Welcome to the second installment of Pulse on Healthcare. This month’s issue takes a look at the issues causing financial distress for healthcare organizations, and how CFOs can take action to relieve it.

According to the 2022 BDO Healthcare CFO Outlook Survey, 63% of healthcare organizations are thriving, but 34% are just surviving. And while healthcare CFOs have an optimistic outlook—82% expect to be thriving in one year—they’ll need to make changes this year if they’re going to reach their revenue goals. To prevent and solve for financial distress, CFOs need to review and address the underlying causes. Otherwise, they might find themselves falling short of expectations in the year ahead.

Here are six ways for CFOs to address financial distress:

1. Staffing shortages: 40% of healthcare CFOs say retaining key talent will be a top workforce challenge in 2022.

How can you avoid a labor shortage? Think about increasing wages for your frontline staff, especially your nurses. You could also reconsider the benefits you’re offering and ask yourself what offerings would be attractive for your frontline staff. For example, whether you offer free childcare could mean the difference between your staff staying and walking out for another employment opportunity. Additionally, consider enhancing or simplifying processes through technology to relieve some strain from day-to-day tasks.

2. Budget forecasting: Almost half (45%) of healthcare organizations will undergo a strategic cost reduction exercise in 2022 to meet their profitability goals.

How else can you cut costs? One option is to adopt a zero-based approach to budgeting this year. This allows you to build your budget from the ground up and find new areas to adjust costs to free up resources. Consider some non-traditional cost reduction areas, like telecommunication or select janitorial expenses, which are overlooked year after year. Cost savings in these areas can be substantial and quick to implement.

3. Bond covenant violations: 42% of healthcare CFOs have defaulted on their bond or loan covenants in the past 12 months. Interestingly, 25% say they have not defaulted but are concerned they will default in the next year.

How can you avoid violations? The first step to take is to meet with your financial advisors, especially if you are worried you’re going to default on your bond or loan covenants. You want to get their counsel before you default so you can prepare your organization and mitigate the damage. Ideally, they can help you avoid a default altogether.

4. Supply chain strains: 84% of healthcare CFOs say supply chain disruption is a risk in 2022.

How can you mitigate these risks? Supply chain shortages are a ubiquitous problem across industries right now, but not all of the issues are within your control. Focus on what is, including assessing your supply chain costs and seeing where you can find the same or similar products for lower prices. Identifying alternative suppliers may end up saving you a lot of frustration, especially if your regular suppliers run into disruptions.

5. Increased cost of resources: 39% of healthcare CFOs are concerned about rising material costs and expect it will pose a significant threat to their supply chain.

How can you alleviate these concerns? Price increases for the resources you purchase — including medical supplies, drugs, technology and more — could deplete your financial reserves and strain your liquidity, exacerbating your financial difficulties. You may be able to switch from physician-preferred products to other, most cost-effective products for the time being. Switching medical suppliers may even save you money in the long run. Involving clinical leadership in the process can keep physicians informed of the choices you are making and the motivation behind them.

6. Patient volume: 39% of healthcare CFOs are making investments to improve the patient experience.

How can you satisfy your patient stakeholders? As hospitals and physician practices get closer to the new normal of care, patients are returning to procedures and check-ins they put off at the height of the pandemic. Patients want a comfortable experience that will keep them coming back, including a safe and clean atmosphere at in-person offices.

They also want access to frictionless telehealth and patient portals for those who don’t want to or can’t travel to receive care. Revisit your “Digital Front Door Strategy” and consider ways to improve and streamline it. These investments can also go toward improving health equity strategies to ensure everyone across communities is receiving the same level of care.

A recent conversation with a health system CFO made us realize that a long-standing nugget of received healthcare wisdom might no longer be true. For as long as we can remember, economic observers have said that healthcare is “recession-proof”—one of those sectors of the economy that suffers least during a downturn. The idea was that people still get sick, and still need care, no matter how bad the economy gets. But this CFO shared that her system was beginning to see a slowdown in demand for non-emergent surgeries, and more sluggish outpatient volume generally.

Her hypothesis: rising inflation is putting increased pressure on household budgets, and is beginning to force consumers into tougher tradeoffs between paying for daily necessities and seeking care for health concerns. This is having a more pronounced effect than during past recessions, because we’ve shifted so much financial risk onto individuals via high deductibles and cost-sharing over the past decade.

There’s a double whammy for providers: because the current inflation problems are happening in the first half of year, most consumers are nowhere near hitting their deductibles, leading this CFO to forecast softer volumes for at least the next several months, until the usual “post-deductible spending spree” kicks in.

Combined with the tight labor market, which has increased operating costs between 15 and 20 percent, this inflation-driven drop in demand may have hospitals and health systems experiencing their own dose of recession—contrary to the old chestnut.

Citi, The American Hospital Association (AHA) and the Healthcare Financial Management Association (HFMA) recently hosted the 22nd annual Not-for-Profit Healthcare Investor Conference. The event was in person, after being virtual in 2021 and canceled in 2020 due to the pandemic. Leaders from over 25 diverse health systems, as well as private equity and fund managers, presented in panel discussions and traditional formats. The following summary attempts to synthesize key themes and particularly interesting work by leading health systems. The conference title was “Refining the Now, Reshaping What’s Next.”

Is Healthcare Headed for Best of Times or Worst of Times?

Clearly the pandemic showed how essential and adaptive the US healthcare industry is, and especially how incredible healthcare workers continue to be. It also exposed and accelerated many underlying dynamics, such as impact of disparities, clinical labor shortages and supply chain challenges. On balance, at this year’s conference presenters remained quite optimistic about the future, and felt that despite enormous pain, the pandemic has helped to accelerate positive transformation across healthcare.

At the same time, almost all presenters referenced future headwinds from labor and supply inflation, concerns about increasing payment pressures, and the continued need to address disparities and social justice. That being said, there was not much disclosure at the conference about just how bad things could get in the future given accelerated operational and financial risks.

As usual at such a conference, there was much passion, creativity, sharing and celebration. While each organization and market differ somewhat, the following are common themes discussed.

