From time to time the blogging process stimulates a conversation between the author and the audience. This type of conversation occurred after the publication of my recent blog, “The Hospital Makeover—Part 2.” This blog focused entirely on the current problems, financial and otherwise, of the hospital physician employment model. I received responses from CEOs and other C-suite executives and those responses are very much worth adding to the physician employment conversation. Hospital executives have obviously given the physician employment strategy considerable thought.

One CEO noted that, looking back from a business perspective, physician employment was not actually a doctor retention strategy but, in the long run, more of a customer acquisition and customer loyalty strategy.

The tactic was to employ the physician and draw his or her patients into the hospital ecosystem. And by extension, if the patient was loyal to the doctor, then the patient would also be loyal to the hospital. Perhaps this approach was once legitimate but new access models, consumerism, and the healthcare preferences of at least two generations of patients have challenged the strategic validity of this tactic.

The struggle now—and the financial numbers validate that struggle—is that the physician employment model has become extraordinarily expensive and, from observation, does not scale.

Therefore, the relevant business question becomes what are the most efficient and durable customer acquisition and loyalty models now available to hospitals and health systems?

A few more physician employment observations worth sharing:

Primary Care. The physician employment model has generally created a one-size-fits all view of primary care. Consumers, however, want choice. They want 32 flavors, not just vanilla. Alternative primary care models need to match up to fast-changing consumer preferences.

Where Physician Employment Works. In general, the employment model has worked where doctor “shift work” is involved. This includes facility-based specialists such as emergency physicians, anesthesiologists, and hospitalists.

Chronic Care Management. Traditional physician employment models that drive toward doctor-led physical clinics have generally not led to the improved monitoring and treatment of chronic care patient problems. As a result, the chronic care space will likely see significant disruption from virtual and in-home tools.

All in all, the four very smart observations detailed above continue the hospital physician employment conversation. Please feel free to add your thoughts on this or on other topics of hospital management which may be of interest to you. Thanks for reading.

A detailed report, published by a group of organizations including the American Antitrust Institute, provides one of the highest-quality examinations of the growth of private equity (PE)-backed physician practices, and the impact of this growth on market competition and healthcare prices.

From 2012 to 2021, the annual number of practice acquisitions by private equity groups increased six-fold, and the number of metropolitan areas in which a single PE-backed practice held over 30 percent market share rose to cover over one quarter of the country. (Check out figure 3B at the bottom of page 20 in the report to see if you live in one of those markets.)

The study also found an association between PE practice acquisitions and higher healthcare prices and per-patient expenditures. In highly concentrated markets, certain specialties, like gastroenterology, saw prices rise by as much as 18 percent.

The Gist: As the report highlights, one of the greatest barriers to assessing PE’s impact on physician practices is the lack of transparency around acquisitions and ownership structures. This analysis brings us closer to understanding the scope of the issue, and makes a strong case for regulatory and legislative intervention.

Recent proposed changes to federal premerger disclosure requirements offer a good start, but many practice acquisitions are still too small to flag review, and slowing future acquisitions will do little to unwind the market concentration already emerging.

PE is also not the sole actor contributing to healthcare consolidation, and proposed remedies may target the activities of payers and health systems considered anti-competitive as well.

That’s the amount you arrive at if you multiply the number of physicians employed by hospitals and health systems (approximately 341,200 as of January 2022, according to data from the Physicians Advocacy Institute and Avalere) by the median $306,362 subsidy—or loss—reported in our Q1 2023 Physician Flash Report.

Subsidizing physician employment has been around for a long time and such subsidies were historically justified as a loss leader for improved clinical services, the potential for increased market share, and the strengthening of traditionally profitable services.

But I am pretty sure the industry did not have $104 billion in losses in mind when the physician employment model first became a key strategic element in the hospital operating model. However, the upward reset in expenses brought on by the pandemic and post-pandemic inflation has made many downstream hospital services that historically operated at a profit now operate at breakeven or even at a loss. The loss leader physician employment model obviously no longer works when it mostly leads to more losses.

This model is clearly broken and in demand of a near-term fix. Perhaps the critical question then is how to begin? How to reconsider physician employment within the hospital operating plan?

Out of the box, rethink the physician productivity model. Our most recent Physician Flash Report data shows that for surgical specialties, there was a median $77 net patient revenue per provider wRVU. For the same specialties, there was a median $80 provider paid compensation per provider wRVU. In other words, before any other expenses are factored in, these specialties are losing $3 per wRVU on paid compensation alone. Getting providers to produce more wRVUs only makes the loss bigger.

