On March 8, 2023, Silicon Valley Bank (SVB) announced a $1.8 billion loss from the sale of securities to cover a decline in clients’ deposits. The following day, SVB’s stock dropped 60% and the bank saw a historic $42 billion in withdrawal requests. Twenty-four hours later, SVB was under the control of U.S. banking regulators and concern turned into panic across the banking sector.

More recently, the cyberattack on Change Healthcare raised the issue of counterparty risk in a different sector. Provider organizations—especially those that had become predominantly reliant on Change Healthcare for health plan payment processing—experienced serious cash flow issues.

Both the SVB and Change Healthcare incidents brought to the fore significant new risks that were at least in part driven by rapidly evolving technological change. An April 28, 2023, report by the Federal Reserve responding to SVB’s collapse noted how “social media enabled depositors to instantly spread concern about a bank run, and technology enabled immediate withdrawals of funding.” The Change Healthcare cyberattack was the most dramatic example to date of a problem that is growing quickly across the healthcare industry, as cyber criminals seek access to data-rich health records.U.S. Department of Health & Human Services data shows a 93% increase in large data breaches the healthcare sector from 2018 to 2022 and a 278% increase in large data breaches involving ransomware over the same period.

Lessons learned over the past year

The SVB collapse and Change Healthcare cyberattack have taught several important lessons:

The risk of contagion is real. The problems of one organization can quickly spread across an entire sector. In the case of SVB, instability and uncertainty led to a flight to safety, as both corporate clients and consumers shifted their deposits into what the Federal Reserve describes as “systemically important institutions,” leaving regional banks scrambling to reassure clients of their financial health.

Not all risks can be anticipated. The Federal Reserve report on the SVB collapse notes that “as risks continue to evolve, we need to…be humble about our ability to assess and identify new and emerging risks.”

Solutions take time to implement. Major relationships with a bank, a payment processing platform, or any other significant counterparty can not be shifted overnight. It can take weeks—or even months—to identify a new partner and implement the processes and technologies needed to transfer data and funds. Existing clients of the new partner can experience impacts as well if a major in-flow of new clients strains the partner’s ability to service its accounts.

Risk diversification must be a priority. These events are generating a “hyper focus” by boards, C-suite executives, and finance and treasury professionals to diversify risk within their major counterparty relationships and create formal counterparty risk policies.

Not all risks can be fully mitigated. Having a balance sheet that can weather the storm if a risk materializes is of paramount importance. Measuring and monitoring counterparty risk should be part of a broader, systematic approach that balances risks and resources across the organization.

Measuring counterparty risk

While one of the lessons learned is that not all risks can be anticipated, there are focus areas specific to different sectors that, even within a rapidly changing macroeconomic environment, will help provide a fuller view of risk. Using the banking sector as an example, key focus areas include:

Market risk outlook. This outlook combines debt ratings and long- and short-term counterparty risk metrics, along with an understanding of country risks for banks not headquartered in the United States.

Capital and asset resiliency. This focus area evaluates the quality of bank assets and liabilities to measure balance sheet strength throughout the business cycle.

Growth and profitability. Here, the overall performance of the banking partner is measured to understand the systemic importance of the institution and how well it is positioned for long-term growth.

Loan portfolio. This focus area measures the mix of loan exposure, highlighting commitments to various industries and the breakdown between consumer and corporate debt.

Representative metrics for each of these four focus areas are provided in Figure 1.

• Tier 1 Capital (%)• Total Debt to Assets• Coverage Ratio

Growth and Profitability

• Net Income• Market Capitalization• Efficiency Ratio

Loan Portfolio

• Total Loan• Residential Real Estate Loans• Credit Card Loans

Staying focused on the challenges of today and tomorrow

Comprehensively measuring counterparty risk can give early insights into troubled situations that could lead to severe business disruptions. Within the banking sector, the focus for 2023 was on banks effectively managing risk through an elevated rate environment. As we move through 2024, the challenges might look significantly different.

With uncertainty around the path forward for the U.S. economy, mixed signals on bank financial performance, and a highly contested election shaping up for the end of the year, there will continue to be a heightened focus on effectively managing a bank group to ensure business resilience and continuity in times of stress.

Beyond the bank financial worries of the past year, the recent disruptions related to the Change Healthcare cyberattack have brought a new focus to the technological resilience of core services partners. Organizations should be digging deeper into the cybersecurity investments of their key partners and investigating the outside technology that is leveraged by these partners.

In all cases, organizations should be asking how and to what extent they should be diversifying risk in counterparty relationships. Both known and unknown risks will continue to emerge. Managing counterparty risk must be a comprehensive and ongoing exercise to both evaluate and mitigate against that risk.

Counterparty risk, also known as default risk, is the chance that a party in a financial transaction will not fulfill their obligations. This can occur in credit, investment, or trading transactions. For example, in a reinsurance transaction, the reinsurer may not reimburse the insurance company for claims, which could lead to financial shortfall.

Companies grappling with liquidity concerns are looking to cut costs and streamline operations, according to a new survey.

Dive Brief:

Over three-quarters of healthcare chief financial officers expect to see profitability increases in 2024, according to a recent survey from advisory firm BDO USA. However, to become profitable, many organizations say they will have to reduce investments in underperforming service lines, or pursue mergers and acquisitions.

More than 40% of respondents said theywill decrease investments in primary care and behavioral health services in 2024, citing disruptions from retail players. They will shift funds to home care, ambulatory services and telehealth that provide higher returns, according to the report.

Nearly three-quarters of healthcare CFOs plan to pursue some type of M&A deal in the year ahead, despite possible regulatory threats.

Dive Insight:

Though inflationary pressures have eased since the height of the COVID-19 pandemic, healthcare CFOs remain cognizant of managing costs amid liquidity concerns, according to the report.

The firmpolled 100 healthcare CFOs serving hospitals, medical groups, outpatient services, academic centers and home health providers with revenues from $250 million to $3 billion or more in October 2023.

Just over a third of organizations surveyed carried more than 60 days of cash on hand. In comparison, a recent analysis from KFF found that financially strong health systems carried at least 150 days of cash on hand in 2022.

Liquidity is a concern for CFOs given high rates of bond and loan covenant violations over the past year. More than half of organizations violated such agreements in 2023, while 41% are concerned they will in 2024, according to the report.

To remain solvent, 44% of CFOs expect to have more strategic conversations about their economic resiliency in 2024, exploring external partnerships, options for service line adjustments and investments in workforce and technology optimization.

Most organizations are interested in exploring sales, according to the report. Financially struggling organizations are among the most likely to consider deals. Nearly one in three organizations that violated their bond or loan covenants in 2023 are planning a carve-out or divestiture this year. Organizations with less than 30 days of cash on hand are also likely to consider carve-outs.

Organizations will also turn to automation to cut costs. Ninety-eight percent of organizations surveyed had pilotedgenerative AI tools in a bid to alleviate resource and cost constraints, according to the consultancy.

“Healthcare leaders believe AI will be essential to helping clinicians operate at the top of their licenses, focusing their time on patient care and interaction over administrative or repetitive tasks,” authors wrote. Nearly one in three CFOs plan to leverage automation and AI in the next 12 months.

However, CFOs are keeping an eye on the risks. As more data flows through their organizations, they are increasingly concerned about cybersecurity. More than half of executives surveyed said data breaches are a bigger risk in 2024 compared to 2023.

This annual look at high-impact trends affecting healthcare in the coming year is based on evaluation of current industry research data. Healthcare Finance Trendsfor2023 (Trends) explores eight themes identified by CommerceHealthcare® ranging across four areas:

Financial. Providers enter the year contending with multiple financial stress points. They will also seek growth in technology-enabled remote care.

Patient financial experience. The need to drive not only improvement but also personalization of the financial experience is paramount. A central role will be played by patient financing programs which will see growing demand in 2023.

Trust. Building trust with all constituencies is explored as a linchpin for long-term provider success. The latest findings on cybersecurity show that this contributor to trust will continue to consume leadership attention.

Digital transformation. Pursuit of digital-first operations is accelerating, with the finance area an important focus. Emerging payment modes are finding a home in healthcare’s digital finance landscape.

This report’s consistent message is that these trends intersect in ways that compound both the challenges and the upside potential of strategies that address them.

1. Multiple Financial Stress Points Will Constrain Options

Healthcare’s financial predicament for the next 12–18 months is being described in strong terms. Citing $450 billion of EBITDA that could be in jeopardy, more than half of the industry’s project profit pool by 2027, one analyst suggests “a gathering storm.” Another perceives “broad and serious threats” as “elevated expenses” erode margins and exact “a profound financial toll.” Fitch Ratings issued a “deteriorating” outlook for nonprofit health systems.

These financial headwinds are upending healthcare’s traditional status as “recession-proof.” It is helpful to probe the multiple forces in play, the urgent workforce management challenge, and the varied solution set.

Multiple stress factors at work

Observing that margins will be down 37% in 2022 relative to pre-pandemic, a recent stark assessment concluded, “U.S. hospitals are likely to face billions of dollars in losses — which would result in the most difficult year for hospitals and health systems since the beginning of the pandemic.”

