Norfolk, Va.-based Sentara Healthcare and Greensboro, N.C.-based Cone Health have abandoned plans to merge into an $11.5 billion system, the organizations said in a joint statement June 2.

The health systems said they mutually agreed to end the plans late last week. Leaders said they believe their respective organizations will be better served by remaining independent.

The two healthcare systems announced plans to combine last August. The deal would have formed an $11.5 billion system with 17 hospitals in Virginia and North Carolina.

“Sentara Healthcare and Cone Health are high performing, well respected, community-focused organizations. Those similarities served as the basis for efforts toward an affiliation. I am confident that this mutual decision will not alter either organization’s ongoing commitment to meet the needs of our respective communities,” Howard Kern, president and CEO of Sentara, said in a prepared statement. “I have no doubt that Cone Health will remain a top tier health system and will continue to pursue new and innovative ways to provide value for North Carolinians for years to come.”

“We appreciate the efforts of Sentara to work with Cone Health to determine whether an affiliation of our two high-performing organizations is in the best interest of those we serve. Recently, in the final analysis, we mutually decided that we can best serve our communities by remaining independent organizations,” Terry Akin, CEO of Cone Health, said in the news release.

As we shared recently, post-pandemic healthcare volume is not returning evenly. While outpatient volume is rebounding quickly, other settings remain sluggish, especially the emergency department. We partnered with healthcare data analytics company Stratasan to take a closer look at ED volume decline. As shown in the graphic above, nationally, ED visits were down 27 percent in 2020, compared to 2019. ED-only volume (cases that started and ended in the ED) took a large hit across last year, down nearly a third from 2019. We expect that a portion of this ED-only volume will never fully recover to pre-COVID levels, with patient demand permanently shifting to lower-acuity care settings, including virtual, and some patients avoiding care altogether for minor ailments as they learn to “live with” problems like back pain.

ED-to-observation volume saw the greatest decline in 2020, likely as a result both of patients avoiding the ED, and presenting in the ED sicker, meeting the criteria for inpatient admission. However,ED-to-inpatient volume, which fell only seven percent in 2020, has been returning. In the second half of 2020, the ED-to-inpatient admission rate was 20 to 30 percent higher than the pre-COVID baseline. Across all three categories of ED volume, pediatrics saw steeper declines compared to adult cases. While some further ED volume rebound is anticipated, health systems should expect that fewer, but sicker, patients will be the new normal for hospital emergency departments.

Fewer low-acuity patients utilizing high-cost emergency care is good news from a public health perspective, but health systems must bolster other access channels like urgent care and telemedicine to ensure patients have convenient access for emergent care needs.

The signs of progress are encouraging, but the metrics are still down slightly when compared to last month.

Slowly, the financial health of the nation’s healthcare institutions are improving. Hospitals and health systems continued to see performance improvements in April compared to the devastating losses experienced in the early months of the COVID-19 pandemic.

Hospital margins, volumes, and revenues were up across most performance metrics, both year-to-date and year-over-year, but were down compared to March, according to the latest issue of Kaufman Hall’s National Hospital Flash Report. There was no explicit reason given for the dip, but any number of factors small and large could play into the results. It’s possible that clearer trend lines will develop over time.

WHAT’S THE IMPACT?

While any signs of progress are encouraging, the April results draw a clear contrast to the severity of record-low performance seen during the first two months of the pandemic in 2020, rather than strong overall performance so far this year.

Operating margin, for example, rose 101.9% (or 8.6 percentage points) compared to January-April 2020, not including federal Coronavirus Aid, Relief, and Economic Security Act funding. With the funding, operating margin was up 90.6% year-to-date, or 6.9 percentage points.

Operating margin was up 113.1% (39.3%) without CARES and 109.5% (21.4%) with CARES, compared to the first full month of the pandemic in April 2020, when nationwide shutdowns and broad restrictions on outpatient procedures caused operating margins to plummet 282% year-over-year.

April 2021 hospital margins, however, remained relatively thin. The median Kaufman Hall hospital operating margin index was 2.4% for the month, not including CARES. Even with the funding, it was 3.3%.

