Jefferson’s hospital network will grow to 18 locations with Einstein’s three general acute care hospitals and an inpatient rehabilitation hospital.

The merger between Pennsylvania-based Jefferson Health and Einstein Healthcare Network can now close after the Federal Trade Commission voted to withdraw its opposition to the deal, Jefferson Health announced this week.

The deal is now expected to be finalized within the next six months.

Earlier this year, the FTC voted 4-0 to voluntarily dismiss its appeal to the Third Circuit of the district court, according to the commission’s case summary.

Once the deal is complete, Jefferson’s network of hospitals will grow to 18 with the addition of Einstein’s three general acute care hospitals and an inpatient rehabilitation hospital.

WHY IT MATTERS

Merger plans were first announced in 2018 in a deal estimated to be worth $599 million.

The FTC initially blocked the merger because it believed it would reduce competition in the Philadelphia and Montgomery counties.

It alleged the deal would give the two health systems control of at least 60% of the inpatient general acute care hospital services market in North Philadelphia, at least 45% of that market in Montgomery County, and at least 70% of the inpatient acute rehabilitation services market in the Philadelphia area.

But late last year, a federal judge blocked the FTC’s attempt to stop the merger. Judge Gerald Pappert of the U.S. District Court for the Eastern District of Pennsylvania wrote that the FTC failed to demonstrate that there’s a credible threat of harm to competition. He pointed to other competitors in the region, such as Penn Medicine, Temple Health and Trinity Health Mid-Atlantic.

The FTC and the Commonwealth of Pennsylvania attempted to appeal the court’s decision, but after Jefferson and Einstein filed a motion to withdraw the case, the commission unanimously voted to drop its appeal.

THE LARGER TREND

The FTC is taking a closer look at healthcare mergers and acquisitions to better understand how physician practice and healthcare facility mergers affect competition. Earlier this year, it sent orders to Aetna, Anthem, Florida Blue, Cigna, Health Care Service Corporation and United Healthcare to share patient-level claims data for inpatient, outpatient and physician services across 15 states from 2015 through 2020.

The analysts expect activity to ramp up moving forward, however. They predict that as health systems evaluate their business strategies post-pandemic, those in strong positions will take advantage of other systems’ divestitures to grow their capabilities and expand into new markets.

ON THE RECORD

“We are excited to have Einstein and Jefferson come together, as our shared vision will enable us to improve the lives of patients, the health of our communities and enhance our health education and research capabilities,” said Ken Levitan, the interim president and CEO of Einstein Healthcare Network.

“By bringing our resources together, we can offer those we care for – particularly the historically underserved populations in Philadelphia and Montgomery County – even greater access to high-quality care.”

The Federal Trade Commission has closed its investigation of the merger between Atrium Health Navicent and Houston Healthcare System following news the two have abandoned their plans for a deal.

FTC staff had recommended commissioners challenge the merger on grounds that it would have led to “significant harm” for area residents and businesses in the form of higher healthcare costs, the FTC alleged.

The tie-up between two of the largest systems in central Georgia would also hamper investment in facilities, technologies and expanded access to services, according to a statement released Wednesday.

Dive Insight:

FTC Acting Chairwoman Rebecca Kelly Slaughter said in the statement, “This is great news for patients in central Georgia.”

When the deal was originally announced, Atrium Health Navicent promised to spend $150 million on Houston over a decade, earmarking the money for routine capital expenditures and strategic growth initiatives, according to a previous review of the transaction by the state attorney general’s office.

After engaging with consultants at Kaufman Hall in 2017, leaders at Houston, an independent system, decided they needed to find a strategic partner to weather long-term challenges and ultimately picked Navicent.

Navicent recently merged with North Carolina-based Atrium Health, formerly known as Carolinas HealthCare System. At the time, the deal gave Atrium a foothold in the state of Georgia.

Healthcare consolidation has continued at a steady clip despite the pandemic, and the FTC will be closely investigating any deal involving close competitors. The agency is seeking to expand its arsenal to block future mergers by researching new theories of harm.

The FTC attempted to block a hospital deal in Philadelphia last year but has since abandoned its challenge after a series of setbacks in court. The judge was not swayed that the consolidation of providers would lead to an increase in prices given the plethora of healthcare options in the area.

Even though signs point to a post-COVID spike in health system mergers, retailers, insurers, and other healthcare industry players already far exceed health system scale. Even the largest of the “mega health systems” pale in comparison to other healthcare companies up and down the value chain, as shown in the graphic above. And with the exception of pharma, these other industry players have seen revenues surge during the pandemic, while health system growth has stagnated.

According to a recent report from Kaufman Hall, hospitals saw a three percent reduction in annual total gross revenue in 2020.The majority of the decrease stemmed from a six percent decline in outpatient revenue, as volumes plummeted during the pandemic.

The largest companies listed here, including Walmart, Amazon, CVS, and UnitedHealth Group, continue to double down on vertical integration strategies, configuring an array of healthcare assets into platform businesses focused on delivering value to consumers.

To remain relevant, health systems will need to increase their focus on this strategy as well, assembling the right capabilities for a marketplace driven by value, at a scale that enables rapid innovation and sustainability.

