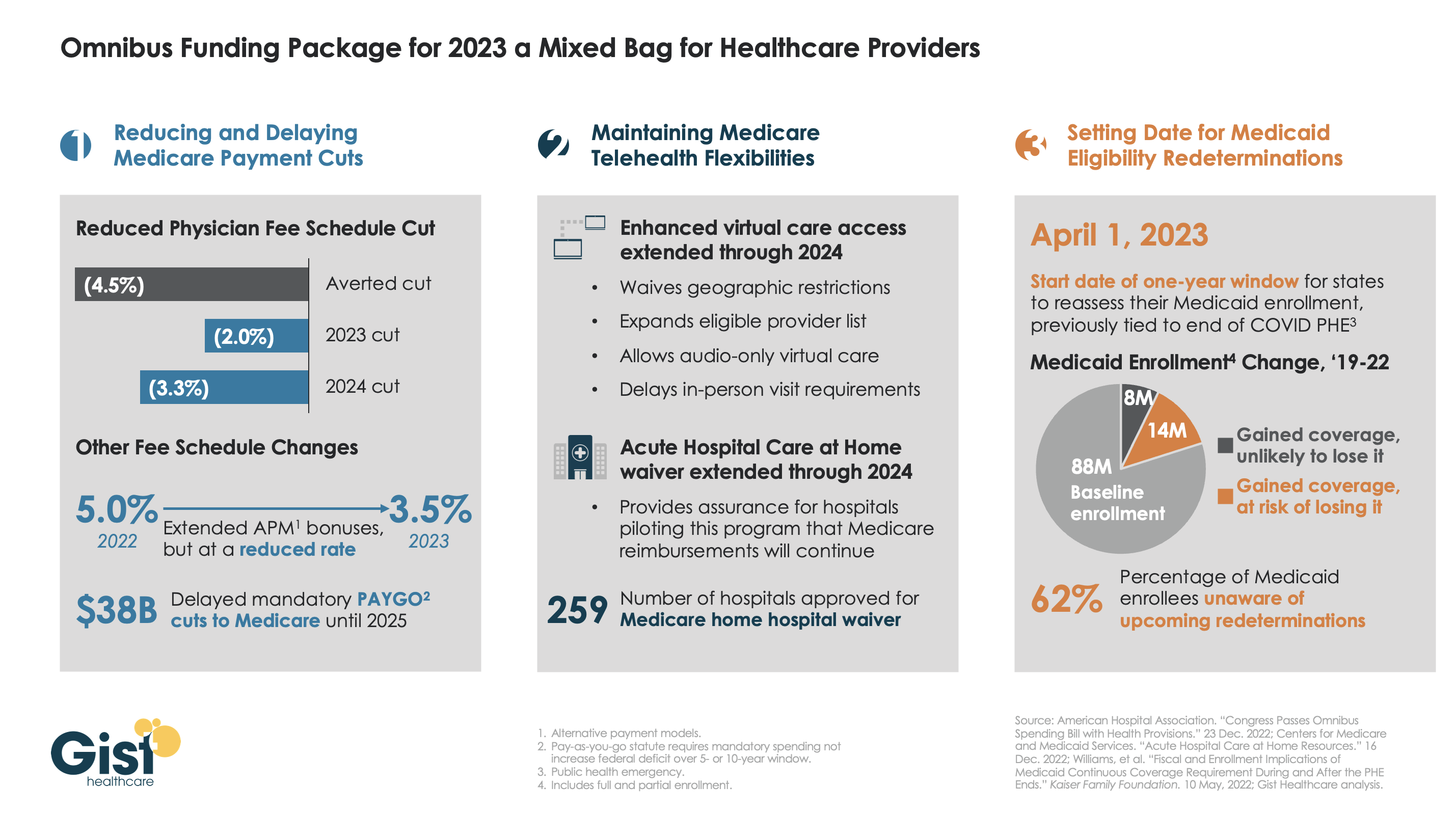

Late last week, President Biden signed a $1.7T spending package to fund the federal government through next September. While around half the funds are dedicated to defense, some important healthcare items made it into the bill, including a reduction in planned Medicare physician pay cuts and a two-year postponement of the $38B Medicare spending cut required by the PAYGO sequester.

