Late last week, Salt Lake City, Utah-based Intermountain Healthcare and University of Colorado-affiliated UCHealth, based in Aurora, CO, shared that they are jointly developing a clinically integrated network (CIN). It will initially comprise 700 primary care physicians working at UCHealth’s 12 hospitals and hundreds of clinics, but may expand in the future. The CIN will leverage Intermountain’s value-based care expertise and its SelectHealth insurance plans. The two health systems will remain independent and operate the CIN as a separate company.

The Gist: This partnership continues Intermountain’s expansion into Colorado, after it finalized its merger with SCL Health in April of last year.

It’s a smart way for Intermountain to strengthen its foothold in the state, especially as further health system acquisitions in the Denver area may raise antitrust concerns.

Intermountain will be able to tap into a larger network ofphysician relationships that it can use tobolster its health plan, with significantly lower infrastructure costs compared to employment.

These types of partnership strategies may also be bed-warming for deeper relationships, with the opportunity to demonstrate value before a full-on merger.

In our decades of working in healthcare, we’ve never seen a time when payer-provider negotiations have been more tense. Emboldened insurers, having seen strong growth during the pandemic, are entering contract negotiations with an aggressive posture.

“They weren’t even willing to discuss a rate increase,” one CFO shared as he described his health system’s recent negotiations with a large national insurer. “The plan’s opening salvo was a fifteen percent rate cut!”

Health systems are feeling lucky to get even a two or three percent rate bump, well short of the historical average of seven percent—and far short of what would be needed to account for skyrocketing labor, supply, and drug costs. According to executives we work with, efforts to describe the current labor crisis and resulting cost impacts with payers are largely falling on deaf ears.

This scenario is playing out in markets across the country, with more insurers and health systems announcing that they are “terming” their contract, publicly stating they will cut ties should the stalemate in negotiations persist.

Speaking off the record, a system executive shared how this played out for them. With negotiations at an impasse, a large insurer began the process of notifying beneficiaries that the system would soon be out-of-network, and patients would be reassigned to new primary care providers. The health plan assumed that the other systems in the market would see this as a growth opportunity—and was shocked when they discovered that other providers were already operating at capacity, unable to accommodate additional patients from the “terminated” system.

Mounting concerns about access brought the plan back to the table. Even in the best of times, a major insurer cutting ties with a health system is extremely disruptive for consumers, who must shift their care to new providers or pay out-of-network rates. But given current capacity challenges in hospitals nationwide, major network disruptions can be even more dire for patients—and may force payers and providers to walk back from the brink of contract termination.