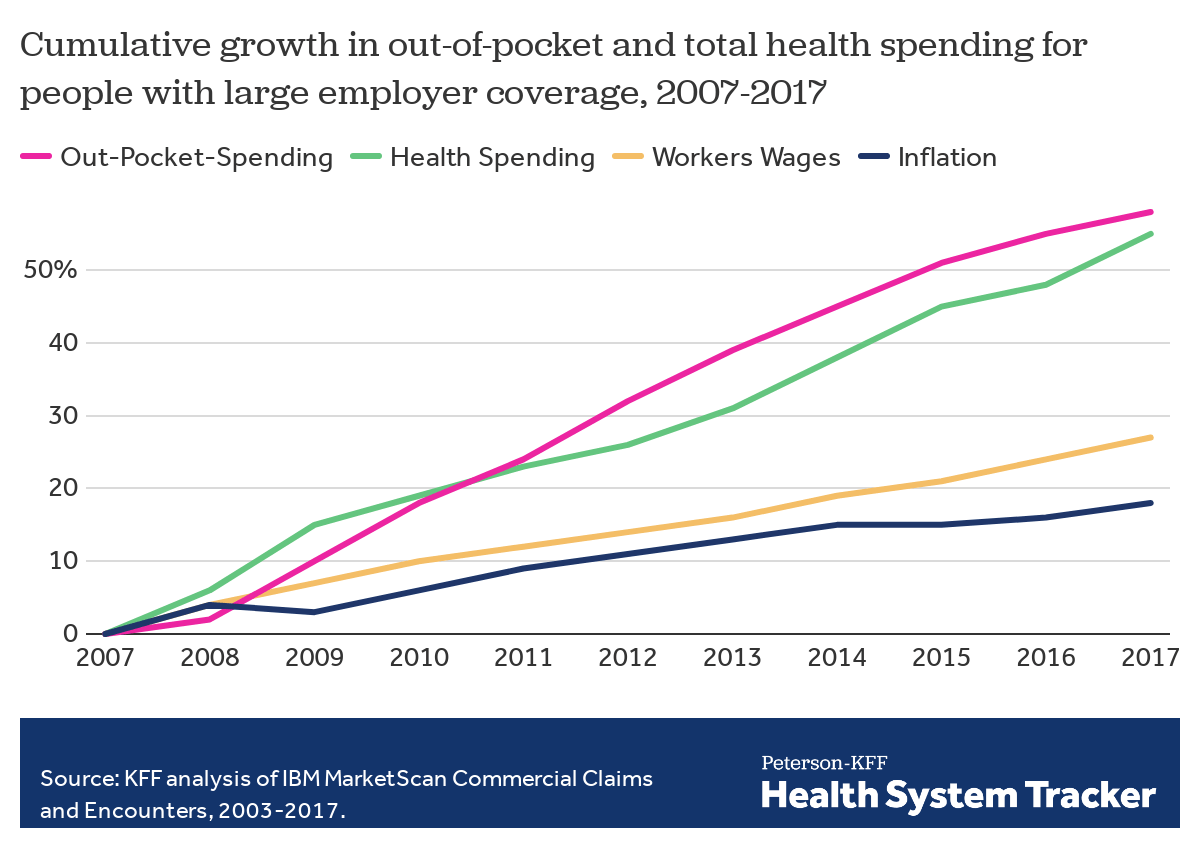

Employers — including companies, state governments and universities — purchase health care on behalf of roughly 150 million Americans. The cost of that care has continued to climb for both businesses and their workers.

For many years, employers saw wasteful care as the primary driver of their rising costs. They made benefits changes like adding wellness programs and raising deductibles to reduce unnecessary care, but costs continued to rise. Now, driven by a combination of new research and changing market forces — especially hospital consolidation — more employers see prices as their primary problem.

By amassing and analyzing employers’ claims data in innovative ways, academics and researchers at organizations like the Health Care Cost Institute (HCCI) and RAND have helped illuminate for employers two key truths about the hospital-based health care they purchase:

1) PRICES VARY WIDELY FOR THE SAME SERVICES

Data show that providers charge private payers very different prices for the exact same services — even within the same geographic area.

For example, HCCI found the price of a C-section delivery in the San Francisco Bay Area varies between hospitals by as much as:$24,107

Data show that hospitals charge employers and private insurers, on average, roughly twice what they charge Medicare for the exact same services. A recent RAND study analyzed more than 3,000 hospitals’ prices and found the most expensive facility in the country charged employers:4.1xMedicare

Hospitals claim this price difference is necessary because public payers like Medicare do not pay enough. However, there is a wide gap between the amount hospitals lose on Medicare (around -9% for inpatient care) and the amount more they charge employers compared to Medicare (200% or more).

Employer Efforts

A small but growing group of companies, public employers (like state governments and universities) and unions is using new data and tactics to tackle these high prices. (Learn more about who’s leading this work, how and why by listening to our full podcast episode in the player above.)

Note that the employers leading this charge tend to be large and self-funded, meaning they shoulder the risk for the insurance they provide employees, giving them extra flexibility and motivation to purchase health care differently. The approaches they are taking include:

Steering Employees

Some employers are implementing so-called tiered networks, where employees pay more if they want to continue seeing certain, more expensive providers. Others are trying to strongly steer employees to particular hospitals, sometimes know as centers of excellence, where employers have made special deals for particular services.