When it came to volumes, hospitals saw them increase across most metrics compared to 2020 levels, but decrease slightly compared to March. Adjusted discharges were up 5.9% year-to-date and jumped 66.4% year-over-year, while adjusted patient days rose 10% year-to-date and 64.8% year-over-year. Both metrics fell 1% month-over-month.

Emergency department visits were mixed, falling 7% compared to the first four months of 2020, but rising 57.2% year-over-year and 5.3% month-over-month. Operating room minutes were down 3.6% from March, but increased 26.1% year-to-date, and shot up 189.2% compared to April 2020, when COVID-19 abruptly halted most outpatient procedures.

Revenues followed a similar pattern, with gross operating revenue (not including CARES) up 16.7% year-to-date and 71.8% year-over-year, but down 2.5% compared to the prior month. Inpatient revenue rose 10.6% year-to-date and 37.1% year-over-year, but was down 1.9% month-over-month. Outpatient revenue rose 20.3% year-to-date, jumped 114.8% compared to April 2020, but fell 2% from March.

Total expenses continued to increase both year-to-date and year-over-year, but saw moderate decreases month-over-month. Total expense was up 6.6% year to date and 13.1% year over year. Total labor expense increased 6.1% year-to-date and 9.4% year-over-year, and total nonlabor expense rose 7% year-to-date and 16.3% year-over-year.

Compared to March, though, all three metrics were down about 3%. Expense results were mixed when adjusted for the month’s volumes. Total expense per adjusted discharge, for example, increased 2% compared to January-April 2020, but fell 32.3% from April 2020 and 2% from March.

THE LARGER TREND

Despite the ongoing pandemic, the 2021 financial outlook for the global healthcare sector is mostly positive, as strong demand for products and services – including those related to COVID-19 – will more than offset lingering pressures from the public health emergency, Moody’s Investors Service found in December.

The demand will remain strong, largely due to aging populations, the improvement in access and the introduction of new and innovative products. There is one caveat: steadily rising healthcare expenditures, which will cause payers to continue to restrict utilization and lower prices.

In October, Moody’s found that owning a public hospital during the COVID-19 pandemic carriedoperational risk, which will compound the fiscal and credit difficulties facing many large urban counties across the U.S.

Whether recovery from the coronavirus this year is relatively rapid or relatively slow, America’s hospitals will face another year of struggle to regain their financial health.

Though consumers say they’re increasingly confident in returning to healthcare settings, hospital volume is not returning with the same momentum across the board. Using the most recent data from analytics firm Strata Decision Technology, covering the first quarter of this year, the graphic above shows that observation, inpatient, and emergency department volumes all remain below pre-COVID levels.

Consumers are still most wary about returning to the emergency department, with volume down nearly 20 percent across the past year. Meanwhile, hospital outpatient visits rebounded quickly, and have been growing steadily month over month, finishing March 2021 at 36 percent above the 2019 level.

Meanwhile, a recent report from the Commonwealth Fund shows that no ambulatory specialty fully made up for the COVID volume hit by the end of last year. But some areas, including rheumatology, urology, and adult primary care, have bounced back faster than others.

With continued success in rolling out vaccines and reducing COVID cases, we’d expect a continued recovery of most hospital visit volume. It may be, however, that some areas, such as the emergency department, will never fully recover to pre-COVID levels. To the extent those visits are now being replaced by more appropriate telemedicine and urgent care utilization, that’s welcome news.

But the continued lag of inpatient admissions indicates that some of the loss of emergency volume is more worrisome—warranting continued efforts on the part of providers to reassure patients it’s safe to use healthcare services. Stay tuned as our team continues to dig into this data.

Optum, a subsidiary of UnitedHealth, provides data analytics and infrastructure, a pharmacy benefit manager called OptumRx, a bank providing patient loans called Optum Bank, and more.

It’s not often that the American Hospital Association—known for fun lobbying tricks like hiring consultants to create studies showing the benefits of hospital mergers—directly goes after another consolidation in the industry.

But when the AHA caught wind of UnitedHealth Group subsidiary Optum’s plans, announced in January 2021, to acquire data analytics firm Change Healthcare, they offered up some fiery language in a letter to the Justice Department. “The acquisition … will concentrate an immense volume of competitively sensitive data in the hands of the most powerful health insurance company in the United States, with substantial clinical provider and health insurance assets, and ultimately removes a neutral intermediary.”