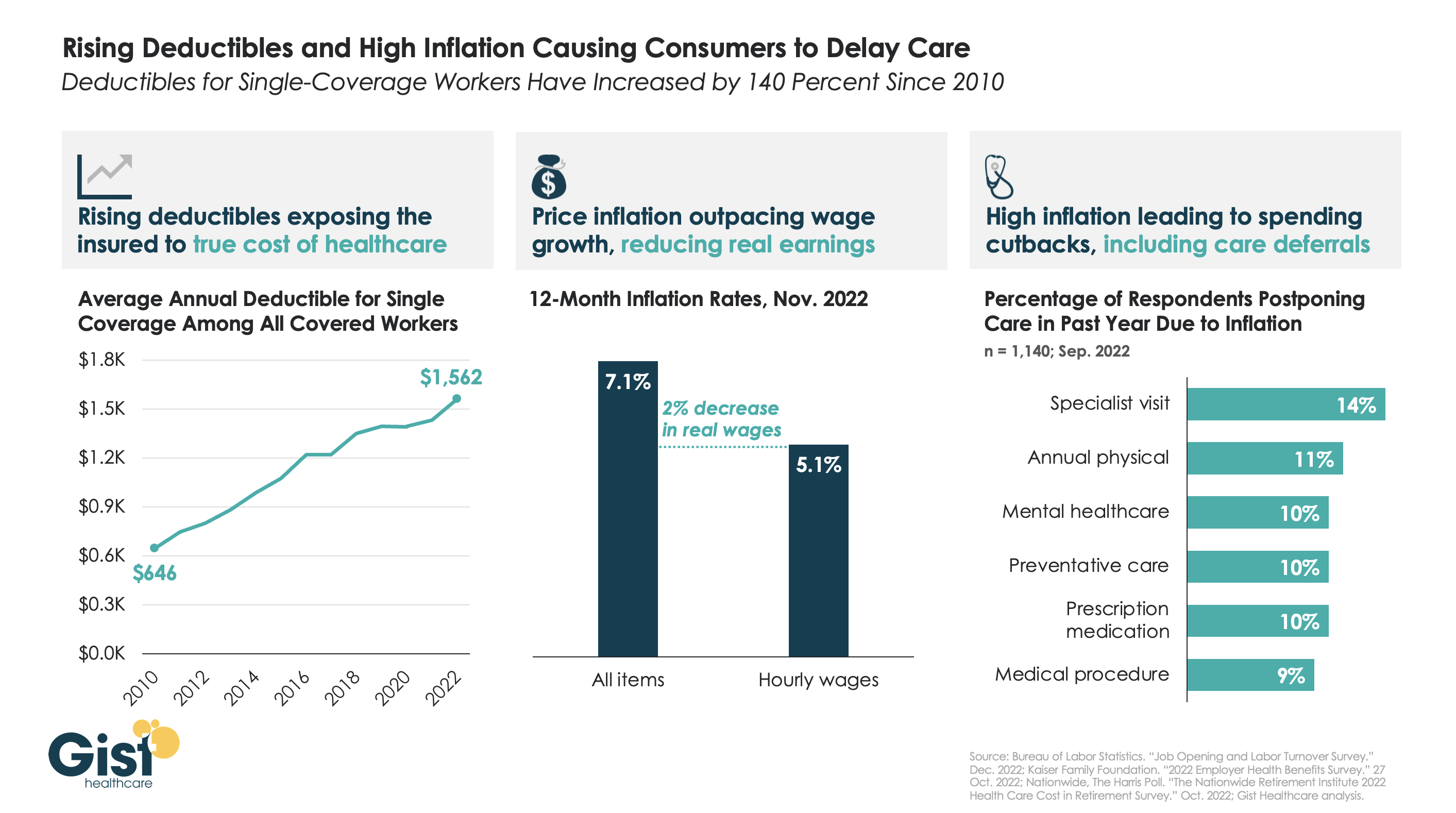

After COVID fears and shutdowns led consumers to delay care early in the pandemic, persistently high inflation over the past year has further suppressed volumes.

As the graphic above illustrates, the average deductible for individual coverage has grown by over 140 percent since 2010, exposing consumers to an increasing portion of healthcare costs, and prompting economists to reevaluate the adage that healthcare is “recession-proof”.

This year, that trend collided with an inflation spike that outpaced wage gains by two percent. Faced with diminished purchasing power, households are making budget tradeoffs which explicitly pit healthcare against other essential household needs.

For some, this cost-cutting impulse even extends to preventative screenings—required to be covered without cost-sharing—when consumers’ financial concerns drive them to avoid healthcare altogether.

While the latest inflation report suggests price increases are moderating, fears of a broader recession persist, making it critical for health systems and physicians to communicate with patients, encouraging them to continue to access preventive care, educating them about lower cost care options, and helping them prioritize treatment that should not be put off.

Last Thursday, the Federal Trade Commission (FTC) released a proposed rule that would ban employers from imposing noncompete agreements on their employees. Noncompetes affect roughly 20 percent of the American workforce, and healthcare providers would be particularly impacted by this change, as far greater shares of physicians—at least 45 percent of primary care physicians, according to one oft-cited study—are bound by such agreements.

The rulemaking process is expected to be contentious, as the US Chamber of Commerce has declared the proposal “blatantly unlawful”. While it is unclear whether the rule would apply to not-for-profit entities, the American Hospital Association has released a statement siding with the Chamber of Commerce and urging that the issue continue to be left to states to determine.

The Gist: Should this sweeping rule go into effect, it would significantly shift bargaining power in the healthcare sector in favor of doctors, allowing them the opportunity to move away from their current employers while retaining local patient relationships.

The competitive landscape for physician talent would change dramatically, particularly for revenue-driving specialists, who would have far greater flexibility to move from one organization to another, and to push aggressively for higher compensation and other benefits.

