidence-based care, cost-effectiveness, not-for-profit, competition, value” and many others. Might SCOTUS force the industry to more specifically define its most widely used phrases in order to justify its claims?

For everyone in healthcare, these rulings open a can of worms. Compliance risk assessments, scenario plan updates required!

Here are 45 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global in 2023.

Note: This is not an exhaustive list. Health system names were compiled from credit rating reports.

1. AdventHealth has an “AA” rating and stable outlook with Fitch. The rating reflects the Altamonte Springs, Fla.-based system’s strong financial profile, characterized by still-adequate liquidity and moderate leverage, typically strong and highly predictable profitability, Fitch said.

2. AnMed Health has an “AA-” rating and stable outlook with Fitch. The Anderson, S.C.-based system has maintained strong performance through the COVID-19 pandemic and current labor market pressures, Fitch said.

3. Atrium Health has an “AA-” and stable outlook with S&P Global. The Charlotte, N.C.-based system’s rating reflects a robust financial profile, growing geographic diversity and expectations that management will continue to deploy capital with discipline.

4. Banner Health has an “AA-” and stable outlook with Fitch. The Phoenix-based system’s rating highlights the strength of its core hospital delivery system and growth of its insurance division, Fitch said.

5. BayCare Health System has an “AA” rating and stable outlook with Fitch. The Tampa, Fla.-based system’s rating reflects its excellent financial profile supported by its leading market position in a four-county area and the ability to sustain a solid operating outlook in the face of inflationary sector headwinds, Fitch said.

6. Beacon Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of the South Bend, Ind.-based system’s balance sheet, the rating agency said.

7. Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

8. Cape Cod Healthcare has an “AA-” and stable outlook with Fitch. The Hyannis, Mass.-based system’s rating reflects a dominant market position in its service area and historically solid operating results, the rating agency said.

9. Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area, Fitch said.

10.CaroMont Health has an “AA-” rating and stable outlook with S&P Global. The Gastonia, N.C.-based system has a healthy financial profile and robust market share in a competitive region.

11. CentraCare has an “AA-” rating and stable outlook with Fitch. The St. Cloud, Minn.-based system has a leading market position, and its management’s focus on addressing workforce pressures, patient access and capacity constraints will improve operating margins over the medium term, Fitch said.

12. Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The Minneapolis-based system’s broad reach within the region continues to support long-term sustainability as a market leader and preferred provider for children’s health care, Fitch said.

13. Concord (N.H.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of Concord’s leverage and liquidity assessment and Fitch’s assessment that two recently acquired hospitals will be strategically and financially accretive.

14. Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

15. Cottage Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Santa Barbara, Calif.-based system’s leading market position and broad reach in a service area that exhibits modest population growth but consistently high demand for acute care services, Fitch said.

16. El Camino Health has an “AA-” rating and stable outlook with Fitch. The Mountain View, Calif.-based system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix, Fitch said.

17. Froedtert Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s maintenance of a strong, albeit compressed, operating performance and a robust liquidity position, Fitch said.

18. Hackensack Meridian Health has an “AA-” rating and stable outlook with Fitch. The Edison, N.J.-based system’s rating is supported by its strong presence in its large and demographically favorable market, Fitch said.

19. Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

20. Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by a leading market position in its immediate area and very strong financial profile, Fitch said.

21. IU Health has an “AA” rating and stable outlook with Fitch. The Indianapolis-based system has a long track record of strong operating margins and an overall credit profile that is supported by a strong balance sheet, the rating agency said.

22. Inspira Health has an “AA-” rating and stable outlook with Fitch. The Mullica Hill, N.J.-based system’s rating reflects its leading market position in a stable service area and a large medical staff supported by a growing residency program, Fitch said.

23. Lucile Packard Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Palo Alto, Calif.-based hospital’s role as a nationally known, leading children’s hospital, Fitch said. It also benefits from resilient clinical volumes and a solid market position, as well as its relationship with Stanford University and Stanford Health Care.

24. Kaiser Permanente has an “AA-” and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by a strong financial profile, which is maintained despite a challenging operating environment in fiscal year 2022.

25. Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The Rochester, Minn.-based system’s credit profile characterized by its excellent reputations for clinical services, research and education, Moody’s said.

26. McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The Grand Blanc, Mich.-based system has a leading market position over a broad service area covering much of Michigan and a track-record of profitability despite sector-wide market challenges in recent years, Fitch said.

27. MemorialCare has an “AA-” rating and stable outlook with Fitch. The rating reflects the Fountain Valley, Calif.-based system’s strong financial profile and excellent leverage metrics despite its weaker operating performance, Fitch said.

28. Memorial Sloan-Kettering Cancer Center has an “AA” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the New York City-based system’s national and international reputation as a premier cancer hospital will continue to support growth in its leading and increasing market share for its specialty services.

29. Midland (Texas) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Midland’s exceptional market position and limited competition for acute-care services and growing outpatient services, Fitch said.

30. Munson Healthcare has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Traverse City, Mich.-based system’s market position and its leverage and liquidity profiles.

31. North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The Tupelo-based system’s rating reflects its very strong cash position and strong market position, Fitch said.

32. Novant Health has an “AA-” rating and stable outlook with Fitch. The Winston-Salem, N.C.-based system has a highly competitive market share in three separate North Carolina markets, Fitch said, including a leading position in Winston-Salem (46.8 percent) and second only to Atrium Health in the Charlotte area.

33. NYC Health + Hospitals has an “AA-” rating with Fitch. The New York City system is the largest municipal health system in the country, serving more than 1 million New Yorkers annually in more than 70 patient locations across the city, including 11 hospitals, and employs more than 43,000 people.

34. Orlando (Fla.) Health has an “AA-” and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

35. The Queen’s Health System has an “AA” rating and stable outlook with Fitch. The Honolulu-based system’s rating reflects its leading state-wide market position, historically strong operating performance and diverse revenue streams, the rating agency said.

36. Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

37. Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The Cape Girardeau, Mo.-based system enjoys robust operational performance and a strong local market share as well as manageable capital plans, Fitch said.

38. Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

39. Stanford Health Care has an “AA” rating and stable outlook with Fitch. The Palo Alto, Calif.-based system’s rating is supported by its extensive clinical reach in the greater San Francisco and Central Valley regions and nationwide/worldwide destination position for extremely high-acuity services, Fitch said.

40. SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system has a strong financial profile, multi-state presence and scale, with solid revenue diversity, Fitch said.

41. St. Clair Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Pittsburgh-based system’s strong financial profile assessment, solid market position and historically strong operating performance, the rating agency said.

42. UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

43. University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

44. WellSpan Health has an “Aa3” rating and stable outlook with Moody’s. The York, Pa.-based system has a distinctly leading market position across several contiguous counties in central Pennsylvania, and management’s financial stewardship and savings initiatives will continue to support sound operating cash flow margins when compared to peers, Moody’s said.

45. Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

A number of hospitals and health systems are trimming their workforces or jobs due to financial and operational challenges.

Below are workforce reduction efforts or job eliminations that were announced within the past year and/or take effect later in 2023.

Editor’s Note: This webpage was updated June 30 and will continue to be updated.

1. Coral Gables-based Baptist Health South Florida is offering its executives at the director level and above a “one-time opportunity” to apply for voluntary separation, according to a June 29 Miami Herald report. Decisions on buyout applications will be made during the summer.

2. MultiCare Health System, a 12-hospital organization based in Tacoma, Wash., will lay off 229 employees, or about 1 percent of its 23,000 staff members, including about two dozen leaders, as part of cost-cutting efforts, the health system said June 29. The layoffs primarily affect support departments, such as marketing, IT and finance.

3. Greensburg, Pa.-based Independence Health System laid off 53 employees and has cut 226 positions — including resignations, retirements and elimination of vacant positions — since January, The Butler Eagle reported June 28. The 226 reductions began at the executive level, with 13 manager positions terminated in March.

4. Billings (Mont.) Clinic will lay off workers as part of a restructuring plan to address financial and operational headwinds in today’s healthcare environment, the organization confirmed. The layoffs are expected to affect approximately 27 or fewer positions.

5. Melbourne, Fla.-based Health First is eliminating some positions and leaving open ones vacant, Florida Today reported June 21. Seventeen jobs will be cut and 36 will be left unfilled, according to Paula Just, the health system’s chief experience officer.

6. Pittsburgh-based Highmark Health laid off 118 employees on June 21, including two from Allegheny Health Network, a spokesperson for the health system told Becker’s. The layoffs follow the health system’s cutbacks in March and April, according to the Pittsburgh Business Times. Highmark laid off 141 workers earlier this year.

7. Vibra Hospital of Western Massachusetts, a long-term-acute care hospital in Springfield, will lay off 87 employees by Aug. 15 ahead of the facility’s planned closure. About 30 patients will be relocated to Baystate Health’s Valley Springs Behavioral Health Hospital in Holyoke, Mass., which will open in August.

8. Cortez, Colo.-based Southwest Memorial Hospital laid off nine people to help ensure the hospital is staffed appropriately, and create financial stability for the future, a spokesperson confirmed to Becker’s. The spokesperson, Chuck Krupa, said the layoffs occurred June 14 and included administrative workers. No bedside care positions were affected.

9. Henry Mayo Newhall Hospital in Valencia, Calif., is making “a little over 100” layoffs amid financial challenges, spokesperson Patrick Moody confirmed to Becker’s. Mr. Moody said the layoffs affect workers “in a wide range of hospital departments.” This includes some management-level employees. The hospital, which has about 1,800 employees total, is not providing specific numbers for specific job titles or departments.

10. Dartmouth Health is laying off 75 workers and eliminating 100 job vacancies. The layoffs came after the Lebanon, N.H.-based health system implemented a performance improvement plan in November.

11. Seattle Children’s is eliminating 135 leader roles, citing financial challenges. The management restructuring and reduction affects 1.5 percent of employees across the organization.

12. White Rock (Texas) Medical Center laid off 30 workers across 28 departments. The layoffs include clinical and administrative roles.

13. Jackson, Miss.-based St. Dominic Health Services is laying off 157 workers and ending behavioral health services. The reduction represents 5.5 percent of the hospital’s workforce.

14. Danville, Pa.-based Geisinger laid off 47 employees from its IT department. The reduction is part of a restructuring plan to offset high labor and supply costs.

15. Cascade Behavioral Health Hospital in Tukwila, Wash., is winding down operations and laying off 288 employees. The 137-bed psychiatric facility is slated to close by July 31.

16. Cambridge (Mass.) Health Alliance is laying off 69 employees, reducing the hours of 15 others and eliminating 170 open positions, according to The Boston Globe. The reductions are primarily in management, administrative and support areas, a health system spokesperson told Becker’s.

17. Wenatchee, Wash.-based Confluence Health has eliminated its chief operating officer amid restructuring efforts and financial pressures, the health system confirmed to Becker’s May 16.

18. Conemaugh Memorial Medical Center, a Duke LifePoint hospital in Johnstown, Pa., has laid off less than 1 percent of its workforce, the hospital confirmed to Becker’s May 15.

19. Community Health Network, a nonprofit health system based in Indianapolis, plans to cut an unspecified number of jobs as it restructures its workforce and makes organizational changes. The health system confirmed the job cuts in a statement shared with Becker’s on May 11. It did not say how many jobs would be cut or which positions would be affected.

20. New Orleans-based Ochsner Health eliminated 770 positions, or about 2 percent of its workforce, on May 11. This is the largest layoff to date for the health system.

21. Cedars-Sinai Medical Center eliminated the positions of 131 employees and cut about two dozen other jobs at related Cedars-Sinai facilities, a spokesperson confirmed via a statement shared with Becker’s May 7. The Los Angeles-based organization said reductions represent less than 1 percent of the workforce and apply to management and non-management roles primarily in non-patient care jobs.

22. Rochester (N.Y.) Regional Health is eliminating about 60 positions. A statement from RRH said the changes affect less than one-half percent of the system population, mostly in nonclinical and management positions.

23. Memorial Health System laid off fewer than 90 people, or less than 2 percent of its workforce.The Gulfport, Miss.-based health system said May 2 that most of the affected positions are nonclinical or management roles, and the majority do not involve direct patient care.

24. Monument Health laid off at least 80 employees, or about 2 percent of its workforce. The Rapid City, S.D.-based system said positions are primarily corporate service roles and will not affect patient services. Unfilled corporate service positions were also eliminated.

25. Habersham Medical Center in Demorest, Ga., laid off four executives. The layoffs are part of cost-cutting measures before the hospital joins Gainesville-based Northeast Georgia Health System in July, nowhaberbasham.com reported April 27.

26. Scripps Health is eliminating 70 administrative roles, according to WARN documents filed by the San Diego-based health system in March. The layoffs take effect May 8 and affect corporate positions in San Diego and La Jolla, Calif.