It’s the classic business school 101 problem.

If a factory is losing $5 on every widget it produces, the answer is not to produce more widgets. Rather, expenses need to come down, whether that is through a readjustment of compensation, new compensation models that reward efficiency, or the more effective use of advanced practice providers.

Second, a number of hospital CEOs have suggested to me that the current employed physician model is quite past its prime. That model was built for a system of care that included generally higher revenues, more inpatient care, and a greater proportion of surgical vs. medical admissions. But overall, these trends were changing and then were accelerated by the Covid pandemic. Inpatient revenue has been flat to down. More clinical work continues to shift to the outpatient setting and, at least for the time being, medical admissions have been more prominent than before the pandemic.

Taking all this into account suggests that in many places the employed physician organizational and operating model is entirely out of balance. One would offer the calculated guess that there are too many coaches on the team and not enough players on the field. This administrative overhead was seemingly justified in a different loss leader environment but now it is a major contributor to that $104 billion industry-wide loss previously calculated.

Finally, perhaps the very idea of physician employment needs to be rethought.

My colleagues Matthew Bates and John Anderson have commented that the “owner” model is more appealing to physicians who remain independent then the “renter” model. The current employment model offers physicians stability of practice and income but appears to come at the cost of both a loss of enthusiasm and lost entrepreneurship. The massive losses currently experienced strongly suggest that new models are essential to reclaim physician interest and establish physician incentives that result in lower practice expenses, higher practice revenues, and steadily reduced overall subsidies.

Please see this blog as an extension of my last blog, “America’s Hospitals Need a Makeover.”It should be obvious that by analogy we are not talking about a coat of paint here or even new appliances in the kitchen.

The financial performance of America’s hospitals has exposed real structural flaws in the healthcare house. A makeover of this magnitude is going to require a few prerequisites:

Don’t start designing the renovation unless you know specifically where profitability has changed within your service lines and by explicitly how much. Right now is the time to know how big the problem is, where those problems are located, and what is the total magnitude of the fix.

The Board must be brought into the discussion of the nature of the physician employment problem and the depth of its proposed solutions. Physicians are not just “any employees.” They are often the engine that runs the hospital and must be afforded a level of communication that is equal to the size of the financial problem. All of this will demand the Board’s knowledge and participation as solutions to the physician employment dilemma are proposed, considered, and eventually acted upon.

The basic rule of home renovation applies here as well: the longer the fix to this problem is delayed the harder and more expensive the project becomes. The losses set out here certainly suggest that physician employment is a significant contributing factor to hospitals’ current financial problems overall. It would be an understatement to say that the time to get after all of this is right now.

I have been both a frontline officer and a staff officer at a health system. I started a solo practice in 1977 and cared for my rheumatology, internal medicine and geriatrics patients in inpatient and outpatient settings. After 23 years in my solo practice, I served 18 years as President and CEO of a profitable, CMS 5-star, 715-bed, two-hospital healthcare system.

From 2015 to 2020, our health system team added 0.6 years of healthy life expectancy for 400,000 folks across the socioeconomic spectrum. We simultaneously decreased healthcare costs 54% for 6,000 colleagues and family members. With our mentoring, four other large, self-insured organizations enjoyed similar measurable results. We wanted to put our healthcare system out of business. Who wants to spend a night in a hospital?

During the frontline part of my career, I had the privilege of “Being in the Room Where It Happens,” be it the examination room at the start of a patient encounter, or at the end of life providing comfort and consoling family. Subsequently, I sat at the head of the table, responsible for most of the hospital care in Southwest Florida. [1]

Many folks commenting on healthcare have never touched a patient nor led a large system. Outside consultants, no matter how competent, have vicarious experience that creates a different perspective.

At this point in my career, I have the luxury of promoting what I believe is in the best interests of patients — prevention and quality outcomes. Keeping folks healthy and changing the healthcare industry’s focus from a “repair shop” mentality to a “prevention program” will save the industry and country from bankruptcy. Avoiding well-meaning but inadvertent suboptimal care by restructuring healthcare delivery avoids misery and saves lives.