A confluence of factors is exacerbating the stress for 2023:

Rising acuity levels. Over two-thirds of surveyed C-suite executives said patient health has worsened from pandemic-induced delayed care. The upshot, stated by 27% of CFOs, is rising expenses due to higher acuity. Inpatient days are projected to increase at an 8% rate over the coming decade.

Reimbursement gaps and inflation. Commercial and government reimbursement rates are not keeping pace with rising costs. Surging inflation is widening this gap. Hospitals are also reporting substantial insurer payment delays and denials.

Investment declines. Stock and bond market declines have removed a cushion for operating weakness. Market uncertainty will complicate 2023 portfolio management.

Persistent workforce concerns remain center stage

Burnout and shortages have disrupted the clinical workforce. Nearly 60% of physician, advanced practice provider and nurse survey respondents said their teams are not adequately staffed, and 40% lack resources to operate at full potential. Many providers face extreme to moderate shortages of allied health professionals.

The problem extends beyond the clinical. A survey saw 48% of respondents experiencing severe labor deficiencies in revenue cycle management (RCM) and billing, and one in four finance leaders must fill over 20 positions to be fully staffed.

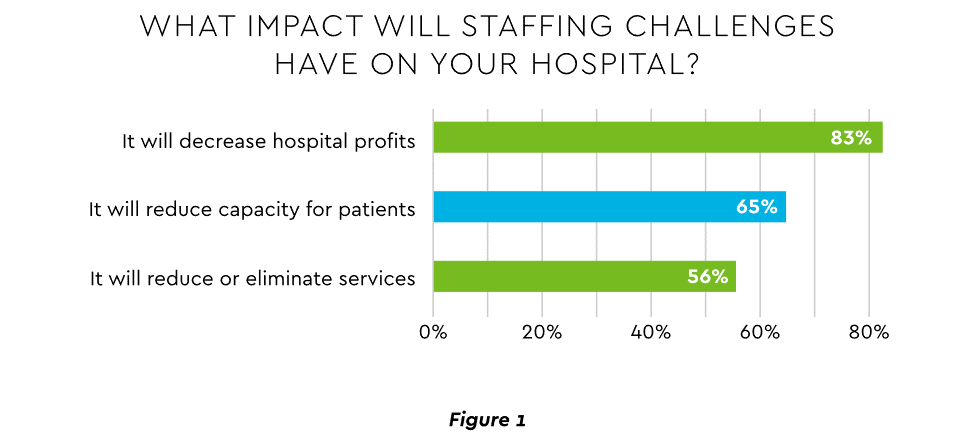

An executive outlook highlighted demonstrable impact on financial performance and growth from these workforce problems, citing reductions in profitability, capacity and service (Figure 1).1

Expenses. Hospital employee expense is expected to increase $57 billion from 2021 to 2022, with contract labor ballooning another $29 billion. Average weekly earnings are up 21.1% since early 2022. Half of medical practices budgeted higher staff cost-of-living increases in 2022. Shortages plague post-acute facilities as well. Their reduced capability to accept discharged patients is lengthening many hospitals’ patient stays.

Capacity constraint. Two-thirds of healthcare leaders identify “ability to meet demand” as their top workforce concern, suggesting a “looming capacity gap between future demand and labor supply.”

Range of measures being deployed

Health systems, hospitals and practices will vigorously pursue at least four direct actions to overcome the financial and staffing hurdles:

Cost cutting. Expense control will be paramount and “hospitals will be forced to take aggressive cost-cutting measures.” McKinsey estimates total industry administrative savings of $1 trillion through multiple aggressive changes.

Service line rationalization. Providers are rethinking how they deliver services to optimize efficiency. One path is utilizing “lower level” healthcare professionals in ways that free RNs and LPAs for more complex work suited to their top skills. Integrating remote care into the mix is another core element of the strategy.

Recruitment and retention programs. Attracting and retaining talent is crucial. Compensation is one avenue. Over two-thirds of organizations are offering signing bonuses for allied health professionals. Some are instituting value-based payments for physicians, offering salary floors to protect from drops in patient volume. CFOs and CNOs are joining forces to invest in nurse retention strategies.

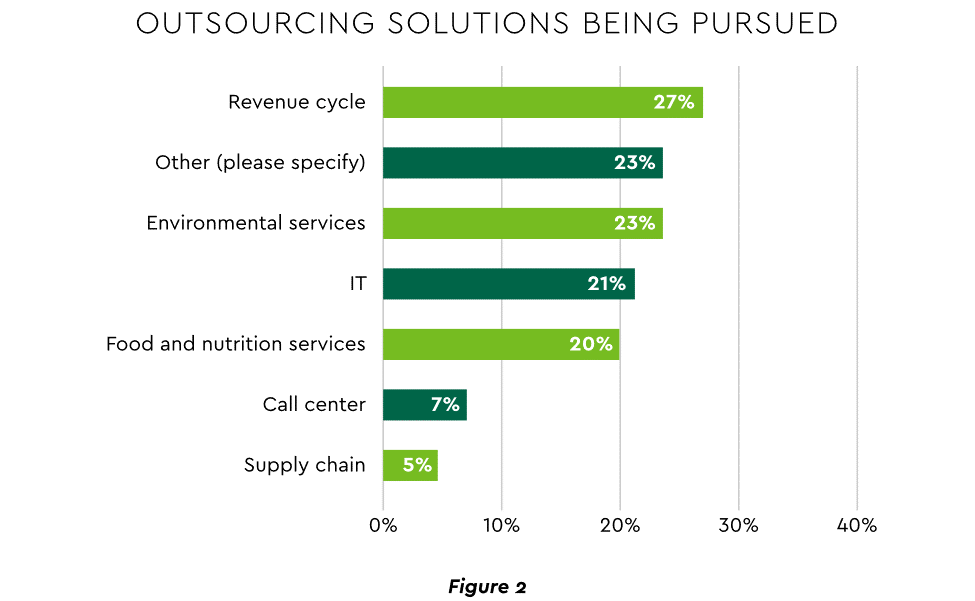

Staffing management. An increasingly popular tool to reduce labor cost and optimize staff resources is outsourcing. Figure 2 shows that RCM is leading the way among those using the solution.

2. Growth Strategies Favor Outpatient, Virtual, Acute Home Care

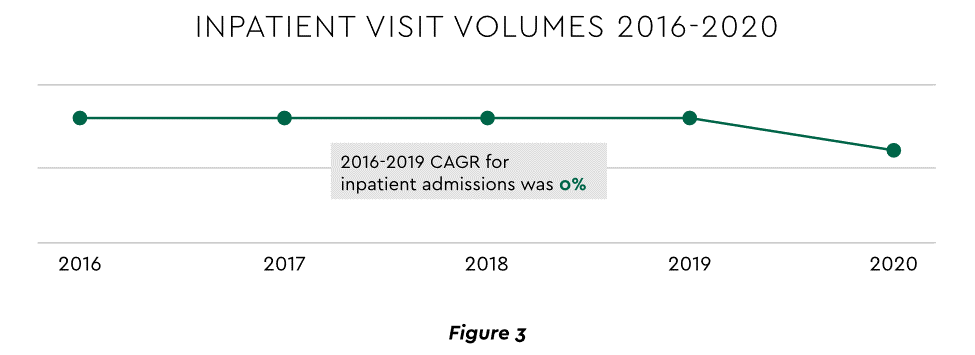

Pursuing top line growth in tandem with reining in expenses is essential. Inpatient volume growth has been tepid for several years ─ essentially flat in the 2016–20 period (Figure 3).

Leaders have been pivoting to outpatient and virtual care to diversify revenue streams. Two high-potential 2023 growth tracks in this sector merit deeper assessment.

Telehealth

Considerable evidence attests to strong commitment to telehealth and remote care. Sixty-three percent of physicians worldwide expect most consultations to be performed remotely within 10 years. Approximately 40% of health centers are using remote patient monitoring today. Consumers are also positive: 94% definitely or probably will use telehealth again, 57% prefer it for regular mental health visits and 61% use it for convenient care.

Telehealth is still in early stages of maturity. Only 4% of surveyed top executives consider their organization proficient at implementing remote care. Healthcare is also recognizing that a full telehealth ecosystem must be constructed. A physician leader explained that the industry’s early telehealth incarnations failed to build “virtual-only environments or really drive e-consults as a way of doing things.” A vital ecosystem demands alterations to current contracts, coding, collections, patient financing, staff training and other business practices.