Purdue University, for example, covers travel and lodging and offers a $500 stipend to employees that get hip or knee replacements done at one Indiana hospital.

Negotiating New Deals

There is a movement among some employers to renegotiate hospital deals using Medicare rates as the baseline — since they are transparent and account for hospitals’ unique attributes like location and patient mix — as opposed to negotiating down from charges set by hospitals, which are seen by many as opaque and arbitrary. Other employers are pressuring their insurance carriers to renegotiate the contracts they have with hospitals.

In 2016, the Montana state employee health plan, led by Marilyn Bartlett, got all of the state’s hospitals to agree to a payment rate based on a multiple of Medicare. They saved more than $30 million in just three years. Bartlett is now advising other states trying to follow her playbook.

In 2020, several large Indiana employers urged insurance carrier Anthem to renegotiate their contract with Parkview Health, a hospital system RAND researchers identified as one of the most expensive in the country. After months of tense back-and-forth, the pair reached a five-year deal expected to save Anthem customers $700 million.

Legislating, Regulating, Litigating

Some employer coalitions are advocating for more intervention by policymakers to cap health care prices or at least make them more transparent. States like Colorado and Indiana have passed price transparency legislation, and new federal rules now require more hospital price transparency on a national level. Advocates expect strong industry opposition to stiffer measures, like price caps, which recently failed in the Montana legislature.

Other advocates are calling for more scrutiny by state and federal officials of hospital mergers and other anticompetitive practices. Some employers and unions have even resorted to suing hospitals like Sutter Health in California.

Employer Challenges

Employers face a few key barriers to purchasing health care in different and more efficient ways:

Provider Power

Hospitals tend to have much more market power than individual employers, and that power has grown in recent years, enabling them to raise prices. Even very large employers have geographically dispersed workforces, making it hard to exert much leverage over any given hospital. Some employers have tried forming purchasing coalitions to pool their buying power, but they face tricky organizational dynamics and laws that prohibit collusion.

Sophistication

Employers can attempt to lower prices by renegotiating contracts with hospitals or tailoring provider networks, but the work is complicated and rife with tradeoffs. Few employers are sophisticated enough, for example, to assess a provider’s quality or to structure hospital payments in new ways.Employers looking for insurers to help them have limited options, as that industry has also become highly consolidated.

Employee Blowback

Employers say they primarily provide benefits to recruit and retain happy and healthy employees. Many are reluctant to risk upsetting employees by cutting out expensive providers or redesigning benefits in other ways. A recent KFF survey found just 4% of employers had dropped a hospital in order to cut costs.

The Tradeoffs

Employers play a unique role in the United States health care system, and in the lives of the 150 million Americans who get insurance through work. For years, critics have questioned the wisdom of an employer-based health care system, and massive job losses created by the pandemic have reinforced those doubts for many.

Assuming employers do continue to purchase insurance on behalf of millions of Americans, though, focusing on lowering the prices they pay is one promising path to lowering total costs. However, as noted above, hospitals have expressed concern over the financial pressures they may face under these new deals. Complex benefit design strategies, like narrow or tiered networks, also run the risk of harming employees, who may make suboptimal choices or experience cost surprises. Finally, these strategies do not necessarily address other drivers of high costs including drug prices and wasteful care.

With nearly 30% of workers now having a high deductible health plan and a typical family being responsible for on average the first $8,000 of costs, consumers are increasingly weighing care versus cost. Historically, with a small copay, you would conveniently take care of an ailment without shopping around, but with the average person now bearing the brunt of the initial costs, wouldn’t you want to know how much a service costs and what other providers are charging before you “buy” the service?

CMS believes“consumers should be able to know, long before they open a medical bill, roughly how much a hospital will charge for items and services it provides.” Cue the hospital price transparency rule that just went into effect January 1, 2021. Hospitals are now required to post their standard charges, including the rates they negotiate with insurers, and the discounted price a hospital is willing to accept directly from a patient if paid in cash. As a consumer, the intent is to make it “easier to shop and compare prices across hospitals and estimate the cost of care before going to the hospital.”

There are a few different angles to analyze here:

Are hospitals following the rules?

Each hospital must post online a comprehensive machine readable file with all items and services, including gross charges, actual negotiated prices with insurers, and the cash price for patients who are uninsured. Additionally, hospitals must post the costs for 300 common “shoppable” services in a “consumer-friendly format.” Some hospitals and health systems have done a good job at posting these prices in a digestible format, like the Cleveland Clinic or Sutter Health, but others have posted complicated spreadsheets, relied on online cost estimator tools, or simply not posted them at all. An analysis from consulting firm ADVI of the top 20 largest hospitals in the U.S. found that not all of them appeared to completely comply with this mandate. In some instances, data was not able to be downloaded in a useable format, others did not post the DRG or service codes, and the variability in the terms/categories used simply created difficulty in comparing pricing information across hospitals. CMS has stated that a failure to comply with the rules could result in a fine of up to $300 per day. As with most new rules, there are growing pains, and hospitals will likely get better at this over time, assuming the data is being used for its original intent.

Is this helpful to consumers?