RESPONDING TO AN ATTACK

Preemptive reinvention is much wiser than responding to an attack. Unfortunately, few industries embrace prevention. The entire healthcare industry, including health systems, physicians, non-physician caregivers, device manufacturers, pharmaceutical firms, and medical insurers, is stressed because most are experiencing serious profit margin squeeze. Simultaneously the public has ongoing concerns about healthcare costs. While some medical insurance companies enjoyed lavish profits during COVID, most of the industry suffered. Examples abound, and Paul Keckley, considered a dean among long-time observers of the medical field, recently highlighted some striking year-end observations for 2022. [2]

Recent Siege Examples

Transparency is generally good but can and has led to tarnishing the noble profession of caring for others. Namely, once a sector starts bleeding, others come along, exacerbating the exsanguination. Current literature is full of unflattering public articles that seem to self-perpetuate, and I’ve highlighted standout samples below.

The Federal Government is the largest spender in the healthcare industry and therefore the most influential. Not surprisingly, congressional lobbying was intense during the last two weeks of 2022 in a partially successful effort to ameliorate spending cuts for Medicare payments for physicians and hospitals. Lobbying spend by Big Pharma, Blue Cross/Blue Shield, American Hospital Association, and American Medical Association are all in the top ten spenders again. [3, 4, 5] These organizations aren’t lobbying for prevention, they’re lobbying to keep the status quo.

Concern about consistent quality should always be top of mind. “Diagnostic Errors in the Emergency Department: A Systematic Review,” shared by the Agency for Healthcare Research and Quality, compiled 279 studies showing a nearly 6% error rate for the 130 million people who visit an ED yearly. Stroke, heart attack, aortic aneurysm, spinal cord injury, and venous thromboembolism were the most common harms. The defense of diagnostic errors in emergency situations is deemed of secondary importance to stabilizing the patient for subsequent diagnosing. Keeping patients alive trumps everything. Commonly, patient ED presentations are not clear-cut with both false positive and negative findings. Retrospectively, what was obscure can become obvious. [6, 7]

Spending mirrors motivations. The Wall Street Journal article “Many Hospitals Get Big Drug Discounts. That Doesn’t Mean Markdowns for Patients” lays out how the savings from a decades-old federal program that offers big drug discounts to hospitals generally stay with the hospitals. Hospitals can chose to sell the prescriptions to patients and their insurers for much more than the discounted price. Originally the legislation was designed for resource-challenged communities, but now some hospitals in these programs are profiting from wealthy folks paying normal prices and the hospitals keeping the difference. [8]

“Hundreds of Hospitals Sue Patients or Threaten Their Credit, a KHN Investigation Finds. Does Yours?” Medical debt is a large and growing problem for both patients and providers. Healthcare systems employ collection agencies that typically assess and screen a patient’s ability to pay. If the credit agency determines a patient has resources and has avoided paying his/her debt, the health system send those bills to a collection agency. Most often legitimately impoverished folks are left alone, but about two-thirds of patients who could pay but lack adequate medical insurance face lawsuits and other legal actions attempting to collect payment including garnishing wages or placing liens on property. [9]

“Hospital Monopolies Are Destroying Health Care Value,” written by Rep. Victoria Spartz (R-Ind.) in The Hill, includes a statement attributed to Adam Smith’s The Wealth of Nations, “that the law which facilitates consolidation ends in a conspiracy against the public to raise prices.” The country has seen over 1,500 hospital mergers in the past twenty years — an example of horizontal consolidation. Hospitals also consolidate vertically by acquiring physician practices. As of January 2022, 74 percent of physicians work directly for hospitals, healthcare systems, other physicians, or corporate entities, causing not only the loss of independent physicians but also tighter control of pricing and financial issues. [10] The healthcare industry is an attractive target to examine. Everyone has had meaningful healthcare experiences, many have had expensive and impactful experiences. Although patients do not typically understand the complexity of providing a diagnosis, treatment, and prognosis, the care receiver may compare the experience to less-complex interactions outside healthcare that are customer centric and more satisfying.

PROFIT-MARGIN SQUEEZE

Both nonprofit and for-profit hospitals must publish financial statements. Three major bond rating agencies (Fitch Ratings, Moody’s Investors Service, and S & P Global Ratings) and other respected observers like KaufmanHall, collate, review, and analyze this publicly available information and rate health systems’ financial stability.

One measure of healthcare system’s financial strength is operating margin, the amount of profit or loss from caring for patients. In January of 2023 the median, or middle value, of hospital operating margin index was -1.0%, which is an improvement from January 2022 but still lags 2021 and 2020.