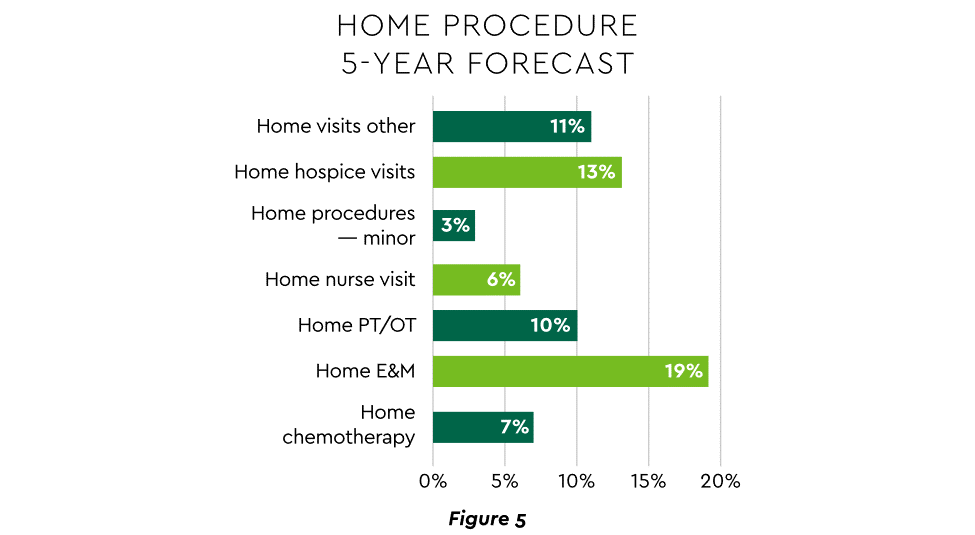

Hospital-at-Home (HaH)

Health systems see particularly promising growth in the provision of acute care in patients’ home settings, including post-surgical and cancer treatment. The federal government has already allowed waivers to 114 systems and 256 hospitals to obtain inpatient-level reimbursement for acute care at home. However, these waivers were prompted by the pandemic and are slated to end in early 2023. The renewal uncertainty has stymied some activity and represents an overhang on the opportunity. However, enthusiasm appears strong, and 33% of hospitals in a recent poll said they would be prone to continue HaH even without renewal.

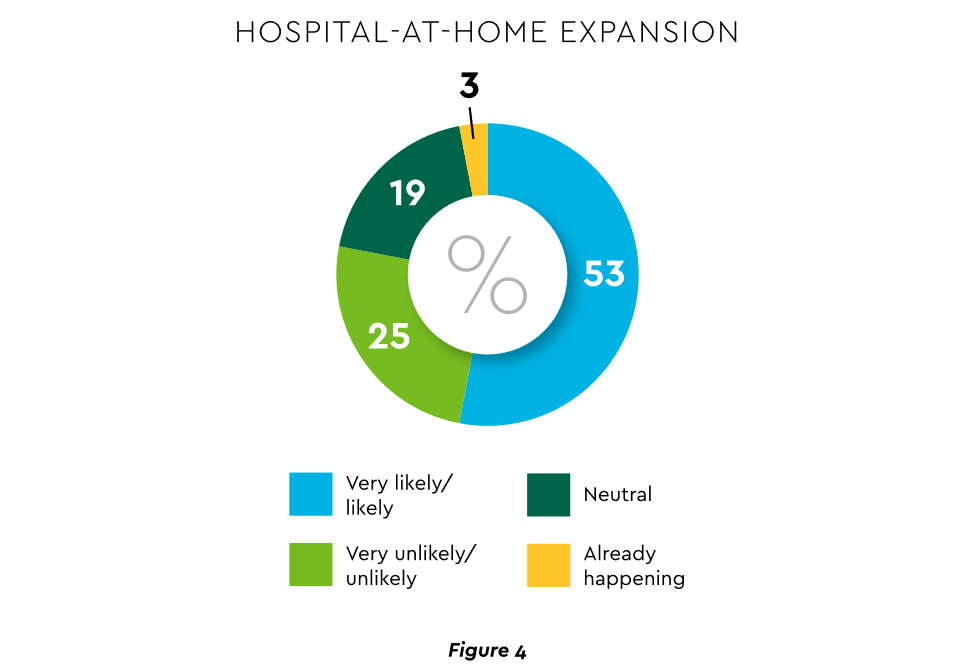

The forecasts are encouraging. Over half of hospitals believe it likely they will utilize HaH for at least half of their chronically ill patients over the next several years (Figure 4).

Harvesting the HaH potential will require implementation of current and emerging enabling technologies in remote monitoring, high-speed networks and artificial intelligence that generates algorithmic guidance for caregivers and patients alike.

3. Strong Drive to Improve and Personalize the Patient Financial Experience

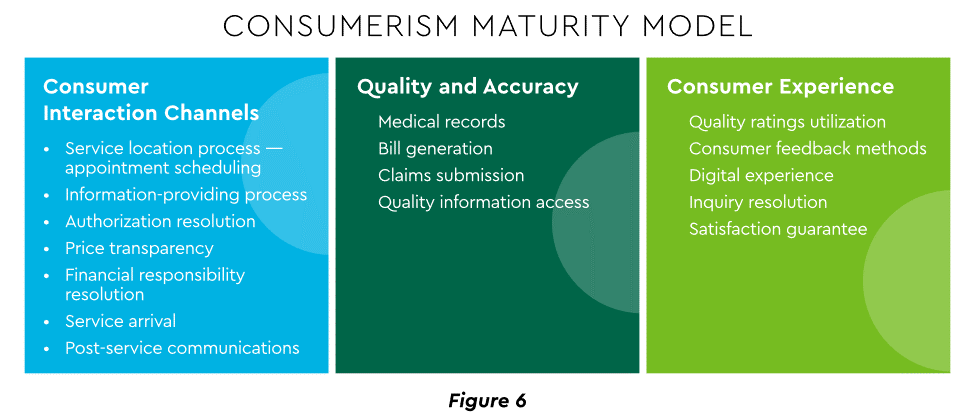

Today’s healthcare market dynamics place a premium on positive patient experiences. The goal is to deliver “an empathetic relationship between customers and brands built on what the customer wants and how they want to be treated.” It is a complex undertaking, with numerous touchpoints as captured in HFMA’s Consumerism Maturity Model (Figure 6).

An array of studies underscores the value proposition for intense provider focus on patient financial experience:

Sixty-one percent of consumers said that ease of making payments is very or somewhat important in decisions to continue seeing a doctor. Over half of patients also said text message reminders make them very or somewhat more likely to pay a bill faster than usual.

Thirty-five percent of respondents “have changed or would change healthcare providers to get a better digital patient administrative experience.”

A quality financial experience encompasses “simplified explanations, consolidated bills that match one’s health plan benefits, clear language displaying patient liability and payment options.”35

Significantly improving the financial experience requires a unified strategy, not just a collection of individual initiatives. Three threads to such a strategy will be prominent in 2023.

Using a Digital Front Door

Organizations have been moving swiftly to channel many patient financial transactions through an integrated Digital Front Door (DFD). This approach offers patients a singular online point of access and intelligent navigation to needed services. Growth is accelerating. A DFD is their patients’ first contact point for 55% of responding organizations, according to one technology survey. A leading forecaster sees 65% of patients engaging services via digital front doors by 2023.

Expanding price transparency

Mandates for full price transparency and “no surprises” billing are in effect, but estimates of compliance are mixed. An analysis of 2,000 hospitals determined that only 16% met the requirement to post an online “machine readable” file displaying clear charges for 300 “shoppable services.” Another assessment showed a more substantial 76% of hospitals had posted files, and 55% were deemed “complete.” One provision of interest to practices is the “good faith estimate” of expected charges required to be given to uninsured and self-pay individuals when they schedule visits. CommerceHealthcare® has worked with clients to enhance the patient financial experience by complementing their website pricing data with clear information on patient financing options and enrollment access. Bill pay information can also be added for one-stop guidance.

Personalizing the experience

Beyond choice and convenience, the deeper objective is truly personalized experiences throughout the care journey. The words of leading analysts best define the drive to personalize:

“Tomorrow’s healthcare experience will be built by patients tailoring their own experience.”

“By 2024, 30% of chronic care patients will truly own and openly leverage their personal health information to advocate for, secure, and realize better personalized care.”

Opportunities abound to personalize the patient financial experience. Automating manual processes establishes a foundation. Patient financing with no- or low-interest credit lines and flexible terms can produce monthly payment schedules tailored to each patient’s needs. Refunds can be made through multiple payment modes to meet varying patient preferences.

4. Evidence Underscores Growing Demand for Patient Financing

Emphasizing patient financing as part of the overall experience is powerful. Patients continue to struggle paying for care. Recent granular data details three related forces at work.

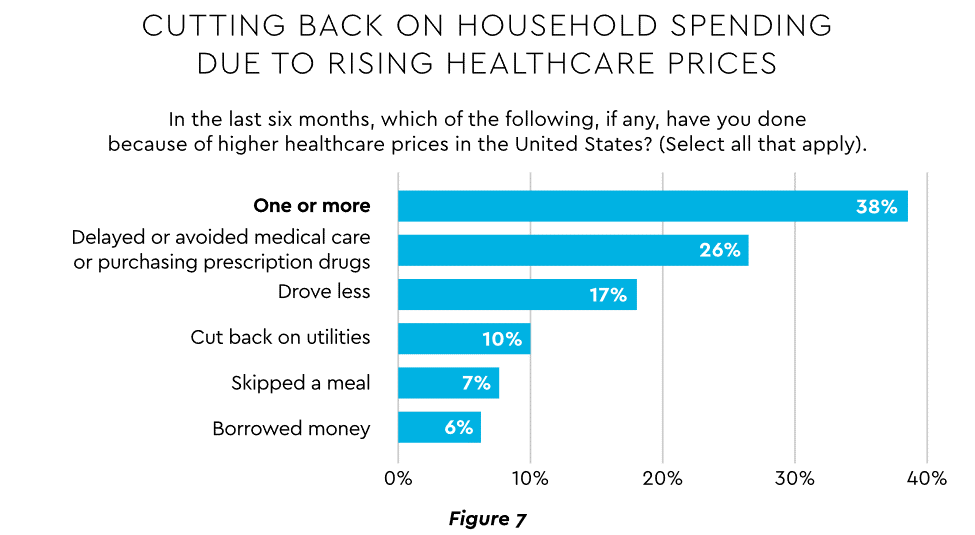

Meeting care costs difficult for many patients

Commonwealth Fund found that 42% of individuals had problems paying medical bills or were paying off medical debt during the past year, while 49% were unable to pay an unexpected $1,000 medical bill.42 Health costs trigger reduction in a range of personal expenditures, led by deferring or avoiding care and drugs (Figure 7).