Consumers will able to see the variation in prices for the exact same service or procedure between hospitals and get an estimate of what they will be charged before getting the care. But how likely is the average person to go to their hospital’s website, look at a price, and change their decision about where to get care? In addition, awareness of these price transparency tools is still low among consumers. Frankly, it is competitors and insurers that have been first in line to review the data. Looking through a number of hospital websites, and even certain state agency sites that have done a good job at summarizing the costs, like Florida Health Price Finder, the price transparency tools are helpful, but appear to be much more suited for relatively standardized services that can be scheduled in advance, like a knee replacement. It’s highly unlikely you will be telling your ambulance driver what hospital to go to based on cost while in cardiac arrest…Plus, it’s all still confusing – even physicians have shared their bewilderment, when trying to decipher and compare pricing. Conceptually, price transparency should be beneficial to consumers, but it will take time; and it will need to involve not just the hospitals posting rates, but the outpatient care facilities as well. Knowing what you will pay before you decide to go to a physician’s office or a clinic or an urgent care or an ED will hopefully help drive consumers to make more educated decisions in the future.

Will this ultimately drive down costs?

I sure hope so. Revealing actual negotiated prices between hospitals and insurers should push the more expensive hospitals in the area to reduce prices, especially if consumers start using the other hospitals, instead. However, it could also have an inverse effect, with lower cost hospitals insisting on a payment increase from insurers; thereby driving up costs. In the end, as has historically been the case, the market power of certain providers will likely dictate the direction of costs in a given region. That is, until both price AND quality become fully transparent and the consumer is armed with the tools to shop for the best care at the lowest cost – consumerism here we come.

Health insurers are no longer immune from federal antitrust scrutiny for conduct considered the business of insurance.

The Competitive Health insurance Reform Act of 2020 became law on January 13, a move praised by the Department of Justice but opposed by health insurers.

Health insurers are no longer immune from federal antitrust scrutiny for conduct considered the business of insurance and regulated by state law.

With enactment of the Competitive Health Insurance Reform Act, the DOJ and Federal Trade Commission have expanded authority to prosecute alleged anticompetitive behavior, including data sharing between insurers.

The McCarran-Ferguson Act previously afforded immunity by exempting from federal antitrust laws certain conduct considered the “business of insurance.” This exemption has sometimes been interpreted by courts to allow a range of what the Justice Department considered “harmful” anticompetitive conduct in health insurance markets.

The new law aims to promote more competition in health insurance markets by limiting the scope of conduct that’s exempt from antitrust laws. This move was praised by the Trump Justice Department shortly before the former president left office.

WHAT’S THE IMPACT?

The antitrust scrutiny is coming at a time when insurers are under a deadline to meet interoperability standards to share information with patients that meet Fast Healthcare Interoperability Resources, or FHIR, standards.

Eliminating the exemption undermines the goal of affordable coverage by adding administrative red tape and reducing market competition, according to Matt Eyles, president and CEO of America’s Health Insurance Plans.

“The McCarran-Ferguson Act recognized that all healthcare is local, and that states should be able to govern their own health insurance markets,” Eyles said in December. “Removal of this exemption adds tremendous administrative costs while delivering absolutely no value for patients and consumers. It will unnecessarily add layers of bureaucracy, destabilize markets, create conflicting federal and state oversight requirements, and lead to costly litigation.”

The National Association of Insurance Commissioners sent a letter to Senate leaders on December 2 voicing its concern for the bill’s passage.

“The premise of the Competitive Health Insurance Reform Act is that collusion among health insurance companies is permitted under state law and that the McCarran-Ferguson Act somehow currently protects these practices. This is not true. The McCarran-Ferguson antitrust exemption for health insurance does not allow or encourage conspiratorial behavior but simply leaves oversight of insurance, including health insurance, to the states – and state laws do not allow collusion,” commissioners said.

“The potential for bid rigging, price-fixing and market allocation is of great concern to state insurance regulators and we share your view that such practices would be harmful to consumers and should not be tolerated. However, we want to assure you that these activities are not permitted under state law,” commissioners wrote.

While insurers have not been thrilled with the move, Consumer Reports said the legislation is good for providers who have felt pressured into contract terms that benefit insurers.

THE LARGER TREND

The Justice Department has a track record of successfully enforcing the antitrust laws against health insurers. Over the past five years, the department has enforced the antitrust laws against health insurers involved in transactions valued at over $160 billion.

The Act will help the department build on those successes by requiring health insurers to play by the same rules as competitors in other industries. It will clarify when health insurers qualify for the McCarran-Ferguson exemption, and it will enable the Antitrust Division to spend resources more efficiently to achieve desired results, the Justice Department said.

On January 13, Trump signed into law the Competitive Health Insurance Reform Act of 2020, which limits the antitrust exemption available to health insurance companies under the McCarran-Ferguson Act. The act, sponsored by Rep. Peter DeFazio (D-Ore), passed the House of Representatives on Sept. 21, 2020 and passed the Senate on Dec. 22.

As happened with cars in the 1960s, price competition among brand-name drugs is hard to find.

Before 1973, when the Arab oil embargo upended the U.S. auto industry, Americans witnessed an annual ritual by carmakers. In the late summer, the Big Three — Ford, Chrysler, and General Motors — would release sticker prices for their products, always showing increases, of course.