Erik Swanson, SVP at KaufmanHall, says 2022,

“Is shaping up to be one of the worst financial years on record for hospitals. Expense pressures — particularly with the cost of labor — outpaced revenues and drove poor performance. While emergency department visits and operating room minutes increased slightly, hospitals struggled to discharge patients due to internal staffing shortages and shortages at post-acute facilities,” [11]

Another force exacerbating health system finance is the competent, if relatively new retailers (CVS, Walmart, Walgreens, and others) that provide routine outpatient care affordably. Ninety percent of Americans live within ten miles of a Walmart and 50% visit weekly. CVS and Walgreens enjoy similar penetration. Profit-margin squeeze, combined with new convenient options to obtain routine care locally, will continue disrupting legacy healthcare systems.

Providers generate profits when patients access care. Additionally, “easy” profitable outpatient care can and has switched to telemedicine. Kaiser-Permanente (KP), even before the pandemic, provided about 50% of the system’s care through virtual visits. Insurance companies profit when services are provided efficiently or when members don’t use services. KP has the enviable position of being both the provider and payor for their members. The balance between KP’s insurance company and provider company favors efficient use of limited resources. Since COVID, 80% of all KP’s visits are virtual, a fact that decreases overhead, resulting in improved profit margins. [12]

On the other hand, KP does feel the profit-margin squeeze because labor costs have risen. To avoid a nurse labor strike, KP gave 21,000 nurses and nurse practitioners a 22.5% raise over four years. KP’s most recent quarter reported a net loss of $1.5B, possibly due to increased overhead. [13]

The public, governmental agencies, and some healthcare leaders are searching for a more efficient system with better outcomes

at a lower cost. Our nation cannot continue to spend the most money of any developed nation and have the worst outcomes. In a globally competitive world, limited resources must go to effective healthcare, balanced with education, infrastructure, the environment, and other societal needs. A new healthcare model could satisfy all these desires and needs.

Even iconic giants are starting to feel the pain of recent annual losses in the billions. Ascension Health, Cleveland Clinic, Jefferson Health, Massachusetts General Hospital, ProMedica, Providence, UPMC, and many others have gone from stable and sustainable to stressed and uncertain. Mayo Clinic had been a notable exception, but recently even this esteemed system’s profit dropped by more than 50% in 2022 with higher wage and supply costs up, according to this Modern Healthcare summary. [14]

The alarming point is even the big multigenerational health system leaders who believed they had fortress balance sheets are struggling. Those systems with decades of financial success and esteemed reputations are in jeopardy. Changing leadership doesn’t change the new environment.

Nonprofit healthcare systems’ income typically comes from three sources — operations, namely caring for patients in ways that are now evolving as noted above; investments, which are inherently risky evidence by this past year’s record losses; and philanthropy, which remains fickle particularly when other investment returns disappoint potential donors. For-profit healthcare systems don’t have the luxury of philanthropic support but typically are more efficient with scale and scope.

The most stable and predictable source of revenue in the past was from patient care. As the healthcare industry’s cost to society continues to increase above 20% of the GDP, most medically self-insured employers and other payors will search for efficiencies. Like it or not, persistently negative profit margins will transform healthcare.

Demand for nurses, physicians, and support folks is increasing, with many shortages looming near term. Labor costs and burnout have become pressing stresses, but more efficient delivery of care and better tools can ameliorate the stress somewhat. If structural process and technology tools can improve productivity per employee, the long-term supply of clinicians may keep up. Additionally, a decreased demand for care resulting from an effective prevention strategy also could help.

Most other successful industries work hard to produce products or services with fewer people. Remember what the industrial revolution did for America by increasing the productivity of each person in the early 1900s. Thereafter, manufacturing needed fewer employees.

PATIENTS’ NEEDS AND DESIRES

Patients want to live a long, happy and healthy life. The best way to do this is to avoid illness, which patients can do with prevention because 80% of disease is self-inflicted. When prevention fails, or the 20% of unstoppable episodic illness kicks in, patients should seek the best care.

The choice of the “best care” should not necessarily rest just on convenience but rather objective outcomes. Closest to home may be important for take-out food, but not healthcare.

Care typically can be divided into three categories — acute, urgent, and elective. Common examples of acute care include childbirth, heart attack, stroke, major trauma, overdoses, ruptured major blood vessel, and similar immediate, life-threatening conditions. Urgent intervention examples include an acute abdomen, gall bladder inflammation, appendicitis, severe undiagnosed pain and other conditions that typically have positive outcomes even with a modest delay of a few hours.