If permitted to go through, Optum’s acquisition of Change would fundamentally alter both the health data landscape and the balance of power in American health care. UnitedHealth, the largest health care corporation in the U.S., would have access to all of its competitors’ business secrets. It would be able to self-preference its own doctors. It would be able to discriminate, racially and geographically, against different groups seeking insurance. None of this will improve public health; all of it will improve the profits of Optum and its corporate parent.

Despite the high stakes, Optum has been successful in keeping this acquisition out of the public eye.Part of this PR success is because few health care players want to openly oppose an entity as large and powerful as UnitedHealth. But perhaps an even larger part is that few fully understand what this acquisition will mean for doctors, patients, and the health care system at large.

If regulators allow the acquisition to take place, Optum will suddenly have access to some of the most secret data in health care.

UnitedHealth is the largest health care entity in the U.S., using several metrics. United Healthcare (the insurance arm) is the largest health insurer in the United States, with over 70 million members, 6,500 hospitals, and 1.4 million physicians and other providers. Optum, a separate subsidiary, provides data analytics and infrastructure, a pharmacy benefit manager called OptumRx, a bank providing patient loans called Optum Bank, and more. Through Optum, UnitedHealth also controls more than 50,000 affiliated physicians, the largest collection of physicians in the country.

While UnitedHealth as a whole has earned a reputation for throwing its weight around the industry, Optum has emerged in recent years as UnitedHealth’s aggressive acquisition arm. Acquisitions of entities as varied as DaVita’s dialysis physicians, MedExpress urgent care, and Advisory Board Company’s consultants have already changed the health care landscape. As Optum gobbles up competitors, customers, and suppliers, it has turned into UnitedHealth’s cash cow, bringing in more than 50 percent of the entity’s annual revenue.

On a recent podcast, Chas Roades and Dr. Lisa Bielamowicz of Gist Healthcare described Optum in a way that sounds eerily similar to a single-payer health care system. “If you think about what Optum is assembling, they are pulling together now the nation’s largest employers of docs, owners of one of the country’s largest ambulatory surgery center chains, the nation’s largest operator of urgent care clinics,” said Bielamowicz. With 98 million customers in 2020, OptumHealth, just one branch of Optum’s services, had eyes on roughly 30 percent of the U.S. population. Optum is, Roades noted, “increasingly the thing that ate American health care.”

Optum has not been shy about its desire to eventually assemble all aspects of a single-payer system under its own roof. “The reason it’s been so hard to make health care and the health-care system work better in the United States is because it’s rare to have patients, providers—especially doctors—payers, and data, all brought together under an organization,” OptumHealth CEO Wyatt Decker told Bloomberg. “That’s the rare combination that we offer. That’s truly a differentiator in the marketplace.” The CEO of UnitedHealth, Andrew Witty, has also expressed the corporation’s goal of “wir[ing] together” all of UnitedHealth’s assets.

Controlling Change Healthcare would get UnitedHealth one step closer to creating their private single-payer system. That’s why UnitedHealth is offering up $13 billion, a 41 percent premium on the public valuation of Change. But here’s why that premium may be worth every penny.

Change Healthcare is Optum’s leading competitor in pre-payment claims integrity; functionally, a middleman service that allows insurers to process provider claims (the receipts from each patient visit) and address any mistakes. To clarify what that looks like in practice, imagine a patient goes to an in-network doctor for an appointment. The doctor performs necessary procedures and uses standardized codes to denote each when filing a claim for reimbursement from the patient’s insurance coverage. The insurer then hires a reviewing service—this is where Change comes in—to check these codes for accuracy. If errors are found in the coded claims, such as accidental duplications or more deliberate up-coding (when a doctor intentionally makes a patient seem sicker than they are), Change will flag them, saving the insurer money.

The most obvious potential outcome of the merger is that the flow of data will allow Optum/UnitedHealth to preference their own entities and physicians above others.

To accurately review the coded claims, Change’s technicians have access to all of their clients’ coverage information, provider claims data, and the negotiated rates that each insurer pays.