Twenty-eight percent of Americans now describe themselves as less prepared than last year to pay for routine or unanticipated care.

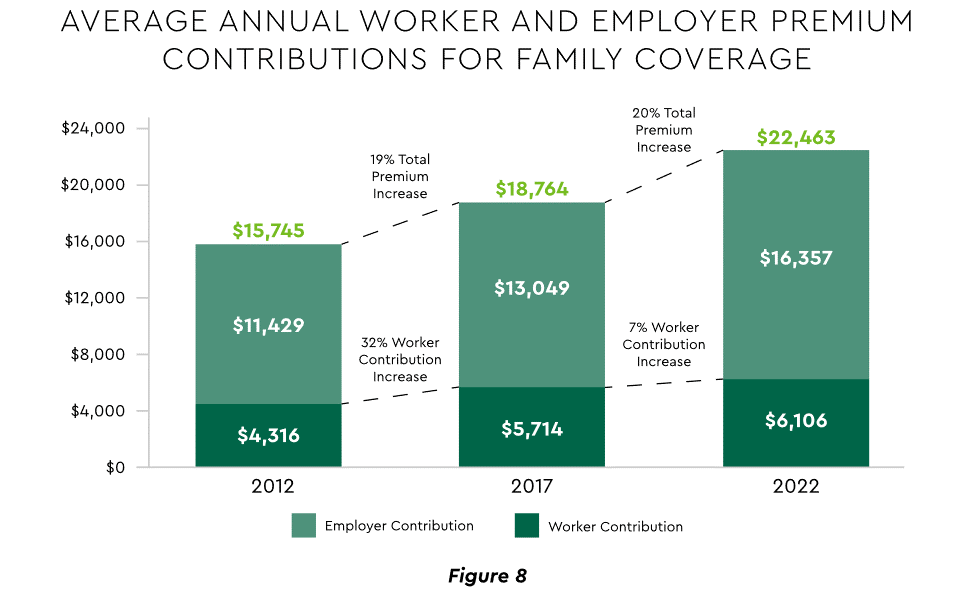

Patient obligation for care costs still rising

Patient obligation continues its upward march. Insurance premiums have climbed steadily for both the insured and their employers, and employees now pay over $6,000 annually on average for family coverage (Figure 8).45

High deductible health plans (HDHP) also place substantial burden on the patient. Through 2021, 28% of workers were enrolled in an HDHP with an average family deductible of $4,705. Employer satisfaction with these plans is high, auguring further expansion.

Providers feeling the financial effects

Patient payment difficulties are clearly impacting provider financials. A recent in-depth analysis uncovered substantial self-pay issues:

Self-pay accounts represented 60% of 2021 patient bad debt, up from 11% in 2018.

Nearly 18% of patient balances were over $7,500 and 17% over $14,000. Collections were noticeably lower at these balances.

Multiple chronic conditions add to the problem. A recent extensive analysis concluded: “Among individuals with medical debt in collections, the estimated amount increased with the number of chronic conditions ($784 for individuals with no conditions to $1,252 for individuals with 7–13).”

For their part, providers will be encouraged to broaden patient financing programs. Patients are certainly interested. When asked, 62% of consumers indicated they would use financing options or creative payment plans if available for large bill amounts. Many health systems, hospitals and practices will turn to outside help to satisfy the demand. A recent analysis recommended that health systems “consider keeping shorter-term payment plans in-house and extended term plans through external partnerships.”

Organizations will also need to step up their communications. A survey revealed that 64% of patients were unaware that their doctors and hospitals offered payment plans or financial help.

5. Building Trust Becoming a Critical Success Factor

Trust has emerged as a paramount issue today for most organizations as they encounter an “imperative to build trust and transparency among different stakeholder groups — employees, customers, suppliers, regulators and the communities in which they operate.” Healthcare is no exception, and the trust issue is growing in both complexity and urgency.

Healthcare’s trust gap

Trust in healthcare took a hit from the COVID-19 experience. A spring 2022 HFMA survey recorded 44% of finance leaders saying they perceived decreased patient trust. Between April 2020 and December 2021, the percentage of Americans who trusted information from doctors “a great deal” declined by 23%, from hospitals 21%, and from nurses 16%. The patient financial experience also faces “drivers of mistrust,” according to surveyed leaders who cited general payment confusion (58%), surprise billing (39%), high prices of commodity items (28%) and lack of price transparency (26%). Building trust reaps dividends. People who trust their providers are five times more likely to stay with them than those who are neutral or distrustful.

Strategies for building trust

Industry experts promote several approaches to galvanize trust among all constituencies:

Commitment. Embedding trust deeply in the organization requires full support from senior leadership.

Data transparency and governance. IDC predicts that “by end of 2023, 20% of expenses on care integration solutions will be centered around ‘trust’ to protect data, workflows and transactions.”

Reliance on fewer business partners. Many health systems, hospitals and practices are reducing their number of vendors in order to focus on a set of trusted long-term partners. For example, almost two-thirds of surveyed providers said they were seeking to streamline the number of software solutions over the next year.

The bank partner advantage

A provider’s banking relationship can yield valuable collaboration in the trust-building endeavor. Banks enjoy solid trust among consumers. As an example, 53.4% of consumers rated banks as most trusted to provide payment “super apps” and financial digital front doors ─ exceeding the next closest source by 10 points.

6. Cybersecurity in 2023: No Rest for the Weary

Cybersecurity is part of the trust calculus and has become an evergreen topic in healthcare. Compromised data and ransomware attacks are ongoing and leaders must continually refine their understanding in at least three areas: the overall security landscape, particular financially related considerations and contemporary security defenses.

The current landscape

The latest statistics quantify the cyber assault on healthcare:

Incidence. 89% of organizations suffered at least one attack in the past 12 months with the average number at 43.

Cost. A provider’s most serious attack costs an average of $4.4 million. IBM calculated healthcare’s average total cost of a breach at $10.1 million, up 42% since 2020.

Attack Characteristics. Healthcare data types most commonly compromised are personal (58%), medical (46%), and credentials (29%). Organizations have an exposure to an average of over 26,000 network-connected devices. A disturbing finding is that those healthcare institutions that paid ransom got back only 65% of their data in 2021.

Specific financial considerations

Finance leaders will also need awareness of the following:

Cyberattacks could affect credit ratings and are often a component of Environmental, Social and Governance assessments.

Financial outsourcing requires monitoring. A recent news story chronicled an accounts receivable firm’s breach that exposed individual information, account balances and payments.

Cyber insurance premiums are likely to increase substantially.

Responses/tools

Beyond a host of management and monitoring tools being deployed, a strategic philosophy is rapidly gaining ground. The “zero trust” model sounds counter to the trust-building mindset described earlier, but it has become essential. It “denies access to applications and data by default,” and 58% of hospitals and health systems have a zero trust initiative in place. Another 37% intend to implement one within 12–18 months.

Cybersecurity investment will challenge CFOs in 2023, especially in areas such as talent. Cybersecurity worker availability is estimated to satisfy only 68% of open positions. Banking partners will also be expected to play an important role. Over the years, major banks have become “leaders in enhancing cyber strategy and investing in cyber defenses, processes and talent.”

7. Digital Transformation of Finance In Focus

Digital transformation is fundamental to healthcare’s business and care delivery model changes. IBM’s website succinctly captures the goal, “Digital transformation means adopting digital-first customer, business partner, and employee experiences.” A leading forecaster believes 70% of healthcare organizations will rely on digital-first strategies by 2027.

Transformation efforts need to accelerate. One study showed that “digital, technology and analytics strategies exist for nearly all organizations, yet only 30% have begun to execute on those plans.”

One functional segment ramping up digital transformation is finance. According to a recent survey, 94% of CFOs and senior leaders stated that such efforts will be at the forefront of financial operations and strategy for 2023–2024, and 79% described it as an “absolute need” for “commercial stabilization and long-term survival of their healthcare organization.”

Advanced technology is gaining traction. Many see optimization in combining robotic process automation (RPA), artificial intelligence and machine learning to create “intelligent automation.” Together, these technologies create algorithms to automate decisions that guide “robotic” software to perform financial actions and thereby reduce manual labor.