Given that the FTC cited suppressed competition in healthcare as an outcome of current noncomplete agreements, the burden will be on organizations that employ physicians—including health systems and insurers, as well as private equity-backed corporate entities—to prove that physician noncompetes areessential to their operations and do not raise prices, as the FTC has suggested.

Big questions tend to have no easy answers. Fortunately, few people would say they went into healthcare for its ease.

The following questions about hospitals’ culture, leadership, survival and opportunity come with a trillion-dollar price tag given the importance of hospitals and health systems in the $4.3 trillion U.S. healthcare industry.

1. How will leaders insist on quality first in a world where it’s increasingly harder to keep trains on time?

Hospitals and health systems have had no shortage of operational challenges since the COVID-19 pandemic began. These organizations at any given time have been or still are short professionals, personal protective equipment, beds, cribs, blood, helium, contrast dye, infant formula, IV tubing, amoxicillin and more than 100 other drugs. After years of working in these conditions, it is understandable why healthcare professionals may think with a scarcity mindset.

This is something strong leaders recognize and will work to shake in 2023, given the known-knowns about the psychology of scarcity. When people feel they lack something, they lose cognitive abilities elsewhere and tend to overvalue immediate benefits at the expense of future ones. Should supply problems persist for two to three more years, hospitals and health systems may near a dangerous intersection where scarcity mindset becomes scarcity culture, hurting patient safety and experience, care quality and outcomes, and employee morale and well-being as a result.

The year ahead will be a great test and an opportunity for leaders to unapologetically prioritize quality within every meeting, rounding session, budgetary decision, huddle and town hall, and then follow through with actions aligned with quality-first thinking and commentary. Working toward a long-term vision and upholding excellence in the quality of healthcare delivery can be difficult when short-term solutions are available. But leaders who prioritize quality throughout 2023 will shape and improve culture.

2. Who or what will bring medicine past the scope-of-practice fights and turf wars that have persisted for decades?

It is naive to think these tensions will dissolve completely, but it would be encouraging if in 2023 the industry could begin moving past the all-too-familiar stalemates and fears of “scope creep,” in which physicians oppose expanded scope of practice for non-physician medical professionals.

Many professions have political squabbles and sticking points that are less palpable to outsiders. Scope-of-practice discord may fall in that category — unless you are in medicine or close to people in the field, it can easily go undetected. But just as it is naive to think physicians and advanced practice providers will reach immediate harmony, so too is it naive to think that aware Americans who watch nightly news segments about healthcare’s labor crisis and face an average wait of 26 days for a medical appointment will have much sympathy for physicians’ staunch resistance to change.

The U.S. could see an estimated shortage of between 37,800 and 124,000 physicians by 2034, according to the Association of American Medical Colleges. Ideally, 2023 is the year in which stakeholders begin to move past the usual tactics, arguments and protectionist thinking and move toward pragmaticism about physician-led care teams that empower advanced practice providers to care for patients to the extent of the education and training they have. The leaders or organizations who move the needle on this stand to make a name for themselves and earn a chapter or two in the story of American healthcare.

3. Which employers will win and which will lose in lowering the cost of healthcare?

Employers have long been incentivized to do two things: keep their workers healthy and spend less money doing it. News of companies’ healthcare ventures can be seen as cutting edge, making it easy to forget the origins of integrated health systems like Oakland, Calif.-based Kaiser Permanente, which dates back to one young surgeon establishing a 12-bed hospital in the height of the Great Depression to treat sick and injured workers building the Colorado River Aqueduct.

Many large companies have tried and failed, quite publicly, to improve healthcare outcomes while lowering costs. Will 2023 be the year in which at least one Fortune 500 company does not only announce intent to transform workforce healthcare, but instead point to proven results that could make for a scalable strategy?

Walmart is doing interesting things. JPMorgan seems to have learned a good deal from the demise of Haven, with Morgan Health now making some important moves. And just as important are the large companies paying attention on the sidelines to learn from others’ mistakes. Health systems with high-performing care teams and little variation in care stand to gain a competitive advantage if they draw employers’ attention for the right reasons.