Change also provides other services, including handling the actual payments from insurers to physicians, reimbursing for services rendered. In this role, Change has access to all of the data that flows between physicians and insurers and between pharmacies and insurers—both of which give insurers leverage when negotiating contracts. Insurers often send additional suggestions to Change as well; essentially their commercial secrets on how the insurer is uniquely saving money. Acquiring Change could allow Optum to see all of this.

Change’s scale (and its independence from payers) has been a selling point; just in the last few months of 2020, the corporation signed multiple contracts with the largest payers in the country.

Optum is not an independent entity; as mentioned above, it’s owned by the largest insurer in the U.S. So, when insurers are choosing between the only two claims editors that can perform at scale and in real time, there is a clear incentive to use Change, the independent reviewer, over Optum, a direct competitor.

If regulators allow the acquisition to take place, Optum will suddenly have access to some of the most secret data in health care. In other words, if the acquisition proceeds and Change is owned by UnitedHealth, the largest health care corporation in the U.S. will own the ability to peek into the book of business for every insurer in the country.

Although UnitedHealth and Optum claim to be separate entities with firewalls that safeguard against anti-competitive information sharing, the porosity of the firewall is an open question. As the AHA pointed out in their letter to the DOJ, “[UnitedHealth] has never demonstrated that the firewalls are sufficiently robust to prevent sensitive and strategic information sharing.”

In some cases, this “firewall” would mean asking Optum employees to forget their work for UnitedHealth’s competitors when they turn to work on implementing changes for UnitedHealth. It is unlikely to work. And that is almost certainly Optum’s intention.

The most obvious potential outcome of the merger is that the flow of data will allow Optum/UnitedHealth to preference their own entities and physicians above others. This means that doctors (and someday, perhaps, hospitals) owned by the corporation will get better rates, funded by increased premiums on patients. Optum drugs might seem cheaper, Optum care better covered. Meanwhile, health care costs will continue to rise as UnitedHealth fuels executive salaries and stock buybacks.

UnitedHealth has already been accused of self-preferencing. A large group of anesthesiologists filed suit in two states last week, accusing the company of using perks to steer surgeons into using service providers within its networks.

Even if UnitedHealth doesn’t purposely use data to discriminate, the corporation has been unable to correct for racially biased data in the past.

Beyond this obvious risk, the data alterations caused by the Change acquisition could worsen existing discrimination and medical racism. Prior to the acquisition, Change launched a geo-demographic analytics unit. Now, UnitedHealth will have access to that data, even as it sells insurance to different demographic categories and geographic areas.

Even if UnitedHealth doesn’t purposely use data to discriminate, the corporation has been unable to correct for racially biased data in the past, and there’s no reason to expect it to do so in the future. A study published in 2019 found that Optum used a racially biased algorithm that could have led to undertreating Black patients. This is a problem for all algorithms. As data scientist Cathy O’Neil told 52 Insights, “if you have a historically biased data set and you trained a new algorithm to use that data set, it would just pick up the patterns.” But Optum’s size and centrality in American health care would give any racially biased algorithms an outsized impact. And antitrust lawyer Maurice Stucke noted in an interview that using racially biased data could be financially lucrative. “With this data, you can get people to buy things they wouldn’t otherwise purchase at the highest price they are willing to pay … when there are often fewer options in their community, the poor are often charged a higher price.”

The fragmentation of American health care has kept Big Data from being fully harnessed as it is in other industries, like online commerce. But Optum’s acquisition of Change heralds the end of that status quo and the emergence of a new “Big Tech” of health care. With the Change data, Optum/UnitedHealth will own the data, providers, and the network through which people receive care. It’s not a stretch to see an analogy to Amazon, and how that corporation uses data from its platform to undercut third parties while keeping all its consumers in a panopticon of data.

The next step is up to the Department of Justice, which has jurisdiction over the acquisition (through an informal agreement, the DOJ monitors health insurance and other industries, while the FTC handles hospital mergers, pharmaceuticals, and more). The longer the review takes, the more likely it is that the public starts to realize that, as Dartmouth health policy professor Dr. Elliott Fisher said, “the harms are likely to outweigh the benefits.”