The law also decoupled several measures from the end of the federal COVID public health emergency (PHE), setting April 1st as the start date for states to begin Medicaid eligibility redeterminations, and extending Medicare’s telehealth flexibilities and the Acute Hospital Care at Home waiver program through the end of 2024. For more details on these changes, see our graphic below.

The Gist: Medical groups were hoping for more of a reprieve from the Medicare physician fee schedule cuts, but Congress proved unwilling to address concerns over rising practice costs. We’re relieved that Medicare’s new telehealth and hospital at home policies will continue beyond the PHE, given the early interest we’ve seen from the provider community in embracing these new, more consumer-friendly care models.

Once the new Congress finally gets underway, we’re expecting this to be an uneventful two years for federal healthcare legislation, with the emphasis of health policy likely to shift toward states, federal agency rulemaking, and judicial activity.

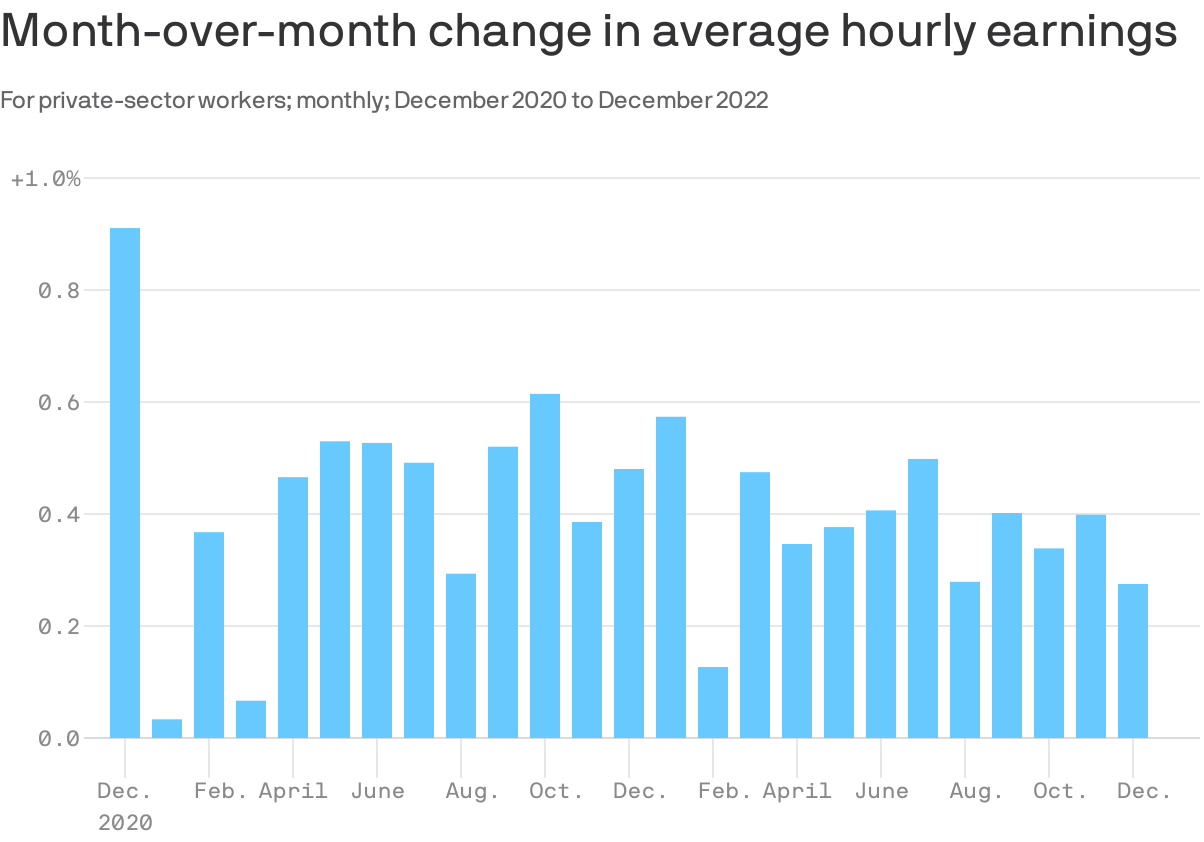

The Goldilocks nature of these jobs numbers is particularly apparent in the wage data.

By the numbers: Average hourly earnings rose by 0.3% in December, and are up 4.6% over the last year. Over the last three months, worker pay rose at a 4.1% annual rate.