Key Themes

Enormous Workforce Challenges – Every speaker referenced workforce as being THE key issue they are facing, specifically retirement, recruitment, retention, well-being and cost. We have talked for years about a future caregiver shortage, but this reality was accelerated by the pandemic. The majority of health systems saw single-digit turnover rates grow to 20-30%, and the cost of temporary labor such as traveling nurses, decimate operating margins. The many strategies discussed at the conference went beyond simply paying more to attract and retain staff. A key question is whether organization-specific strategies will be enough, or whether we need a broader societal and industry-wide collaborative effort to dramatically increase training slots for nurses and other allied health professionals.

Pandemic Stressed Organizations and Accelerated Transformation – At the 2021 virtual Citi/AHA/HFMA conference, many posited that the country was past the worst of the pandemic. (In fact this author’s summary of last year’s conference was titled “Sunrise After the Storm”). That was before the Omicron wave hit hard in Q1 2022. First-quarter 2022 operating margins were negative for most but not all healthcare systems due to cumulative impact of Omicron, temporary labor and supply costs, especially since the governmental support that partially offset those costs in 2020 ended. Organizations and their teams remain resilient, but highly stressed. Risks and challenges associated with future waves continue, as well as high reliance on foreign drug and supply manufacturing. While highly distracting and painful, many organizations discussed how the pandemic actually accelerated the pace of transformation. Necessity drives required action, and at least temporarily overcomes political and cultural barriers to change.

Growing Pursuit of Scale, Including through M&A and Partnerships – All health systems continue to be highly complex with multiple competing “big-dot” priorities. Multiple systems described their current M&A and growth strategies, pursuit of scale, as well as how these strategies were impacted by the pandemic. While the provider community remains highly unconsolidated on a national basis, mergers are more frequent, including between non-contiguous markets. Systems said that larger size, coupled with disciplined management, can reduce cost structure and improve quality and patient experience. While some pursue scale through organic growth initiatives or M&A, others described success in creating scale by leveraging partnerships with “best-in-class” niche organizations and other outside expertise.

Health Equity, Diversity and ESG as Core to Mission – Consistent with last year, most speakers discussed their efforts to address health equity, social justice, diversity, and Social Determinants of Health. Many health systems have developed robust strategies quickly as the pandemic spotlighted the impact of existing disparities. There is increasing interest in Environment, Social and Governance (ESG) initiatives, including environmental stewardship to improve the health of their communities and the world by reducing their carbon footprint and medical waste.

Patient-Centric Care Transformation Continues as a Priority – The pandemic significantly accelerated the shift to telehealth and virtual care. Many health systems are increasing their efforts to design care around the patient instead of the traditional provider centric focus. While the need for inpatient care will always continue, more care is taking place in settings closer to or at home, with digital enablement. Expansion of personalized medicine, genetic testing and therapies, and drug discovery are transforming how healthcare is provided.

Affordability and Value-Based Care – US healthcare costs as a percentage of GDP increased from 18% in 2019 to almost 20% in 2020, mainly driven by the pandemic. There remains a dichotomy between reliance on fee-for-service payment and commitment to value-based care. Although only 11% of commercial payment is currently through two-sided risk arrangements, almost all presenting health systems discussed their strategies to continue moving to value-based care and to improve affordability. Some systems are leveraging their integrated health plans and/or expanding risk-based contracts. Many are trying to reduce unnecessary care through adoption of evidence-based models and to shift care to less costly settings.

Inflation and Accelerating Financial Pressures – Health systems are facing unprecedented increases in labor and supply costs, that are likely to continue into the foreseeable future. At the same time, commercial payment rate adjustments are “sticky low” as insurers and employers push back on rate increases. Governmental payment rate increases are less than cost inflation. In addition to current cuts like the re-implementation of sequestration, longer-term cuts to provider assessment programs, provider-based billing, disproportionate share and Medicaid expansion may severely impact many organizations over time. Benefits like 340b discounts are also experiencing pressure. Post-pandemic clinical-volume trends remain unclear, and additional governmental support associated with future pandemic waves is unlikely. Adding to these challenges, declines in stock and bond prices are negatively impacting currently strong balance sheets.

Conclusion: Best or Worst of Times in Healthcare?

Time will tell, in retrospect, if the next five years will be the best of times, worst of times, or both in healthcare. Optimists point to the resiliency of healthcare organizations; enormous opportunity to reduce unnecessary cost through adoption of evidence-based care and scale; pipeline of new cures and technology; and opportunities to address social and health equity. Pessimists point to likely unprecedented financial pressures and operational challenges due to endemic labor and supply shortages; high-cost inflation vs. constrained payment rates; and future uncertainty about the pandemic, the economy and investment markets.

The situation will undoubtedly vary by market and organization as reflected in conference presentations, but all systems will likely face substantial pressure. As one speaker noted “humans have a great ability to respond to pain,” so this may be the inflection point where more healthcare systems radically accelerate necessary change to improve health, make healthcare more equitable and affordable, with higher quality and better outcomes. Some health systems are clearly doing that, with pace, nimbleness and passion. Can the industry as a whole accomplish it successfully?

The Federal Reserve just raised interest rates by three-quarters of a percentage point, the biggest single increase in interest rates since 1994. It’s another move in the Fed’s effort to tackle the fastest inflation in four decades.

I understand the Fed’s urgency, but it has entered dangerous territory. If the Fed continues down this path – as it has signaled it will – the economy will be plunged into a recession. Every time over the last half century the Fed has raised interest rates this much and this quickly, it has caused a recession.