There are signs that the DOJ knows that to approve this acquisition is to approve a new era of vertical integration. In a document filed on March 24, Change informed the SEC that the DOJ had requested more information and extended its initial 30-day review period. But the stakes are high. If the acquisition is approved, we face a future in which UnitedHealth/Optum is undoubtedly “the thing that ate American health care.”

Though the COVID-19 pandemic hampered Providence’s operational performance in 2020, the regional nonprofit powerhouse still ended the year in the black with net income of $1 billion, down about 9% from 2019.

Providence ended 2020 with an operating loss of $306 million, compared to an operating income of $214 million in 2019. However, healthy non-operating income recouped operating losses and offset reimbursement shortfalls from Medicaid and Medicare coverage, Providence said in full-year financial results released Monday.

The system, which operates 51 hospitals spanning seven states, posted drastic net losses in the first half of 2020 due to the pandemic, but seems to have closed out the year on more stable financial footing though volumes remain down.

Dive Insight:

Like other major systems, the pandemic railroaded Providence’s operational performance in 2020, as state and local lockdowns and orders to pause non-emergency procedures contributed to an unprecedented drop in patient volumes starting in March. As a result, the West Coast system reported a significant dip in patient revenue, along with skyrocketing expenses for personal protective equipment, pharmaceuticals and labor.

Volumes as measured by adjusted admissions were down 9% for the fiscal year ended Dec. 31, Providence said. Despite the lower volume, operating revenues were actually up 3% year over year to $25.7 billion, driven by growth in capitation, premium and diversified revenue streams — and supported by the recognition of $957 million in federal COVID-19 grants to providers from the Coronavirus Aid, Relief, and Economic Security Act passed a year ago.

However, operating expenses climbed 5% year over year to $26 billion, resulting in operating earnings before interest, depreciation and amortization of $1.1 billion, compared with $1.6 billion in 2019.

Overall, Providence’s financial results suggest the system was able to sidestep the worst of the pandemic’s financial effects, and mirrors 2020 reports from other major nonprofits.

Kaiser Permanente,which reported in early February, was also able to stay in the black despite COVID-19 deflating operating and net income, which fell about 19% and 15% respectively from 2019. Similarly, nonprofit Mayo Clinic reported a shrinking bottom line, with net income down almost 24% from 2019 though it remained profitable.

California-based nonprofit Sutter Health also squeaked to overall profitability in 2020 despite a operational loss of $321 million. The system, which said it expected to take several years to fully recover from COVID-19, launched a systemwide operational and financial review as a result of its weak operational performance.

For-profit operators weathered similar headwinds and were able to turn a profit in 2020, including Universal Health Services, HCA Healthcare, Tenet and Community Health Systems.

A number of hospital executives have called out CARES grants and other federal aid as a key help in turning their finances around in 2020. However, despite the pandemic’s financial pressures, numerous major operators, including Kaiser Permanante, Mayo Clinic and HCA said they would return all or a portion of congressional aid, even as powerful hospital lobbies call on Washington for additional funds.

A recent Kaufman Hall report suggests providers could be overwhelmed by ongoing COVID-19 expenses following a surge in cases over the winter. Researchers estimate hospitals could lose anywhere from $53 billion to $122 billion in revenue in 2021 if pandemic pressures don’t abate, despite the glimmer of hope brought by ongoing vaccination efforts.

Despite increasing distribution of coronavirus vaccines, Moody’s Investors Service has placed a negative outlook on nonprofit hospitals in 2021.

Providence came together in 2016 with the merger of Washington-based Providence Health & Services and California-based St. Joseph Health to create the nation’s fourth-biggest Catholic hospital chain. Its full-year earnings come a week after California Attorney General and Biden nominee for HHS Secretary Xavier Becerra disclosed his office is investigating whether Providence violated legal commitments in applying religious restrictions to medical care at a hospital in Orange County.

“For the most part providers were dependent on that CARES funding. I think they would have been in the red or break even without it,” Suzie Desai, a senior director at S&P Global Ratings, said.

The pandemic weighed heavily on the financial performance of not-for-profit hospitals in 2020, but some of the larger health systems remained profitable despite the upheaval — in large part thanks to substantial federal funding earmarked to prop up providers during the global health crisis.

Industry observers have been closely watching to see how health systems ultimately fared in 2020. Now, with the fiscal-year ended and accounted for, analysts say the $175 billion in federal funds was crucial for providers’ bottom lines.