Most every other condition can be cared for in an appropriate timeframe that allows for a car trip of a few hours. These illnesses can range in severity from benign that typically resolve on their own to serious, which are life-threatening if left undiagnosed and untreated. Musculoskeletal aches are benign while cancer is life-threatening if not identified and treated.

Getting the right diagnosis and treatment for both benign and malignant conditions is crucial but we’re not even near perfect for either. That’s unsettling.

In a 2017 study,

“Mayo Clinic reports that as many as 88 percent of those patients [who travel to Mayo] go home [after getting a second opinion] with a new or refined diagnosis — changing their care plan and potentially their lives. Conversely, only 12 percent receive confirmation that the original diagnosis was complete and correct. In 21 percent of the cases, the diagnosis was completely changed; and 66 percent of patients received a refined or redefined diagnosis. There were no significant differences between provider types [physician and non-physician caregivers].” [15]

The frequency of significant mis- or refined-diagnosis and treatment should send chills up your spine. With healthcare we are not talking about trivial concerns like a bad meal at a restaurant, we are discussing life-threatening risks. Making an initial, correct first decision has a tremendous influence on your outcome.

Sleeping in your own bed is nice but secondary to obtaining the best outcome possible, even if car or plane travel are necessary. For urgent and elective diagnosis/treatment, travel may be a

good option. Acute illness usually doesn’t permit a few hours of grace, although a surprising number of stroke and heart attack victims delay treatment through denial or overnight timing. But even most of these delayed, recognized illnesses usually survive. And urgent and elective care gives the patient the luxury of some time to get to a location that delivers proven, objective outcomes, not necessarily the one closest to home.

Measuring quality in healthcare has traditionally been difficult for the average patient. Roadside billboards, commercials, displays at major sporting events, fancy logos, name changes and image building campaigns do not relate to quality. Confusingly, some heavily advertised metrics rely on a combination of subjective reputational and lagging objective measures. Most consumers don’t know enough about the sources of information to understand which ratings are meaningful to outcomes.

Arguably, hospital quality star ratings created by the Centers for Medicare and Medicaid Services (CMS) are the best information for potential patients to rate hospital mortality, safety, readmission, patient experience, and timely/effective care. These five categories combine 47 of the more than 100 measures CMS publicly reports. [16]

A 2017 JAMA article by lead author Dr. Ashish Jha said:

“Found that a higher CMS star rating was associated with lower patient mortality and readmissions. It is reassuring that patients can use the star ratings in guiding their health care seeking decisions given that hospitals with more stars not only offer a better experience of care, but also have lower mortality and readmissions.”

The study included only Medicare patients who typically are over 65, and the differences were most apparent at the extremes, nevertheless,

“These findings should be encouraging for policymakers and consumers; choosing 5-star hospitals does not seem to lead to worse outcomes and in fact may be driving patients to better institutions.” [17]

Developing more 5-star hospitals is not only better and safer for patients but also will save resources by avoiding expensive complications and suffering.

As a patient, doing your homework before you have an urgent or elective need can change your outcome for the better. Driving a

couple of hours to a CMS 5-star hospital or flying to a specialty hospital for an elective procedure could make a difference.

Business case studies have noted that hospitals with a focus on a specific condition deliver improved outcomes while becoming more efficient. [18] Similarly, specialty surgical areas within general hospitals have also been effective in improving quality while reducing costs. Mayo Clinic demonstrated this with its cardiac surgery department. [19] A similar example is Shouldice Hospital near Toronto, a focused factory specializing in hernia repairs. In the last 75 years, the Shouldice team has completed four hundred thousand hernia repairs, mostly performed under local anesthesia with the patient walking to and from the operating room. [20] [21]

THE BOTTOM LINE

The Mayo Brother’s quote, “The patient’s needs come first,” is more relevant today than when first articulated over a century ago. Driving treatment into distinct categories of acute, urgent, and elective, with subsequent directing care to the appropriate facilities, improves the entire care process for the patient. The saved resources can fund prevention and decrease the need for future care. The healthcare industry’s focus has been on sickness,

not prevention. The virtuous cycle’s flywheel effect of distinct categories for care and embracing prevention of illness will decrease misery and lower the percentage of GDP devoted to healthcare.

Editor’s note: This is a multi-part series on reinventing the healthcare industry. Part 2 addresses physicians, non-physician caregivers, and communities’ responses to the coming transformation.