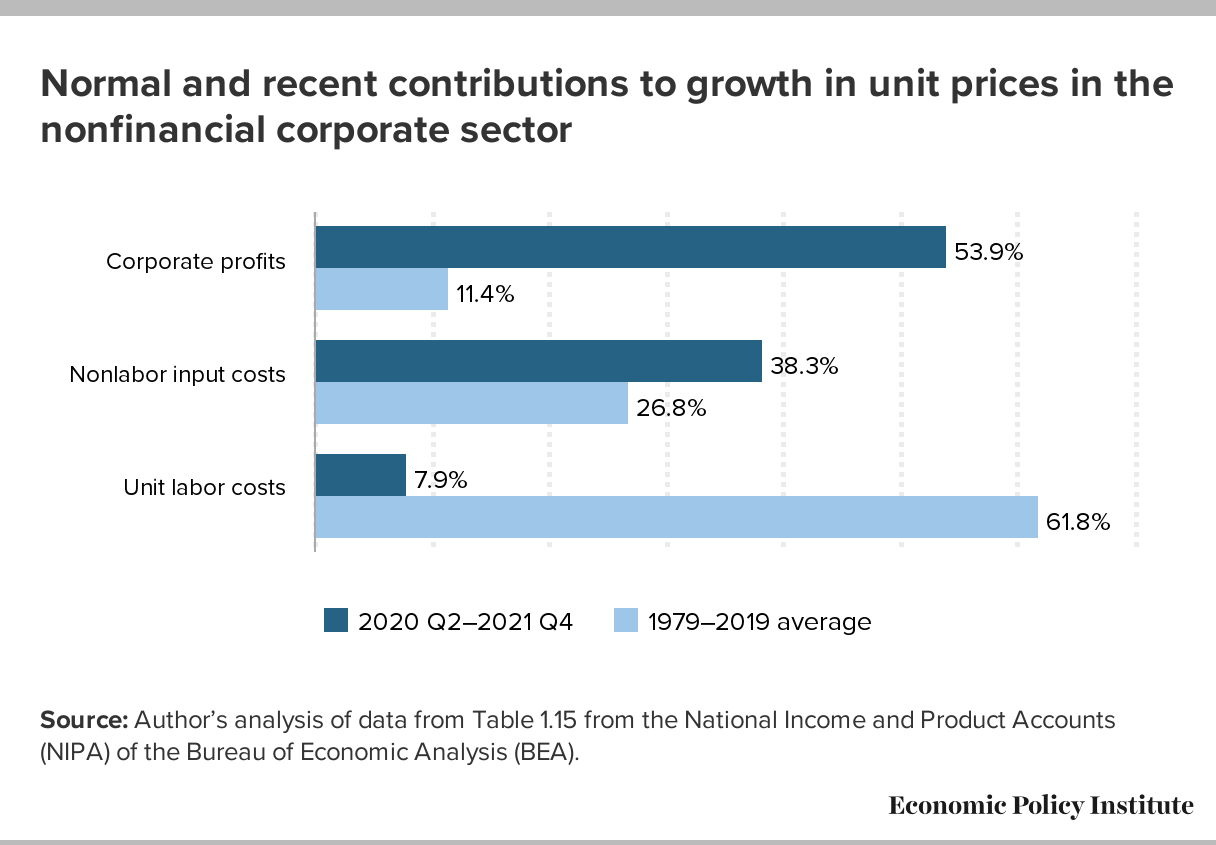

Besides, interest rate increases will not remedy the major causes of the current inflation – huge pent-up worldwide demand from two years of pandemic, shortages of goods and services responding to that demand, Putin’s war in Ukraine, and big profitable corporations with enough pricing power to use inflation as a cover for pushing up prices even further.

The Fed assumes that price increases are being driven by wage increases — so-called “wage-price inflation.” That’s incorrect. Wages are lagging behind inflation. A more accurate description of what we’re now seeing might be called “profit-price inflation” — prices driven upward by corporations seeking increased profits. (See chart below, from the Economic Policy Institute.)

A recession will be especially harmful to people who are most vulnerable to downturns in the economy — who are the first to be fired (and last to be hired again when the economy turns upward): lower-wage workers, disproportionately women and people of color.

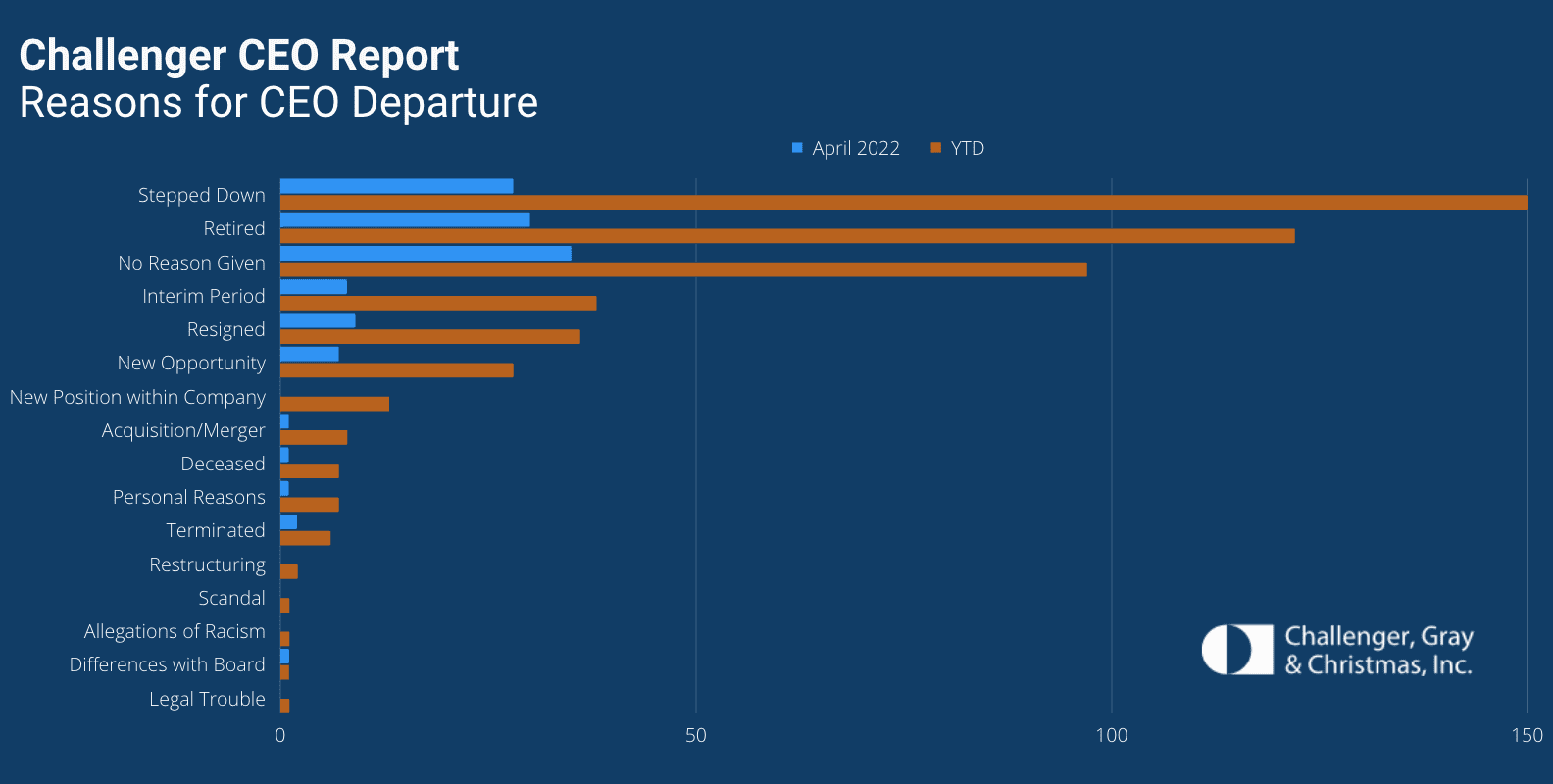

Dozens of hospital CEOs have resigned this year as a record number of chiefs across all industries have exited their roles, according to a May 18 Challenger, Gray & Christmas report.

