A review of Trump’s health care record so far. Avoiding the problematic issue of Trump’s alleged plan, analysts at the nonpartisan Kaiser Family Foundation released a report this week that examines President Trump’s record on health care over the last three and half years. Some highlights from the overview and the full analysis:

On the Affordable Care Act: “From the start of his presidential term, President Trump took aim at the Affordable Care Act, consistent with his campaign pledge leading up to the 2016 election. He supported many efforts in Congress to repeal the law and replace it with an alternative that would have weakened protections for people with pre-existing conditions, eliminated the Medicaid expansion, and reduced premium assistance for people seeking marketplace coverage. While the ACA remains in force, President Trump’s Administration is supporting the case pending before the U.S. Supreme Court to overturn the ACA in its entirety that is scheduled for oral arguments one week after the election.”

On Medicare and Medicaid: “The Administration has proposed spending reductions for both Medicaid and Medicare, along with proposals that would promote flexibility for states but limit eligibility for coverage under Medicaid (e.g., work requirements).”

On drug prices: “The President has made prescription drug prices a top health policy priority and has issued several executive orders and other proposals that aim to lower drug prices; most of these proposals, however, have not been implemented, other than one change that would lower the cost of insulin for some Medicare beneficiaries with diabetes, and another that allows pharmacists to tell consumers if they could save money on their prescriptions. The Trump Administration has also moved forward with an initiative to improve price transparency in an effort to lower costs, though it is held up in the courts.”

On the response to the coronavirus: “The Trump administration has not established a coordinated, national plan to scale-up and implement public health measures to control the spread of coronavirus, instead choosing to have states assume primary responsibility for the COVID-19 response, with the federal government acting as back-up and ‘supplier of last resort.’ The President has downplayed the threat of COVID-19, given conflicting messages and misinformation, and often been at odds with public health officials and scientific evidence.”

Americans became wealthier and more held jobs last year.

Yet at the very same time, one million people lost health insurance. And that number has steadily climbed this year under the pandemic.

A U.S. Census Bureau report released yesterday showed a continued slow erosion of the nation’s insured rate in 2019. The decline of coverage illustrates both the shortcomings of President Barack Obama’s 2010 health-care law and repeated attempts by President Trump and Republicans to undermine it.

“Though the reasons are sharply debated, the new data signifies that the first three years of President Trump’s tenure were a period of contracting health insurance coverage,” Amy Goldstein writes. “The decreases reversed gains that began near the end of the Great Recession and accelerated during early years of expanded access to health plans and Medicaid through the Affordable Care Act.”

Nearly 30 million Americans lacked health coverage in 2019.

The uninsured rate rose to 29.6 million people, totaling 9.2 percent of the population. It has slowly ticked upward since 2016, when 28.1 million people didn’t have a health plan. Between 2018 and 2019, the share of people without coverage increased in 19 states and decreased in just one.

The share of people on Medicare and with employer-sponsored coverage actually increased slightly. That was due to an aging population and last year’s booming economy, which meant more people had workplace plans — still the chief way Americans get their coverage.

The biggest erosions in coverage took place in state Medicaid programs.

Medicaid enrollment fell from 17.9 percent of Americans to 17.2 percent.

One reason for the decline is positive: As poverty rates fell for all major racial and ethnic groups, more people earned too much to qualify for the program. The poverty rate fell to 18.8 percent for Blacks, 15.7 percent for Hispanics and 9.1 percent for Whites.

But other factors were also at play. People no longer face a tax penalty for being uninsured, after Congress repealed it in 2017. Several GOP-led states expanded enrollment requirements. And wide disparities persisted in how states run their programs.

Missouri voters recently approved Medicaid expansion, making the state the seventh to do so under President Trump.

“There is huge variation state-to-state in the ease of enrollment, the administrative process, the mechanisms for verifying eligibility, how hard the state works to sign people up,” said Katherine Baicker, a health economist at the University of Chicago. “All those have big effects on net take-up rates.”

The trickle of coverage losses has become a flood under the pandemic.

Before the coronavirus pandemic upended life, the United States was enjoying a record-long economic expansion. By the end of last year, the unemployment rate was at a 50-year low of 3.5 percent.

“Women outnumbered men in the workforce for only the second time, buoyed by a tight labor market and fast job growth in health care and education,” Amy writes. “Minimum-wage increases were also fueling faster wage growth for those at the bottom.”

But now millions of people have lost their jobs — and, in the process, their health insurance.