Wages are rising, but unlike a year ago, the pace is consistent with the economy settling into the 2% inflation that the Fed seeks.

For example, there were stretches in 2018 and 2019 that featured wage growth similar to that in Q4 paired with low inflation levels — which meant rising real wages for workers.

In other words, current pay growth, if sustained, would help diminish the Fed’s fears of an upward spiral of wages and prices. Also, it sets workers up to see gains in their real compensation, if and when inflation comes down.

The intrigue: It appears that a surge in earnings initially reported in November was a head fake. The Labor Department revised those numbers to show a 0.4% rise in hourly earnings, not the 0.6% first reported.

The original figures had been a source of alarm among Fed watchers, suggesting the central bank might need to step up its monetary tightening campaign.

It is a good reminder — for both policymakers and those of us in the media — to not overreact to single-month shifts in any volatile data series.

We really liked what we saw in the December jobs report, which made us more optimistic about the possibility the 2023 economy will hold up reasonably well. More details below.

Situational awareness: In less optimistic news, the Institute for Supply Management’s survey of service industry activity plunged in December, to 49.6% — down from 56.5% in November. This is the first time the index has been in negative territory since May 2020.

The U.S. labor market is extraordinarily strong, despite gloom-and-doom economic forecasts and high-profile layoffs.

That is the takeaway from December numbers, out this morning, that were outstanding in subtle and not-so-subtle ways.

Why it matters: If America’s economy is going to come in for a soft-landing — inflation dissipating without mass unemployment — you would expect to see numbers that look a lot like last month’s.

The economy continues to add a healthy number of new jobs, though the pace is moderating. Wages are rising, but not so quickly as to alarm economic policymakers. And more workers are entering the labor force, which — if sustained — could heal labor shortages.

The data has positive developments both for American workers — who continue to have abundant job opportunities — and for Fed officials seeking evidence that their inflation-fighting efforts are starting to cool job creation and wage growth to more sustainable rates.

The headline unemployment rate, at 3.5%, matched its lowest levels in decades. If you extend the calculation out a couple more decimal places, University of Michigan economist Justin Wolfers points out, it was 3.468%, the lowest since 1969!

It fell even as the labor force expanded by 439,000 workers, a welcome development on the supply front after months of little progress. More Americans working means fewer of the labor shortages that have contributed to inflation.

An additional 717,000 Americans reported being employed, helping resolve what had been a puzzling disconnect between different sources of labor market data — and in a positive direction.

A stunningly low jobless rate might raise some alarm bells at the Fed over the possibility the job market is too tight, and that this could fuel inflation. But the labor force growth and benign wage data (more on that below) may take the edge off those fears.

By the numbers: Employers are still hiring at a rapid pace — 223,000 in December — but slowing from early last year’s unsustainable numbers.

The economy has added roughly 247,000 jobs per month on average in the last three months, slower than the 366,000 in the prior three-month stretch, and less than half of the 539,000 jobs added each month in Q1 2022.

Evidence of tech layoffs did show up somewhat in the report, with the information sector shedding 5,000 jobs. Temporary help services employment fell by 35,000, the clearest sign employers are paring back demand for workers.

But most other sectors, including leisure and hospitality, construction and health care, continued to add jobs.

The bottom line: If we keep getting numbers like these, 2023 may not be such a rough year for workers after all.

It covers 589,901 healthcare workers and 166,087 registered nurses from 272 facilities and 32 states. Participants were asked to report data on turnover, retention, vacancy rates, recruitment metrics and staffing strategies from January to December 2021.

The survey found a wide range of helpful figures for understanding the financial fallout of one of healthcare’s hardest labor disruptions:

The average hospital lost $7.1 million in 2021 to higher turnover rates.

The average hospital loses $5.2 to $9 million on RN turnover yearly.

The average turnover cost for a staff RN is $46,100, up more than 15 percent from the 2020 average.

The average hospital can save $262,300 per year for each percentage point it drops from its RN turnover rate.

To improve margins, hospitals need to control labor costs by decreasing dependence on travel and agency staff, but only 22.7 percent anticipate being able to do so.

For every 20 travel RNs eliminated, a hospital can save $4.2 million on average.