Nearly 520 CEOs left their posts between Jan. 1 and the end of April, the highest total since the executive outplacement and coaching firm began tracking CEO changes in 2002. The total is up 18 percent from the 440 CEO exits announced in the same period of 2021.

Thirty-six hospital CEOs exited their roles in the first four months of this year. That’s up from the 20 hospital chiefs who resigned in the same period last year, according to the report.

CEOs are leaving their positions and businesses are making changes at the top for several reasons, Challenger, Gray & Christmas Senior Vice President Andrew Challenger said.

“Inflation, staffing shortages, and possible recession concerns are giving more cause for companies to reevaluate leadership,” Mr. Challenger said. “This, after years of companies trying to figure out the right formula to attract and retain talent and create a culture of inclusion, issues that often start at the top.”

Hospitals are experiencing significant increases in expenses for workforce, drugs and medical supplies

Introduction

For over two years since the outset of the COVID-19 pandemic, America’s hospitals and health systems have been on the front lines caring for patients, comforting families and protecting communities.

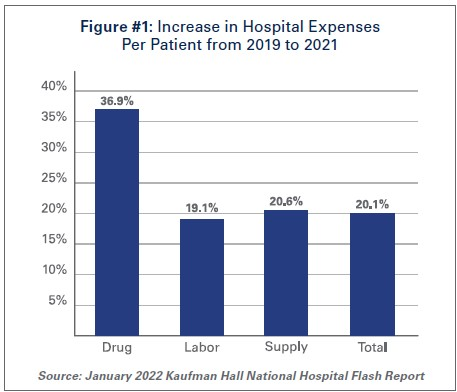

With over 80 million cases1, nearly 1 million deaths2, and over 4.6 million hospitalizations3, the pandemic has taken a significant toll on hospitals and health systems and placed enormous strain on the nation’s health care workforce. During this unprecedented public health crisis, hospitals and health systems have confronted many challenges, including historic volume and revenue losses, as well as skyrocketing expenses (See Figure #1).

Hospitals and health systems have been nimble in responding to surges in COVID-19 cases throughout the pandemic by expanding treatment capacity, hiring staff to meet demand, acquiring and maintaining adequate supplies and personal protective equipment (PPE) to protect patients and staff and ensuring that critical services and programs remain available to the patients and communities they serve. However, these and other factors have led to billions of dollars in losses over the last two years for hospitals, and over 33% of hospitals are operating on negative margins.

The most recent surges triggered by the delta and omicron variants have added even more pressure to hospitals. During these surges, hospitals saw the number of COVID-19 infected patients rise while other patient volumes fell, and patient acuity increased. This drove up expenses and added significant financial pressure for hospitals. Moreover, hospitals did not receive any government assistance through the COVID-19 Provider Relief Fund (PRF) to help mitigate rising expenses and lost revenues during the delta and omicron surges. This is despite the fact that more than half of COVID-19 hospitalizations have occurred since July 1, 2021, during these two most recent COVID-19 surges.

At the same time, patient acuity has increased, as measured by how long patients need to stay in the hospital. The increase in acuity is a result of the complexity of COVID-19 care, as well as treatment for patients who may have put off care during the pandemic. The average length of a patient stay increased 9.9% by the end of 2021 compared to pre-pandemic levels in 2019.4

As hospitals treat sicker patients requiring more intensive treatment, they also must ensure that sufficient staffing levels are available to care for these patients, and must acquire the necessary expensive drugs and medical supplies to provide high-quality care. As a result, overall hospital expenses have experienced considerable growth.

Data from Kaufman Hall, a consulting firm that tracks hospital financial metrics, shows that by the end of 2021, total hospital expenses were up 11% compared to pre-pandemic levels in 2019. Even after accounting for changes in volume that occurred during the pandemic, hospital expenses per patient increased significantly from pre-pandemic levels across every category. (See Figure #1)

The pandemic has strained hospitals’ and health systems’ finances. Many hospitals operate on razorthin margins, so even slight increases in expenses can have dramatic negative effects on operating margins, which can jeopardize their ability to care for patients. These expense increases have been more challenging to withstand in light of rising inflation and growth in input prices. In fact, despite modest growth in revenues compared to pre-pandemic levels, median hospital operating margins were down 3.8% by the end of 2021 compared to pre-pandemic levels, according to Kaufman Hall. Further exacerbating the problem for hospitals are Medicare sequestration cuts and payment increases that are well below increases in costs. For example, an analysis by PINC found that for fiscal year 2022, hospitals received a 2.4% increase in their Medicare inpatient payment rate, while hospital labor rates increased 6.5%.5

These levels of increased expenses and declines in operating margins are not sustainable. This report highlights key pressures currently facing hospitals and health systems, including:

Each of these issues separately presents significant challenges to the hospital field. Taken together, they represent conditions that would be potentially catastrophic for most organizations, institutions and industries. However, the fact that the nation’s hospitals and health systems continue to serve on the front lines of the ongoing pandemic is a testament to their resiliency and steadfast commitment to their mission to serve patients and communities around the country.

Hospitals and health systems are the cornerstones of their communities. Their patients depend on them for access to care 24 hours a day, seven days a week. Hospitals are often the largest employers in their community, and large purchasers of local services and goods. Additional support is needed to help ensure hospitals have the adequate resources to care for their communities.

I. Workforce and Contract Labor Expenses

The hospital workforce is central to the care process and often the largest expense for hospitals. It is no surprise then that even before the pandemic, labor costs — which include costs associated with recruiting and retaining employed staff, benefits and incentives — accounted for more than 50% of hospitals’ total expenses. Therefore, even a slight increase in these costs can have significant impacts on a hospital’s total expenses and operating margins.