“Since March … job losses have disproportionately hit low-income workers and women, many of whom held service-sector jobs that were gutted by shutdown measures to help protect people from infection,” Amy writes. “Nearly 40 percent of households with income below $40,000 were laid off or furloughed by early April, according to the Federal Reserve.”

The Economic Policy Institute has estimated that 12 million people have lost health insurance received through their workplace or that of a family member. Some of those have been able to enroll in Medicaid — its rolls have risen by about 4 million during the pandemic — but others find it unaffordable.

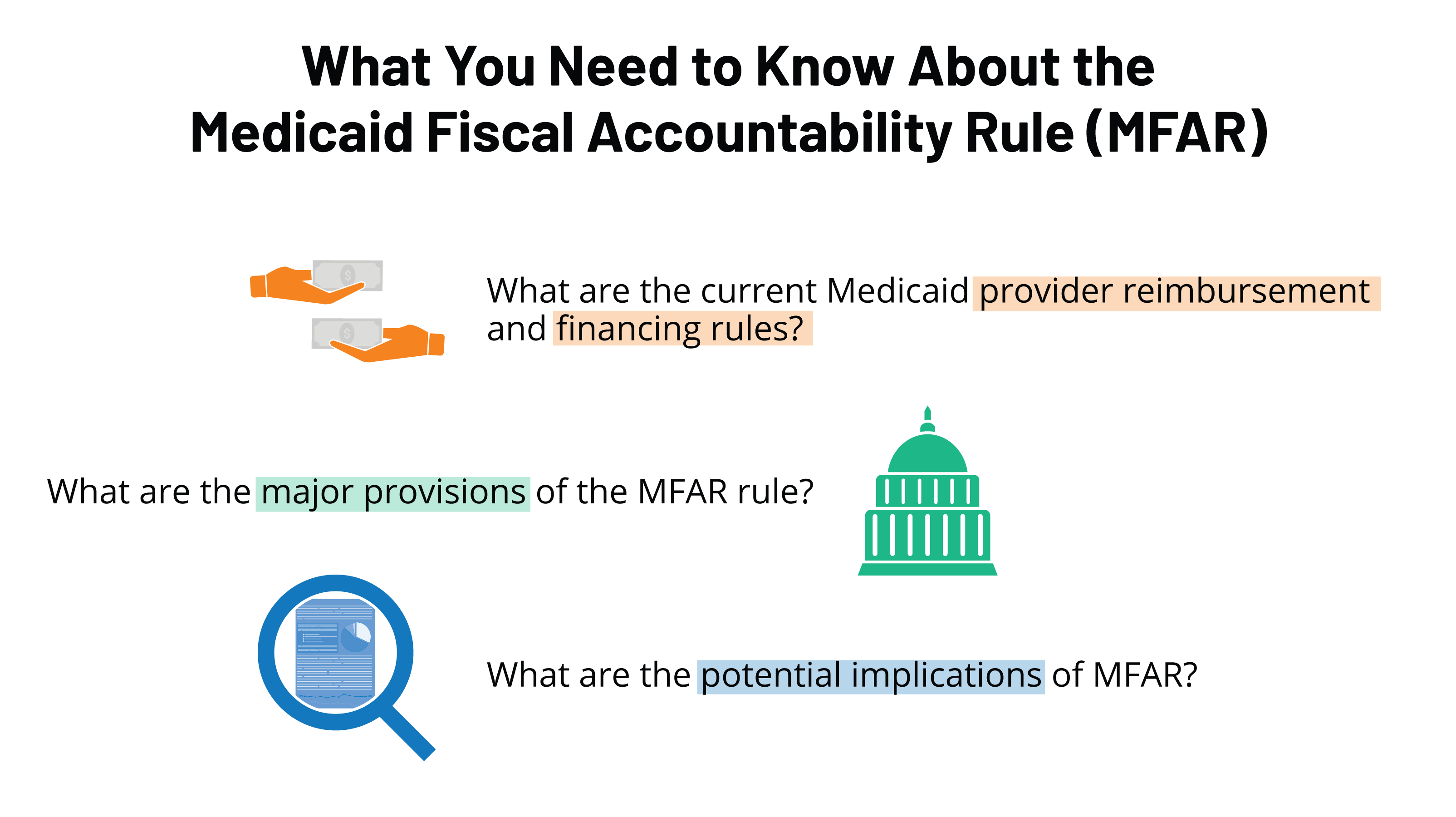

CMS is axing its proposed Medicaid Fiscal Accountability Rule, agency head Seema Verma announced via Twitter late Monday afternoon, in a move quickly cheered by provider organizations.