In the last edition of the Weekly Gist, we illustrated how non-hospital physician employment spiked during the pandemic. Diving deeper into the same report from consulting firm Avalere Health and the nonprofit Physicians Advocacy Institute, the graphic above looks at the specialties that currently have the greatest number of physicians employed by hospitals and corporate entities (which include insurers, private equity, and non-provider umbrella organizations), and those that remain the most independent.

To date, there has been little overlap in the fields most heavily targeted for employment by hospitals and corporate entities. Hospitals have largely employed doctors critical for key service lines, like cancer and cardiology, as well as hospitalists and other doctors central to day-to-day hospital operations.

In contrast, corporate entities have made the greatest strides in specialties with lucrative outpatient procedural business, like nephrology (dialysis) and orthopedics (ambulatory surgery), as well as specialties like allergy-immunology, that can bring profitable pharmaceutical revenue.

Meanwhile, only a few specialties remain majority independent. Historically independent fields like psychiatry and oral surgery saw the number of independent practitioners fall over 25 percent during the pandemic.

While hospitals will remain the dominant physician employer in the near term, corporate employment is growing unabated, as payers and investors, unrestrained by fair market value requirements, can offer top dollar prices to practices.

While hospitals, payers, and private equity firms have long been competing to acquire independent physician groups, theCOVID pandemic spurred a marked acceleration of the physician employment trend, with non-hospital corporate entities leading the charge.

The graphic above uses data released by consulting firm Avalere Health and the nonprofit Physicians Advocacy Institute to show that nearly three quarters of American physicians were employed by a larger entity as of January 2022, up from 62 percent just three years prior.

While hospitals employ a majority of those physicians, corporate entities (a group that includes payers, private equity groups, and non-provider umbrella organizations) have been increasing their physician rolls at a much faster rate.

Corporate entities employed over 40 percent more physicians in 2022 than in 2019, and in the southern part of the country—a hotspot for growth of Medicare Advantage—corporate physician employment grew by over 50 percent.

We expect the move away from private practice, accelerated by the pandemic, will only continue as physicians seek financial returns, secure a path to retirement, and look to access capital for necessary investments to help grow and manage the increasing complexities of running a practice.

Given the economic situation most hospitals face today, it was only a matter of time before we started to hear comments like we heard recently from a system CEO.

“We’ve got to pump the brakes on physician employment this year,” she said. “This arms race with Optum and PE firms has gotten out of control, and we’re looking at almost $300K per year of loss per employed doc.”

Of course, that system (like most) has been calling that loss a “subsidy” or an “investment” for the past several years, justified by the ability to pursue an integrated model of care and to grow the overall system book of business.

But with non-hospital competitors unfettered by the requirement to pay “fair market value” for physicians, the bidding war for doctors has become unsustainable for many hospitals. Around half of physicians are now employed by hospitals, with many more employed in other corporate settings.

There’s a growing sense that the pendulum has swung too far in the direction of employment, and now the phrase “stopping the bleed”—commonplace in the post-PhyCor days of the early 2000s—has begun to ring out again.

One challenge: finding ways to talk openly about “pumping the brakes” with the board, given that most systems have key physician stakeholders as part of their governance structure. Twice in the last month we’ve had CEOs ask us about reconfiguring their boards so that there are fewer doctors involved in governance—a sharp about-face from the “integration” narrative of just a few years ago.

It’s a tricky balance to strike. We recently heard a fascinating statistic that we’re working to verify: a third of all hospital CEO turnover in the last year was driven by votes of no-confidence by the medical staff. True or not, there’s no doubt that running afoul of physicians can be a career-limiting move for hospital executives, so if we’re about to enter an era of dialing back physician employment strategies, it’ll be fascinating to see how the conversations unfold. We’ll continue to keep an eye on this shift in direction and would love to know what you’re hearing as well, and to discuss how we might be of assistance in navigating what are sure to be a series of difficult choices.

Running a health system recently has proven to be a very hard job. Mounting losses in the face of higher operating expenses, softer than expected volumes, deferred capex, and strained C-suite succession planning are just a few of the immediate issues with which CEOs and boards must deal.

But frankly, none of those are the biggest strategic issue facing health systems. The biggest strategic issue is the reorganization of the American healthcare landscape into an ambulatory care business that emphasizes competing for covered lives at scale in lower cost and convenient settings of care. This shift in business model has significant ramifications, if you own and operate acute care hospitals.