Almost always, the increases from each company for similar models were nearly identical. If one company’s was out of line — substantially bigger or smaller than its erstwhile competitors’ — it quickly made an adjustment. Explicit collusion to fix prices was never proven, but the effect for consumers was the same.

Now, researchers report that something very similar seems to be occurring for big-market brand-name drugs, including anti-diabetic medications and blood thinners.

Average wholesale prices for products in five classes — direct-acting oral anticoagulants (DOACs), P2Y12 inhibitors, glucagon-like peptide-1 (GLP-1) agonists, dipeptidyl dipeptidase-4 (DPP-4) inhibitors, and sodium-glucose transport protein-2 (SGLT-2) inhibitors — increased in “lock-step” each year from 2015 to 2020, according to Joseph Ross, MD, of Yale University in New Haven, Connecticut, and colleagues writing in JAMA Network Open.

These increases ranged from annual averages of 6.6% for DDP4 inhibitors to 13.5% for P2Y12 inhibitors — far outpacing not only inflation in general, but even the 2.1% average for all prescription drugs.

Within each class, Kendall τb correlation coefficients for average wholesale prices were as follows:

DOACs: 0.98

SGLT-2 inhibitors: 0.98

DPP-4 inhibitors: 0.96

GLP-1 agonists: 0.92

P2Y12 inhibitors: 0.75

“These results suggest there was little price competition among the sponsors of these products,” Ross and colleagues wrote.

Although the analysis came with significant limitations — it didn’t account for rebates or other discounts, for example — the researchers said some patients must suffer from these increases.

“Rebates, list prices, and net prices have been growing for brand-name medications, and rebate growth has been shown to positively correlate with list price growth, thereby impacting costs faced by patients paying a percentage of (or the full) list price,“ the group noted. “Therefore, the lock-step price increases of brand-name medications, without evidence of price competition, raise concerns and would be expected to adversely affect patient adherence to medications and thus clinical outcomes.”

For the car buyers, the solution to lock-step price increases was imposed from outside: soaring gas prices in the mid-1970s prompted demand for vehicles with better fuel economy than domestic makers were prepared to sell. That opened the market to Japanese cars that not only got better mileage, but were also more reliable and (in many cases) cheaper than Big Three products. Thus ended Detroit’s ability to set prices.

How to rein in Big Pharma is less clear. For their part, Ross and colleagues suggested policies to limit such lock-step price hikes, shortened patent exclusivity periods, and faster introduction of generic equivalents.

UnitedHealth Group, both the nation’s largest health insurer and largest employer of physicians, just announced plans to continue to rapidly grow the number of physicians in its Optum division.

This week CEO Dave Wichmann told investors in the company’s fourth quarter earnings call that Optum entered 2021 with over 50,000 employed or affiliated physicians, and expects to add at least 10,000 more across the year.(For context,HCA Healthcare, the largest for-profit US health system, employs or affiliates with roughly 46,000 physicians, and Kaiser Permanente employs about 23,300.) Optum is already making progress toward its ambitious goal with the announcement last week that the company is in talks to acquire Atrius Health, a 715-physician practice in the Boston area.

As was the case with other health plans, United’s health insurance business took an expected hit last quarter due to increased costs from COVID testing and treatment, combined with rebounding healthcare utilization. Optum, however, saw revenue up over 20 percent, which drove much of the company’s overall fourth quarter growth.

Expect United, and other large insurers, flush with record profits from last year, to continue to expand their portfolio of care, digital and analytics assets(see also Optum’s recently announced plan to acquire Change Healthcare for $13B) as they looks to grow integrated insurance and care delivery offerings.

It’s part of what we expect to be a 2021 “land grab” for strategic advantage in healthcare, as providers, health plans, and disruptors look to create comprehensive platforms to secure long-term consumer loyalty.

Neighborhoods in cities like Chicago are rapidly becoming places where people can’t fill medical prescriptions locally because their drugstores have shuttered or don’t accept Medicaid.

Why it matters:The pandemic has accelerated the growth of “pharmacy deserts” as unprofitable and less-profitable stores have closed. It’s a worrisome trend for the urban poor, who are less likely to try online pharmacies and more likely to let their drug regimens lapse when they can’t get medication locally.

Driving the news: Effective Dec. 1, Medicaid patients in Illinois — of which there are 400,000, per the Chicago Tribune — could no longer get their prescriptions filled at Walgreens, a prevalent chain headquartered in a Chicago suburb.

The change came because Aetna, which provides contracts with the state of Illinois to serve Medicaid recipients, dropped Walgreens as a provider. CVS — a top Walgreens rival — owns Aetna as well as the pharmacy benefits manager CVS Caremark.

CVS “has no pharmacies in five key West Side neighborhoods,” per the Tribune.

Illinois state Rep. La Shawn Ford called Aetna’s decision “pathetic” and told the Tribune, “It’s an attack not just on Black people, but on those that are struggling during the pandemic.”

The backstory:Researcher Dima Qato coined the term “pharmacy desert” in a 2014 article that found there were far fewer pharmacies in Chicago’s Black neighborhoods than in white and mixed neighborhoods.

Medicaid policies like the one in Illinois “are all over the country, where Medicaid dictates where and where you can go fill your medication,” Qato tells Axios. “And that leads to certain pharmacies having less patients in them, which leads to less profits, which leads to closures.”