27. Trinity Health Mid-Atlantic, part of Livonia, Mich.-based Trinity Health, eliminated fewer than 40 positions, a spokesperson confirmed to Becker’s April 24. The layoffs represent 0.5 percent of the health system’s approximately 7,000-person workforce.

28. PeaceHealth eliminated 251 caregiver roles across multiple locations. The Vancouver, Wash.-based health system said affected roles include 121 from Shared Services, which supports its 16,000 caregivers in Washington, Oregon and Alaska.

29. Toledo, Ohio-based ProMedica plans to lay off 26 skilled nursing support staff. The layoffs, effective in June, affect 20 employees who work remotely across the U.S, and six who work at the ProMedica Summit Center in Toledo, according to a Worker Adjustment and Retraining Notification filed April 18. Most affected positions support sales, marketing and administrative functions for the skilled nursing facilities, Promecia told Becker’s.

30. Northern Inyo Healthcare District, which operates a 25-bed critical access hospital in Bishop, Calif., anticipates eliminating about 15 positions, or less than 4 percent of its 460-member workforce, by April 21, a spokesperson confirmed to Becker’s. The layoffs include nonclinical roles within support and administration, according to a news release. No further details were provided about specific positions affected.

31. West Reading, Pa.-based Tower Health is eliminating 100 full-time equivalent positions. The move will affect 45 individuals, according to an April 13 news release the health system shared with Becker’s. The other 55 positions are either recently vacated or involve individuals who plan to retire in the coming weeks and months.

32. Grand Forks, N.D.-based Altru Health is trimming its executive team as its new hospital project moves forward. The health system is trimming its executive team from nine to six and incentivizing 34 other employees to take early retirement.

33. Tacoma, Wash.-based Virginia Mason Franciscan Health laid off nearly 400 employees, most of whom are in non-patient-facing roles. The job cuts affected less than 2 percent of the health system’s 19,000-plus workforce.

34. Katherine Shaw Bethea Hospital in Dixon, Ill., will lay off 20 employees, citing financial headwinds affecting health organizations across the U.S. It will also leave other positions unfilled to reduce expenses amid rising labor and supply costs and reductions in payments by insurance plans. Affected employees largely work in administrative support areas and not direct patient care.

35. Danbury, Conn.-based Nuvance Health will close a 100-bed rehabilitation facility in Rhinebeck, N.Y., resulting in 102 layoffs. The layoffs are effective April 12, according to the Daily Freeman.

36. Charleston, S.C.-based MUSC Health University Medical Center laid off an unspecified number of employees from its Midlands hospitals in the Columbia, S.C. area. Division President Terry Gunn also resigned after the facilities missed budget expectations by $40 million in the first six months of the fiscal year, The Post and Courier reported March 30.

37. Winston-Salem, N.C.-based Novant Health laid off about 50 workers, including C-level executives, the health system confirmed to Becker’s March 29. The layoffs affected Jesse Cureton, the health system’s executive vice president and chief consumer officer since 2013; Angela Yochem, its executive vice president and chief transformation and digital officer since 2020; and Paula Dean Kranz, vice president of innovation enablement and executive director of the Novant Health Innovation Labs.

38. Penn Medicine Lancaster (Pa.) General Health eliminated fewer than 65 jobs, or less than 1 percent of its workforce of about 9,700, the health system confirmed to Becker’s March 30. The layoffs include support, administrative and executive roles, and COVID-19-related support staff, spokesperson John Lines said, according to lancasteronline.com. Mr. Lines did not provide a specific number of affected workers.

39. McLaren St. Luke’s Hospital in Maumee, Ohio, will lay off 743 workers, including 239 registered nurses, when it permanently closes this spring. Other affected roles include physical therapists, radiology technicians, respiratory therapists, pharmacists and pharmacy support staff, and nursing assistants. The hospital’s COO is also affected, and a spokesperson for McLaren Health Care told Becker’s other senior leadership roles are also affected.

40. Bellevue, Wash.-based Overlake Medical Center and Clinics laid off administrative staff, the health system confirmed to the Puget Sound Business Journal. The layoffs, which occurred earlier this year, included 30 workers across Overlake’s human resources, information technology and finance departments, a spokesperson said, according to the publication. This represents about 6 percent of the organization’s administrative workforce. Overlake’s website says it employs more than 3,000 people total.

41. Columbia-based University of Missouri Health Care is eliminating five hospital leadership positions across the organization, spokesperson Eric Maze confirmed to Becker’s March 20. Mr. Maze did not specify which roles are being eliminated saying that the organization won’t address individual personnel actions. According to MU Health Care, the move is a result of restructuring “to better support patients and the future healthcare needs of Missourians.”

42. Greensboro, N.C.-based Cone Health eliminated 68 senior-level jobs. The job eliminations occurred Feb. 21, Cone Health COO Mandy Eaton told The Alamance News. Of the 68 positions eliminated, 21 were filled. Affected employees were offered severance packages.

43. The newly merged Greensburg, Pa.-based organization made up of Excela Health and Butler Health System eliminated 13 filled managerial jobs. The affected employees and positions are from across both sides of the new organization, Tom Chakurda, spokesperson for the Excela-Butler enterprise, confirmed to Becker’s. The positions were in various support functions unrelated to direct patient care.

44. Crozer Health, a four-hospital system based in Upland, Pa., is laying off roughly 215 employees amid financial challenges. The system announced the layoffs March 15 as part of its “operational restructuring plan” that “focuses on removing duplication in administrative oversight and discontinuing underutilized services.” Affected employees represent about 4 percent of the organization’s workforce.

45. Philadelphia-based Penn Medicine is eliminating administrative positions. The change is part of a reorganization plan to save the health system $40 million annually, the Philadelphia Business Journal reported March 13. Kevin Mahoney, CEO of the University of Pennsylvania Health System, told Penn Medicine’s 49,000 employees last week that changes include the elimination of a “small number of administrative positions which no longer align with our key objectives,” according to the publication. The memo did not indicate the exact number of positions that were eliminated.

46. Sovah Health, part of Brentwood, Tenn.-based Lifepoint Health, eliminated the COO positions at its Danville and Martinsville, Va., campuses. The responsibilities of both COO roles will now be spread across members of the existing administrative team.

47. Valley Health, a six-hospital health system based in Winchester, Va., eliminated 31 administrative positions. The job cuts are part of the consolidation of the organization’s leadership team and administrative roles.

48. Marshfield (Wis.) Clinic Health System said it would lay off 346 employees, representing less than 3 percent of its employee base.