Village MD and Optum are two of the organizations driving the business model shift. They are owned by large publicly traded companies (Walgreens and UnitedHealth Group, respectively). Both Optum and Village MD have had a string of announced major patient care acquisitions over the past few years, none of which is in the acute care space.

The future of American healthcare will likely be dominated by large well-organized and well-run multi-specialty physician groups with a very strong primary care component. These physician service companies will be payer agnostic and focused on value-based care, though will still be prepared to operate in markets where fee-for-service dominates. They will deliver highly coordinated care in lower cost settings than hospital outpatient departments. And these companies will be armed with tools and analytics that permit them to manage the care for populations of patients, in order to deliver both better health outcomes and lower costs.

At the same time this is happening, we are experiencing steady growth in Medicare Advantage. And along with it, a stream of primary care groups who operate purpose-built clinics to take full risk on Medicare Advantage populations. These companies include ChenMed, Cano Health and Oak Street, among others. These organizations use strong culture, training, and analytics to better manage care, significantly reduce utilization, and produce better health outcomes and lower costs.

Public and private equity capital are pouring into the non-acute care sectors, fueling this growth. As of the start of 2022, nearly three quarters of all physicians in the US were employed by either corporate entities (such as private equity, insurance companies, and pharmacy companies), or employed by health systems. And this employment trend has accelerated since the start of the pandemic. The corporate entities, rather than health systems, are driving this increasing trend. Corporate purchases of physician practices increased by 86% from 2019 to 2021.

What can health systems do? To succeed in the future, you must be the nexus of care for the covered lives in your community. But that does not mean the health system must own all the healthcare assets or employ all of the physicians. The health system can be the platform to convene these assets and services in the community. In some respects, it is similar to an Apple iPhone. They are the platform that convenes the apps. Some of those apps are developed and owned by Apple. But many more apps are developed by people outside of Apple, and the iPhone is simply the platform to provide access.

Creating this platform requires a change in mindset. And it requires capital. There are many opportunities for health systems to partner with outside capital providers, such as private equity, to position for the future – from both a capital and a mindset point of view.

The change in mindset, and the access to flexible capital, is necessary as the future becomes more and more about reorganizing into an ambulatory care business that emphasizes competing for covered lives at scale in lower cost and convenient settings of care.

Last Thursday, the Federal Trade Commission (FTC) released a proposed rule that would ban employers from imposing noncompete agreements on their employees. Noncompetes affect roughly 20 percent of the American workforce, and healthcare providers would be particularly impacted by this change, as far greater shares of physicians—at least 45 percent of primary care physicians, according to one oft-cited study—are bound by such agreements.

The rulemaking process is expected to be contentious, as the US Chamber of Commerce has declared the proposal “blatantly unlawful”. While it is unclear whether the rule would apply to not-for-profit entities, the American Hospital Association has released a statement siding with the Chamber of Commerce and urging that the issue continue to be left to states to determine.

The Gist: Should this sweeping rule go into effect, it would significantly shift bargaining power in the healthcare sector in favor of doctors, allowing them the opportunity to move away from their current employers while retaining local patient relationships.

The competitive landscape for physician talent would change dramatically, particularly for revenue-driving specialists, who would have far greater flexibility to move from one organization to another, and to push aggressively for higher compensation and other benefits.

Given that the FTC cited suppressed competition in healthcare as an outcome of current noncomplete agreements, the burden will be on organizations that employ physicians—including health systems and insurers, as well as private equity-backed corporate entities—to prove that physician noncompetes areessential to their operations and do not raise prices, as the FTC has suggested.