4. Who or what will stabilize at-risk hospitals?

More than 600 rural hospitals — nearly 30 percent of all rural hospitals in the country — are at risk of closing in the near future. Just as concerning is the growing number of inner-city hospitals at increased risk of closure. Both can leave millions in less-affluent communities with reduced access to nearby emergency and critical care facilities. Although hospital closures are not a new problem, 2022 further crystalized a problem no one is eager to confront.

One way for at-risk hospitals to survive is via mergers and acquisitions, but the Federal Trade Commission is making buying a tougher hurdle to clear for health systems. The COVID-19 public health emergency began to seem like a makeshift hospital subsidy when it was extended after President Joe Biden declared the pandemic over, inviting questions about the need for permanent aid, reimbursement models and flexibilities from the government to hospitals. Recently, a group of lawmakers turned to an agency not usually seen as a watchdog for hospital solvency — HHS — to ask if anything was being done in response to hospital closures or to thwart them.

Maintaining hospital access in rural and urban settings is a top priority, and the lack of interest and creativity to maintain it is strikingly stark. As a realistic expectation for 2023, it would be encouraging to at least have an injection of energy, innovation and mission-first thinking toward a problem that grows like a snowball, seemingly bigger, faster and more insurmountable year after year.

Look at what Mark Cuban was able to accomplish within one year to democratize prescription drug pricing. Remember how humble and small the origins of that effort were. Recall how he — albeit being a billionaire — has put profit secondary to social mission. There’s no one savior that will curb hospital closures in the U.S., but it would be a good thing if 2023 brought more leadership in problem-solving and matching a big problem with big energy and ideas.

5. Which hospital and health system CEOs will successfully redefine the role?

Many of the largest and most prominent health systems in the country saw CEO turnover over the past two years. With that, health systems lost decades of collective industry and institutional knowledge. Their tenure spanned across numerous milestones and headwinds, including input and compliance with the Affordable Care Act, the move from paper to digital records, and major mergers and labor strikes. The retiring CEOs had been top decision-makers as their organizations met the demands of COVID-19 and its consequences. They set the tone and had final say in how forcefully their institutions condemned racism and what actions they took to address health inequities.

To assume the role of health system CEO now comes with a different job description than it did when outgoing leaders assumed their posts. Many Americans may carry on daily life with little awareness as to who is at the top of their local hospital or health system. The pandemic challenged that status quo, throwing hospital leaders into the limelight as many Americans sought leadership, expertise and local voices to make sense of what could easily feel unsensible. The public saw hospital CEOs’ faces, heard their voices and read their words more within the past two years than ever.

In 2023, newly named CEOs and incoming leaders will assume greater responsibility in addition to a fragile workforce that may be more susceptible to any slight change in communication, transparency or security. They will need to avoid white-collar ivory towers, and earn reputations as leaders who show up for their people in real, meaningful ways. Healthcare leaders who distance themselves from their workforce will only let the realistic, genuine servant leaders outshine them. In 2023, watch for the latter, emulate them and help up-and-comers get as much exposure to them as possible.

The percentage of healthcare organizations with an internal minimum wage of $15 or higher increased significantly over the last year, according to the “2022 Health Care Staff Compensation Survey” from SullivanCotter.

In 2021, less than 30 percent of healthcare organizations had an internal minimum wage of $15 per hour or more; this year, nearly 70 percent do. Some health systems are increasing the internal minimum wage to stay competitive amid staffing shortages and rising inflation. Others are increasing hourly rates as a result of union negotiations.

Health systems reported large increases in overall staff salaries, wages and benefits this year, and many expect to see increases in 2023 as well.

Here is how the internal minimum wage rates changed over the last year:

1. Less than $10 per hour 2021: 2.9 percent 2022: 2.2 percent

2. $10 per hour 2021: 14.7 percent 2022: 5 percent

3. $11 per hour 2021: 13.7 percent 2022: 3.9 percent

4. $12 per hour 2021: 12.7 percent 2022: 7.8 percent

5. $13 per hour 2021: 12.7 percent 2022: 6.1 percent

6. $14 per hour 2021: 14.7 percent 2022: 5.6 percent

7. $15 per hour 2021: 26.5 percent 2022: 53.9 percent

8. More than $15 per hour 2021: 2 percent 2022: 15.6 percent

Here are 30 health systems with strong operational metrics and solid financial positions in 2022, according to reports from Fitch Ratings and Moody’s Investors Service.