The rule proposed last year would have increased federal oversight of how states fund their Medicaid programs and potentially resulted in funding cuts for the cash-strapped safety net insurance. Myriad providers, patient advocacy groups and lawmakers in both states and the halls of Congress opposed the rule as a result.

“We’ve listened closely to concerns that have been raised by our state and provider partners about potential unintended consequences of the proposed rule, which require further study. Therefore, CMS is withdrawing the rule from the regulatory agenda,” Verma said.

Dive Insight:

MFAR was designed to increase fiscal transparency in the 55-year-old Medicaid program, but was quickly met with a firestorm of controversy, with even bipartisan House and Senate members raising concerns it could lead to states being forced to choose between program cuts or raising taxes to replace the lost funding.

One estimate, conducted by Manatt Health for the American Hospital Association, estimated the changes proposed in the rule would cut Medicaid funding by almost $50 billion annually, shrinking the program by 8%.

“Hospitals and health systems will be greatly relieved when the proposed rule is formally withdrawn,” AHA EVP Tom Nickels said in a statement.

Bruce Siegel, CEO of America’s Essential Hospitals, a lobby representing hospitals serving a disproportionate amount of vulnerable patients, called CMS’ decision “wise and welcome … especially as state budgets and providers strain under the heavy financial burden and economic fallout of COVID-19.”

Medicaid is jointly funded by the states and the federal government. Generally, CMS matches every dollar states spend at rates that vary depending on the state, its covered services and its population. There are no limits for how much federal funding a state can receive, and snowballing spending in Medicaid has resulted in concerns about cost control.

Medicaid spending swelled from $456 billion in 2013 to $576 billion in 2016, per CMS data, mostly due to an expanding federal share.

The most acute worries on the federal side stemmed from supplemental payments, or payments state Medicaid agencies give to providers for going above and beyond routine care, normally for high-need patients or those in underserved areas.

Supplemental payments to healthcare providers have increased from 9.4% of all other payments in 2010 to 17.5% in 2017, according to CMS, and are generally uneven across state lines, contributing to geographic funding disparities.

Oversight agencies, including the Government Accountability Office and the Office of the Inspector General, flagged the growth in payments and called for stronger Medicaid oversight in a series of reports from 2006 to 2015.

As a result, CMS proposed the MFAR rule in November 2019. If finalized, it would require states to report Medicaid payment and financing data at the individual provider level, instead of an aggregate, and establish definitions for “base” and “supplemental” payments. It would also have allowed CMS to sunset existing supplemental payment methodologies after up to three years, requiring states to get approval for a longer period, and close financing loopholes that might allow states to re-use federal Medicaid dollars to fund additional payments.

At the outset, CMS attempted to stamp out criticisms the rule could winnow Medicaid funding. “Alarmist estimates that this rule, if finalized, will suddenly remove billions of dollars from the program and threaten beneficiary access are overblown and without credibility,” Verma wrote in a blog post on the proposal in February.

But the rule received more than 4,000 public comments, most of them negative. The swirling concerns about unintended consequences, especially as COVID-19 exacerbates worries about care access, have now brought CMS back to the drawing board on Medicaid fiscal accountability.

As of late Monday, MFAR remained on the Federal Register.

Other actions from the Trump administration to overhaul Medicaid have faced similar backlash, including unpopular efforts to instill requirements linking coverage to work hours and an early 2020 push to cap federal funding for states in exchange for wider latitude in program administration.

This week’s contributor is Larry Levitt, the Executive Vice President for Health Policy at the Kaiser Family Foundation.

For the first time in an economic downturn, the Affordable Care Act (ACA) exists as a health care safety net for people losing their jobs and employer-provided health insurance. A new study provides some clues as to how well the health care law works for people who lose their jobs and insurance.

The study– by Sumit Agarwal and Benjamin Sommers, published in the New England Journal of Medicine – compares people who lost their jobs before and after the ACA went into effect in 2014 to see if there is a difference in how many people retained health insurance. During the pre-ACA period (2011-2013), there was about a 5% increase in the uninsured rate for people following a job loss. After the ACA went into effect (2014-2016), no such increase occurred. Instead, Medicaid and the marketplaces saw large increases in utilization.