As the pandemic has persisted for over two years, the toll on the health care workforce has been immense. A recent survey of health care workers found that approximately half of respondents felt “burned out” and nearly a quarter of respondents said they anticipated leaving the health care field.6

This has been mirrored by a significant and sustained decline in hospital employment, down approximately 100,000 employees from pre-pandemic levels.7 At the height of the omicron surge, approximately 1,400 hospitals or 30% of all U.S. hospitals reporting data to the government, indicated that they anticipated a critical staffing shortage within the week.8This high percentage of hospitals reporting a critical staffing shortage stayed relatively consistent throughout the delta and omicron surges.

The combination of employee burnout, fewer available staff, increased patient acuity and higher demand for care especially during the delta and omicron surges, has forced hospitals to turn to contract staffing firms to help address staffing shortages.

Though hospitals have long worked with contract staffing firms to bridge temporary gaps in staffing, the pandemic-driven-staffing-shortage has created an expanded reliance on contract staff, especially contract or travel registered nurses. Travel nurses are in particularly high demand because they serve a critical role in delivering care for both COVID-19 and non-COVID-19 patients and allow the hospital to meet the demand for care, especially during pandemic surges.

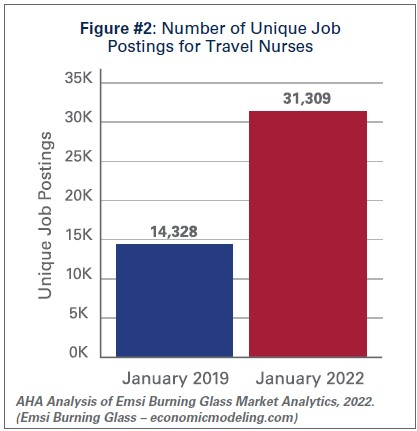

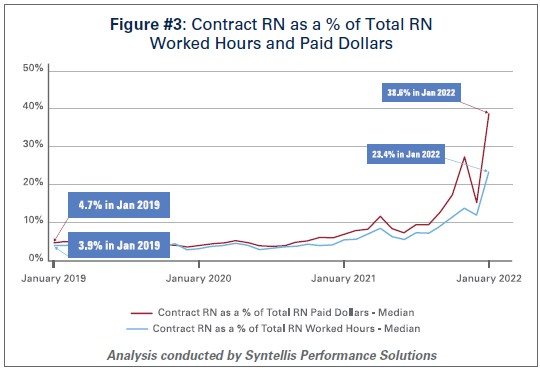

According to a survey by AMN Healthcare, one of the nation’s largest health care staffing agencies, 95% of health care facilities reported hiring nurse staff from contract labor firms during the pandemic.9Staffing firms have increased their recruitment of contract or travel nurses, illustrating the significant growth in their demand. According to data from EMSI/Burning Glass, there has been a nearly 120% increase in job postings for contract or travel nurses from pre-pandemic levels in January 2019 to January 2022. (See Figure #2)

Similarly, the hours worked by contract or travel nurses as a percentage of total hours worked by nurses in hospitals has grown from 3.9% in January 2019 to 23.4% in January 2022, according to data from Syntellis Performance Solutions. (See Figure #3) In fact, a quarter of hospitals have experienced nearly a third of their total nurse hours accounted for by contract or travel nurses.

As the share of contract travel nurse hours has grown significantly compared to before the pandemic, so too have the costs of employing travel nurses compared to pre-pandemic levels. In 2019, hospitals spent a median of 4.7% of their total nurse labor expenses for contract travel nurses, which skyrocketed to a median of 38.6% in January 2022. (See Figure #3) A quarter of hospitals — those who have had to rely disproportionately on contract travel nurses — saw their costs for contract travel nurses account for over 50% of their total nurse labor expenses. In fact, while contract travel nurses accounted for 23.4% of total nurse hours in January 2022, they accounted for nearly 40% of the labor expenses for nurses. (See Figure #3) This difference has grown considerably compared to pre-pandemic levels in 2019, suggesting that the exorbitant prices charged by staffing companies are a primary driver of higher labor expenses for hospitals.

Data from Syntellis Performance Solutions show a 213% increase in hourly rates charged to hospitals by staffing companies for travel nurses in January 2022 compared to pre-pandemic levels in January 2019. This is because staffing agencies have exploited the situation by increasing the hourly rates billed to hospitals for contract travel nurses more than the hourly rates they pay to travel nurses. This is effectively the “margin” retained by the staffing agencies. During pre-pandemic levels in 2019, the average “margin” retained by staffing agencies for travel nurses was about 15%. As of January 2022, the average “margin” has grown to an astounding 62%. (See Figure #4)

These high “margins” have fueled massive growth in the revenues and profits of health care staffing companies. Several staffing firms have reported significant growth in their revenues to as high as $1.1 billion in just the fourth quarter of 202110, tripling their revenues and net income compared to 2020 levels.11

The data indicate that the growth in labor expenses for hospitals and health systems was in large part due to the exorbitant rates charged by contract staffing firms. By the end of 2021, hospital labor expenses per patient were 36.9% higher than pre-pandemic levels, and increased to 57% at the height of the omicron surge in January 2022.12 A study looking at hospitals in New Jersey found that the increased labor expenses for contract staff amounted to $670 million in 2021 alone, which was more than triple what their hospitals spent in 2020.13High reliance on contract or travel staff prevents hospitals and health systems from investing those costs into their existing employees, leading to low morale and high turnover, which further exacerbates the challenges hospitals and health systems have been facing.