1. Advocate Aurora Health has an “AA” rating and a stable outlook with Fitch. The health system, dually headquartered in Milwaukee and Downers Grove, Ill., has a strong financial profile and a leading market position over a broad service area in Illinois and Wisconsin, Fitch said. The health system’s fundamental operating platform is strong, the credit rating agency said.

2. Atlantic Health System has an “Aa3” rating and stable outlook with Moody’s. The Morristown, N.J.-based health system has strong operating performance and liquidity metrics, Moody’s said. The credit rating agency expects Atlantic Health System to sustain strong performance to support capital spending.

3. Banner Health has an “AA-” rating and stable outlook with Fitch. The Phoenix-based health system’s core hospital delivery system and growth of its insurance division combine to make it a successful, highly integrated delivery system, Fitch said. The credit rating agency said it expects Banner to maintain operating EBITDA margins of about 8 percent on an annual basis, reflecting the growing revenues from the system’s insurance division and large employed physician base.

4. BayCare has an “AA” rating and stable outlook with Fitch. The 14-hospital system based in Clearwater, Fla., has excellent liquidity and operating metrics, which are supported by its leading market position in a four-county area, Fitch said. The credit rating agency expects strong revenue growth and cost management to sustain BayCare’s operating performance.

5. Bon Secours Mercy Health has an “AA-” rating and stable outlook with Fitch. The Cincinnati-based health system has a broad geographic footprint as one of the five largest Catholic health systems in the U.S., a good payer mix and a leading or near-leading market share in eight of its 11 markets in the U.S., Fitch said.

6. Bryan Health has an “AA-” rating and stable outlook with Fitch. The Lincoln, Neb.-based health system has a leading and growing market position, very strong cash flow and a strong financial position, Fitch said. The credit rating agency said Bryan Health has been resilient through the COVID-19 pandemic and is well-positioned to accommodate additional strategic investments.

7. CaroMont Health has an “AA-” rating and stable outlook with Fitch. The Gastonia, N.C.-based system has a leading market position in a growing services area and a track record of good cash flow, Fitch said.

8. Christiana Care Health System has an “Aa2” rating and stable outlook with Moody’s. The Newark, Del.-based system has a unique position as the state’s largest teaching hospital and extensive clinical depth that affords strong regional and statewide market capture, and it is expected to return to near pre-pandemic level margins over the medium-term, Moody’s said.

9. Cone Health has an “AA” rating and stable outlook with Fitch. The Greensboro, N.C.-based health system has a leading market share and a favorable payer mix, Fitch said. The health system’s broad operating platform and strategic capital investments should enable it to return to stronger operating results, the credit rating agency said.

10. Deaconess Health System has an “AA” rating and stable outlook with Fitch. The Evansville, Ind.-based system has a leading market position in its primary service area and a favorable payer mix, Fitch said. The ratings agency said it expects Deaconess’ operating EBITDA margins to improve and stabilize around 10 percent by 2023, reflecting strong volumes and focus on operating efficiencies.

11. El Camino Health has an “AA-” rating and stable outlook with Fitch. El Camino Health, which includes hospital campuses in Los Gatos, Calif., and Mountain View, Calif., has a solid market share in a competitive market and a stable payer mix, Fitch said. The credit rating agency said El Camino Health’s balance sheet provides moderate financial flexibility.

12. Gundersen Health System has an “AA-” rating and stable outlook with Fitch. The La Crosse, Wis.-based health system has strong balance sheet metrics, a leading market position and an expanding operating platform in its service area, Fitch said. The credit rating agency expects the health system to return to strong operating performance as it emerges from disruption related to the COVID-19 pandemic.

13. Hackensack Meridian Health has an “AA-” rating and stable outlook with Fitch. The Edison, N.J.-based health system has shown consistent year-over-year increases in market share and has a solid liquidity position, Fitch said.

14. Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The Falls Church, Va.-based health system has a consistently strong operating cash flow margin and ample balance sheet resources, Moody’s said. Inova’s financial excellence will remain undergirded by its favorable regulatory and economic environment, the credit rating agency said.