With millions of Americans losing their jobs during the pandemic, the number of people without health coverage has undoubtedly risen. However, by how much is unknown, since we don’t track insurance coverage in real-time like we do employment. Many who have lost jobs may not have had employer-sponsored insurance in the first place, if they worked an industry like food service or retail. And the vast majority of people who are unemployed are classified as on temporary layoff, with employers who may be continuing health benefits for their furloughed workers, at least for now. However, the share of unemployed workers who have permanently lost their jobs is growing.

If the economic crisis persists, the number of people losing job-based health insurance will climb, making the ACA’s role as a safety net more relevant than ever.

“It’s new territory, which is why we’re taking that measured approach on rating actions,” Suzie Desai, senior director at S&P, said.

The healthcare sector has been bruised from the novel coronavirus and the effects are likely to linger for years, but the first half of 2020 has not resulted in an avalanche of hospital and health system downgrades.

At the outset of the pandemic, some hospitals warned of dire financial pressures as they burned through cash while revenue plunged. In response, the federal government unleashed $175 billion in bailout funds to help prop up the sector as providers battled the effects of the virus.

Still, across all of public finance — which includes hospitals — the second quarter saw downgrades outpacing upgrades for the first time since the second quarter of 2017.

S&P characterized the second quarter as a “historic low” for upgrades across its entire portfolio of public finance credits.

“While only partially driven by the coronavirus, the second quarter was the firstsince Q2 2017 with the number of downgrades surpassing upgrades and by the largest margin since Q3 2014,” according to a recent Moody’s Investors Service report.

Through the first six months of this year, Moody’s has recorded 164 downgrades throughout public finance and, more specifically, 27 downgrades among the nonprofit healthcare entities it rates.

By comparison, Fitch Ratings has recorded 14 nonprofit hospital and health system downgrades through July and just two upgrades, both of which occurred before COVID-19 hit.

“Is this a massive amount of rating changes? By no means,” Kevin Holloran, senior director of U.S. Public Finance for Fitch, said of the first half of 2020 for healthcare.

Also through July, S&P Global recorded 22 downgrades among nonprofit acute care hospitals and health systems, significantly outpacing the six healthcare upgrades recorded over the same period.

“It’s new territory, which is why we’re taking that measured approach on rating actions,” Suzie Desai, senior director at S&P, said.

Still, other parts of the economy lead healthcare in terms of downgrades. State and local governments and the housing sector are outpacing the healthcare sector in terms of downgrades, according to S&P.

Virus has not ‘wiped out the healthcare sector’

Earlier this year when the pandemic hit the U.S., some made dire predictions about the novel coronavirus and its potential effect on the healthcare sector.

Reports from the ratings agencies warned of the potential for rising covenant violations and an outlook for the second quarter that would result in the “worst on record,“ one Fitch analyst said during a webinar in May.

That was likely “too broad of a brushstroke,” Holloran said. “It has not come in and wiped out the healthcare sector,” he said. He attributes that in part to the billions in financial aid that the federal government earmarked for providers.

Though, what it has revealed is the gaps between the strongest and weakest systems, and that the disparities are only likely to widen, S&P analysts said during a recent webinar.

The nonprofit hospitals and health systems pegged with a downgrade have tended to be smaller in size in terms of scale, lower-rated already and light on cash, Holloran said.

Still, some of the larger health systems were downgraded in the first half of the year by either one of the three rating agencies, including Sutter Health, Bon Secours Mercy Health, Geisinger, University of Pittsburgh Medical Center and Care New England.

“This is something that individual management of a hospital couldn’t control,” said Rick Gundling, senior vice president of Healthcare Financial Management Association, which has members from small and large organizations. “It wasn’t a bad strategy — that goes into a downgrade. This happened to everybody.”

Deteriorating payer mix

Looking forward, some analysts say they’re more concerned about the long-term effects for hospitals and health systems that were brought on by the downturn in the economy and the virus.

One major concern is the potential shift in payer mix for providers.

As millions of people lose their job they risk losing their employer-sponsored health insurance. They may transition to another private insurer, Medicaid or go uninsured.

For providers, commercial coverage typically reimburses at higher rates than government-sponsored coverage such as Medicare and Medicaid. Treating a greater share of privately insured patients is highly prized.

If providers experience a decline in the share of their privately insured patients and see a growth in patients covered with government-sponsored plans, it’s likely to put a squeeze on margins.