II. Drug Expenses

Prescription drug spending in the U.S. has grown significantly since the pandemic. In 2021, drug spending (including spending in both retail and non-retail settings) increased 7.7%14, which was on top of an increase of 4.9%15 in 2020. While some of this growth can be attributed to increased utilization as patient acuity increased during the pandemic, a significant driver has been the continued increase in prices of existing drugs as well as the introduction of new products at very high prices. A study by GoodRx found that in January 2022 alone, drug companies increased the price of about 810 brand and generic drugs that they reviewed by an average of 5.1%.16 These price increases followed massive price hikes for certain drugs often used in the hospital such as Hydromorphone (107%), Mitomycin (99%), and Vasopressin (97%).17 For another example, the drug manufacturer of Humira, one of the most popular brand drugs used to treat rheumatoid arthritis, increased the price of the drug by 21% between 2019 and 2021.18 A study by the Kaiser Family Foundation found that in Medicare Part B and D markets, half of all drugs in each market experienced price increases above the rate of inflation between 2019 and 2020 – in fact, a third of these drugs experienced price increases of greater than 7.5%.19 At the same time, according to a report by the Institute for Clinical and Economic Review (ICER), eight drugs with unsupported U.S. drug price increases between 2019 and 2020 alone accounted for an additional $1.67 billion in drug spending, further illustrating that drug companies’ decisions to raise the prices of their drugs are simply an unsustainable practice.20

As hospitals have worked to treat sicker patients during the pandemic, they have been forced to contend with sky-high prices for drugs, many of which are critical and lifesaving for their patients. For example, in 2020, 16 of the top 25 drugs by spending in Medicare Part B (hospital outpatient settings) had price increases greater than inflation — two of the top three drugs, Keytruda and Prolia — experienced price increases of 3.3% and 4.1%, respectively.21

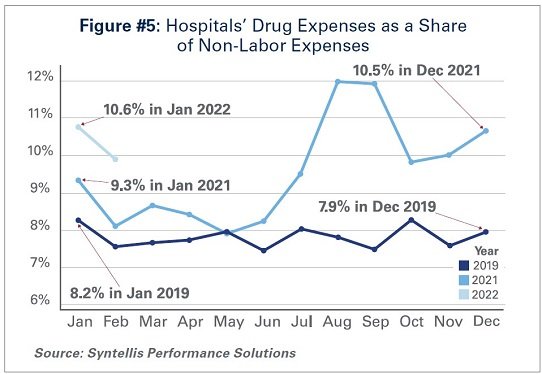

As a result of these price increases, hospital drug expenses have skyrocketed. By the end of 2021, total drug expenses were 28.2% higher than pre-pandemic levels.22 When taken as a share of all non-labor expenses, drug expenses have grown from approximately 8.2% in January 2019, to 9.3% in January 2021, and to 10.6% in January 2022. (See Figure #5) Even when considering changes in volume during the pandemic, drug expenses per patient compared to pre-pandemic levels in 2019 saw significant increases, with a 36.9% increase through 2021.

While continued drug price increases by drug companies have been a major driver of the growth in overall hospital drug expenses, there also are other important driving factors to consider:

Drug Treatments for COVID-19 Patients:Remdesivir, one of the primary drugs used to treat COVID-19 patients in the hospital, has become the top spend drug for most hospitals since the pandemic. This drug alone accounted for over $1 billion in sales in the fourth quarter of 2021.23 Priced at an average of $3,12024, Remdesivir’s cost was initially covered by the federal government. However, hospitals must now purchase the drug directly.

Limitation of 340B Contract Pharmacies: The 340B program allows eligible providers, including hospitals that treat many low-income patients or treat certain patient populations like children and cancer patients, to buy certain outpatient drugs at discounted prices and use those savings to provide more comprehensive services to the patients and communities they serve. Since July 2020, several of the largest drug manufacturers have denied 340B pricing to eligible hospitals through pharmacies with whom they contract, despite calls from the Department of Health and Human Services that such actions are illegal. Because of these actions, many 340B hospitals, especially rural hospitals who disproportionately rely on contract pharmacies to ensure access to drugs for their patients, have lost millions in 340B drug savings.25 In addition, these manufacturers have required claim-level data submissions as a condition of receiving 340B discounts, which has increased costs to deliver the data as well as staff time and expense to manage that process. The loss of 340B savings coupled with increased burden of providing detailed data to drug companies have contributed to increasing drug expenses.

Health Plans’/Pharmacy Benefit Managers’ (PBMs’) “White Bagging” Policies: Health plans and PBMs have engaged in a tactic that steers hospital patients to third-party specialty pharmacies to acquire medication necessary for clinician-administered treatments, known as “white-bagging.” This practice disallows the hospital from procuring and managing the handling of a drug — typically drugs that are infused or injected requiring a clinician to administer in a hospital or clinic setting — used in patient care. These policies not only create serious patient safety concerns, but create delays and risks in patient care; add to administration, storage and handling costs; and create important liability issues for hospitals.

Taken together, these factors increase both drug expenses and overall hospital expenses.

III. Medical Supply and PPE Expenses

The U.S., like most countries in the world, relies on global supply chains for goods and services. This is especially true for medical supplies used at hospitals and other health care settings. Everything from the masks and gloves worn by staff to medical devices used in patient care come from a large network of global suppliers. Prior to the global pandemic, hospitals had established relationships with distributors and other vendors in the global health care supply chain to deliver goods as necessitated by demand. After the pandemic hit, many factories, distributors and other vendors shut down their operations, leaving hospitals, which were on the front lines facing surging demand, to fend for themselves. In fact, supply chain disruptions across industries, including health care, increased by 67% in 2020 alone.26

As a result, hospitals turned to local suppliers and non-traditional suppliers, often paying significantly higher rates than they did prior to the pandemic. Between fall 2020 and early 2022 costs for energy, resins, cotton and most metals surged in excess of 30%; these all are critical elements in the manufacturing of medical supplies and devices used every day in hospitals.27 As COVID-19 cases surged, demand for hospital PPE, such as N95 masks, gloves, eye protection and surgical gowns, increased dramatically causing hospitals to invest in acquiring and maintaining reserves of these supplies. Further, downstream effects from other global events such as the war in Ukraine and the energy crisis in China, as well as domestic issues, such as labor shortages and rising fuel and transportation costs, have all contributed to drive up even higher overall medical supply expenses for hospitals in the U.S.28 For instance, according to the Health Industry Distributors Association, transportation times for medical supplies are 440% longer than pre-pandemic times resulting in massive delays.29

Compared to 2019 levels, supply expenses for hospitals were up 15.9%30 through the end of 2021. When focusing on hospital departments involved most directly in care for COVID-19 patients − primarily hospital intensive care units (ICUs) and respiratory care departments − the increase in expenses is significantly higher. Medical supply expenses in ICUs and respiratory care departments increased 31.5% and 22.3%, respectively. Further, accounting for changes in volume during surge and non-surge periods of the pandemic, medical supply expenses per patient in ICUs and respiratory care departments were 31.8% and 25.9% higher, respectively. (See Figure #6) These numbers help illustrate the magnitude of the impact that increases in supply costs have had on hospital finances during the pandemic.