In the past 5 years, the average hospital turned over 100.5 percent of its workforce:

In 2021, hospitals set a goal of reducing turnover by 4.8 percent. Instead, it increased 6.4 percent and ranged from 5.1 percent to 40.8 percent. The current average hospital turnover rate nationally is 25.9 percent, according to the report.

While 72.6 percent of hospitals have a formal nurse retention strategy, less than half of those (44.5 percent) have a measurable goal.

Overall, 55.5 percent of hospitals do not have a measurable nurse retention goal.

Retirement is the number four reason staff RNs leave, and it is expected to remain a primary driver through 2030. More than half (52.8 percent) of hospitals today have a strategy to retain senior nurses. In 2018, only 21.6 percent had one.

Historically, RN turnover has trended below the hospital average across all staff. For the first time since conducting the survey, this is no longer true:

In the past five years, the average hospital turned over 95.7 percent of its RN workforce.

Close to a third (31.0 percent) of all newly hired RNs left within a year, with first year turnover accounting for 27.7 percent of all RN separations. Given the projected surge in retirements, expect to see the more tenured groups edge up creating an inverted bell curve.

Operating room RNs continue to be the toughest to recruit, while labor and delivery RNs are trending easier to recruit than in the year prior.

Hospitals are experiencing a dramatically higher RN vacancy rate (17 percent) compared to last year’s rate of 9.9 percent.

The vast majority (81.3 percent) reported a vacancy rate higher than 10 percent.

Healthcare leaders now need to strike a delicate balance that requires managing financial and growth metrics, increasing the speed of transformation, and building the health systems of tomorrow. So how do we redefine compensation models to reward all these behaviors?

Executive compensation might not spring to mind as a key driver of healthcare transformation, nor does it seem naturally connected to critical issues such as health equity, patient safety, or quality of care – just a few of the areas where significant changes can be made to transform healthcare. But, in fact, executives leading not-for-profit health systems today are tasked with delivering measurable results that improve the health status of their patients and their communities. And to ensure that these new performance metrics are met, we must change how we think about —and deliver—compensation.

Defining a new model

While executive compensation has always been tied to specific objectives, they have historically leaned heavily toward financial performance, volume and margins, with a modest portion of compensation aligned to quality of care and patient outcomes. But transformative approaches such as population health, value-based care, patient wellness and health outcomes are shifting the mark.

Healthcare leaders now need to strike a delicate balance that requires managing financial and growth metrics, increasing the speed of transformation, and building the health systems of tomorrow. So how do we redefine compensation models to reward all these behaviors?

Some might say that the answer lies in adjusting incentive plans. While incentive plans across health care have not changed significantly in the past decade, the sophistication of the plans has changed, reflecting greater attention to delivering a better patient experience. But delivering better experiences does not imply that health systems have transformed from the top down. In my mind, adjusting incentive plans only solves part of the problem.

If we want true health care transformation—and we should, in order to best serve patients and communities—health systems need to re-evaluate the outcomes for each stakeholder and create incentives to evolve leadership as a whole. We need to rethink executive compensation models to align with value-based care, patient experience, and the resulting outcomes, along with traditional performance measurements.

Leading through lingering disruption

But rethinking executive compensation models won’t be an easy task, especially given the external challenges and changes thrust upon the health care system over the last few years.

As with nearly every other aspect of health care, pay for performance was disrupted during the pandemic. Demand for health services changed dramatically, labor and attrition issues intensified, and supply chain problems and operational costs increased. These new pressures required executives to manage through long periods of uncertainty where meeting operational pay-for-performance goals was nearly impossible. Fast-forward to today, the executive talent market remains extraordinarily competitive. Demand outpaces supply due to higher-than-typical retirements, effects of the great resignation, the need for new skill sets and overall burnout.

As a result, there has been upward pressure on compensation to address and fulfill unexpected but immediate needs such as rewarding executives for managing in a unique and challenging performance environment, increasing efforts to recruit and retain, and recognizing leaders for their hard-won accomplishments.

Considerations and changes

When considering adjusting models for 2023 and beyond, CEOs and compensation committees need to take these pressures and disruptions into account. They should look closely at their own compensation data from the past two years – not as a lighthouse for future compensation, but as data that may need to be set aside due to the volume of performance goals and achievements that were up-ended by the pandemic. When relying on external industry data, the same rules apply; smaller data sets or those that don’t account for the past two years may be misleading, so review carefully before using limited data sets to inform adjusted models.