The shift also poses a serious strain for states, and ultimately providers. States are facing a potential influx of Medicaid members at the same time state budgets are under tremendous financial pressure. It raises concerns about whether states will cut rates to their Medicaid programs, which ultimately affects providers.

Some states have already started to re-examine and slash rates, including Ohio.

Drugmakers are getting bolder in their bid to restrict access to drugs discounted under the 340B program as legal experts say a lack of enforcement has created a regulatory void.

Hospitals are imploring the Department of Health and Human Services (HHS) to clamp down on several moves by drug companies, including Novartis and AstraZeneca, to limit distribution of certain 340B drugs. But experts say an administration-wide change in what agencies can enforce is likely behind drugmakers’ aggressive moves.

“It is an outrage that these actions are being taken at a time when hospitals are in the midst of their response to the COVID-19 public health emergency, which has further demonstrated the fractured, inadequate state of the prescription drug supply chain,” the American Hospital Association said in a release last week.

Hospitals and 340B advocates are furious that AstraZeneca announced last Friday that starting Oct. 1 it will not offer any discounted drugs to contract pharmacies, which are third-party entities that dispense drugs acquired under the program.

It is the most aggressive move in a fight sparked last month between drug companies against contract pharmacies, which are a popular tool among 340B hospitals.

The back story

In exchange for participating in Medicaid, a drug manufacturer is required to offer discounts to safety-net hospitals that participate in 340B. But the program has been beset with controversy in recent years as drug companies claim the program has gotten too large and patients aren’t benefiting from the discounts.

Eli Lilly decided last month to restrict sales to contract pharmacies of certain formulations of erectile dysfunction drug Cialis. Merck and Novartis also said contract pharmacies would need to submit claims data to avoid duplicate discounts.

We’ve reached out to pharmaceutical companies for comment and will update when we hear back.

Industry advocacy organization Pharmaceutical Research and Manufacturers of America (PhRMA) has previously called for reforms to the 340B program, including to the ability for covered entities to contract with multiple outside pharmacies to dispense drugs that receive 340B discounts. Even though the number of Americans who are insured has risen, 340B is growing exponentially, they said. “Not all 340B hospitals are good stewards of the program,” PhRMA said.

Hospital groups and 340B allies charge that the moves blatantly violate a 2010 guidance released by the Health Resources and Services Administration (HRSA), which oversees the 340B program.

The guidance permits a hospital participating in 340B to voluntarily use a contract pharmacy and outlines the requirements to do so. The guidance also says a manufacturer must still sell a drug at a price not to exceed the statutory 340B price.

But an October 2019 executive order said federal agencies cannot enforce guidance documents unless they are part of a contract amid other exceptions.

HRSA has said that it doesn’t have the authority under the 340B statute to take enforcement action on “requirements that have been established under guidance,” said Emily Cook, a partner with law firm McDermott Will & Emery.

The agency’s current position is that it can only take enforcement actions on clear violations of the 340B statute, she added.

HRSA told Fierce Healthcarein a statementit is considering the issues raised by the manufacturers and “evaluating our next steps.”

What’s next

Hospitals are hoping HHS steps in and clears up the issue.

If not, then hospitals could either take drug companies to court or lobby Congress to give HRSA more authority over the program.

The advocacy group 340B Health said last week that if the administration refuses to step in then it will “pursue all legislative and legal avenues available to us to defend the safety net.”

Hospitals need to re-examine their 340B contract pharmacy deals to exclude AstraZeneca drugs, according to an article from Brenda Maloney Shafer and Richard Davis of law firm Quarles & Brady.

If they fail to do this, then the contract pharmacy could pay for dispensing and administrative fees for drugs that won’t get a 340B discount.

This is the latest spat over the controversial program. Hospitals took the administration to court after it tried to cut payments under the program by nearly 30%.

List of bullet points prompts debate over lack of detail, potential for actual achievement.

Health policy scholars critiqued the Trump campaign’s broad strokes healthcare agenda for his potential second term. While some found it overly vague, even dishonest, one suggested it was precisely what voters want.

Released Sunday night as a list of bullet points, the “Fighting for You” agenda will apparently serve as the Republican platform for the 2020 election. The GOP’s platform committee voted over the weekend to dispense with the customary detailed policy document for this cycle, in favor of simply backing President Trump’s agenda.