IV. Impact of Rising Inflation

Higher economy-wide costs have serious implications for hospitals and health systems, increasing the pressures of higher labor, supply, and acquisition costs; and potentially lower consumer demand. Inflation is defined as the general increase in prices and the decrease in purchasing power. It is measured by the Consumer Price Index (CPI-U). In April 2021, the Bureau of Labor Statistics (BLS) reported that the CPI-U had the largest 12-month increase since September 2008. The CPI-U hit 40-year highs in February 2022.31 Overall, consumer prices rose by a historic 8.5% on an annualized basis in March 2022 alone.32

As inflation measured by consumer prices is at record highs, below are key considerations on the potential impact of higher general inflation on hospital prices:

Labor Costs and Retention: Labor costs represent a significant portion of hospital costs (typically more than 50% of hospital expenses are related to labor costs). As the cost-of-living increases, employees generally demand higher wages/total compensation packages to offset those costs. This is especially true in the health care sector, where labor demands are already high, and labor supply is low.

Supply Chain Costs: Medical supplies account for approximately 20% of hospital expenses, on average. As input/raw good costs increase due to general inflation, hospital supplies and medical device costs increase as well. Furthermore, shortages of raw materials, including those used to manufacture drugs, could stress supply chains (i.e., medical supply shortages), which may result in changes in care patterns and add further burden on staff to implement work arounds.

Capital Investment Costs: Capital investments also may be strained, especially as hospitals have already invested heavily in expanding capacity to treat patients during the pandemic (e.g., constructing spaces for testing and isolation of COVID-19 patients). One of the areas that has seen the largest increase in prices/shortages is building materials (e.g., lumber). Additionally, a historically large increase in inflation has resulted in increases in interest rates, which may hamper borrowing options and add to overall costs.

Consumer Demand: Higher inflation also may result in decreases in demand for health care services, specifically if inflation exceeds wage growth. Specifically, higher costs for necessities (food, transportation, etc.) could push down demand for health care services and, in turn, dampen hospital volumes and revenues in the long run.

Health care and hospital prices are not driving recent overall inflation increases. The BLS has cited increases in the indices for gasoline, shelter and food as the largest contributors to the seasonally adjusted all items increase. The CPI-U increased 0.8% in February on a seasonally adjusted basis, whereas the medical care index rose 0.2% in February. The index for prescription drugs rose 0.3%, but the hospital index for hospital services declined 0.1%.33

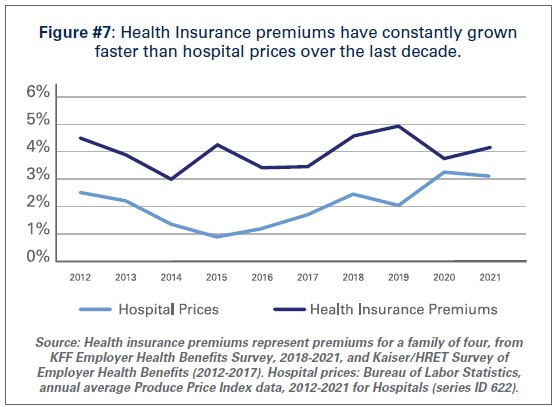

This is consistent with pre-pandemic trends. Despite persistent cost pressures, hospital prices have seen consistently modest growth in recent years. According to BLS data, hospital prices have grown an average 2.1% per year over the last decade, about half the average annual increase in health insurance premiums. (See Figure #7) More recently, hospital prices have grown much more slowly than the overall rate of inflation. In the 12 months ending in February 2022, hospital prices increased 2.1%. In fact, even when excluding the artificially low rates paid to hospitals by Medicare and Medicaid, average annual price growth has still been below 3% in recent years.34

Conclusion

While we hope that our nation is rounding the corner in the battle against COVID-19, it is clear that the pandemic is not over. During the week of April 11, there have been an average of over 33,000 cases per day35 and reports suggest that a new subvariant of the virus (Omicron BA.2) is now the dominant strain in the U.S.36As a result, the challenges hospitals and health systems are currently facing are bound to last much longer.

As COVID-19 infections and hospitalizations are decreasing in some parts of the U.S. and increasing in others, hospitals and health systems continue to care for COVID-19 and non-COVID-19 patients. With additional surges potentially on the horizon, the massive growth in expenses is unsustainable. Most of the nation’s hospitals were operating on razor thin margins prior to the pandemic; and now, many of these hospitals are in an even more precarious financial situation. Regardless of potential new surges of COVID-19, hospitals and health systems continue to face workforce retention and recruitment challenges, supply chain disruptions and exorbitant expenses as outlined in this report.

Hospitals appreciate the support and resources that Congress has provided throughout the pandemic; however, additional support is needed now to keep hospitals strong so they can continue to provide care to patients and communities.

It was a winter of surging job creation. Employers created jobs on a mass scale, Americans returned to the workforce, and the labor market shrugged off the Omicron variant and its broader pandemic funk.

That’s the takeaway from the February jobs report, which showed employers added 678,000 jobs last month. December and January job growth was better than previously thought, and the unemployment rate fell to 3.8%.

Why it matters: Yes, inflation is high as prices rose 7.5% over the last year as of January, and could rise higher as disruptions from the Ukraine war ripple through the economy.

But rising prices are coming amid an astonishingly rapid jobs boom.

Between the lines: The report shows the pandemic impact is fading. But some analysts warn not to expect this level of gains to continue as the crisis in Ukraine cuts into growth.

“The improvement in the American labor market is now very much a rearview mirror phenomenon,” economist Joe Brusuelas wrote in a research note.

One big surprise: Wage growth was essentially nonexistent, with average hourly earnings rising only a penny to $31.58.

That may reflect the nature of the jobs being added — disproportionately in the low-paying leisure and hospitality sector.

That is good news for those worried that rising wages and prices will drive further inflation. It is worse news for workers, whose average pay gain of 5.1% over the last year is far below inflation.

The share of adults in the labor force — which includes those looking for work — ticked up, as did the share of the population that’s actually employed. That suggests the robust job growth is pulling people back into the workforce, if gradually.

