Norfolk, Va.-based Sentara Healthcare and Greensboro, N.C.-based Cone Health have abandoned plans to merge into an $11.5 billion system, the organizations said in a joint statement June 2.

The health systems said they mutually agreed to end the plans late last week. Leaders said they believe their respective organizations will be better served by remaining independent.

The two healthcare systems announced plans to combine last August. The deal would have formed an $11.5 billion system with 17 hospitals in Virginia and North Carolina.

“Sentara Healthcare and Cone Health are high performing, well respected, community-focused organizations. Those similarities served as the basis for efforts toward an affiliation. I am confident that this mutual decision will not alter either organization’s ongoing commitment to meet the needs of our respective communities,” Howard Kern, president and CEO of Sentara, said in a prepared statement. “I have no doubt that Cone Health will remain a top tier health system and will continue to pursue new and innovative ways to provide value for North Carolinians for years to come.”

“We appreciate the efforts of Sentara to work with Cone Health to determine whether an affiliation of our two high-performing organizations is in the best interest of those we serve. Recently, in the final analysis, we mutually decided that we can best serve our communities by remaining independent organizations,” Terry Akin, CEO of Cone Health, said in the news release.

Here are 10 health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings, Moody’s Investors Service and S&P Global Ratings.

1. St. Louis-basedBJC HealthCare has an “AA” rating and stable outlook with S&P. The health system has a leading market share and highly regarded reputation, particularly for its flagship hospitals that are affiliated with Washington University School of Medicine in St. Louis, S&P said. The health system consistently has produced stable earnings and cash flow, even during the COVID-19 pandemic, according to the credit rating agency.

2. Cleveland Clinic has an “Aa2” rating and stable outlook from Moody’s. The credit rating agency said the health system benefits from its reputation as an international brand, which will allow it to grow revenue outside of the Ohio market. Moody’s said it maintains good cash flow margins and therefore very strong liquidity.

3. Fountain Valley, Calif.-basedMemorialCarehas an “AA-” rating and stable outlook with Fitch. The health system has a strong financial profile and maintains high liquidity, Fitch said. The credit rating agency expects the system to generate cash flows of approximately 7 percent in the years after fiscal 2021.

4. Winston-Salem, N.C.-based Novant Health has an “AA-” rating and stable outlook with Fitch. The health system has a solid market position in four regions and strong financial metrics that support the rating. The credit rating agency said Novant Health’s acquisition of New Hanover Regional Medical Center in Wilmington, N.C., will benefit the system financially and strategically in the long term.

5. OhioHealth has an “Aa2” rating and stable outlook from Moody’s. The credit rating agency said the health system has a leading market position with several growth opportunities in an attractive market and a favorable payer market that contributes to stability. Moody’s also said OhioHealth’s ongoing cost reductions and management discipline will continue to support strong margins and liquidity levels.

6. Rady Children’s Hospital and Health Center in San Diego has an “Aa3” rating and stable outlook with Moody’s. The credit rating agency said that Rady Children’s has an extremely high market share in San Diego County and benefits from its status as a regional referral center for tertiary and quaternary pediatric services. The health system also has very strong liquidity, Moody’s said.

7.Stanford (Calif.) Health has an “AA” rating and stable outlook with Fitch. The credit rating agency said the hospital has a broad reach and benefits, as it is a clinical destination for high-acuity services, a largely favorable service area and a close relationship with Stanford University. Fitch said it expects the health system’s post-2021 EBITDA margin to be closer to its historical 11 percent operating margin.

8. Spectrum Health in Grand Rapids, Mich., has an “Aa3” rating and stable outlook with Moody’s. The credit rating agency said the health system has a stable operating performance and strong balance sheet metrics. In particular, the system generated positive margins even without federal relief aid in fiscal year 2020. Moody’s added that the health system will continue to benefit from a strong market share for patient care in western Michigan.

9.SSM Health in St. Louis has an “AA-” rating and stable outlook with Fitch. The credit rating agency said it has a strong financial profile and a solid market presence in multiple states with no dependence on any one location. Fitch also said its expanding health plan is a credit positive.