50. Roseville, Calif.-based Adventist Health plans to go from seven networks of care to five systemwide to reduce costs and strengthen operations. The reorganization will result in job cuts, including reducing administration by more than $100 million.

51. Arcata, Calif.-based Mad River Community Hospital is cutting 27 jobs as it suspends home health services.

52. Hutchinson (Kan.) Regional Medical Center laid off 85 employees, a move tied to challenges in today’s healthcare environment.

53. Oklahoma City-based OU Health eliminated about 100 positions as part of an organizational redesign to complete the integration from its 2021 merger.

54. Memorial Sloan Kettering Cancer Center announced it would lay off to reduce costs amid widespread hospital financial challenges. The layoffs are spread across 14 sites in New York City, and equate to about 1.8 percent of Memorial Sloan’s 22,500 workforce.

55. St. Louis-based Ascension completed layoffs in Texas, the health system confirmed in January. A statement shared with Becker’s says the layoffs primarily affected nonclinical support roles. The health system declined to specify to Becker’s the number of employees or positions affected.

57. Chillicothe, Ohio-based Adena Health System announced it would eliminate 69 positions — 1.6 percent of its workforce — and send 340 revenue cycle department employees to Ensemble Health Partners’ payroll in a move aimed to help the health system’s financial stability.

58. Ascension St. Vincent’s Riverside in Jacksonville, Fla., will end maternity care at the hospital, affecting 68 jobs, according to a Workforce Adjustment and Retraining Notification filed with the state Jan. 17. The move will affect 62 registered nurses as well as six other positions.

59. Visalia, Calif.-based Kaweah Health said it aimed to eliminate 94 positions as part of a new strategy to reduce labor costs. The job cuts come in addition to previously announced workforce reductions; the health system already eliminated 90 unfilled positions and lowered its workforce by 106 employees.

60. Oklahoma City-based Integris Health said it would eliminate 200 jobs to curb expenses. The eliminations include 140 caregiver roles and 60 vacant jobs.

61. Toledo, Ohio-based ProMedica announced plans to lay off 262 employees, a move tied to its exit from a skilled-nursing facility joint venture late last year. The layoffs will take effect between March 10 and April 1.

62. Employees at Las Vegas-based Desert Springs Hospital Medical Center were notified of layoffs coming to the facility, which will transition to a freestanding emergency department. There are 970 employees affected. Desert Springs is part of the Valley Health System, a system owned and operated by King of Prussia, Pa.-based Universal Health Services.

63. Philadelphia-based Jefferson Health plans to go from five divisions to three in an effort to flatten management and become more efficient. The reorganization will result in an unspecified number of job cuts, primarily among executives.

64. Pikeville (Ky.) Medical Center said it would lay off 112 employees as it outsources its environmental services department. The 112 layoffs were effective Jan. 1, 2023.

65. Southern Illinois Healthcare, a four-hospital system based in Carbondale, announced it would eliminate or restructure 76 jobs in management and leadership. The 76 positions fall under senior leadership, management and corporate services. Included in that figure are 33 vacant positions, which will not be filled. No positions in patient care are affected.

66. Citing a need to further reduce overhead expenses and support additional investments in patient care and wages, Traverse City, Mich.-based Munson Health said it would eliminate 31 positions and leave another 20 jobs unfilled. All affected positions are in corporate services or management. The layoffs represent less than 1 percent of the health system’s workforce of nearly 8,000.

67. West Reading, Pa.-based Tower Health on Nov. 16 laid off 52 corporate employees as the health system shrinks from six hospitals to four. The layoffs, which are expected to save $15 million a year, account for 13 percent of Tower Health’s corporate management staff.

68. Sioux Falls, S.D.-based Sanford Health announced layoffs affecting an undisclosed number of staff in October, a decision its CEO said was made “to streamline leadership structure and simplify operations” in certain areas. The layoffs primarily affect nonclinical areas.

69. St. Vincent Charity Medical Center in Cleveland closed its inpatient and emergency room care Nov. 11, four days before originally planned — and laid off 978 workers in doing so. After the transition, the Sisters of Charity Health System will offer outpatient behavioral health, urgent care and primary care.

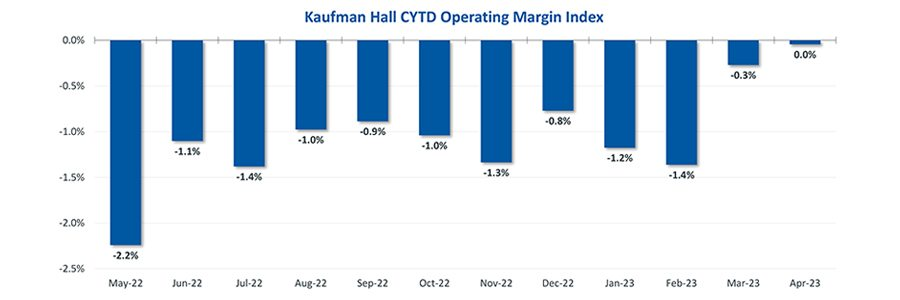

Hospital finances showed signs of stabilizing in May amid slightly improving operating margins, declining expenses and notable increases in outpatient visits.

The median Kaufman Hall Year-To-Date Operating Margin Index reflecting actual margins was 0.3% in May.

The National Hospital Flash Report uses both actual and budget data over the last three years, sampled from more than 900 hospitals on a recurring monthly basis from Syntellis Performance Solutions.

The sample of hospitals for this report is representative of all hospitals in the United States both geographically and by bed size. Additionally, hospitals of all types are represented, from large academic to small critical access. Advanced statistical techniques are used to standardize data, identify and handle outliers, and ensure statistical soundness prior to inclusion in the report.

While this report presents data in the aggregate, Syntellis Performance Solutions also has real-time data down to individual department, jobcode, paytype, and account levels, which can be customized into peer groups for unparalleled comparisons to drive operational decisions and performance improvement initiatives.

Key Takeaways

Hospitals broke even in April. The median operating margin for hospitals was 0% in April, leaving most hospitals with little to no financial wiggle room.

Volumes dropped while lengths of stay increased. Hospital volumes dropped across the board—including inpatient and outpatient. Emergency department volumes were the least affected.

Effects of Medicaid disenrollment could be materializing. Hospitals experienced increases in bad debt and charity care in April. Combined with anemic patient volumes, experts note this data could illustrate the effects of the start of widespread disenrollment from Medicaid following the end of the COVID-19 public health emergency.

Inflation continued to throttle hospital finances. Labor costs jumped in April and the costs of goods and services continued to be well above pre-pandemic levels. Though expenses generally fell in April, revenues declined at a faster rate.