Just as important, CEOs and compensation committees should consider new performance measurements tied to both financial and quality or value-based transformation metrics. We don’t need to eliminate traditional financial and operational goals because viability is still a business mandate. But how can we articulate compensation-driven KPIs for stewardship of patient and community health, improved outcomes and reduced cost of care? Too many measures are akin to having no measures at all.

The compensation mix should take into account a more focused approach to long-term measures. The old paradigm of 12-month incentive cycles is not enough to address the time required to truly transform health care. Another consideration should be performance-based funding of deferred compensation based on achieving transformation goals, and greater use of retention programs to support the maintenance of a stable executive team during the transformation period. Covid-19 proved how crisis can be an accelerator for change. True transformation should blend the skills gained from crisis management with planful, thoughtful and intentional change.

In addition, some metrics may need to incorporate a discretionary component, considering ongoing disruption within the workforce, supply chain limitations, and energy, equipment and labor cost increases. More organizations are also including health equity, DE&I, and ESG goals in incentive programs to tighten alignment with mission-critical board-mandated goals.

Transformative change

There are four elements that are vital in the journey to transform health care from “heads in beds” to the public-service-oriented organizations that they were meant to be—and can be again. With mounting pressure from patients, communities, and payers to boards and employees, CEOs and compensation committees must become key drivers of change, setting the right goals and incentives from the top down.

Affordability: can patients afford the care they need?

Quality: is the care being delivered of the utmost quality?

Usability: how can we reduce hurdles to undertaking the care plan?

Access: are all community members able to access needed care?

Solving for each of these elements is one of the biggest challenges we face, and as we begin to emerge from the disruption of the pandemic, leaders will be watched closely to ensure that they deliver—and can clearly show the path to delivery.

Ideally, end achievements would include patients spending less to achieve better health; payers controlling costs and reducing risk; providers realizing efficiencies and greater patient satisfaction; and alignment of medical supplier pricing to patient outcomes. And when you zoom out to reveal the bigger picture, all of these pieces come together to achieve healthier populations and lower overall health care costs, while still meeting the financial goals of the organization.

We’re asking a lot of already-overburdened health care executives. Stakeholders must prove that we value leaders with the right mindset and skillset in order to attract executives who can shepherd organizations through the transformation journey. This requires a setting where there is supportive leadership, a compelling mission and opportunity for personal growth and development. It will not be easy, but without rethinking how we design compensation models from the top down, it will be unnecessarily challenging.

We expect 2023 to be a pivotal year for the industry, as the accelerated acceptance of virtual care and demographic trends, such as an aging population, increasing chronic illnesses and healthcare worker shortages, sustain demand for medtech-enabled solutions.

The combination of rapid developments in novel healthcare technology and heightened demand for integrated tech-enabled care has continued to fuel innovation in the medtech industry. At the same time, medtech innovators – whether in digital health, wearables and AI-driven offerings in healthcare, or diagnostics, telemedicine and health IT solutions – continue to face a patchwork of laws, rules and norms across the world. Life sciences and healthcare innovators and regulators are also looking to medtech to increase access to care and health equity. Here are ten global medtech themes we are tracking in the coming year:

Focus on digital tuck-in acquisitions in medtech M&A

Despite continued uncertainty in the overall financial market, medtech M&A activity continued at a steady pace in 2022. This year witnessed a rise in tuck-in acquisitions of smaller companies that can be easily integrated into buyers’ existing infrastructure and product offerings, as opposed to significantly sized takeovers of businesses that aren’t squarely aligned with buyers’ existing businesses lines. Medtech acquirers have been particularly focused on developing their digital capabilities to innovate and reach customers in new ways. As digitization continues to transform the industry, we expect acquirers to continue to prioritize the value of digital and data assets as they evaluate potential targets.

Continued interest by private equity and other financial sponsors

Private equity firms, healthcare-focused funds and other financial sponsors have continued to display a strong appetite for investing in Medtech companies, with top targets in subsectors such as diagnostics and healthcare IT solutions. Later-stage medtech companies in particular are gaining a larger share of venture capital funding, as later-stage investments allow financial sponsors to focus on businesses with higher yields, as well as less time to market and capital reimbursement. Demographic trends, including an aging population and the increasing prevalence of chronic diseases, coupled with healthcare technology advancements have created robust demand for medtech-enabled solutions. Additionally, medtech offerings have broad applications that can extend beyond stakeholders in a specific therapy area, product category or care setting, offering the ability to satisfy unmet needs with large patient bases.