10. Birmingham, Ala.-based UAB Medicine has an “Aa3” rating and stable outlook with Moody’s. The credit rating agency said the health system has high patient demand, strong margins and a leading market share in Birmingham. The credit rating agency expects UAB Medicine to generate strong cash flow in fiscal year 2021.

Optum, a subsidiary of UnitedHealth, provides data analytics and infrastructure, a pharmacy benefit manager called OptumRx, a bank providing patient loans called Optum Bank, and more.

It’s not often that the American Hospital Association—known for fun lobbying tricks like hiring consultants to create studies showing the benefits of hospital mergers—directly goes after another consolidation in the industry.

But when the AHA caught wind of UnitedHealth Group subsidiary Optum’s plans, announced in January 2021, to acquire data analytics firm Change Healthcare, they offered up some fiery language in a letter to the Justice Department. “The acquisition … will concentrate an immense volume of competitively sensitive data in the hands of the most powerful health insurance company in the United States, with substantial clinical provider and health insurance assets, and ultimately removes a neutral intermediary.”

If permitted to go through, Optum’s acquisition of Change would fundamentally alter both the health data landscape and the balance of power in American health care. UnitedHealth, the largest health care corporation in the U.S., would have access to all of its competitors’ business secrets. It would be able to self-preference its own doctors. It would be able to discriminate, racially and geographically, against different groups seeking insurance. None of this will improve public health; all of it will improve the profits of Optum and its corporate parent.

Despite the high stakes, Optum has been successful in keeping this acquisition out of the public eye.Part of this PR success is because few health care players want to openly oppose an entity as large and powerful as UnitedHealth. But perhaps an even larger part is that few fully understand what this acquisition will mean for doctors, patients, and the health care system at large.

If regulators allow the acquisition to take place, Optum will suddenly have access to some of the most secret data in health care.

UnitedHealth is the largest health care entity in the U.S., using several metrics. United Healthcare (the insurance arm) is the largest health insurer in the United States, with over 70 million members, 6,500 hospitals, and 1.4 million physicians and other providers. Optum, a separate subsidiary, provides data analytics and infrastructure, a pharmacy benefit manager called OptumRx, a bank providing patient loans called Optum Bank, and more. Through Optum, UnitedHealth also controls more than 50,000 affiliated physicians, the largest collection of physicians in the country.

While UnitedHealth as a whole has earned a reputation for throwing its weight around the industry, Optum has emerged in recent years as UnitedHealth’s aggressive acquisition arm. Acquisitions of entities as varied as DaVita’s dialysis physicians, MedExpress urgent care, and Advisory Board Company’s consultants have already changed the health care landscape. As Optum gobbles up competitors, customers, and suppliers, it has turned into UnitedHealth’s cash cow, bringing in more than 50 percent of the entity’s annual revenue.

On a recent podcast, Chas Roades and Dr. Lisa Bielamowicz of Gist Healthcare described Optum in a way that sounds eerily similar to a single-payer health care system. “If you think about what Optum is assembling, they are pulling together now the nation’s largest employers of docs, owners of one of the country’s largest ambulatory surgery center chains, the nation’s largest operator of urgent care clinics,” said Bielamowicz. With 98 million customers in 2020, OptumHealth, just one branch of Optum’s services, had eyes on roughly 30 percent of the U.S. population. Optum is, Roades noted, “increasingly the thing that ate American health care.”

Optum has not been shy about its desire to eventually assemble all aspects of a single-payer system under its own roof. “The reason it’s been so hard to make health care and the health-care system work better in the United States is because it’s rare to have patients, providers—especially doctors—payers, and data, all brought together under an organization,” OptumHealth CEO Wyatt Decker told Bloomberg. “That’s the rare combination that we offer. That’s truly a differentiator in the marketplace.” The CEO of UnitedHealth, Andrew Witty, has also expressed the corporation’s goal of “wir[ing] together” all of UnitedHealth’s assets.

Controlling Change Healthcare would get UnitedHealth one step closer to creating their private single-payer system. That’s why UnitedHealth is offering up $13 billion, a 41 percent premium on the public valuation of Change. But here’s why that premium may be worth every penny.