Qato — who recently took a post as a professor at the University of Southern California, and is in the process of moving from Chicago — said that the new Medicaid policy in Illinois is generating “a lot of outrage in the community right now.”

Per Qato’s definition, people live in a “pharmacy desert” if they can’t fill a prescription within a half-a-mile of their homes (for low-income people without cars), and a mile for others.

“We’ve estimated it for Chicago at a third of the city’s population, with substantial difference by racial composition,” Qato says.

Between the lines:Because pharmacies get the lowest reimbursements for filling Medicaid prescriptions, they’re more likely to close stores in low-income neighborhoods and open them in wealthy ones, notes Antonio Ciaccia, chief strategy officer of 3 Axis Advisors, a consultancy focused on the drug supply chain.

“We’re seeing a general retreat from impoverished areas,” said Ciaccia, who serves as an adviser to the American Pharmacy Association.

Of note:Studies draw a direct line between pharmacy closures and people stopping their vital medications — with terrible health outcomes.

Adults over 50 were more likely to drop their cardiovascular pills after their local drug store closed, according to a study published in the Journal of the American Medical Association in 2019 (of which Qato is the lead author).

Benjy Renton, the Middlebury College senior who has been closely tracking the COVID-19 outbreak, noted on Twitter that pharmacy deserts could hold back the administration of vaccines.

What’s next:While “food deserts,” where inner-city residents lack access to fresh and healthy groceries, are a bigger problem in places like New York City, pharmacy access is a growing concern. The number of drugstores has declined 20% in NYC since 2016, according to Jonathan Bowles, executive director of the Center for an Urban Future.

“I for one will miss the 70 Duane Reades that closed this year,” was the headline of an an article that New York Magazine’s “Curbed” ran on Dec. 30. (Duane Reade is owned by Walgreens.)

The annual J.P. Morgan Healthcare Conference is one of the best ways to diagnose the financial condition of the healthcare industry. Every January, every key stakeholder — providers, payers, pharmaceutical companies, tech companies, medical device and supply companies as well as bankers, venture capital and private equity firms — comes together in one exam room, even when it is virtual, for their annual check-up. But as we all know, this January is unlike any other as this past year has been unlike any other year.

You would have to go back to the banking crisis of 2008 to find a similar moment from an economic perspective. At the time, we were asking, “Are banks too big to fail?” The concern behind the question was that if they did fail, the economic chaos that would follow would lead to a collapse with the consumer ultimately picking up the tab. The rest is history.

Healthcare is “Too Vital to Fail”

2020 was historic in too many ways to count. But in a year when healthcare providers faced the worst financial crisis in the history of healthcare, the headline is that they are still standing. And what they proved is that in contrast to banks in 2008 that were seen by many as “too big to fail,” healthcare providers in 2020 proved that they were “too vital to fail.”

One of the many unique things about the COVID-19 pandemic is we are simultaneously experiencing a health crisis, where healthcare providers are the front line in the battle, and an economic crisis, felt in a big way in healthcare given the unique role hospitals play as the largest employer in most communities. Hospitals and health systems have done the vast majority of testing, treating, monitoring, counseling, educating and vaccinating all while searching for PPE and ventilators, and conducting clinical trials. And that’s just the beginning of the list.

Stop and think about that for a minute. What would we have done without them? Thinking through that question will give you some appreciation for the critical, challenging and central role that healthcare providers have had to play over the past year.

Simply stated, healthcare providers are the heart of healthcare, both clinically (essentially 100 percent of the care) and financially (over 50 percent of the $4 trillion annual spend on U.S. healthcare). Over the last year they stepped up and they stepped in at the moment where we needed them the most. This was despite the fact that, like most businesses, they were experiencing calamitous losses with no assurances of any assistance.

Healthcare is “Pandemic-Proof”

This was absolutely the worst-case scenario and the biggest test possible for our nation’s healthcare delivery system. Patient volume and therefore revenue dropped by over 50 percent when the panic of the pandemic was at its peak, driving over $60 billion in losses per month across hospitals and healthcare providers. At the same time, they were dramatically increasing their expenses with PPE, ventilators and additional staff. This was not heading in a good direction. While failure may not have been seen as an option, it was clearly a possibility.

The CARES Act clearly provided a temporary lifeline, providing funding for our nation’s hospitals to weather the storm. While there are more challenging times ahead, it is now clear that most are going to make it to the other side. The system of care in our country is often criticized, but when faced with perhaps the most challenging moment in the history of healthcare, our nation’s hospitals and health systems stepped up heroically and performed miraculously. The work of our healthcare providers on the front line and those who supported them was and is one thing that we all should be exceptionally proud of and thankful for.In 2020, they proved that not only is our nation’s healthcare system too vital to fail, but also that it is “pandemic proof.”

Listening to Front Line at the 2021 J.P. Morgan Healthcare Conference

There has never been a more important year to listen to the lessons from healthcare providers. They are and were the front line of our fight against COVID-19. If there was a class given about how to deal with a pandemic at an institutional level, this conference is where those lessons were being taught.

This year at the J.P. Morgan Healthcare Conference, CEOs, and CFOs from many of the most prestigious and most well-respected health systems in the world presented including AdventHealth, Advocate Aurora Health, Ascension, Baylor Scott & White Health, CommonSpirit Health, Henry Ford Health System, Intermountain Healthcare, Jefferson Health, Mass General Brigham, Northwell Health, OhioHealth, Prisma Health, ProMedica Health System, Providence, Spectrum Health and SSM Health.