Strategic medtech collaborations as the new norm

Strategic medtech collaborations and partnerships have become the new norm in our increasingly connected digital healthcare ecosystem. In response to heightened consumer demand for tech-enabled care, pharmaceutical and medtech companies are collaborating to use digital technologies to engage with consumers, unlocking a vast range of treatments such as personalized medicine. Additionally, as the market rapidly evolves towards data-driven healthcare, we expect medtech companies to continue to work collaboratively to address existing barriers to data sharing and promote interoperability of healthcare data.

Continued scrutiny by antitrust and competition authorities

As expected, global antitrust and competition authorities continued to focus on the tech, life sciences and medtech sectors in 2022. The US, UK and EU authorities have stepped up efforts to investigate and challenge conduct by large pharma and technology companies pursuing mergers and acquisitions. We expect these authorities to assess similar concerns in the digital health context in an effort to account for the value of combined datasets and the interoperability of various offerings that could be derived from digital health mergers and acquisitions. Furthermore, geopolitical tensions have resulted in new and expanded foreign investment regimes to improve the resilience of domestic healthcare systems. Notably this year, the UK government implemented the National Security and Investment Act that allows it to restrict transactions that may threaten national security, including in the AI and data infrastructure sectors. Sensitive data continues to be a recurring theme for foreign investment review for Committee on Foreign Investment in the US and that of the EU as well.

Growing importance of data privacy and security

Increasing regulatory attention to sensitive health data and the escalating rise of ransomware attacks has made data privacy and security more important than ever for medtech innovators. The Federal Trade Commission has issued several statements about its willingness to “fully” enforce the law against the illegal use and sharing of highly sensitive data. Additionally, several state privacy laws coming into effect in 2023 create new categories of sensitive personal data, including health data, and impose novel obligations on innovators to obtain data-related consents. As ransomware continues to pose security-related threats, the US Department of Health and Human Services renewed calls for all covered entities and business associates to prioritize cybersecurity. New standards, such as cybersecurity label rating programs for connected devices, aim to address security risks. In the EU, medtech providers will need to consider how the launch of the European Health Data Space and newly proposed data regulation, such as the Data Act and AI Act, could impact their data use and sharing practices.

More active engagement with FDA/EMA/MHRA

We expect companies active in the medtech sector, particularly those that make use of AI and other advanced technologies, to continue their conversations with the U.S. Food and Drug Administration (“FDA”), the European Medicines Agency (“EMA”), the Medicines and Healthcare Products Regulatory Agency (“MHRA”) and other regulators as such companies grow their medtech business lines and establish their associated regulatory compliance infrastructure. Given the unique regulatory issues arising from the implementation of digital health technologies, we expect the FDA, EMA and MHRA to provide additional guidance on AI/ML-based software-as-a-medical device and the remote management of clinical trials. 2022 saw stakeholders in the life sciences and medtech industries collaborate with regulatory authorities to push forward the acceptance of digital endpoints that rely on sensor-generated data collected outside of a clinical setting. As the industry shifts to decentralized clinical trials, we expect both innovators and regulators to work together to evaluate the associated clinical, privacy and safety risks in the development and use of such digital endpoints.

Increasing medtech localization in the Asia Pacific region

2022 saw multinational companies (“MNCs”), including American pharma/device makers make an active effort to expand their medtech business lines in the Asia Pacific region. At the same time, government authorities in the region have been increasingly focused on incentivizing local innovation, approving government grants and prohibiting the importation of non-approved medical equipment. In light of MNCs’ market share of the medical device market in the Asia Pacific region, especially in China, we expect the emergence of the domestic medtech industry to prompt discussions among MNCs, local innovators and government authorities over the long-term development of the global market for medical technology.

Long-term adoption of telehealth and remote patient monitoring technologies

The Covid-19 pandemic saw the rise of telehealth and remote patient monitoring technologies as key modes of healthcare delivery. The telehealth industry remains focused on enabling remote consultations and long-term patient management for patients with chronic conditions. Looking forward, we expect to see increased innovation in non-invasive technologies that can provide early diagnostics and ongoing disease management in a low-friction manner. At the same time, we anticipate telehealth companies to face increasing scrutiny from regulatory authorities around the world for fraud and abuse by patients and providers. Consumer and patient data privacy and security in connection with telehealth and remote patient monitoring continue to remain top of mind for regulators as well.