Change Healthcare is Optum’s leading competitor in pre-payment claims integrity; functionally, a middleman service that allows insurers to process provider claims (the receipts from each patient visit) and address any mistakes. To clarify what that looks like in practice, imagine a patient goes to an in-network doctor for an appointment. The doctor performs necessary procedures and uses standardized codes to denote each when filing a claim for reimbursement from the patient’s insurance coverage. The insurer then hires a reviewing service—this is where Change comes in—to check these codes for accuracy. If errors are found in the coded claims, such as accidental duplications or more deliberate up-coding (when a doctor intentionally makes a patient seem sicker than they are), Change will flag them, saving the insurer money.

The most obvious potential outcome of the merger is that the flow of data will allow Optum/UnitedHealth to preference their own entities and physicians above others.

To accurately review the coded claims, Change’s technicians have access to all of their clients’ coverage information, provider claims data, and the negotiated rates that each insurer pays.

Change also provides other services, including handling the actual payments from insurers to physicians, reimbursing for services rendered. In this role, Change has access to all of the data that flows between physicians and insurers and between pharmacies and insurers—both of which give insurers leverage when negotiating contracts. Insurers often send additional suggestions to Change as well; essentially their commercial secrets on how the insurer is uniquely saving money. Acquiring Change could allow Optum to see all of this.

Change’s scale (and its independence from payers) has been a selling point; just in the last few months of 2020, the corporation signed multiple contracts with the largest payers in the country.

Optum is not an independent entity; as mentioned above, it’s owned by the largest insurer in the U.S. So, when insurers are choosing between the only two claims editors that can perform at scale and in real time, there is a clear incentive to use Change, the independent reviewer, over Optum, a direct competitor.

If regulators allow the acquisition to take place, Optum will suddenly have access to some of the most secret data in health care. In other words, if the acquisition proceeds and Change is owned by UnitedHealth, the largest health care corporation in the U.S. will own the ability to peek into the book of business for every insurer in the country.

Although UnitedHealth and Optum claim to be separate entities with firewalls that safeguard against anti-competitive information sharing, the porosity of the firewall is an open question. As the AHA pointed out in their letter to the DOJ, “[UnitedHealth] has never demonstrated that the firewalls are sufficiently robust to prevent sensitive and strategic information sharing.”

In some cases, this “firewall” would mean asking Optum employees to forget their work for UnitedHealth’s competitors when they turn to work on implementing changes for UnitedHealth. It is unlikely to work. And that is almost certainly Optum’s intention.

The most obvious potential outcome of the merger is that the flow of data will allow Optum/UnitedHealth to preference their own entities and physicians above others. This means that doctors (and someday, perhaps, hospitals) owned by the corporation will get better rates, funded by increased premiums on patients. Optum drugs might seem cheaper, Optum care better covered. Meanwhile, health care costs will continue to rise as UnitedHealth fuels executive salaries and stock buybacks.

UnitedHealth has already been accused of self-preferencing. A large group of anesthesiologists filed suit in two states last week, accusing the company of using perks to steer surgeons into using service providers within its networks.

Even if UnitedHealth doesn’t purposely use data to discriminate, the corporation has been unable to correct for racially biased data in the past.

Beyond this obvious risk, the data alterations caused by the Change acquisition could worsen existing discrimination and medical racism. Prior to the acquisition, Change launched a geo-demographic analytics unit. Now, UnitedHealth will have access to that data, even as it sells insurance to different demographic categories and geographic areas.

Even if UnitedHealth doesn’t purposely use data to discriminate, the corporation has been unable to correct for racially biased data in the past, and there’s no reason to expect it to do so in the future. A study published in 2019 found that Optum used a racially biased algorithm that could have led to undertreating Black patients. This is a problem for all algorithms. As data scientist Cathy O’Neil told 52 Insights, “if you have a historically biased data set and you trained a new algorithm to use that data set, it would just pick up the patterns.” But Optum’s size and centrality in American health care would give any racially biased algorithms an outsized impact. And antitrust lawyer Maurice Stucke noted in an interview that using racially biased data could be financially lucrative. “With this data, you can get people to buy things they wouldn’t otherwise purchase at the highest price they are willing to pay … when there are often fewer options in their community, the poor are often charged a higher price.”