National Non-Operating Results

Key Observations

At their May meeting, the Federal Open Market Committee (FOMC) raised the benchmark borrowing rate another 25 basis points, setting the range to 5.00-5.25% and marking the 10th consecutive hike in the cycle as well as a 16-year high

Fed officials acknowledged discussion of a potential pause in tightening while leaving wiggle room, saying “rates are going to come down” over a long period of time while also warning inflation “continues to run high” and the Fed will be taking a “data-dependent approach”

The consumer price index (CPI) rose 0.4% in April, a 4.9% increase year-over-year, an annual pace of inflation below 5% for the first time in two years

The labor market continued to show resilience in April as U.S. nonfarm payrolls grew by 253,000 and unemployment fell back to a 53-year low of 3.4%

Strong inflation, a robust labor market, continued banking sector woes, and a debt ceiling standoff further complicates credit conditions and may challenge the Fed to stabilize financial markets

Equities in April, as measured by the S&P 500, were up 1.5% in April and 8.6% YTD despite downbeat economic data, reoccurring banking sector fears, and mixed earnings

Two important reports released last Wednesday point to a disconnect in how policymakers are managing the U.S. economy and how the health economy fits.

Report One: The Federal Reserve Open Market Meeting

At its meeting last week, the Governors of the Federal Open Market Committee (FOMC) voted unanimously to keep the target range for the federal funds rate at 5% to 5.25%–the first time since last March that the Fed has concluded a policy meeting without raising interest rates.

In its statement by Chairman Powell, the central bank left open the possibility of additional rate hikes this year which means interest rates could hit 5.6% before trending slightly lower in 2024.

In conjunction with the (FOMC) meeting, meeting participants submitted projections of the most likely outcomes for each year from 2023 to 2025 and over the longer run:

Median

2023

2024

2025

Longer Run

Longer Run Range

% Change in GDP

1.1

1.1

1.8

1.8

1.6-2.5

Unemployment rate &

4.1

4.5

4.5

4.0

3.6-4.4

PCE Inflation rate

3.2

2.5

2.1

2.0

2.0

Core PCE Inflation

3.9

2.6

2.2

*

*

*Longer-run projections for core PCE inflation are not collected.

Notes re: the Fed’s projections based on these indicators:

The GDP (a measure of economic growth) is expected to increase 1% more this year than anticipated in its March 2023 analysis while estimates for 2024 were lowered just slightly by 0.1%. Economic growth will continue but at a slower pace.

The unemployment rate is expected to increase to 4.1% by the end of 2023, a smaller rise in joblessness than the previous estimate of 4.5%. (As of May, the unemployment rate was 3.7%). Unemployment is returning to normalcy impacting the labor supply and wages.

inflation: as measured by the Personal Consumption Expenditures index, will be 3.2% at the end of 2023 vs. 3.3% they previously projected. By the end of 2024, it expects inflation will be 2.5% reaching 2.1% at the end of 2025. Its 2.0% target is within reach on or after 2025 barring unforeseen circumstances.

Core inflation projections, which excludes energy and food prices, increased: the Fed now anticipates 3.9% by the end of 2023–0.3% above the March estimate. Price concerns will continue among consumers.

Based on these projections, two conclusions about nation’s monetary policy may be deduced the Fed’s report and discussion:

The Fed is cautiously optimistic about the U.S. economy in for the near term (through 2025) while acknowledging uncertainty exists.

Interest rates will continue to increase but at a slower rate than 2022 making borrowing and operating costs higher and creditworthiness might also be under more pressure.

Report Two: CMS

On the same day as the Fed meeting, the actuaries at the Centers for Medicare and Medicaid Services (CMS) released their projections for overall U.S. national healthcare spending for the next several years:

“CMS projects that over 2022-2031, average annual growth in NHE (5.4%) will outpace average annual growth in gross domestic product (GDP) (4.6%), resulting in an increase in the health spending share of GDP from 18.3% in 2021 to 19.6% in 2031. The insured percentage of the population is projected to have reached a historic high of 92.3% in 2022 (due to high Medicaid enrollment and gains in Marketplace coverage). It is expected to remain at that rate through 2023. Given the expiration of the Medicaid continuous enrollment condition on March 31, 2023 and the resumption of Medicaid redeterminations, Medicaid enrollment is projected to fall over 2023-2025, most notably in 2024, with an expected net loss in enrollment of 8 million beneficiaries. If current law provisions in the Affordable Care Act are allowed to expire at the end of 2025, the insured share of the population is projected to be 91.2%. In 2031, the insured share of the population is projected to be 90.5%, similar to pre-pandemic levels.”

The report includes CMS’ assumptions for 4 major payer categories:

Medicare Part D: Several provisions from the Inflation Reduction Act (IRA) are expected to result in out-of-pocket savings for individuals enrolled in Medicare Part D. These provisions have notable effects on the growth rates for total out-of-pocket spending for prescription drugs, which are projected to decline by 5.9% in 2024, 4.2% in 2025, and 0.2% in 2026.

Medicare: Average annual expenditure growth of 7.5% is projected for Medicare over 2022-2031. In 2022, the combination of fee-for-service beneficiaries utilizing emergent hospital care at lower rates and the reinstatement of payment rate cuts associated with the Medicare Sequester Relief Act of 2022 resulted in slower Medicare spending growth of 4.8% (down from 8.4% in 2021).

Medicaid: On average, over 2022-2031, Medicaid expenditures are projected to grow by 5.0%. With the end of the continuous enrollment condition in 2023, Medicaid enrollment is projected to decline over 2023-2025, with most of the net loss in enrollment (8 million) occurring in 2024 as states resume annual Medicaid redeterminations. Medicaid enrollment is expected to increase and average less than 1% through 2031, with average expenditure growth of 5.6% over 2025-2031.

Private Health Insurance: Over 2022-2031, private health insurance spending growth is projected to average 5.4%. Despite faster growth in private health insurance enrollment in 2022 (led by increases in Marketplace enrollment related to the American Rescue Plan Act’s subsidies), private health insurance expenditures are expected to have risen 3.0% (compared to 5.8% in 2021) due to lower utilization growth, especially for hospital services.

And for the 3 major recipient/payee categories:

Hospitals: Over 2022-2031, hospital spending growth is expected to average 5.8% annually. In 2023, faster growth in hospital utilization rates and accelerating growth in hospital prices (related to economy wide inflation and rising labor costs) are expected to lead to faster hospital spending growth of 9.3%. For 2025-2031, hospital spending trends are expected to normalize (with projected average annual growth of 6.1%) as there is a transition away from pandemic public health emergency funding impacts on spending.