Women’s health and privacy concerns for medtech

We expect to see increased consumer health tech adoption for reproductive care, especially in light of the U.S. Supreme Court’s decision to overturn Roe v. Wade. Following the Dobbs decision, a number of states introduced or passed legislation that prohibits or restricts access to reproductive health services beyond abortion. In response, women’s health-focused companies are expanding their virtual fertility and pregnancy, telemedicine and other services to patients. At the same time, such companies need to assess the legal risks stemming from the collection and storage of their customers’ personal health information, which could then be used as evidence to prosecute customers for obtaining illegal reproductive health services. We expect companies active in this space to take steps to navigate the patchwork of data privacy and security laws across jurisdictions while establishing clear digital health governance mechanisms to safeguard their customers’ data privacy and security.

Addressing inequities in the implementation of digital healthcare technologies

Medtech innovators and regulators have been increasingly focused on addressing inequities in the healthcare system and the data used to train AI and ML-based digital healthcare technologies. In 2022, a number of medtech companies collaborated to provide technologies that result in improved patient outcomes across all populations, as well as boost participation of diverse populations in clinical trials. In parallel, we are seeing increased interest from regulators to reduce bias in digital health technologies and the accompanying datasets, as evidenced by the EU’s proposed AI Act and the UK’s health data strategy. In the US, which currently lacks comprehensive government regulation of AI in healthcare, there have been increasing calls for institutional commitments in the area of algorithmovigilance. Because of the inaccurate conclusions that may result from biased technologies and data, MedTech companies must prioritize health equity in the implementation of digital healthcare technologies so that everyone can benefit from the latest scientific advances.

In conclusion, the medtech industry has remained resilient amidst the challenging macroeconomic environment. We expect 2023 to be a pivotal year for the industry, as the accelerated acceptance of virtual care and demographic trends, such as an aging population, increasing chronic illnesses and healthcare worker shortages, sustain demand for medtech-enabled solutions. At the same time, the rapidly changing legal and regulatory landscape will continue to be a key issue for medtech innovators moving forward. Adopting a global, forward-thinking regulatory compliance strategy can help MedTech companies stay competitive and ultimately, achieve better outcomes for patients.

Financial analysts have said that 2022 may have been the worst year for hospital finances in decades. This year looks like it will be yet another year of financial underperformance, with rural providers in especially dire circumstances.

What’s driving this bleak financial reality? It’s “primarily an expense story,” said Erik Swanson, a senior vice president at Kaufman Hall‘s data analytics practice.

“Growth in expenses has vastly outpaced growth in revenues — since pre-pandemic levels since last year, and even the year prior — such that margins are ultimately being pushed downward. And hospitals’ median operating margin is still below zero on a cumulative basis,” he declared, referring to 2021 and 2020.

Here’s some context about how dismal this situation is: Even in 2020, a year in which hospitals saw extraordinary losses during the first few months of the pandemic, they still reported operating margins of 2%.

What’s even more disconcerting is that hospitals are underperforming financially pretty much across the board, Swanson said.

Even Kaiser Permanente, one of the country’s largest health systems with an integrated delivery model, reported a $1.5 billion loss for the third quarter of 2022.

Rural hospitals are in even worse shape, but more on that below.

Other hospitals have been forced to shutter service lines to offset these financial losses. Some are also turning to integration and consolidation.

For example, Hermann Area District Hospital in Missouri said last month that it is seeking a “deeper affiliation” with Mercy Health or another provider. This announcement came after the hospital eliminated its home health agency as a cost-cutting measure. In December, the hospital projected a loss of $2 million for 2022.

We can also look at the mega-merger between Atrium Health and Advocate Aurora Health, which was completed last month. The deal, which is designed for cost synergy, creates the fifth-largest nonprofit integrated health system in the U.S.

The merger was finalized one day after North Carolina Attorney General Josh Stein expressed concern about how the deal could impact rural communities. He said that while he didn’t have a legal basis within his office’s limited statutory authority to block the deal, he was worried that it could further restrict access to healthcare in rural and underserved communities.