Getting to digital-first in finance and across the enterprise has several critical success factors. These include sustained commitment, a platform-centric mindset and effective governance.

Commitment

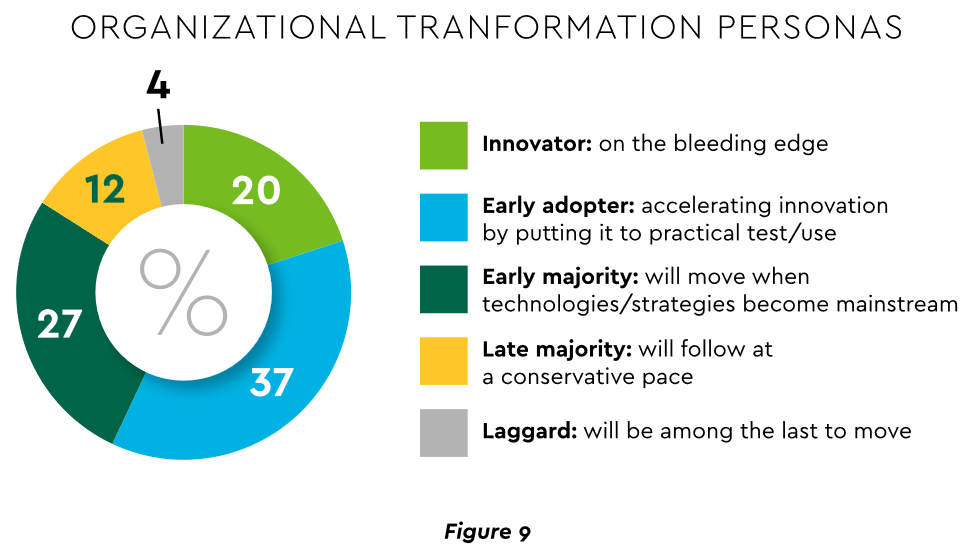

Some assert that few healthcare executives have “created digital strategies that look far enough into the future.” Speed of change is also important. Health systems, hospitals and practices exhibit varying risk appetites and change rates. When asked to self-identify “transformation personas,” a little over half regarded themselves as being on the innovative “early mover” end of the spectrum, while the remainder will adapt as technologies prove themselves (Figure 9). Slower organizations will likely need to increase the pace.

Implementing enterprise platforms rather than proliferating “point solutions” is obligatory. Organizations must be “prepared to compete in the platform economy as platform-based business models have changed the way we live, work and receive care.”

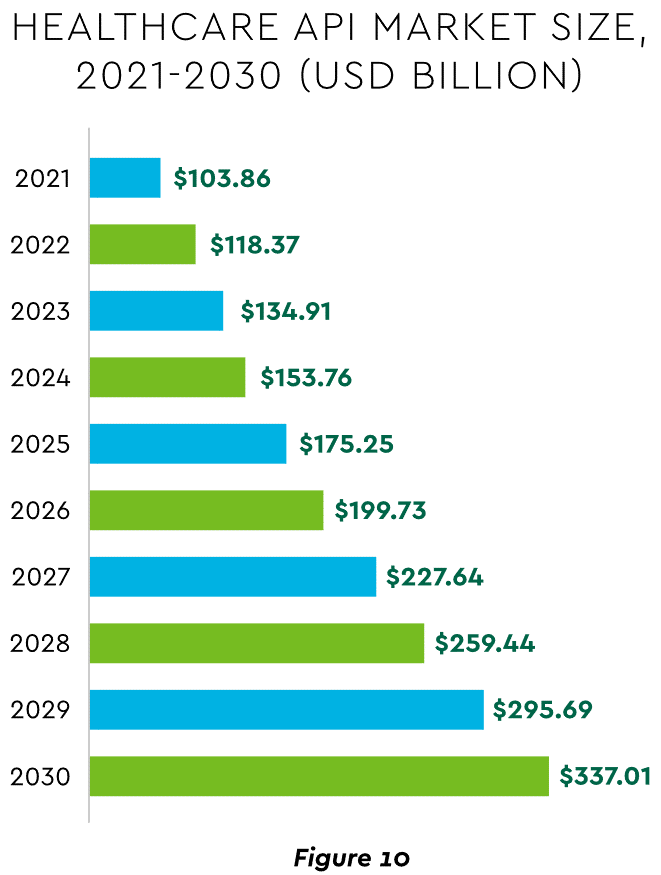

There are still too many tools and applications. A survey of top decision-makers at health systems found that 60% use over 50 software solutions just in operations (24% have over 150). System integration is one answer. Use of application programming interfaces (API) helps this effort substantially. API-first is fast becoming the norm among solution providers, with global API investment expected to nearly triple by 2030 (Figure 10)

Effective governance is vital to constructing a platform-based transformative model and to ensuring wide user adoption. Healthcare has seen the rise of new senior roles such as Chief Digital Officer and Chief Transformation Officer, positions focusing on initiatives like ownership of technology success at the department level and devising user incentives.

8. Digital Payments on the Horizon for Healthcare

A variety of emerging digital payment modes will further the transformation of finance. These payments are expected to grow almost 23% annually in healthcare. ACH payments have been on a strong upward trajectory in healthcare for several years, especially for business transactions. In 2021, ACH tallied a yearly increase of 18% in volume and 5% in dollars.

Notable technologies and payment rails to watch for expected crossover from consumer markets to healthcare include:

Mobile payments. The market for mobile payment technologies has been growing at a 16% compound annual clip and should reach $90 billion in 2023, powered by wide smartphone use, 5G networks and convenience. This category encompasses technologies such as e-wallets, forecasted to grow 23% annually worldwide through 2030.

Real-time payments (RTP). These digital transactions are settled nearly instantaneously through platforms such as The Clearing House. One forecast sees 30.4% compound RTP growth in the U.S. from 2022 to 2030.

Buy Now Pay Later (BNPL). This growing mode offers consumers short-term financing to stretch payments over several installments. A recent survey established that 23% of American adult respondents have used a BNPL service. BNPL is just entering healthcare and is currently regarded as an option for certain elective or cosmetic procedures or for specific individual credit scenarios.

Earned Wage Access (EWA). Using an RTP approach, employers are beginning to offer on-demand pay which enables “instant access to earned wages right after the work is performed, at the end of the shift, or upon completion of a project.” It is not a loan or advance pay. A 2021 poll conducted by Harris found that 83% of U.S. workers feel they should be able to access earned wages at the end of each day. Millennials were particularly interested: 80% would like daily automatic pay streaming to their bank accounts, and 78% said free EWA would boost loyalty to their employer. Given its pressing workforce concerns, healthcare is likely to find EWA a tool to promote retention.

Seeking the right use cases for these payment technologies offers many potential provider benefits.

Conclusion

The connected forces discussed and quantified here create major challenges to address in 2023. The strategic agenda calls for balancing tight cost control with investment in growth opportunities, significantly enhancing patient financial experience by meeting growing patient financial need, shoring up trusted relationships and cybersecurity, and accelerating the digital transformation of finance.

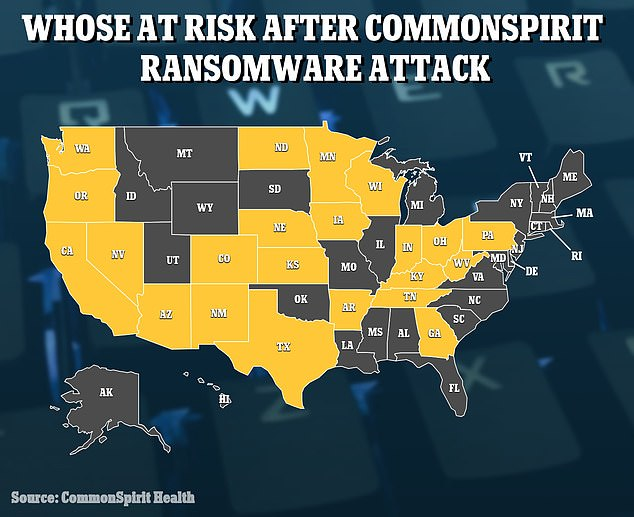

The fourth-largest US hospital system, Chicago-based CommonSpirit Health, is struggling with the impact of a major cyberattack, more than a week after it began disrupting electronic health record access and delaying care in multiple regions across the country. Beyond confirming the attack, the system has not provided many details, other than that it took immediate steps to protect its systems and has begun an investigation.

The Gist: Healthcare hacking is on the rise—our industry experienced the largest increase in cyberattacks of any in 2021. Sitting on troves of valuable patient data, health systems must ready themselves for the reality that hacking attempts are no longer a question of “if,” but “when.” Now is the time not only to ensure proper safeguards are in place to prevent such attacks, but also to prepare response plans for once a hack is confirmed, to be able to continue patient care amid disruption when time is of the essence and patient lives are at stake.

From the largest global meat producer to a major gas pipeline company, cyberattacks have been on the rise everywhere—and with copious amounts of valuable patient data, healthcare organizations have become a prime target.

The graphic above outlines the recent wave of data attacks plaguing the sector. Healthcare data breaches reached an all-time high in 2020, and hacking is now the most common type of breach, tripling from 2018 to 2020. This year is already on pace to break last year’s record, with nearly a third more data breaches during the first half of the year, compared to the same period last year.