That agenda, which the Trump campaign promised would be fleshed out in future speeches and statements, included the following points relevant to healthcare:

Eradicate COVID-19

Develop a vaccine by the end of 2020

Return to normal in 2021

Make all critical medicines and supplies for healthcare workers

Refill stockpiles and prepare for future pandemics

Healthcare

Cut prescription drug prices

Put patients and doctors back in charge of our healthcare system

Lower healthcare insurance premiums

End surprise billing

Cover all pre-existing conditions

Protect Social Security and Medicare

Protect our veterans and provide world-class healthcare and services

Reliance on China

Allow 100% expensing deductions for essential industries like pharmaceuticals and robotics who bring back their manufacturing to the U.S.

No federal contracts for companies who outsource to China

Hold China fully accountable for allowing the virus to spread around the world

Joseph Antos, PhD, a resident scholar in healthcare and retirement policy at the American Enterprise Institute, characterized Trump’s strategy as “Don’t explain it. Just say what your goals are.”

He applauded the brevity of the document, 6 pages in total, covering 10 different policy areas from jobs to healthcare to immigration, as a “smart strategy.”

Voters don’t want to read lengthy policy briefs and gave the “Biden-Sanders Unity Task Force Recommendations” which were over 100 pages long and “unbelievably complicated stuff” as an example of how not to reach voters.

“I think [Trump] got it right. He’s not running a think tank…. He’s running for office. He does have a keen eye for what the average voter could stand to listen to.”

Gail Wilensky, PhD, an economist and senior fellow at Project Hope in Bethesda, Maryland, and CMS administrator under President George H.W. Bush, agreed that a platform packed with policy details doesn’t sway many voters.

This election, she said, is about one thing only: “Trump or not Trump.”

Whither the ACA?

Nevertheless, the Trump campaign’s goals merit attention, often for what they don’t include as well as what they do.

As for the substance of the agenda, the key difference between the Trump administration’s proposed agenda and that of the Democratic nominee, former Vice President Joe Biden, is that the latter aims to expand access to health insurance using the Affordable Care Act’s (ACA) framework, said Wilensky.

While Trump’s 2016 healthcare agenda centered around repealing the ACA, his second-term agenda doesn’t mention the law by name.

Wilensky said she’s glad that Trump did not include ACA repeal among his goals, given that “there’s no historical precedence” for eliminating the core benefits of such far-reaching legislation, now on the books for 10 years and fully implemented for 6.

Kavita Patel, MD, a primary care physician and Brookings Institution scholar in Washington, D.C., who was an advisor on the Democrats’ platform, said, “This is all just posturing and politics and almost a continuation of things [Trump’s] been saying without any real details behind it.”

Many of these items — such as ending surprise billing, lowering health insurance premiums, and cutting prescription drug prices — would have Democrats’ support “but they would get there in a different way,” Patel said.

One thing she was surprised not to see in the agenda were references to abortion or other reproductive health issues, she noted.

Insurance Coverage Neglected

Rosemarie Day, founder and CEO of Day Health Strategies and author of Marching Toward Coverage: How Women can Lead the Fight for Universal Healthcare, was dumbfounded by the overall lack of substance in the agenda, and particularly by the absence of a plan to deal with rising rates of uninsurance related to the pandemic.

Day thought the Trump campaign could have at least included a plan for returning to the “baseline” on the number of uninsured. Another administration might have chosen to promote Medicaid coverage or encourage unemployed workers to enroll on the health insurance exchanges, but not this administration, she said.

“So, they’re really just leaving people out in the cold,” Day said.

Wilensky, too, suggested it would have been “useful” for the Trump campaign to have “talked about how they envision getting more people covered.”

Paul Ginsburg, PhD, director of the USC-Brookings Schaeffer Initiative for Health Policy, said much of the agenda is “just aspirations.”

“‘Put patients and doctors in charge of our healthcare system’? … I don’t know what the policy is, [but] who’s going to quarrel with that?”

Lowering healthcare premiums also sounds “nice” but how that would be achieved is unclear, he said.

One agenda item in the document that really really irked Day was the Trump administration’s pledge to protect people who have pre-existing conditions.

“I consider the ‘covering all pre-existing conditions’ an outright lie,” she said. “I find it incredibly upsetting that [Trump] continues to say that” because he spent his first term attacking the ACA, which does protect pre-existing condition coverage.

Day also noted that the administration has repeatedly promised an ACA replacement without ever delivering an actual proposal.

Responding to the Pandemic

The Trump campaign agenda lists “eradicate COVID-19” on its bullet list, but Patel said it’s “probably not an achievable goal.” A more realistic target is to control it better.