“Without the stimulus funding, it is very likely we would have seen more issuers [hospitals/health] systems experience either lower profitable margins, or outright losses from operations,” Kevin Holloran, senior director of U.S. public finance for Fitch Ratings, said.

Still, the pandemic put a squeeze on nonprofit hospital margins last year, according to a recent Moody’s report that showed the median operating margin was 0.5% in 2020 compared to 2.4% in 2019.

The first half of the year hit providers especially hard as volumes fell drastically, seemingly overnight. Revenue plummeted alongside the volume declines as the nation paused lucrative elective procedures to preserve medical resources.

One estimate showed hospitals lost more than $20 billion as they halted surgeries in the early months of the outbreak in the U.S.

But as the year wore on, the outlook improved as some volumes returned closer to pre-pandemic levels. At the same time, health systems worked to cut expenses to mitigate the financial strain.

Still, some health systems did post operational losses even with the federal funds meant to help them. Moody’s found that 42% of 130 hospitals surveyed posted an operating loss, an increase from 23% the year prior. Yet, the 2019 survey included more hospitals, a total of 282.

Sutter Health, the Northern California giant, reported an operating loss for 2020 and said it was launching a “sweeping review” of its finances as the pandemic exacerbated existing challenges for the provider. Washington-based Providence also reported an operating loss for 2020. However, both Sutter and Providence were able to post positive net income thanks in large part to investment gains.

Investment income can aid nonprofit operators even when core operations are stunted like during 2020. Though, initially, the pandemic put stress on the stock market as uncertainty around the virus and its duration ballooned. The stock market took a dive and it was reflected in some six-month financials as both operations and investments took a hit.

“COVID and the stimulus is (hopefully) a once in a lifetime disruption of operations,” Holloran said, who noted analysts have been trying to assess whether the top line losses can be placed squarely on COVID-19. If that’s the case, analysts are typically more apt to keep the provider’s existing rating.

“For the most part providers were dependent on that CARES funding. I think they would have been in the red or break even without it,” Suzie Desai, a senior director at S&P Global Ratings, said.

For example, Arizona’s Banner Health would have posted an operating loss without federal relief, according to their financial reports. Banner Health was able to work its way back to black after it reported a loss through the first six months of the year. The same was true for Midwest behemoth Advocate Aurora.

The providers that were able to weather the storm of the pandemic tended to be integrated systems that had a health plan under their umbrella.

Kaiser Permanente ended the year with both positive operating and net income and returned relief funds it received.

“The integrated providers, yeah, were one group that just had a natural hedge with the insurance premiums still coming in,” Desai said.

Still, the hospital lobby is hoping to secure more funding for its members as the threat of the virus is still present even amid large scale efforts to vaccinate a majority of Americans to reach a blanket of protection from the novel coronavirus and its variants.

In our work over the years advising health systems on M&A, we’ve been struck by how often “social issues” cause deals that are otherwise strategically sound to go off the rails.

Of course, it’s an old chestnut that “culture eats strategy for breakfast”, but what’s been notable, especially recently, is how early in the process hot-button governance and leadership issues enter the discussions.

Where is the headquarters going to be? Who’s going to be the CEO of the combined entity? And most vexingly, how many board seats is each organization going to get? That last issue is particularly troublesome, as it’s often where negotiations get bogged down. But as one health system board member recently pointed out to us, getting hung up on whether board seats are split 7-6 or 8-5 is just silly—in her words, “If you’re in a position where board decisions turn on that close of a margin, you’ve got much bigger strategic problems.”

It’s an excellent point. While boards shouldn’t just rubber stamp decisions made by management, it’s incumbent on the CEO and senior leaders to enfranchise and collaborate with the board in setting strategy, and critical decisions should rarely, if ever, come down to razor-thin vote tallies.

If a merger makes sense on its merits, and the strategic vision for the combined organization is clear, quibbling over how many seats each legacy system “gets” seems foolish. No board should go into a merger anticipating a future in which small majorities determine the outcome of big decisions.

Doctors and health systems with a significant portion of risk-based contracts weathered the pandemic better than their peers still fully tethered to fee-for-service payment. Lower healthcare utilization translated into record profits, just as it did for insurers.