Recovering from ransomware attacks is expensive for any business, but healthcare organizations have the highest average recovery costs, driven by the “life and death” nature of healthcare data, and need to quickly restore patient records. A single healthcare record can command up to $250 on the black market, 50 times as much as a credit card, the next highest-value record. Healthcare organizations are also slower to identify and contain data breaches, further driving up recovery costs.

A new report from Fitch Ratings finds cyberattacks may soon threaten hospitals’ bottom lines, especially if they affect a hospital’s ability to bill patients when systems become locked or financial records are compromised. The rise in healthcare hacking is shining a light on many health systems’ lax cybersecurity systems, and use of outdated technology.

And as virtual delivery solutions expand, health systems must double down on performing continuous risk assessments to keep valuable data assets safe and avoid disruptions to care delivery.

CFOs whose finance and accounting functions are built on legacy computer systems got a stark reminder last week from the Colonial pipeline hacking of what’s at stake if their system is breached.

The hack to Colonial’s system led to widespread gas shortages throughout the East and reportedly forced the company to pay $5 million in ransomware to get the instructions for reclaiming its data.

“For finance departments, the cybersecurity risk is huge,” Samir Jaipati, a finance solutions leader with EY Americas, told CFO Dive in an email. “Something built on outdated technology won’t be able to keep hackers out.”

Security specialists generally agree legacy, on-premises systems starting from about 10 years ago typically have solid cybersecurity features built in, but those that are older might require significant upgrades if they’re going to stand a chance against today’s sophisticated hackers.

The risk for CFOs who must manage their processes on an outdated system is they’ll try to get by with short-term fixes that won’t solve the systemic problems they face.

“These temporary fixes aren’t as dependable and in the long-term may cost more,” said Kaipati.

Best effort

For CFOs who don’t have the time or budget to implement the system overhaul they need or to transfer their processes to a more secure on-premises system or to a cloud-based system, the best step is to do a comprehensive review of their end-to-end finance processes to audit for consistency and reliability, said Steve Adams, Gartner finance director.

He suggested reviewing the organization’s record-to-report process from start to finish to understand where non-secure platforms are used, whether there are audit trails that don’t exist, and if exogenous data is incorporated. By eliminating these and other red flags, CFOs can go a significant way to clean up their processes and reduce risk without making system changes, Adams said.

CFOs taking this approach should first engage their IT business partner and ask for a full audit of the cybersecurity capabilities of the suite of financial applications and to use that review as a starting point to making improvements, he said.

Wider integration

Legacy systems pose a broader problem than just security risk; they can impede company growth because CFOs aren’t generating the data or producing the analytics that can help them identify ways to make more money or reduce costs in the same way they can get from sophisticated cloud-based solutions.

Nor can legacy systems be expected to be as good at integrating data throughout the organization in the same way as cloud systems.

For CFOs who can do it, switching from an old on-premises system to the cloud can be a game-changer, said Manish Sharma, an Accenture operations group executive.

“CFOs that are agile and able to overcome these restrictions by scaling digital and cloud-powered technologies have been able to break down data silos and siloed ways of working to support the ever-evolving business strategy with speed and flexibility,” he said.

The importance of using up-to-date IT was emphasized in a recent Accenture report that found “future-ready” leaders are emerging ahead of the pack with higher efficiency and profitability by scaling digital capabilities in ways to improve operational maturity.

“These leaders use better, more diverse data to inform decision-making as part of a cloud-powered continuous feedback loop,” said Sharma.

Flexible categorization

Another benefit of moving to the cloud or a hybrid cloud-on-premises arrangement is cost flexibility.

On average, the cost of managing an outdated IT system can cost a business around $3.61 per line of code or over $1 million for an application with 300,000 lines of code, said Kevin Shuler, owner and CEO of the Quandary Consulting Group, a Denver-based IT firm.

“It accounts for customizations, maintenance, reporting, server and hardware, etc.,” he said.

While replacing the old with the new might appear to be prohibitively expensive at first glance, Shuler noted what can put a CFO more at ease is the costs are more transparent than maintaining a legacy system.

“Better, they can be categorized as either an operating expense or a capital expense since a lot of software is classified as a service rather than software,” he said.

This gives flexibility to the CFO’s finances and forecasting. It also means more resources can be available for modernized systems.

“That means you can get superior resources at a lower cost than trying to pull from a pool of highly specialized and competitive contractors who work mainly with legacy systems,” he said.

Business perspectives on what it will take to shift from crisis mode are solidifying. US finance leaders are focused on shoring up financial positions, as US businesses head into a period of even more operational complexity while they orchestrate a safe return to the workplace. Back-to-work playbooks put workforce health first, as companies set course for a phased-in return to the workplace that will not be uniform across the US or internationally, findings from the survey show. Returning employees and customers are going to experience a work environment that will differ in marked ways as a result. Another change likely to endure post-crisis is the strong role corporate leaders have taken within their communities, placing a renewed emphasis on environmental, social and governance (ESG) efforts going forward.

The actions CFOs are taking show how US businesses continue to adjust to very difficult current conditions with an eye toward an evolving post-COVID world. The level of concern related to the crisis is holding steady. It is high but stabilizing, with 72% of respondents reporting that COVID-19 has the potential for “significant impact” to their business operations vs. 74% two weeks ago.

Key findings

Back-to-work playbooks reshape how jobs performed

49% say remote work is here to stay for some roles, as companies plan to alternate crews and reconfigure worksites.

Protecting people top of mind

77% plan to change safety measures like testing, while 50% expect higher demand for enhanced sick leave and other policy protections.

Substantive impacts expected in 2020 results

Half of all respondents (53%) are projecting a decline of at least 10% in company revenue and/or profit this year.

Cost pressures intensify

A third (32%) expect layoffs to occur, as CFOs continue to target costs, while 70% consider deferring or canceling planned investments.

Economic events shaping CFO response last week

This survey, our fourth since emergency lockdowns took effect in the US, reflects the views of 305 US finance leaders during the week of April 20. It was a week when oil futures traded below $0 as energy markets confronted downshifting global demand, Congress replenished emergency funding of $480 billion for small firms and healthcare systems, and everyone heard the call to get ready to go back to work as the US and Europe firmed up plans to ease quarantines.

Post-crisis world taking shape in plans to reboot the workplace

Health and safety are top priorities for leaders as they prepare to bring people back to on-site work. More than three-quarters (77%) are putting new safety measures in place, while others are taking steps to promote physical distancing, such as reconfiguring workspaces (65%). Findings also show where the virus may have longer-lasting impact on ways of working. Half (49%) of companies say they’re planning to make remote work a permanent option for roles that allow. That’s even higher (60%) among financial services organizations.

Takeaways

Among the small percentage of companies that are beginning to bring people back, returning to work will not mean a return to normal. Companies should consider how to help frontline managers lead with empathy, to communicate transparently and make decisions quickly so employees understand where they stand, have access to the resources available to them, and can share feedback to ensure they feel safe and get what they need. Tools such as workforce location tracking and contact tracing can help support employees with suspected or confirmed infections, while also helping to identify the level of risk exposure. Companies looking to make remote work a permanent option will need to enable leaders to manage a blended workforce of on-site and remote workers during the next 12 to 18 months.

Given that many people may be wary of returning to on-site work, there’s an opportunity for companies to create more targeted benefits to help make the transition easier. Paid sick leaves and worker protections, help with childcare, private transportation to and from work, or other benefits could help employees who may need extra flexibility or who want additional support as they prepare to come back.

Forecasting substantive impacts on 2020 performance

A majority of respondents (80%) continue to expect a decline in revenues and/or profits in 2020. Projections by sector vary, with consumer markets likely the hardest hit: one-third (32%) of CFOs expect a 25% or greater decline in revenues and/or profits this year, compared to 24% of respondents in all sectors.

Takeaways

Outlooks for financial results have held relatively steady in the survey over the last month, and are probably indicative of actual impact. Companies have had the time to evaluate the effects. CFO projections for declining revenue and profits coincide with a widening realization that the US economy is in recession. Since mid-March, jobless claims have soared past 26 million, and Congress passed relief packages of $2.5 trillion. CFOs are evaluating a wide range of scenarios that cover the health situation, the shape of the economic recovery, the spillover into the financial markets, and the resulting impacts on their business. This crisis is setting a new benchmark standard for “unknowable.”

Cost pressures intensifying

CFOs are considering additional ways to scale back on planned investment and/or other fixed costs amid volatility in demand. A third (32%) expect layoffs to occur in the next month, up from 26% two weeks ago. Protecting cash and liquidity positions is paramount. Financial impacts of COVID-19, including effects on liquidity and capital resources, remain the top concern of CFOs (71%). Over half (56%) say they are changing company financing plans, up from 46% two weeks ago.

Among other actions, 43% plan to adjust guidance, which is consistent with responses two weeks ago. This figure will likely increase as companies go through the earnings season over the next two to three weeks. Separately, 91% of respondents are planning to include a discussion of COVID-19 in external reporting. Depending on the type of company, this can mean inclusion in financial statements and/or in risk factors and MD&A results of operations, earnings release or MD&A liquidity sections.