Physicians and Clinical Services: Growth in physician and clinical services spending is projected to average 5.3% over 2022-2031. An expected deceleration in growth in 2022, to 2.4% from 5.6% in 2021, reflects slowing growth in the use of services following the pandemic-driven rebound in use in 2021. For 2025-2031, average spending growth for physician and clinical services is projected to be 5.7%, with an expectation that average Medicare spending growth (8.1%) for these services will exceed that of average Private Health Insurance growth (4.6%) partly as a result of comparatively faster growth in Medicare enrollment.

Prescription Drugs: Total expenditures for retail prescription drugs are projected to grow at an average annual rate of 4.6% over 2022-2031. For 2025-2031, total spending growth on prescription drugs is projected to average 4.8%, reflecting the net effects of key IRA provisions: Part D benefit enhancements (putting upward pressure on Medicare spending growth) and price negotiations/inflation rebates (putting downward pressure on Medicare and out-of-pocket spending growth).

Thus, CMS Actuaries believe spending for healthcare will be considerably higher than the growth of the overall economy (GDP) and inflation and become 19.6% of the total US economy in 2031. And it also projects that the economy will absorb annual spending increases for hospitals (5.8%) physician and clinical services (5.3%) and prescription drugs (4.6%).

My take:

Side-by-side, these reports present a curious projection for the U.S. economy through 2031: the overall economy will return to a slightly lower-level pre-pandemic normalcy and the healthcare industry will play a bigger role despite pushback from budget hawks preferring lower government spending and employers and consumers frustrated by high health prices today.

They also point to two obvious near-term problems:

1-The Federal Reserve pays inadequate attention to the healthcare economy. In Chairman Powell’s press conference following release of the FOMC report, there was no comment relating healthcare demand or spending to the broader economy nor a question from any of the 20 press corps relating healthcare to the overall economy. In his opening statement (below), Chairman Powell reiterated the Fed’s focus on prices and called out food, housing and transportation specifically but no mention of healthcare prices and costs which are equivalent or more stressful to household financial security:

“Good afternoon. My colleagues and I remain squarely focused on our dual mandate to promote maximum employment and stable prices for the American people…My colleagues and I are acutely aware that high inflation imposes hardship as it erodes purchasing power, especially for those least able to meet the higher costs of essentials like food, housing, and transportation. We are highly attentive to the risks that high inflation poses to both sides of our mandate, and we are strongly committed to returning inflation to our 2% objective.”

2-Congress is reticent to make substantive changes in Medicare and other healthcare programs despite its significance in the U.S. economy. It’s politically risky. In the June 2 Congressional standoff to lift the $31.4 debt ceiling, cuts to Medicare and Social Security were specifically EXCLUDED. Medicare is 12% of mandated spending in the 2022 federal budget and is expected to grow from a rate of 4.8% in 2022 to 8% in 2023—good news for investors in Medicare Advantage but concerning to consumers and employers facing higher prices as a result.

Even simplifying the Medicare program to replace its complicated Parts A, B, C, and D programs or addressing over-payments to Medicare Advantage plans (in 2022, $25 billion per MedPAC and $75 billion per USC) is politically tricky. It’s safer for elected officials to support price transparency (hospitals, drugs & insurers) and espouse replacing fee for service payments with “value” than step back and address the bigger issue: how should the health system be structured and financed to achieve lower costs and better health…not just for seniors or other groups but everyone.

These two realities contribute to the disconnect between the Fed and CMS. Looking back 20 years across 4 Presidencies, two economic downturns and the pandemic, it’s also clear the health economy’s emergence did not occur overnight as the Fed navigated its monetary policy. Consider:

National health expenditures were $1.366 trillion (13.3% of GDP) in 2000 and $4.255 billion in 2021 (18.3% of the GDP). This represents 210% increase in nominal spending and a 37.5% increase in the relative percentage of the nation’s GDP devoted to healthcare. No other sector in the economy has increased as much.

In the same period, the population increased 17% from 282 million to 334 million while per capita healthcare spending increased 166% from $4,845 to $12,914. This disproportionate disconnect between population and health spending growth is attributed by economists to escalating unit costs increases for the pills, facilities, technologies and specialty-provider services we use—their underlying cost escalation notably higher than other industries.

There were notable changes in where dollars were spent: hospitals were unchanged (from $415 billion/30.4% of total spending to $1.323 trillion/31.4% of total spending), physician services shrank (from $288.2 billion/21.1% of total spending to 664.6 billion/15.6% pf total spending), prescription drugs were unchanged (from $122.3 billion/8.95% to $378 billion/8.88% of total spending) and public health increased slightly (from $43 billion/$3.2% of total spending to $187.6 billion/4.4% of total spending).

And striking differences in sources of funding: out of pocket spending shrank from $193.6/14.2% of payments to $433 billion/10.2% % of payments; private insurance shrank from $441 billion/32.3% of payments to $1.21 trillion/28.4% of total payments; Medicare grew from $224.8 billion/16.5% of payments to $900.8 billion/21.2% of payments; Medicaid + CHIP grew from $203.4 billion/14.9% to $756.2 billion/17.8% of payments; and Veterans Health grew from $19.1 billion/1.4% of payments to $106.0 billion/2.5% of payments.

Thus, if these trends continue…

Aggregate payments to providers from government programs will play a bigger role and payments from privately insured individuals and companies will play a lesser role.

Hospital price increases will exceed price increases for physician services and prescription drugs.

Spending for healthcare will (continue to) exceed overall economic growth requiring additional funding from taxpayers, employers and consumers AND/OR increased dependence on private investments that require shareholder return AND/OR a massive restructure of the entire system to address its structure and financing.

What’s clear from these reports is the enormity of the health economy today and tomorrow, the lack of adequate attention and Congressional Action to address its sustainability and the range of unintended, negative consequences on households and every other industry if left unattended. It’s illustrative of the disconnect between the Fed and CMS: one assumes it controls the money supply while delegating to the other spending and policies independent of broader societal issues and concerns.

The health economy needs fresh attention from inside and outside the industry. Its impact includes not only the wellbeing of its workforce and services provided its users. It includes its direct impact on household financial security, community health and the economic potential of other industries who get less because healthcare gets more.