We’re now seeing an increasing number of health systems asking again whether they should enter the health plan business—levels of interest we haven’t seen since the “rush to risk” in the immediate aftermath of the passage of the Affordable Care Act a decade ago.

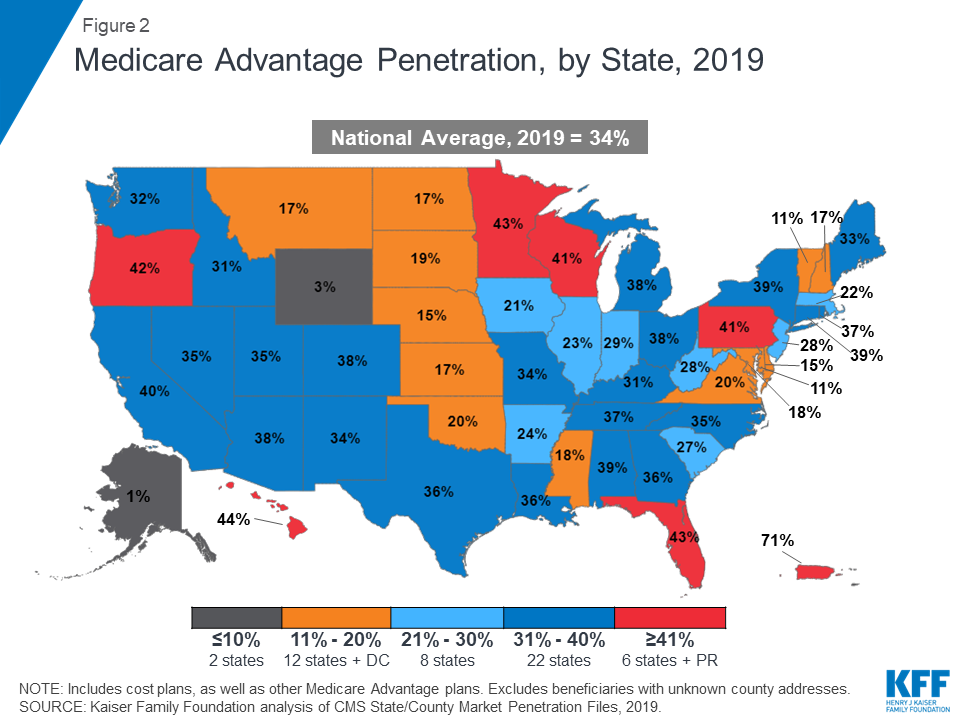

The discussions feel appreciably different this time around (which is a good thing, since many systems who launched plans in the prior wave had trouble growing and sustaining them). First, systems are approaching the market this time with a focus on Medicare Advantage, having seen that growing a base of covered lives with their networks is much easier than starting with the commercial market, where large insurers, particularly incumbent Blues plans, dominate the market, and many employers are still reticent to limit choice.

But foremost, there is new appreciation for the scale needed for a health plan to compete. In 2010, many executives set a goal of 100K covered lives as a target for sustainability; today, a plan with three times that number is considered small. Now many leaders posit that regional insurers need a plan to get to half a million lives, or more. (Somehow this doesn’t seem to hold for insurance startups: see the recent public offerings of Clover Health and Alignment Health, who have just 57K and 82K lives, respectively, nationwide.)

We’re watching for a coming wave of health system consolidation to gain the financial footing and geographic footprint needed to compete in the Medicare Advantage market, and would expect traditional payers to respond with regional consolidation of their own.

Glenview Capital Management, the hedge fund run by Larry Robbins, has a 12.9 percent stake in Tenet Healthcare after recently selling shares of the Dallas-based company, according to a Securities and Exchange Commission filing.

Glenview sold 2.5 million shares of Tenet, a 65-hospital system, on March 22 for $53.3 per share, bringing in a total of $133.25 million.

Tenet shares closed March 24 at $50.03 per share, down from $50.49 a day earlier, according to Yahoo Finance.

Tenet ended 2020 with net income of $399 million on revenue of $17.64 billion, compared to a net loss of $215 million on revenue of $18.48 billion a year earlier.