“We have deaths every year and hospitalizations from influenza, but we have a vaccine and we have … strategies to protect people like seniors and young children,” Patel said. “That’s exactly the kind of attitude we have to take” with regard to COVID-19.

For both Patel and Ginsburg, “return to normal” is another aspiration that’s beyond the government’s power to deliver.

“So much depends on a vaccine and its acceptance and how quickly it can be produced,” Ginsburg said.

As for making all critical medicines and supplies for healthcare workers in the United States, Ginsburg acknowledged that it’s theoretically doable, but still unrealistic because it would be “way too expensive.”

“Brand name drugs are routinely produced in other countries as well as the U.S.; I wouldn’t want to upset that supply chain, especially for drugs that are in shortage,” he said.

Across four nights of a national convention that was anything but conventional, with the nominating process, acceptance speeches, and traditional pomp and circumstance forced into a virtual format due to the coronavirus pandemic, Democrats returned to the healthcare playbook widely viewed as successful in the 2018 midterm elections.

In addition to promising a more robust and concerted response to the COVID crisis gripping the nation, party leaders vowed to protect and expand the Affordable Care Act (ACA), rather than aiming to replace it with the more aggressive “Medicare for All” (M4A) approach that dominated much of the discussion during the primary campaign.

In his acceptance speech on Thursday, Democratic nominee Joseph R. Biden, Jr. promised “a healthcare system that lowers premiums, deductibles, and drug prices by building on the Affordable Care Act he’s trying to rip away,” referring to President Trump’s continued support for the full repeal of the 2010 healthcare reform law.

Earlier, progressive runner-up and vocal M4A advocate Sen. Bernie Sanders signaled a closing of the party’s ranks around Biden’s more moderate approach: “While Joe and I disagree on the best path to get to universal coverage, he has a plan that will greatly expand healthcare and cut the cost of prescription drugs. Further, he will lower the eligibility age of Medicare from 65 to 60.”

Several other speakers highlighted the need to protect the ACA’s guarantee of affordable insurance to those with preexisting conditions, most powerfully the prominent M4A crusader Ady Barkan, who suffers from amyotrophic lateral sclerosis (ALS).

“Even during this terrible crisis,” Barkan said, “Donald Trump and Republican politicians are trying to take away millions of people’s health insurance.”

Several factors will shape the financial performance of physician- and hospital-led organizations under total cost of care payment models.

Introduction

Broad consensus has long existed among public- and private-sector leaders in US healthcare that improvements in healthcare affordability will require, among other changes, a shift away from fee-for-service (FFS) payments to alternative payment models that reward quality and efficiency. The alternative payment model that has gained broadest adoption over the past ten years is the accountable care organization (ACO), in which physicians and/or hospitals assume responsibility for the total cost of care for a population of patients.

Launched by the Centers for Medicare & Medicaid Services (CMS) Innovation Center in 2012, Pioneer ACO was the first such model design to generate savings for Medicare. In this incarnation, Medicare set a benchmark for total cost of care per attributed ACO beneficiary: If total cost of care was kept below the benchmark, ACOs were eligible to share in the implied savings, as long as they also met established targets for quality of care. If total cost of care exceeded the benchmark, ACOs were required to repay the government for a portion of total cost of care above the benchmark.

Payment models similar to the one adopted by Pioneer ACOs also have been extended to other Medicare ACO programs, with important technical differences in estimates for savings and rules for the distribution of savings or losses as well as some models offering gain sharing without potential for penalties for costs exceeding the benchmark. State Medicaid programs as well as private payers (across Commercial, Medicare Advantage, and Medicaid Managed Care) also have adopted ACO-like models with similar goals and payment model structures. Of the roughly 33 million lives covered by an ACO in 2018, more than 50 percent were commercially insured and approximately 10 percent were Medicaid lives.2

On the whole, ACOs in the Medicare Shared Savings Program (MSSP) have delivered high-quality care, with an average composite score of 93.4 percent for quality metrics. However, cost savings achieved by the program have been limited: ACOs that entered MSSP during the period from January 1, 2012 to December 31, 2014, were estimated to have reduced cumulative Medicare FFS spending by $704M by 2015; after bonuses were accounted for, net savings to the Medicare program were estimated to be $144M.3 Put another way, in aggregate, savings from Medicare ACOs in 2015 represented only 0.02 percent of total Medicare spending. The savings achieved were largely concentrated among physician-led ACOs (rather than hospital-led ACOs). In fact, after accounting for bonuses, hospital-led ACOs actually had higher total Medicare spending by $112M on average over three years.4