Stein brings up an extremely valid concern. Rural hospitals’ dismal financial circumstances are becoming more and more worrisome — in fact, about 30% of all rural hospitals are at risk of closing in the near future, according to a recent report from the Center for Healthcare Quality and Payment Reform (CHQPR).

A crucial reason for this is that it is more expensive to deliver healthcare in rural areas — usually because of smaller patient volumes and higher costs for attracting staff. Another factor is that payments rural hospitals receive from commercial health plans isn’t enough to cover the cost of delivering care to patients in rural areas, said Harold Miller, CEO of CHQPR.

“Many people assume that private commercial insurance plans pay more than Medicare and Medicaid. But for small rural hospitals, the exact opposite is true,” he said. “In many cases, Medicare is their best payer. And private health plans actually pay them well below their costs — well below what they pay their larger hospitals. One of the biggest drivers of rural hospital losses is the payments they receive from private health plans.”

In Miller’s view, rural hospitals perform two main functions: taking care of sick people in the hospital and being there for people in case they need to go to the hospital.

To fulfill the latter job, rural hospitals must operate 24/7 emergency rooms. These hospitals get paid when there’s an emergency, but not when there isn’t — even though the hospital is incurring costs by operating and staffing these units.

“Rural hospitals have a physician on duty 24/7 to be available for emergencies. But they don’t get paid for that by most payers. Medicare does pay them for that, but other payers don’t. If the hospital is doing two different things, we should be paying them for both of those things. Hospitals should be paid for what I refer to as ‘standby capacity,’” Miller said.

He bolstered his argument by pointing to these analogies: Do we only pay firefighters when there’s a fire? Do we only pay police officers when there’s a crime?

It’s also important to remember that rural hospitals are in the midst of transitioning to a post-pandemic environment, now without the pandemic-era financial assistance they received from the government, said Brock Slabach, chief operations officer at the National Rural Health Association.

“Rural providers are looking to move into the future without the benefit of those extra payments. And they’re in an environment of really high inflation. It’s over 8%, and for some goods and services in the healthcare sector, that’s going to be over 20% in terms of increased prices. Wages and salaries have also gone up significantly. But patient volumes have maintained below average or average. That all presents a huge challenge,” Slabach said.

Rural providers across the country are dealing with the stressors Slabach described and clamoring for more government help. For example, the Michigan Health & Hospital Association sought more money from the state last month after having to take 1,700 beds offline.

Many rural hospitals can’t escape their fate. From 2010 to 2021, there were 136 rural hospital closures. There were only two closures in 2021, and Slabach said 2022 produced a similarly low number. But these low totals are due to government relief, he explained. Slabach said he’s expecting an increase in rural hospital closures in 2023.

When a rural hospital closes, it means community members have to travel far distances for emergency or inpatient care. Miller pointed out another problem: in many rural communities, the hospital is the only place people can go to get laboratory or imaging work done. The hospital might also be the only source of primary care for the community. Shuttering these hospitals would be a massive blow to rural Americans’ healthcare access.

In the face of these potentially devastating blows to patient access, financial analysts’ outlook is bleak.

Higher inflation and costly labor expenses will continue to have negative effects on hospitals — both rural and urban — in 2023, according to an analysis from Moody’s. Expenses will also continue to increase due to supply chain bottlenecks, the need for more robust cybersecurity investments and longer hospital stays due to higher levels of patient acuity.

All of this doom and gloom begs the question — are any hospitals doing well financially?

The answer is yes, a select few. Let’s look at the three largest for-profit health systems in the nation — Community Health Systems, HCA Healthcare and Tenet Healthcare. As of 2020, these three public health systems accounted for about 8% of hospital beds in the U.S.

These three systems all had positive operating margins for the majority of the pandemic, including most recently in the third quarter of 2022.

Large public health systems have shareholders to report to and stock prices to worry about. Does this mean they’re more likely to deny care to patients who can’t afford it while other hospitals pick up the slack?

Slabach said it’s tough to say.

“Obviously, hospitals try to mitigate their exposure to risk when it comes to taking care of patients. Most hospitals do a really good job of providing services and care to people who don’t have insurance or don’t have the means to pay. But that gets stressed in this current financial environment. So indeed, there may be instances where what you suggested might happen, but it’s not because they want to deny services or deny care. It’s because they have a bigger picture they have to maintain,” Slabach said.

And the big picture involving dollar signs for hospitals looks pretty bleak in 2023.