Securing the long-term sustainability of the U.S. economy and its role in world affairs cannot be appropriately addressed unless its health economy is more directly integrated and scrutinized. That might be uncomfortable for insiders but necessary for the greater good. Recognition of the disconnect between the Fed and CMS is a start!

Last Thursday, the Senate Finance Committee heard testimony from experts who offered damning testimony about hospital consolidation (excerpts below). Committee Chair Ron Wyden (D-OR) gaveled the session to order with this commentary:

“I’d like to talk about health care costs and quality. Advocates for proposed mergers often say they will bring lower health costs due to increased efficiency. Time after time, it’s simply not proven to be the case. When hospitals merge, prices go up, not down. When insurers merge, premiums go up, not down. And quality of care is not any better with this higher cost. “

Ranking Member Mike Crapo (R-ID) offered a more conciliatory assessment in his opening statement: “In exploring and addressing these problems, we have the opportunity to build on our efforts to improve medication access and affordability by taking a broader look at the health care system through a similarly bipartisan, consensus-based lens…We need to examine the drivers of consolidation, as well as its effects on care quality and costs, both for patients and taxpayers. We also need to develop focused, bipartisan and bicameral solutions that reduce out-of-pocket spending while protecting access to lifesaving services.”

Congress’ concern about consolidation in healthcare is broad-based. Pharmacy benefits managers and health insurers face similar scrutiny. Drug price control referenda have passed in several states and a federal cap was included in the Inflation Reduction Act.

The reality is this: the entire U.S. health system is on trial in the court of public opinion for ‘careless disregard for affordability’. And hospitals are seen as part of the problem justifying consolidation as a defense mechanism.

What followed in this 3-hour hearing was testimony from 3 experts critical of hospital consolidation, a Colorado community hospital CEO who opined to competition with big hospital systems and a Peterson Foundation spokesperson who offered that data access and transparency are necessary to mitigate consolidation’s downside impact.

None of their testimony was surprising. Nor were questions from the 25 members of the committee. It’s a narrative that played out in House Energy and Commerce and Ways and Means Committee hearings last month. It’s likely to continue.

Often, Congressional Hearings on healthcare issues amount to little more than political theatre. In this one, four key themes emerged:

Consolidation among hospitals has adversely impacted quality of care and affordability of healthcare. Prices have gone up without commensurate improvements in quality harming consumers.

Larger organizations use horizontal and vertical integration to strengthen their positions relative to smaller competitors. Physician employment by hospitals is concerning. Rural and safety net hospitals are impaired most.

Anti-trust efforts, price transparency mandates, data sharing and value-based programs have not been as effective as anticipated.

Physicians are victims of consolidation and corporatization in U.S. healthcare. They’re paid less because others are paid more.

While committee members varied widely in the intensity of their animosity toward hospitals, a consensus emerged that the hospital status quo is not working for voters and consumers.

My take:

Consolidation is part of everyday life. Last Tuesday’s bombshell announcement of the merger of the PGA Tour and the Saudi Arabia’s Public Investment Fund caught the golfing world by surprise. Anti-trust issues and monopolistic behaviors are noticed by voters and lawmakers. Hospital consolidation is no exception festering suspicions among lawmakers and voters that the public’s good is ill-served. And studies showing that charity care among not-for-profit hospitals is lower than for-profit confuse and complicate.

As I listened to the hearing, I had questions…

Were all relevant perspectives presented?

Was the information provided by witnesses and cited in Committee member questioning accurate?

Will meaningful action result?

But having testified before Congressional Committees, I find myself dismissive of most hearings which seem heavy on political staging but light on meaningful insight. Many are little more than political theatre. Hospital consolidation seems different. There seems to be growing consensus that it’s harmful to some and costly to all.

Sadly, this hearing is the latest evidence that the good will built by hospital heroics in the pandemic is now forgotten. It’s clear hospital consolidation is an issue that faces strong and increased headwinds with evidence mounting—accurate or not– showing more harm than good.

Many health system mergers today are “all about leverage” when negotiating with payers, rather than significant cost savings or increasing market share, Charlie Shields, CEO of Kansas City, Mo.-based University Health, told the Kansas City Business Journal.

Mr. Shields’ comments came after Kansas City-based St. Luke’s Health System and St. Louis-based BJC HealthCare signed a letter of intent to form an integrated academic health system.

The proposed merger is not about reducing costs — since the two systems have been part of a buying collective for a decade —- and is not about a rapid gain in market share, since St. Luke’s and BJC will largely stick to their respective areas, Mr. Shields told the Journal in a June 1 article. Instead, he argues, the merger, and similar ones like it, aims to leverage a better seat at the table when negotiating care rates with payers.

BJC and St. Luke’s operate the three top hospitals in Missouri, according to U.S. News & World Report. Together, they would pool $10 billion in revenue to serve more than 6 million residents across Missouri, Illinois and Kansas.

The transaction is expected to close by the end of 2023, pending regulatory review.

On October 1, 1908, Ford produced the first Model T automobile. More than 60 years later, this affordable, mass produced, gasoline-powered car was still the top-selling automobile of all time. The Model T was geared to the broadest possible market, produced with the most efficient methods, and used the most modern technology—core elements of Ford’s business strategy and corporate DNA.

On April 25, 2018, almost 100 years later, Ford announced that it would stop making all U.S. internal-combustion sedans except the Mustang.

The world had changed. The Taurus, Fusion, and Fiesta were hardly exciting the imaginations of car-buyers. Ford no longer produced its U.S. cars efficiently enough to return a suitable profit. And the internal combustion technology was far from modern, with electronic vehicles widely seen as the future of automobiles.

Ford’s core strategy, and many of its accompanying products, had aged out. But not all was doom and gloom; Ford was doing big and profitable business in its line of pickups, SUVs, and -utility vehicles, led by the popular F-150.

It’s hard to imagine the level of strategic soul-searching and cultural angst that went into making the decision to stop producing the cars that had been the basis of Ford’s history. Yet, change was necessary for survival. At the time, Ford’s then-CEO Jim Hackett said, “We’re going to feed the healthy parts of our business and deal decisively with the areas that destroy value.”

So Ford took several bold steps designed to update—and in many ways upend—its strategy. The company got rid of large chunks of the portfolio that would not be relevant going forward, particularly internal combustion sedans. Ford also reorganized the company into separate divisions for electric and internal combustion vehicles. And Ford pivoted to the future by electrifying its fleet.

Ford did not fully abandon its existing strategies. Rather, it took what was relevant and successful, and added that to the future-focused pivot, placing the F-150 as the lead vehicle in its new electric fleet.