Takeaways

Many CFOs have focused on how they can manage their cash pressures to ride out the crisis. Common approaches have included stop-gap measures, such as hiring freezes and tightening controls on discretionary costs to put an end to travel and events, or the use of contractors. Findings show that these types of cost actions are likely to continue, and they remain at the top of the CFO agenda.

Of those who say they’re considering deferring or canceling planned investments, 80% are considering facilities and general capital expenditures. At the same time, investment programs in areas that are considered important to future growth — including digital transformations, customer experience, or cybersecurity and privacy — are less likely to be targeted. CFOs will increasingly look for ways to prioritize costs in these areas, as businesses grow more confident in recovery prospects — even though current demand is subdued.

Priorities to de-risk supply chains

As companies continue to wade through mitigation efforts and start to think about recovery, many are planning changes to make their supply chains more resilient. Findings show CFOs prioritizing specific actions: 56% cite developing alternate options for sourcing, and 54% say better understanding the financial and operational health of their suppliers.

Takeaways

Findings confirm an emphasis on de-risking supply chains, as companies prioritize the health and reliability of their supplier base among changes they’re planning as a result of COVID-19. In particular, there is a focus on managing risk around supply elements, such as reducing structural vulnerability with other sourcing options.

Some companies are starting to invest in creating data-backed profiles of their supplier base so they know where and when to look for second sources. Others are increasing communication with suppliers to better understand financial health. For many, conducting deeper financial and health reviews of suppliers will become a regular part of their business reviews. Physical supply chain relocations will likely happen only as a last resort, given the costs involved. However, automation of certain elements of the supply chain — to eliminate time-consuming manual tracking efforts and check tariff structures, for example — will likely become more common as companies seek better data to make more informed decisions.

Strategies yet to change, but tech likely to drive M&A

The impact of the outbreak on mergers and acquisitions (M&A) strategies remains mixed. While 40% of respondents say their company’s M&A strategy is not being affected by COVID-19, compared with 34% two weeks ago, one in five say it’s too difficult to assess what changes, if any, will need to be made to strategy. CFOs within the technology, media and telecommunications industry stand out in particular. They are less likely to report decreasing appetite for M&A due to COVID-19, compared with peers in other sectors, and 55% say the crisis hasn’t changed their M&A strategy.

Takeaways

These findings highlight the fundamental strengths of the tech sector and suggest it will be among those driving M&A in the months ahead. Tech giants, in particular, have large cash reserves. Moreover, demand for some tech products and services is strong as businesses return to work — 40% of CFOs say they will accelerate automation and new ways of working as they transition back. Additionally, technologies such as drones, artificial intelligence and robotics, will likely enjoy wider adoption in the post-COVID-19 environment. This leaves tech better-positioned to weather the pandemic’s economic fallout and to execute on inorganic growth strategies. M&A is likely to recover faster than the US economy, with tech among the cash and capital-rich sectors leading the charge.PwC studies show that a combination of factors has been driving a decoupling of deals from the broader economy.

Business recovery timeframes have extended

Organizations are realizing the business recovery from the impacts of the virus will take longer. The March measures of manufacturing and services activities show sharp drops. Demand is not only declining, it’s shifting. Moreover, even as some US states start to reopen, difficulties in setting up testing could keep some states in a holding pattern. As a result, for CFOs, the time required to return to “business as usual” the moment that COVID-19 ends continues to lengthen. Currently, 48% believe it will take at least three months to return to normal, up from 39% two weeks ago.

Takeaways

As reality sets in and companies understand the true impacts to their operations, CFO perceptions of the length of time to business recovery has extended. According to our analysis of how companies gauge their response to the crisis in PwC’s COVID-19 Navigator diagnostic tool, the expected impact of COVID-19 on businesses globally remains high, with consumer markets and manufacturing the most susceptible among industries. Put another way, businesses that are less reliant on a large, complex supply chain to deliver products, or are able to work relatively effectively while remote, are also likely to be among the least exposed.

Consumer-facing companies reconfigure physical sites as shutdowns start to lift

Companies in consumer-facing sectors continue to contend with both sides of the demand equation, as consumers sheltering in place focus single-mindedly on essential products to the exclusion of other offerings. Consumer markets (CM) CFOs are more likely to list a decrease in consumer confidence and spending as a top-three concern than they were two weeks ago (66% vs. 50%). For CM CFOs, consumer confidence trends translate almost directly to revenues, with 32% projecting an adverse impact on revenue and/or profit of at least 25% in 2020, compared with 24% of respondents across all industries.

In response, almost three-quarters of CM CFOs (73%) are considering deferring or canceling planned investments, targeting mostly general capital expenses, such as facilities. They also say technologies that can improve their understanding of changes in customer demand are a top-three priority as they plan changes to their supply chain strategies (41% vs. 30% for all sectors).

CM CFOs are planning workplace safety measures (86% vs. 77% for all sectors) and reconfiguring work sites to promote physical distancing as part of their transition back to on-site work (77% vs. 65% for all sectors). They recognize that consumers want the assurance of a safe physical environment above all else, especially because the majority of CM products and services require a physical component, despite the continuing shift to online.

Takeaways

Consumer-facing companies continue to be among the hardest hit, as the public health crisis keeps the majority of consumers confined to their homes for now. As they grapple with immediate challenges, CM companies are pulling back on capital investments. However, most are still planning to shore up their digital presence in response to accelerated online demand that could last well beyond the recovery period.

Health system pivots to new ways of working

What’s on the mind of financial leaders in the health industry? As they plan to bring more of their workforce back on-site, they are more likely than leaders in other industries to be leaning on technology to help them manage staffing uncertainties. Fifty-four percent of healthcare CFO respondents said they plan to accelerate automation and new ways of working, compared with an average of 40% across all industries.

Healthcare organizations are simultaneously solving two critical issues: uncertainty about demand and protecting their workforce. Health organization CFOs (70%) were more likely than executives from other industries (an average of 50%) to report that they expect higher demand for employee protections in the next month. Meanwhile, consumer anxiety over their own safety is driving up uncertainty about demand for healthcare and medical products. Forty-one percent of healthcare finance leaders listed tools to better understand customer demand as a top-three priority area when considering changes to their supply chain strategies, compared to 30% of financial leaders in all sectors. Fifty-one percent of healthcare finance leaders said they are making staffing changes as a result of slowed demand.

Takeaways

A survey conducted by PwC’s Health Research Institute in early April found that some consumers are delaying care and medications amid the pandemic. In this latest PwC survey of CFOs, healthcare leaders report uncertainty about how much of their business will return as the threat of the pandemic ebbs, making staffing decisions difficult.

As the nation continues to grapple with the pandemic, getting back to work is top of mind for US financial leaders overall, but this is an especially pressing issue for health leaders. They must plan for their own workforces, while dealing with an unfolding financial calamity — 81% expect their company’s revenue and/or profits to decline this year as a result of COVID-19. On par with other industries, they expect this decline, even though their organizations play central roles in addressing the human toll of the pandemic. One strategy is to use telehealth technology to virtually care for patients, thereby protecting patients and caregivers during the pandemic.

Financial firms see fewer layoffs, but slower recovery

Financial services (FS) CFOs are bracing for a longer road back to normal. About a third (35%) now think it could take six months to get back to business as usual, up sharply from 15% just two weeks ago. They’re also more optimistic about the bottom line. More than a quarter (27%) of FS survey respondents expect revenue and/or profits to fall by 10% or less. Across all industries, only 18% felt as confident.

Takeaways

Banks are playing a critical role in helping stabilize the economy, as they work on the front lines to distribute CARES Act provisions. Along with insurers and asset managers, they also rely heavily on workers with specialized technical and institutional knowledge. This may explain why FS CFOs expect fewer layoffs (15% vs. 32% overall) or furloughs (17% vs. 44% overall) over the next month. Now, they’re trying to focus on keeping workers healthy and safe.

Conversations are starting to shift toward when and how to transition back to physical offices. For some employees, work may look very different: More FS CFOs are considering making remote work a permanent option for roles that allow it (60% vs. 49% overall). To better protect their employees, they’re also looking to evaluate new tools to support workforce tracking and contact tracing (32% vs. 22% overall) as part of the return-to-work process.

Deeper insight into health of suppliers is top priority for industrial products

The industrial products (IP) sector is in full-throttle cost-cutting mode. Nearly all IP CFOs (96%) report considering cost containment measures, compared with 87% two weeks ago. Some of this comes in the form of layoffs: 49% of IP CFOs expect layoffs to occur vs. 36% two weeks ago. The longer the crisis lasts, the longer the impact on recovery times for their business. When asked how long it would take for their business to return to business as usual if the COVID-19 crisis were to end today, 15% of IP CFOs said less than one month, down from 25% two weeks ago.

Meanwhile, they’re closely examining challenged supply chains. When asked to list their top-three priority areas when planning changes to supply-chain strategies, 66% of IP CFOs identified understanding the financial and operational health of their suppliers, compared to 54% of CFOs across all industries. A majority (56%) also cited developing additional and alternate sourcing options as a priority. And the extent of the financial damage is sinking in: 65% of IP CFOs estimate 2020 revenues and/or profits will drop at least 10%.