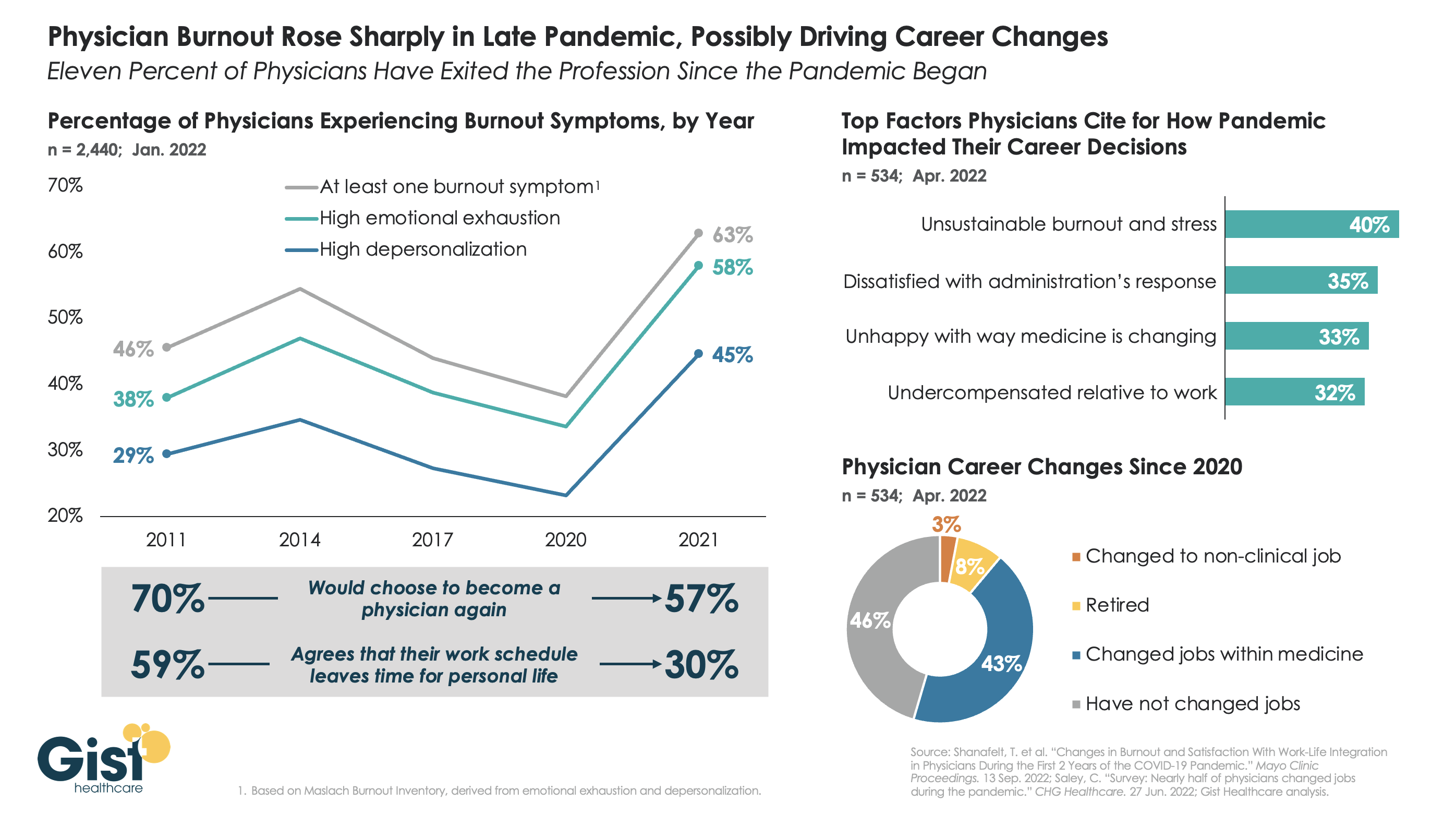

The long hours, stressful conditions, and labor shortages brought on by the pandemic have done serious harm to the physician workforce. The graphic above tracks physician burnout, a combination of emotional exhaustion, loss of agency, and depersonalization that has become the primary measure of the pandemic’s toll on workers, to reveal that physicians are demoralized like never before.

Physician burnout levels had been decreasing since 2014, in part due to practice consolidation and the expansion of team-based care models. Burnout reached its lowest levels in 2020—perhaps explained by a pandemic-induced sense of purpose—but 2021 then saw a dramatic spike in every measure of physician dissatisfaction, as the heroic glow of the early pandemic faded, and an overtaxed and understaffed delivery system became the new norm.

In explaining how the pandemic has impacted their career decisions, surveyed physicians list unsustainable burnout and stress as their top concern, and 11 percent say they have exited the profession, either for retirement or a non-clinical job, in the past two years.Four in ten surveyed physicians report changing jobs since 2020, mainly within similar or different practice settings, citing a desire for better work-life balance as their primary motivation. (It should be caveated that these data are from a smaller survey of 534 physicians, 40 percent of whom identified as “early career”.)

While the solutions here aren’t new, they are challenging: we must continue to implement team-based care models that provide physicians top-of-license practice and improved work-life balance, remove administrative tasks wherever possible, and ensure that we are communicating and engaging physicians—employed and independent alike—in organizational strategy and decision-making.