I’ve been in healthcare for 30 years and this is my fifth year of writing up the summary of the non-profit provider track of the conference for Becker’s Healthcare to help share the wisdom of the crowd of provider organizations that share their stories. Clearly, this year was different and not because the presentations were virtual, but because they were inspirational.

What did we learn? The good news is that they have made many changes that have the potential to move healthcare in a much better direction and to get to a better place much faster. So, this year instead of providing you a nugget from each presentation, I am going to take a shot at summarizing what they collectively have in motion to stay vital after COVID.

10 Moves Healthcare Providers are Making to Stay Vital After-COVID

As a leader in healthcare, you will never have a bigger opportunity to drive change than right now. Smart leaders are framing this as essentially “before-COVID (BC)” and “after-COVID (AC)” and using this moment as their burning platform to drive change. Credit to the team at Providence for the acronym, but every CEO talked about this concept. As the saying goes, “never let a good crisis go to waste.” Well, we’ve certainly had a crisis, so here is a list of what the top health systems are doing to ensure that they don’t waste it and that they stay vital after-COVID:

1. Take Care of Your Team and They’ll Take Care of You: In a crisis, you can either come together as a team or fall apart. Clearly there has been a significant and stunning amount of pressure on healthcare providers. Many are fearing that mental health might be our nation’s next pandemic in the near future because they are seeing it right now with their own team. Perhaps one of their biggest lessons from this crisis has been the need to address the mental, physical and spiritual health of both team members as well as providers. They have put programs in place to help and have also built a tremendous amount of trust with their team by, in many cases, not laying off and/or furloughing employees. While they have made cuts in other areas such as benefits, this collective approach proved incredibly beneficial. And the last point here that relates to thinking differently about their team is that similar to other businesses, many health systems are making remote arrangements permanent for certain administrative roles and moving to a flexible approach regarding their team and their space in the future.

2. Focus on Health Equity, Not Just Health Care: This was perhaps the most notable and encouraging change from presentations in past years at J.P. Morgan. I have been going to the conference for over a decade, and I’ve never heard someone mention this term or outline their efforts on “health equity” — this year, nearly everyone did. In the past, they have outlined many wonderful programs on “social determinants of health,” but this year they have seen the disproportionate impact of COVID on low-income communities bringing the ongoing issue of racial disparities in access to care and outcomes to light. As the bedrock of employment in their community, this provides an opportunity to not just provide health care, but also health equity, taking an active role to help make progress on issues like hunger, homelessness, and housing. Many are making significant investments in a number of these and other areas.

3. Take the Lead in Public Health — the Message is the Medicine:One of the greatest failings of COVID, perhaps the greatest lesson learned, is the need for clear and consistent messaging from a public health perspective. That is a role that healthcare providers can and should play. In the pandemic, it represented the greatest opportunity to save lives as the essence of public health is communication — the message is the medicine. A number of health systems stepped into this opportunity to build trust and to build their brand, which are essentially one in the same. Some organizations have created a new role — a Chief Community Health Officer — which is a good way to capture the work that is in motion relative to social determinants of health as well as health equity. Many understand the opportunity here and will take the lead relative to vaccine distribution as clear messaging to build confidence is clearly needed.

4. Make the Home and Everywhere a Venue of Care:A number of presenters stated that “COVID didn’t change our strategy, it accelerated it.” For the most part, they were referring to virtual visits, which increased dramatically now representing around 10 percent of their visits vs. 1 percent before-COVID. One presenter said, “Digital has been tested and perfected during COVID,” but that is only considering the role we see digital playing in this moment. It is clear some organizations have a very narrow tactical lens while others are looking at the opportunity much more strategically. For many, they are looking at a “care anywhere and everywhere” strategy. From a full “hospital in the home” approach to remote monitoring devices, it is clear that your home will be seen as a venue of care and an access point moving forward. The pandemic of 2020 may have sparked a new era of “post-hospital healthcare” — stay tuned.

5. Bury Your Budget and Pivot to Planning:The budget process has been a source of incredible distrust, dissatisfaction and distraction for every health system for decades. The chaos and uncertainty of the pandemic forced every organization to bury their budget last year. With that said, many of the organizations that presented are now making a permanent shift away from a “budget-based culture” where the focus is on hitting a now irrelevant target set that was set six to nine months ago to a “performance-based culture” where the focus is on making progress every day, week, month and quarter. Given that the traditional annual operating budget process has been the core of how health systems have operated, this shift to a rolling forecast and a more dynamic planning process is likely the single most substantial and permanent change in how hospitals and health systems operate due to COVID. In other words, it is arguably a much bigger headline than what’s happened with virtual visits.