The labor force participation rate was 62.3% in February, more than a percentage point below its level two years ago, before the pandemic.

State of play: The Federal Reserve is set to begin an interest rate hiking campaign on March 16, amid high inflation and new geopolitical uncertainty from the Ukraine war. The new numbers are unlikely to change that one way or the other.

Many Americans, even those who don’t pay much attention to investing and the markets, know the name Warren Buffett.

Buffett, of course, is the billionaire philanthropist who created one of the greatest investment fortunes in history. Far fewer, however, know the name of his longtime business partner Charlie Munger.

And that’s a shame, because Munger is at least half the brains behind Berkshire Hathaway BRK.ABRK.B, the holding company he runs with Buffett and which manages billions and billions of investor dollars.

Munger turned 98 on Jan. 1. To celebrate his wit and market wisdom, here is a collection of quips from various interviews and question-and-answer sessions over the years.

On business education

Those of you who are about to enter business school, or who are there, I recommend you learn to do it our way. But at least until you’re out of school you have to pretend to do it their way.

On common sense

If people weren’t so often wrong, we wouldn’t be so rich.

On company earnings

Yeah, I think you would understand any presentation using the word EBITDA, if every time you saw that word you just substituted the phrase “bullsh** earnings.”

On a changing economy

So no, I’m optimistic about life. If I can be optimistic when I’m nearly dead, surely the rest of you can handle a little inflation.

On public spending

Everybody wants fiscal virtue but not quite yet. They’re like that guy who felt that way about sex. He was willing to give it up but not quite yet.

On legacy

Well, you don’t want to be like the motion picture executive in California. They said the funeral was so large because everybody wanted to make sure he was dead.

On stock buybacks

I think some people just buy it to keep the stock up. And that, of course, is insane. And immoral. But apart from that, it’s fine.

On marriage

Warren: Charlie is big on lowering expectations.

Munger: Absolutely. That’s the way I got married. My wife lowered her expectations.

On the purpose of money

Sure, there are a lot of things in life way more important than wealth. All that said…some people do get confused. I play golf with a man. He says: “What good is health? You can’t buy money with it.”

On money managers

The general system for money management requires people to pretend that they can do something that they can’t do, and to pretend to like it when they really don’t. I think that’s a terrible way to spend your life, but it’s very well paid.

On systematic investing

Well, I can’t give you a formulaic approach, because I don’t use one. If you want a formula you should go back to graduate school. They’ll give you lots of formulas that won’t work.

On human nature

As Samuel Johnson said, famously: “I can give you an argument, but I can’t give you an understanding.”

On financial innovation

It’s perfectly obvious, at least to me, that to say that derivative accounting in America is a sewer. is an insult to sewage.

On business competition

Competency is a relative concept. And what a lot of us needed to get ahead was to compete against idiots. And luckily there’s a large supply.

On cryptocurrency

I think the people who are professional traders that go into trading cryptocurrencies, it’s just disgusting. It’s like somebody else is trading turds and you decide, “I can’t be left out.”

On investment bankers

Once I asked a man who just left a large investment bank, and I said, “How does your firm make its money?” He said, “Off the top, off the bottom, off both sides, and in the middle.”

The boom in global mergers and acquisitions in 2021 will surge into 2022, fueled by abundant investment capital, historically low interest rates and a rebound in global economic growth, according to a survey of 345 corporate dealmakers in the U.S. by KPMG.

“Based on the volume of new pitches in November and December — transactions that would come to market in Q1 and Q2 of 2022 — there are no signs of a slowing deal market,” according to Philip Isom, global head of M&A at KPMG. While facing high valuations, “most investors have limited time horizons to invest in, so they may be willing to reach further on price than they have historically.”

More than 80% of the survey respondents across several industries expect total M&A valuations to rise further next year, with about one out of every three predicting at least a 10% increase, KPMG said. Dealmakers said transaction levels will remain robust because companies “need to remain on the offense with the competition” and “feel pressure from investors to raise their own valuations.”

Dive Insight:

Worldwide deal value from January until mid-November this year hit $5.1 trillion, the highest level since 2015 and a 34% gain compared with all of 2020, KPMG said. U.S. transactions rose to $2.9 trillion, or 55% more than during all of last year.

M&A has soared in 2021 as the economy recovered from a pandemic shock, record monetary and fiscal stimulus pumped up liquidity and many companies sought through acquisitions to regain their footing after months of lockdowns and persistent supply chain disruptions.

A widespread labor shortage will probably push up dealmaking next year. One-third of survey respondents said they want to use M&A to acquire talent, KPMG said.

Also, companies increasingly use acquisitions to change their business or operating models, KPMG said, noting that industrial and financial services companies buy companies that help speed their digital transformation.

“The aim is to increase efficiencies and contribute to having more agile workforces,” according to Carole Streicher, KPMG’s deal advisory and strategy service group leader in the U.S.

Private equity firms will continue to push up the volume and value of M&A next year, after increasing their involvement in transaction value by more than 55% so far in 2021, KPMG said. PE firms have pursued deals this year in part because of the prospect of an increase in corporate capital gains taxes.

Growing support for sustainability among investors, regulators and other stakeholders may prompt M&A, “as businesses look at their ecological footprint and consider purchasing, rationalizing or divesting assets,” KPMG said. Investors are likely to consider sustainable businesses more adaptable to market shifts.

Finally, concerns about the potential for rising borrowing costs may prompt dealmakers who rely on debt financing to speed up acquisition plans. Federal Reserve Chair Jerome Powell late last month said policymakers at their two-day meeting beginning Tuesday will likely consider speeding up the withdrawal of accommodation.

Dealmakers face some headwinds. Democrats in the Senate have yet to muster enough support for a roughly $2 trillion social policy bill that would help sustain economic growth. Meanwhile, the outbreak of the omicron variant of COVID-19 has highlighted the fragility of financial markets and the economy to any setbacks in curbing the pandemic.

Survey respondents identified several factors that will influence dealmaking next year, with 61% underscoring high valuations, 56% pointing to liquidity and other economic considerations, and 55% noting intense competition for a limited number of highly valued acquisition targets, KPMG said.

Still, only 7% of the survey respondents said they expect deal volumes to decline in their industries next year.

Survey respondents work at companies in industries ranging from media and financial services to energy and technology, with 194 of them CFOs, CEOs or other C-suite executives.