The fragmentation of American health care has kept Big Data from being fully harnessed as it is in other industries, like online commerce. But Optum’s acquisition of Change heralds the end of that status quo and the emergence of a new “Big Tech” of health care. With the Change data, Optum/UnitedHealth will own the data, providers, and the network through which people receive care. It’s not a stretch to see an analogy to Amazon, and how that corporation uses data from its platform to undercut third parties while keeping all its consumers in a panopticon of data.

The next step is up to the Department of Justice, which has jurisdiction over the acquisition (through an informal agreement, the DOJ monitors health insurance and other industries, while the FTC handles hospital mergers, pharmaceuticals, and more). The longer the review takes, the more likely it is that the public starts to realize that, as Dartmouth health policy professor Dr. Elliott Fisher said, “the harms are likely to outweigh the benefits.”

There are signs that the DOJ knows that to approve this acquisition is to approve a new era of vertical integration. In a document filed on March 24, Change informed the SEC that the DOJ had requested more information and extended its initial 30-day review period. But the stakes are high. If the acquisition is approved, we face a future in which UnitedHealth/Optum is undoubtedly “the thing that ate American health care.”

In our work over the years advising health systems on M&A, we’ve been struck by how often “social issues” cause deals that are otherwise strategically sound to go off the rails.

Of course, it’s an old chestnut that “culture eats strategy for breakfast”, but what’s been notable, especially recently, is how early in the process hot-button governance and leadership issues enter the discussions.

Where is the headquarters going to be? Who’s going to be the CEO of the combined entity? And most vexingly, how many board seats is each organization going to get? That last issue is particularly troublesome, as it’s often where negotiations get bogged down. But as one health system board member recently pointed out to us, getting hung up on whether board seats are split 7-6 or 8-5 is just silly—in her words, “If you’re in a position where board decisions turn on that close of a margin, you’ve got much bigger strategic problems.”

It’s an excellent point. While boards shouldn’t just rubber stamp decisions made by management, it’s incumbent on the CEO and senior leaders to enfranchise and collaborate with the board in setting strategy, and critical decisions should rarely, if ever, come down to razor-thin vote tallies.

If a merger makes sense on its merits, and the strategic vision for the combined organization is clear, quibbling over how many seats each legacy system “gets” seems foolish. No board should go into a merger anticipating a future in which small majorities determine the outcome of big decisions.

Doctors and health systems with a significant portion of risk-based contracts weathered the pandemic better than their peers still fully tethered to fee-for-service payment. Lower healthcare utilization translated into record profits, just as it did for insurers.

We’re now seeing an increasing number of health systems asking again whether they should enter the health plan business—levels of interest we haven’t seen since the “rush to risk” in the immediate aftermath of the passage of the Affordable Care Act a decade ago.