This need for strategic change happens to all large organizations. All organizations, including America’s hospitals and health systems, need to confront the fact that no strategic plan lasts forever.

Over the past 25-30 years, America’s hospitals and health systems based their strategies on the provision of a high-quality clinical care, largely in inpatient settings. Over time, physicians and clinics were brought into the fold to strengthen referral channels, but the strategic focus remained on driving volume to higher-acuity services.

More recently, the longstanding traditional patient-physician-referral relationship began to change. A smarter, internet-savvy, and self-interested patient population was looking for different aspects of service in different situations. In some cases, patients’ priority was convenience. In other cases, their priority was affordability. In other cases, patients began going to great lengths to find the best doctors for high-end care regardless of geographic location. In other cases, patients wanted care as close as their phone.

Around the country, hospitals and health systems have seen these environmental changes and adjusted their strategies, but for the most part only incrementally. The strategic focus remains centered on clinical quality delivered on campus, while convenience, access, value, affordability, efficiency, and many virtual innovations remain on the strategic periphery.

Health system leaders need to ask themselves whether their long-time, traditional strategy is beginning to age out. And if so, what is the “Ford strategy” for America’s health systems?

The questions asked and answered by Ford in the past five years are highly relevant to health system strategic planning at a time of changing demand, economic and clinical uncertainty, and rapid innovation. For example, as you view your organization in its entirety, what must be preserved from the existing structure and operations, and what operations, costs, and strategies must leave? And which competencies and capabilities must be woven into a going-forward structure?

America’s hospitals and health systems have an extremely long history—in some cases, longer than Ford’s. With that history comes a natural tendency to stick with deeply entrenched strategies. Now is the time for health systems to ask themselves, what is our Ford F150? And how do we “electrify” our strategic plan going forward?

A couple of months ago, I got a call from a CEO of a regional health system—a long-time client and one of the smartest and most committed executives I know. This health system lost tens of millions of dollars in fiscal year 2022 and the CEO told me that he had come to the conclusion that he could not solve a problem of this magnitude with the usual and traditional solutions. Pushing the pre-Covid managerial buttons was just not getting the job done.

This organization is fiercely independent. It has been very successful in almost every respect for many years. It has had an effective and stable board and management team over the past 30 to 40 years.

But when the CEO looked at the current situation—economic, social, financial, operational, clinical—he saw that everything has changed and he knew that his healthcare organization needed to change as well. The system would not be able to return to profitability just by doing the same things it would have done five years or 10 years ago. Instead of looking at a small number of factors and making incremental improvements, he wanted to look across the total enterprise all at once. And to look at all aspects of the enterprise with an eye toward organizational renovation.

I said, “So, you want a makeover.”

The CEO is right. In an environment unlike anything any of us have experienced, and in an industry of complex interdependencies, the only way to get back to financial equilibrium is to take a comprehensive, holistic view of our organizations and environments, and to be open to an outcome in which we do things very differently.

In other words, a makeover.

Consider just a few areas that the hospital makeover could and should address:

There’s the REVENUE SIDE: Getting paid for what you are doing and the severity of the patient you are treating—which requires a focus on clinical documentation improvement and core revenue cycle delivery—and looking for any material revenue diversification opportunities.

There is the relationship with payers: Involving a mix of growth, disruption, and optimization strategies to increase payments, grow share of wallet, or develop new revenue streams.

There’s the EXPENSE SIDE: Optimizing workforce performance, focusing on care management and patient throughput, rethinking the shared services infrastructure, and realizing opportunities for savings in administrative services, purchased services, and the supply chain. While these have been historic areas of focus, organizations must move from an episodic to a constant, ongoing approach.

There’s the BALANCE SHEET: Establishing a parallel balance sheet strategy that will create the bridge across the operational makeover by reconfiguring invested assets and capital structure, repositioning the real estate portfolio, and optimizing liquidity management and treasury operations.

There is NETWORK REDESIGN: Ensuring that the services offered across the network are delivered efficiently and that each market and asset is optimized; reducing redundancy, increasing quality, and improving financial performance.

There is a whole concept around PORTFOLIO OPTIMIZATION: Developing a deep understanding of how the various components of your business perform, and how to optimize, scale back, or partner to drive further value and operational performance.

Incrementalism is a long-held business approach in healthcare, and for good reason. Any prominent change has the potential to affect the health of communities and those changes must be considered carefully to ensure that any outcome of those changes is a positive one. Any ill-considered action could have unintended consequences for any of a hospital’s many constituencies.

But today, incrementalism is both unrealistic and insufficient.

Just for starters, healthcare executive teams must recognize that back-office expenses are having a significant and negative impact on the ability of hospitals to make a sufficient operating margin. And also, healthcare executive teams must further realize that the old concept of “all things to all people” is literally bringing parts of the hospital industry toward bankruptcy.

As I described in a previous blog post, healthcare comprises some of the most wicked problems in our society—problems that are complex, that have no clear solution, and for which a solution intended to fix one aspect of a problem may well make other aspects worse.

The very nature of wicked problems argues for the kind of comprehensive approach that the CEO of this organization is taking—not tackling one issue at a time in linear fashion but making a sophisticated assessment of multiple solutions and studying their potential interdependencies, interactions, and intertwined effects.

My colleague Eric Jordahl has noted that “reverting to a 2019 world is not going to happen, which means that restructuring is the only option. . . . Where we are is not sustainable and waiting for a reversion is a rapidly decaying option.”

The very nature of the socioeconomic environment makes doing nothing or taking an incremental approach untenable. It is clearly beyond time for the hospital industry makeover.

A recent chat with a former physician entrepreneur who recently sold his practice to a large health system highlighted the fact that “hospital-physician integration” can sometimes be a misnomer. “I feel like we were sold a bill of goods,” he told us, referring to his ten-person primary care group.

“We worked hard to build this practice, and the health system CEO made a lot of promises about the value of bringing us in, and the investments they’d make in our growth.” Instead, the group has experienced a different reality: little meaningful integration, an unclear bureaucracy to navigate, zero transparency into the finances of the medical group or system, leadership turnover, and a lack of strategic vision.

“We would never sign this deal again,” he said, “and we’re not the only ones—they might not realize it, but this system is on the precipice of a full-on physician mutiny.”

Of course, there are two sides to every story, but the anecdote reinforced in our minds the importance of careful planning and attention to integration following practice acquisitions. There needs to be a plan, it needs to be clear, and it needs to be resourced.

Otherwise, systems risk ending up with unhappy, disengaged doctors—a situation to be avoided at all costs.