6. Get Your M&A Machine in Motion: It was clear from the presentations that activity around acquisitions is going to return, perhaps significantly. These organizations have strong balance sheets and while the strong have gotten stronger during COVID, the weak have in many cases gotten weaker. Many are going to be opportunistic to acquire hospitals, but at the same time they have concluded that they can’t just be a system of care delivery. They are also focused on acquiring and investing in other types of entities as well as forming more robust partnerships to create new revenue streams. Organizations that already had diversified revenue streams in place came through this pandemic the best. Most hospitals are overly reliant on the ED and surgical volume. Trying to drive that volume in a value-based world, with the end of site of service differentials and the inpatient only list, will be an even bigger challenge in the future as new niche players enter the market. As I wrote in the headline of my summary two years ago, “It’s the platform, stupid.” There are better ways to create a financial path forward that involve leveraging their assets — their platform — in new and creative ways.

7. Hey, You, Get into the Cloud:With apologies for wrapping a Rolling Stones song into a conference summary, one of the main things touted during presentations was “the cloud” and their ability to pull clinical, operational and financial dashboards together to monitor the impact of COVID on their organization and organize their actions. Focus over the last decade has been on the clinical (implementing EHRs), but it is now shifting to “digitizing operations” with a focus on finance and operations (planning, cost accounting, ERPs, etc.) as well as advanced analytics and data science capabilities to automate, gather insight, manage and predict. It is clear that the cloud has moved from a curiosity to a necessity for health systems, making this one of the biggest areas of investment for every health system over the next decade.

8. Make Price Transparency a Key Differentiator: One of the great lessons from Amazon (and others) is that you can make a lot of money when you make something easy to buy. While many health systems are skeptical of the value of the price transparency requirements, those that have a deep understanding of both their true cost of care and margins are using this as an opportunity to prove their value and accelerate their strategy to become consumer-centric. While there is certainly a level of risk, no business has ever been unsuccessful because they made their product easier to understand and access. Because healthcare is so opaque, there is an opening for healthcare providers to build trust, which is their main asset, and volume, which is their main source of revenue, by becoming stunningly easy to do business with. This may be tough sledding for some as this isn’t something healthcare providers are known for. To understand this, spend a few minutes on Tesla’s website vs. Ford’s. The concept of making something easy, or hard, to buy will become crystal clear as fast as a battery-driven car can go from zero to 60.

9. Make Care More Affordable:This represents the biggest challenge for hospitals and health systems as they ultimately need to be on the right side of this issue or the trust that they have will disappear and they will remain very vulnerable to outside players. All are investing in advanced cost accounting systems (time-driven costing, physician costing, supply, and drug costing) to truly understand their cost and use that as a basis to price more strategically in the market. Some are dropping prices for shoppable services and using loss leader strategies to build their brand. The incoming Secretary of Health and Human Services has a strong belief regarding the accountability of health systems to be consumer centric. The health systems that understand this are working to get ahead of this issue as it is likely one of their most significant threats (or opportunities) over the next decade. This means getting all care to the right site of care, evaluating every opportunity to improve, and getting serious about eliminating the need for expensive care through building healthy communities. If you’re worried about Wal-Mart or Amazon, this is your secret weapon to keep them on the sideline.

10. Scale = Survival: One of the big lessons here is that the strong got stronger, the weak got weaker. For the strong, many have been able to “snapback” in financial performance because they were resilient. They were able to designate COVID-only facilities, while keeping others running at a higher capacity. To be clear, while most health systems are going to get to the other side and are positioned better than ever, there are many others that will continue to struggle for years to come. According to our data at Strata, we see 25 percent operating at negative margins right now and another 50 percent just above breakeven. They key to survival moving forward, for those that don’t have a captive market, will be scale. If this pandemic proved one thing relative to the future of health systems it is this — scale equals survival.

When Will We Return to Normal?

Based on what the projections that these health systems shared, the “new normal” for health systems for the first half of 2021 will be roughly 95 percent of prior year inpatient volume with a 20 percent year-over-year drop in ED volume and a drop of 10-15 percent in observation visits. So, the pain will continue, but given the adjustments that were already made in 2020, it looks like they will be able to manage through COVID effectively. While there will be a pickup in the second half of 2021, the safe bet is that a “return to normal” pre-COVID volumes likely won’t occur until 2022. And there are some who believe that some of the volume should have never been there to begin with and we might see a permanent shift downward in ED volume as well as in some other areas.

With that said, I’ll steal a quote from Bert Zimmerli, the CFO of Intermountain Healthcare, who said, “Normal wasn’t ever nearly good enough in healthcare.”In that spirit, the goal should be to not return to normal, but rather to use this moment as an opportunity to take the positive changes driven by COVID — from technology to processes to areas of focus to a sense of responsibility — and make them permanent.

Thanking Our “Healthcare Heroes”

We’ll never see another 2020 again, hopefully. With that said, one of the silver linings of the year is everything we learned in healthcare. The most important lesson was this — in healthcare there are literally heroes everywhere. To each of them, I just want to say “thank you” for being there for us when we needed you the most. We should all be writing love letters to those on the front line who risked their lives to save others. Our nation’s healthcare system has taken a lot of criticism through the years from those on the outside, often with a blind eye to how things work in practice vs. in concept. But this year we all got to see first-hand what’s happening inside of healthcare — the heroic work of our healthcare providers and those who support them.

They faced the worst crisis in the history of healthcare. They responded heroically and were there for our families and friends.

They proved that healthcare is too vital to fail. They proved that healthcare is pandemic-proof.

/the-us-federal-trade-commission--ftc--bu-71968930-e5e36febe53543aaa53329c6c17fc982.jpg)