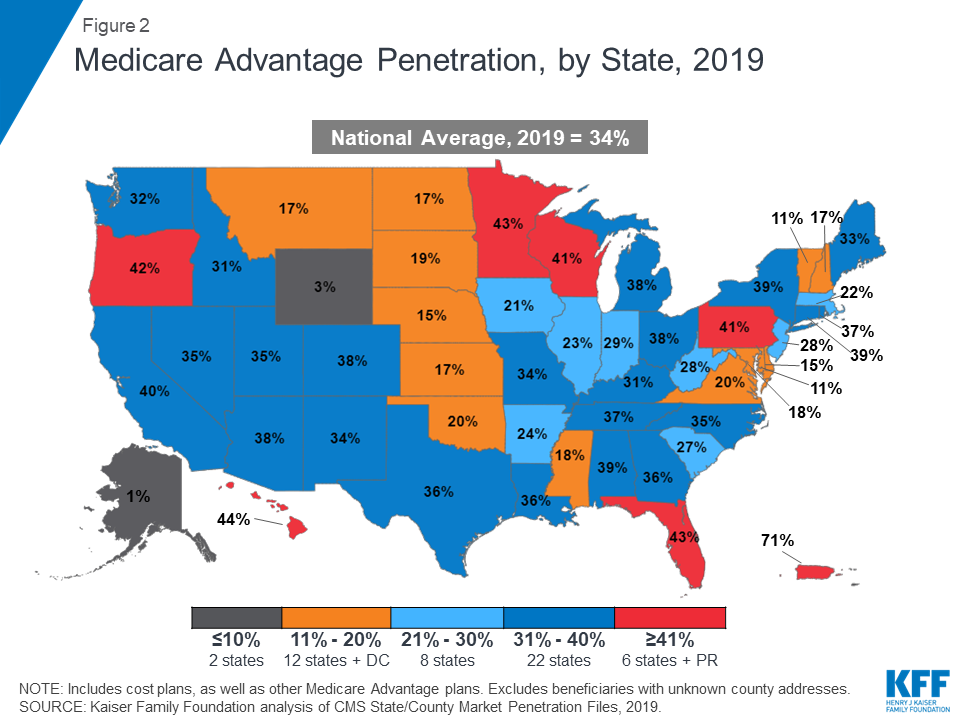

The discussions feel appreciably different this time around (which is a good thing, since many systems who launched plans in the prior wave had trouble growing and sustaining them). First, systems are approaching the market this time with a focus on Medicare Advantage, having seen that growing a base of covered lives with their networks is much easier than starting with the commercial market, where large insurers, particularly incumbent Blues plans, dominate the market, and many employers are still reticent to limit choice.

But foremost, there is new appreciation for the scale needed for a health plan to compete. In 2010, many executives set a goal of 100K covered lives as a target for sustainability; today, a plan with three times that number is considered small. Now many leaders posit that regional insurers need a plan to get to half a million lives, or more. (Somehow this doesn’t seem to hold for insurance startups: see the recent public offerings of Clover Health and Alignment Health, who have just 57K and 82K lives, respectively, nationwide.)

We’re watching for a coming wave of health system consolidation to gain the financial footing and geographic footprint needed to compete in the Medicare Advantage market, and would expect traditional payers to respond with regional consolidation of their own.

Virtual care company Doctor on Demand and clinical navigator Grand Rounds have announced plans to merge, creating a multibillion-dollar digital health firm.

The goal of combining the two venture-backed companies, which will continue to operate under their existing brands for the time being, is to integrate medical and behavioral healthcare with patient navigation and advocacy to try to better coordinate care in the fragmented U.S. medical system.

Financial terms of the deal, which is expected to close in the first half of this year, were not disclosed, but it is an all-stock deal with no capital from outside investors, company spokespeople told Healthcare Dive.

Dive Insight:

The digital health boom stemming from the coronavirus pandemic resulted in a flurry of high-profile deals last year, including the biggest U.S. digital health acquisition of all time: Teladoc Health’s $18.5 billion buy of chronic care management company Livongo. Such tie-ups in the virtual care space come as a slew of growing companies race to build out end-to-end offerings, making them more attractive to potential payer and employer clients and helping them snap up valuable market share.

Ten-year-old Grand Rounds peddles a clinical navigation platform and patient advocacy tools to businesses to help their workers navigate the complex and disjointed healthcare system, while nine-year-old Doctor on Demand is one of the major virtual care providers in the U.S.

Merging is meant to ameliorate the problem of uncoordinated care while accelerating telehealth utilization in previously niche areas like primary care, specialty care, behavioral health and chronic condition management, the two companies said in a Tuesday release.

Grand Rounds and Doctor on Demand first started discussing a potential deal in the early days of the coronavirus pandemic, as both companies saw surging demand for their offerings. COVID-19 completely overhauled how healthcare is delivered as consumers sought safe digital access to doctors, resulting in massive tailwinds for digital health companies and unprecedented investor interest in the sector.

Equity funding in digital health globally hit an all-time high of $26.5 billion in 2020, according to CB Insights, with mental and women’s health services seeing particularly fast growth in investor interest.

Both companies reported strong funding rounds in the middle of last year, catapulting Grand Rounds and Doctor on Demand to enterprise valuations of $1.34 billion and $821 million respectively, according to private equity marketplace SharesPost. Doctor on Demand says its current valuation is $875 million.