15. Intermountain Healthcare has an “Aa1” rating and stable outlook with Moody’s. The Salt Lake City-based health system has exceptional credit quality, which will continue to benefit from its leading market position in Utah, Moody’s said. The credit rating agency said the health system’s merger with Broomfield, Colo.-based SCL Health will also give Intermountain greater geographic reach.

16. Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The Boston-based health system has an excellent clinical reputation, good financial performance and strong balance sheet metrics, Moody’s said. The credit rating agency said it expects Mass General Brigham to maintain a strong market position and stable financial performance.

17. Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The credit rating agency said Mayo Clinic’s strong market position and patient demand will drive favorable financial results. The Rochester, Minn.-based health system “will continue to leverage its excellent reputation and patient demand to continue generating favorable operating performance while maintaining strong balance sheet ratios,” Moody’s said.

18. MemorialCare has an “AA-” rating and stable outlook with Fitch. The Fountain Valley, Calif.-based health system has excellent leverage metrics and a strong financial profile, Fitch said. The credit rating agency said it expects the system’s leverage metrics to remain strong over the next several years.

19. Methodist Health System has an “Aa3” rating and stable outlook with Moody’s. The Dallas-based system has strong operating performance, and investments in facilities have allowed it to continue to capture more market share in the fast-growing Dallas-Fort Worth, Texas, area, Moody’s said. The credit rating agency said it expects Methodist Health System’s strong operating performance and favorable liquidity to continue.

20. OhioHealth has an “AA+” rating and stable outlook with Fitch. The Columbus, Ohio-based system has an exceptionally strong credit profile, broad regional operating platform and leading market position in both its competitive two-county primary service area and broader 47-county total service area, Fitch said.

21. Parkview Health has an “Aa3” rating and stable outlook with Moody’s. The Fort Wayne, Ind.-based system has a leading market position with expansive tertiary and quaternary clinical services in Northeastern Indiana and Northwestern Ohio, Moody’s said.

22. Presbyterian Healthcare Services has an “Aa3” rating and stable outlook with Moody’s and an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system is the largest in the state, and it has strong revenue growth and a healthy balance sheet, Moody’s said. The credit rating agency said it expects the health system’s balance sheet and debt metrics to remain strong.

23. Rady Children’s Hospital has an “AA” rating and stable outlook with Fitch. The San Diego-based hospital has a very strong balance sheet position and operating performance, and it is also a leading provider of pediatric services in the growing city and tri-county service area, Fitch said.

24. Rush Health has an “AA-” rating and stable outlook with Fitch. The Chicago-based health system has a strong financial profile and a broad reach for high-acuity services as a leading academic medical center, Fitch said. The credit rating agency expects Rush’s services to remain profitable over time.

25. Stanford (Calif.) Health Care has an “AA” rating and stable outlook with Fitch. The health system has extensive clinical reach in a competitive market and its financial profile is improving, Fitch said. The health system’s EBITDA margins rebounded in fiscal year 2021 and are expected to remain strong going forward, the crediting rating agency said.

26. ThedaCare has an “AA-” rating and stable outlook with Fitch. The Neenah, Wis.-based system has a focused strategy, strong financial profile and robust market share, Fitch said.

27. Trinity Health has an “AA-” rating and stable outlook with Fitch. The Livonia, Mich.-based system’s large size and market presence in multiple states disperses risk and the long-term ratings incorporate the expectation that Trinity will return to sustained stronger operating EBITDA margins.

28. UnityPoint Health has an “AA-” rating and stable outlook with Fitch. The Des Moines, Iowa-based health system has strong leverage metrics and cash position, Fitch said. The credit rating agency expects the health system’s balance sheet and debt service coverage metrics to remain robust.

29. University of Chicago Medical Center has an “AA-” rating and stable outlook with Fitch. The credit rating agency said it expects University of Chicago Medical Center’s capital-related ratios to remain strong, in part because of its broad reach of high-acuity services.

30. Yale New Haven (Conn.) Health has an “AA-” rating and stable outlook with Fitch. The health system’s turnaround efforts, brand recognition and market presence will help it return to strong operating results, Fitch said.

Hospitals experienced a slight boost to operating margins in November, but not enough to restore the median negative margins that persisted for 2022 to date.