Takeaways

IP CFOs are signaling they’re in the thick of the crisis, as they absorb historical lows in production, with March US industrial output plunging to levels not seen since the end of WWII. Continued cost actions are still in the cards.

IP finance leaders are looking ahead to get back to business, with some already bringing workers back on-site. Some are expecting changes to the workplace. Thirty-nine percent of IP CFOs are considering making remote work a permanent option for roles that allow, and 31% are considering accelerating automation and new ways of working. While these are still early days for US producers in returning to work, bringing millions of workers back into the fold may well usher in more change management than the industry now expects.

Tech, media and telecom well-positioned to power the recovery

Technology, media and telecommunications (TMT) companies are well-positioned for recovery from the initial blow of COVID-19. As they stabilize operations in response to the crisis, the percentage of TMT CFOs anticipating revenue and/or profit declines is down 19 percentage points from two weeks ago to 65%. The data suggest that TMT companies are preparing for a future in which virtual work options gain greater acceptance over traditional office settings. TMT companies are more likely to reduce their real estate footprint as they transition back to on-site work (38% compared to 26% for all sectors), and 55% say they’re planning to make remote work permanent for positions that allow.

Of those who said they’re considering deferring or canceling planned investments, TMT companies are less likely to reduce digital transformation investments (13%) than all sectors (22%). Their increased optimism about digital investment as they strategize for the future is further borne out by the data: Two weeks ago, of those who said they were deferring or canceling planned investment, TMT was on track to reduce digital investments at the same rate as other sectors (25%).

Takeaways

The resilience of TMT companies is evident in their approach to this crisis. Bolstered by robust liquidity, the majority of companies in the sector are looking ahead to a recovery they will power by using both organic growth and M&A. In the wake of a crisis that has accelerated more widespread virtual connectivity, look for new emerging-tech-enabled business models to take shape.

Where to focus next

COVID-19 has put businesses under enormous strain to drive new ways of working. When the pandemic began, many companies put their people’s health and safety at the center of their decision-making, and they appear to be doing the same as they prepare to ramp up business. With most firms expecting to bring people back on-site in phases, leaders will need to help employees adjust to a changed environment while still managing the well-being, engagement and productivity of all workers. Purpose-led communication will continue to be critical to keep people informed, and leaders should demonstrate empathy while helping employees adjust to what will likely be an extended transition period.

The new offerings include HP Pro Security Edition, HP Proactive Security, and HP Sure Click Enterprise. These are aimed at the security threats that evolve and disrupt business every day.

With the recent surge of remote workers — due to work-from-home rules forced upon us by COVID-19 — HP said we must all be aware of the increased risks of working from home. Over 80% of home office routers have been found to be vulnerable to potential cyberattacks.

Emails also pose a significant risk to organizations, with over 90% of PC infections originating from attachments and 96% of security breaches not discovered until months later. There are 5 billion new threats per month, based on HP’s estimates.

“Our HP Pro Security Edition takes Sure Sense and Sure Click and bundles [them] with our system,” said Andy Rhodes, global head of commercial PCs, in a press briefing. “Endpoints are still an enormous risk — 90% of infections originate with emails. Every user is at risk here.”

HP Pro Security for small businesses.

With public health concerns over COVID-19 spreading worldwide, HP wants customers to have the information they need to effectively clean HP devices and maintain a healthy work environment.

The Centers for Disease Control and Prevention (CDC) recommendscleaning surfaces, followed by disinfection, as a best practice for the prevention of COVID-19 and other viral respiratory illnesses in households and community settings.

In fact, HP has issued its own whitepaper for cleaning your devices.

“We get asked [about] this every day,” said Rhodes. “If you use the wrong disinfectant, you can actually damage the product.”

A CDC-recommended disinfectant that is also within HP’s cleaning guidelines is an alcohol solution consisting of 70% isopropyl alcohol and 30% water.

The steps below use the CDC-recommended alcohol solution to clean high-touch, external surfaces on HP products:

Wear disposable gloves made of latex (or nitrile gloves if you are latex-sensitive) when cleaning and disinfecting surfaces.

Turn off the device and disconnect AC power (printers should be unplugged from the outlet). Remove batteries from items like wireless keyboards. Never clean a product while it is powered on or plugged in.

Disconnect any external devices.

Moisten a microfiber cloth with a mixture of 70% isopropyl alcohol and 30% water. Do not use fibrous materials, such as paper towels or toilet paper. The cloth should be moist, but not dripping wet. (Isopropyl alcohol is sold in most stores, usually in a 70% isopropyl alcohol/30% water solution. It may also be marketed as rubbing alcohol.)

Do not spray any liquids directly onto your device.

Gently wipe the moistened cloth on the surfaces to be cleaned. Do not allow any moisture to drip into areas like keyboards, display panels, or USB ports located on the printer control panels, as moisture entering the inside of an electronic product can cause extensive damage to the product.

Start with the display or printer control panel (if applicable) and end with any flexible cables, like power, keyboard, and USB cables.

When cleaning a display screen or printer control panel, carefully wipe in one direction, moving from the top of the display to the bottom.

Ensure surfaces have completely air-dried before turning the device on after cleaning. No moisture should be visible on the surfaces of the product before it is powered on.

After disinfecting, copier/scanner glass should be cleaned again using an office glass cleaner sprayed onto a clean rag to remove streaking. Streaking on the copier/scanner glass from the CDC-recommended cleaning solution could cause copy quality defects.

Gloves should be discarded after each cleaning. Clean hands immediately after gloves are removed.

Yesterday we spoke with a senior healthcare executive leading the COVID-19 response for a regional health system on the West Coast. Their area is now experiencing exponential growth of new cases, with the number of local diagnoses doubling every couple of days. In all likelihood, they’re less than two weeks from having the number of cases seen in harder-hit areas like San Francisco, Seattle and New York City. She said the “anticipation of what is about to happen” is the scariest part of the around-the-clock work they are doing to prepare.

But that two-week lead time has given them precious time to organize, and she generously shared key elements of their action plan. Their preparation work—surely similar to what hundreds of health systems around the country are doing—impressed us not only with its breadth, depth and comprehensiveness, but also the level of energy and confidence conveyed by the hundreds of actions and decisions, large and small, the system is making every day. Here are some of their important learnings so far:

Even though the surge of patients has yet to begin, staff are “worried and scared”. They are concerned about PPE shortages and personal safety and stressed at home with schools and daycare closed. Detailed and regular communication is more critical than ever—and they’re trying to answer every inbound concern or question from associates directly. They are funding and expanding childcare options for staff, through partnerships with community organizations and daily stipends for home-based care.

As the system works through worst-case scenario planning, they anticipate the need forcritical care nurses, respiratory therapists, and emergency physicians will be the worst bottlenecks, and they are working to cross-train adjacent clinicians and build new staffing models to increase capacity. While most providers are deeply dedicated to providing care for COVID-19 patients, a small number have already “called off” and refused to report—creating unanticipated questions around how to manage these difficult situations.

As they prepare to implement new surge staffing models, the system is now navigating through a period of downtime. With elective procedures cancelled and some ambulatory sites closed, they currently need fewer nurses and clinical staff than a month ago, and are creating policies, like allowing staff to go negative into PTO, to maintain income while they wait for the surge. Staff who must work in-person are working variable shifts to reduce crowding. They are also working to credential nurses and staff furloughed from local ambulatory surgery centers, so they have them ready to deploy when needed.

IT staff are working nonstop to quickly make it possible for all eligible employees to work remotely, and to enable staff to safely gain access to the system’s intranet while guarding against new cybersecurity threats. The system is training and enabling hundreds of doctors to deliver care virtually, including affiliated independents.

Guidelines for coronavirus patient management and recommended PPE practices change daily; it’s a full-time job for clinical leaders to keep up. Doctors are eager to try novel and creative treatments for very sick patients. (For instance, one doctor is developing a 3-D printed device that will allow one ventilator to be used for four patients simultaneously.) This eagerness to “do something” is understandable but creates a bit of chaos as leaders work to create policies around how to best manage patients.

While leaders communicate with other health systems and local and state authorities daily, the vast majority of decisions are made internally, on the fly. For instance, the system is connecting with now-empty local hotels and universities to provide options for low-acuity patient capacity, but leaders hope that parallel efforts at other organizations can be brought together into a more unified regional response. For now, however, coordination would likely create unacceptable delays.

Long-term health and stamina of staff is top among the system’s concerns. “If I borrow worry from the future”, this leader said, “I am worried that we are facing years-long trauma, both emotional and financial, and I’m not sure how we will sort it out”. For now, efforts to support staff and provide moments of relief and joy, are critical, and very appreciated by front-line team members.

We left this conversation emotionally overwhelmed ourselves, and with a huge sense of gratitude for clinicians and health system leaders. Americans can take comfort in the amount of work that is taking place even before critical patients begin to appear—and that doctors, nurses and hospitals are truly dedicated to providing us the best possible care under circumstances they have never faced before. If you know about creative approaches or new ideas organizations are putting in place to contend with the current situation, please let us know. We’re eager to share great ideas!