The combined entity will operate in an increasingly competitive space against such market giants as Teladoc, which currently sits at a market cap of $31.3 billion, and Amwell, which went public in September last year and has a market cap of $5.1 billion.

Grand Rounds CEO Owen Tripp will serve as CEO of the combined business, while Doctor on Demand’s current CEO Hill Ferguson will continue to lead the Doctor on Demand business as the two companies integrate and will join the combined company’s board.

When Jeff Goldsmith and Ian Morrison talk, people listen (apologies to E.F. Hutton…Goldsmith and Morrison are old enough to get that reference, anyway). These two lions of health policy and strategy came together recently to pen an editorial in Health Affairs examining the impact of large integrated health systems on the nation’s response to COVID-19. Morrison and Goldsmith admit to often finding themselves on opposite sides of consolidation issue, but looking back over the past year, both agree the scale systems have built over decades has been foundational to their effective and rapid response to the pandemic, which they rate as “better than just about any other element of our society”.

Larger health systems were able to mobilize the resources to secure protective gear as supplies dwindled.They responded at a speed many would have thought impossible, doubling ICU capacity in a matter of days, and shifting care to telemedicine, implementing their five-year digital strategies during the last two weeks of March.

This kind of innovation would have been impossible without the investments in IT and electronic records enabled by scale—butsystems also exhibited an impressive degree of “systemness”, making important decisions quickly, and mobilizing across regional footprints. Given the financial stresses experienced by smaller providers, consolidation is sure to increase. And the Biden healthcare team will likely bring more scrutiny to health system mergers.

Morrison and Goldsmith urge regulators to reconsider the role of health systems. The government should continue to pursue truly anticompetitive behavior that raises employer and consumer prices. But lawmakers should focus less on the sheer size of health systems and rather on their behavior, considering the potential societal impact a combined system might deliver—and creating policy that takes into account the role health systems have played in bolstering our public health infrastructure.

Even though signs point to a post-COVID spike in health system mergers, retailers, insurers, and other healthcare industry players already far exceed health system scale. Even the largest of the “mega health systems” pale in comparison to other healthcare companies up and down the value chain, as shown in the graphic above. And with the exception of pharma, these other industry players have seen revenues surge during the pandemic, while health system growth has stagnated.

According to a recent report from Kaufman Hall, hospitals saw a three percent reduction in annual total gross revenue in 2020.The majority of the decrease stemmed from a six percent decline in outpatient revenue, as volumes plummeted during the pandemic.

The largest companies listed here, including Walmart, Amazon, CVS, and UnitedHealth Group, continue to double down on vertical integration strategies, configuring an array of healthcare assets into platform businesses focused on delivering value to consumers.

To remain relevant, health systems will need to increase their focus on this strategy as well, assembling the right capabilities for a marketplace driven by value, at a scale that enables rapid innovation and sustainability.

Employers — including companies, state governments and universities — purchase health care on behalf of roughly 150 million Americans. The cost of that care has continued to climb for both businesses and their workers.

For many years, employers saw wasteful care as the primary driver of their rising costs. They made benefits changes like adding wellness programs and raising deductibles to reduce unnecessary care, but costs continued to rise. Now, driven by a combination of new research and changing market forces — especially hospital consolidation — more employers see prices as their primary problem.

By amassing and analyzing employers’ claims data in innovative ways, academics and researchers at organizations like the Health Care Cost Institute (HCCI) and RAND have helped illuminate for employers two key truths about the hospital-based health care they purchase:

1) PRICES VARY WIDELY FOR THE SAME SERVICES

Data show that providers charge private payers very different prices for the exact same services — even within the same geographic area.

For example, HCCI found the price of a C-section delivery in the San Francisco Bay Area varies between hospitals by as much as:$24,107

Data show that hospitals charge employers and private insurers, on average, roughly twice what they charge Medicare for the exact same services. A recent RAND study analyzed more than 3,000 hospitals’ prices and found the most expensive facility in the country charged employers:4.1xMedicare

Hospitals claim this price difference is necessary because public payers like Medicare do not pay enough. However, there is a wide gap between the amount hospitals lose on Medicare (around -9% for inpatient care) and the amount more they charge employers compared to Medicare (200% or more).