Kaufman Hall’s December “National Flash Hospital Report“ — based on data from more than 900 hospitals — found hospitals’ median operating margin was -0.2 percent through November, a slight improvement from the median of -0.3 percent recorded a month prior.

A 1 percent decline in expenses from October to November drove the eleventh-hour improvement to margins and tipped the scales on hospitals’ relatively flat revenue. Additionally, hospitals saw labor expenses decrease 2 percent in November, potentially driven by less reliance on contract labor.

The median -0.2 percent margin recorded in November 2022 marks a 44 percent decline for margins in 22 year-to-date compared to 2021 year-to-date. Kaufman Hall’s index shows hospitals’ median monthly margins have been in the red throughout 2022, starting with the -3.4 percent recorded in January, driven by the omicron surge. November is tied with September as hospitals’ best month of the year, with both sharing a median margin of -0.2 percent.

Outpatient care marks one of the brighter spots for hospitals’ finances, with outpatient revenue up 10 percent year-over-year while inpatient revenue was flat over the same time period.

“The November data, while mildly improved compared to October, solidifies what has been a difficult year for hospitals amidst labor shortages, supply chain issues and rising interest rates,” Erik Swanson, senior vice president of data and analytics with Kaufman Hall, said. “Hospital leaders should continue to develop their outpatient care capabilities amid ongoing industry uncertainty and transformation.”

The December issue of Health Affairs included an intriguing study that sought to explain the recent trend toward more high-intensity billing in emergency departments (EDs). Using ED visit data for “treat-and-release” visits (i.e. ED patients who were not admitted to the hospital), the study found that visits deemed high-intensity, as defined by certain high-complexity or critical care billing codes, rose from around 5 percent of visits in 2006 to 19 percent in 2019.

The authors conclude that while about half of this increase can be explained by changes in patient case mix and available care services that were visible in claims data, the other half is due to the adoption of sophisticated revenue cycle management programs, and industry-wide changes to billing practices that include upcoding.

The Gist: At first blush, an increase in high-intensity ED billing may not be a bad thing, if it means that greater numbers of people with low-acuity needs are going to urgent care centers, and avoiding EDs for needs that can be managed elsewhere. But the study finds thattreat-and-release rates are going up for high-intensity patients.

Though the authors list many potential reasons for this—including the changed role of the ED as a diagnostic referral center used by primary care physicians for quick workups of complex patients, the growing number of multimorbid seniors, and value-based care’s pressure to reduce hospital admission rates in favor of more resource-intensive ED visits—we have a strong suspicion that good old-fashioned upcoding also plays a role, especially as the percentage of emergency medicine practices managed by private equity companies increased from four percent to over eleven percent across the same time period as the study.

At a recent health system retreat, the CFO shared data describing a trend we’ve observed at a number of systems: for the past few months, emergency department (ED) volumes have been up, but the percentage of patients admitted through the ED is precipitously down.

The CFO walked to through a run of data to diagnose possible causes of this “uncoupling” of ED visits and inpatient admissions. Overall, the severity of patients coming to the ED was higher compared to 2019, so it didn’t appear that the ED was being flooded with low-level cases that didn’t merit admission. Apart from the recent spike in respiratory illness brought on by the “tripledemic” of flu, COVID and RSV, there wasn’t a noteworthy change in case mix, or the types of patients and conditions being evaluated in the emergency room. (Fewer COVID patients were admitted compared to 2021, but that wasn’t enough to account for the decline.) The physicians staffing the ED hadn’t changed, so a shift in practice patterns was also unlikely.

A physician leader attending the retreat spoke up from the audience: “I can diagnose this for you. I work in the ED, and the problem is we can’t move them. Patients are sitting in the ED, in hallways, in observation, sometimes for days, because we can’t get a bed on the floor. The whole time we are treating them, and many of them get better, and we’re able to discharge them before a bed frees up.”

With nursing shortages and other staffing challenges, many hospitals have been unable to run at full capacity even if the demand for beds is there. So total admissions may be down, even if the hospital feels like it’s bursting at the seams.

The current staffing crisis not only presents a business challenge, but also adversely impacts patient experience, and makes it more difficult to deliver the highest quality care. A good reminder of the complexity of hospital operations, where strain in one part of the system will quickly impact the performance of other parts of the care delivery continuum.