Employer Efforts

A small but growing group of companies, public employers (like state governments and universities) and unions is using new data and tactics to tackle these high prices. (Learn more about who’s leading this work, how and why by listening to our full podcast episode in the player above.)

Note that the employers leading this charge tend to be large and self-funded, meaning they shoulder the risk for the insurance they provide employees, giving them extra flexibility and motivation to purchase health care differently. The approaches they are taking include:

Steering Employees

Some employers are implementing so-called tiered networks, where employees pay more if they want to continue seeing certain, more expensive providers. Others are trying to strongly steer employees to particular hospitals, sometimes know as centers of excellence, where employers have made special deals for particular services.

Purdue University, for example, covers travel and lodging and offers a $500 stipend to employees that get hip or knee replacements done at one Indiana hospital.

Negotiating New Deals

There is a movement among some employers to renegotiate hospital deals using Medicare rates as the baseline — since they are transparent and account for hospitals’ unique attributes like location and patient mix — as opposed to negotiating down from charges set by hospitals, which are seen by many as opaque and arbitrary. Other employers are pressuring their insurance carriers to renegotiate the contracts they have with hospitals.

In 2016, the Montana state employee health plan, led by Marilyn Bartlett, got all of the state’s hospitals to agree to a payment rate based on a multiple of Medicare. They saved more than $30 million in just three years. Bartlett is now advising other states trying to follow her playbook.

In 2020, several large Indiana employers urged insurance carrier Anthem to renegotiate their contract with Parkview Health, a hospital system RAND researchers identified as one of the most expensive in the country. After months of tense back-and-forth, the pair reached a five-year deal expected to save Anthem customers $700 million.

Legislating, Regulating, Litigating

Some employer coalitions are advocating for more intervention by policymakers to cap health care prices or at least make them more transparent. States like Colorado and Indiana have passed price transparency legislation, and new federal rules now require more hospital price transparency on a national level. Advocates expect strong industry opposition to stiffer measures, like price caps, which recently failed in the Montana legislature.

Other advocates are calling for more scrutiny by state and federal officials of hospital mergers and other anticompetitive practices. Some employers and unions have even resorted to suing hospitals like Sutter Health in California.

Employer Challenges

Employers face a few key barriers to purchasing health care in different and more efficient ways:

Provider Power

Hospitals tend to have much more market power than individual employers, and that power has grown in recent years, enabling them to raise prices. Even very large employers have geographically dispersed workforces, making it hard to exert much leverage over any given hospital. Some employers have tried forming purchasing coalitions to pool their buying power, but they face tricky organizational dynamics and laws that prohibit collusion.

Sophistication

Employers can attempt to lower prices by renegotiating contracts with hospitals or tailoring provider networks, but the work is complicated and rife with tradeoffs. Few employers are sophisticated enough, for example, to assess a provider’s quality or to structure hospital payments in new ways.Employers looking for insurers to help them have limited options, as that industry has also become highly consolidated.

Employee Blowback

Employers say they primarily provide benefits to recruit and retain happy and healthy employees. Many are reluctant to risk upsetting employees by cutting out expensive providers or redesigning benefits in other ways. A recent KFF survey found just 4% of employers had dropped a hospital in order to cut costs.

The Tradeoffs

Employers play a unique role in the United States health care system, and in the lives of the 150 million Americans who get insurance through work. For years, critics have questioned the wisdom of an employer-based health care system, and massive job losses created by the pandemic have reinforced those doubts for many.

Assuming employers do continue to purchase insurance on behalf of millions of Americans, though, focusing on lowering the prices they pay is one promising path to lowering total costs. However, as noted above, hospitals have expressed concern over the financial pressures they may face under these new deals. Complex benefit design strategies, like narrow or tiered networks, also run the risk of harming employees, who may make suboptimal choices or experience cost surprises. Finally, these strategies do not necessarily address other drivers of high costs including drug prices and wasteful care.

![Chapter 1 - Private Equity as an Economic Driver: An Historical Perspective - Introduction to Private Equity [Book]](https://www.oreilly.com/library/view/introduction-to-private/9780470711880/dema_9780470711880_oeb_004_r1.gif)