While savings from MSSP have been relatively limited, in aggregate, numerous examples exist of ACOs that have achieved meaningful savings—in some cases in excess of 5 percent of total cost of care—with significant rewards to both themselves as well as sponsoring payers (for example, Millennium, Palm Beach, BCBSMA AQC).567 The wide disparity of performance among ACOs (and across Medicare, Medicaid, and Commercial ACO programs) raises the question of whether certain provider organizations are better suited than others to succeed under total cost of care arrangements, and whether success is dictated more by ACO model design or by structural characteristics of participating providers.

In the pages that follow, we examine these questions in two ways. First, we analyze “the math of ACOs” by isolating four factors that contribute to overall ACO profitability: bonus payments, “demand destruction,” market share gains, and operating expenses. Following these factors, we illustrate the math of ACOs through modeling of the performance of five different archetypes: physician-led ACOs; hospital-led ACOs with low ACO penetration and low leakage reduction; hospital-led ACOs with high ACO penetration; hospital-led ACOs with high leakage reduction; and hospital-led ACOs with high penetration and leakage reduction.

The Math of ACOs

In the pages that follow, we break down “the math of ACOs” into several key parameters, each of which hospital and physician group leaders could consider evaluating when deciding whether to participate in an ACO arrangement with one or more payers. Specifically, we measure the total economic value to ACO-participating providers as the sum of four factors: bonus payments, less “demand destruction,” plus market share gains, less operating costs for the ACO (Exhibit 1).

In the discussion that follows, we examine each of these factors and understand their importance to the overall profitability of ACOs, using both academic research as well as McKinsey’s experience advising and supporting payers and providers participating in ACO models.

1. Bonus payments

The premise of ACOs rests on the opportunity for payers and participating providers to share in cost savings arising from curbing unnecessary utilization and more efficient population health management, thus aligning incentives to control total cost of care. Because ACOs are designed to reduce utilization, the bonus—or share of estimated savings received by an ACO—is one factor that significantly influences ACO profitability and has garnered the greatest attention both in academic research and in private sector negotiations and deliberations over ACO participation. Bonus payments made to ACOs are themselves based on several key design elements:

The baseline and benchmark for total costs, against which savings are estimated8 ;

The shared savings rate and minimum savings/loss rates;

Risk corridors, based on caps on gains/losses and/or “haircuts” to benchmarks; and,

Frequency of rebasing, with implications for benchmark and shared savings.

1a. Baseline and benchmark

Most ACO models are grounded in a historical baseline for total cost of care, typically on the population attributed to providers participating in the ACO. Most ACO models apply an annual trend rate to the historical baseline, in order to develop a benchmark for total cost of care for the performance period. This benchmark is then used as the point of reference to which actual costs are compared for purposes of determining the bonus to be paid.

Historical baselines may be based either on one year or averaged over multiple years in order to mitigate the potential for a single-year fluctuation in total cost of care that could create an artificially high or low point of comparison in the future. Trend factors may be based on historically observed growth rates in per capita costs, or forward-looking projections, which may depart from historical trends due to changes in policy, fee schedules, or anticipated differences between past and future population health. Trend factors may be based on national projections, more market-specific projections, or even ACO-specific projections. For these and other reasons, a pre-determined benchmark may not be a good estimate of what total cost of care would have been in the absence of the ACO. As a result, estimated savings, and hence bonuses, may not reflect the true savings generated by ACOs if compared to a rigorous assessment of what otherwise would have occurred.

Recent research suggests that an ACO’s benchmark should be set using trend data from providers in similar geographic areas and/or with similar populations instead of using a national market average trend factor.9 It has been observed in Medicare (and other) populations that regions (and therefore possibly ACOs) that start at a lower-than-average cost base tend to have a higher-than-average growth trend. For example, Medicare FFS spending in low-cost regions grew at a rate 1.2 percentage points faster than the national average (2.8 percent and 1.6 percent from 2013 to 2017 compound annual growth rate, respectively). This finding is particularly relevant in low-cost rural communities, where healthcare spending grows faster than the national average.10 Based on this research, some ACO models, such as MSSP and the Next Generation Medicare ACO model, have developed benchmarks based on blending ACO-specific baselines with market-wide baselines. This approach is intended to account for the differences in “status quo” trend, which sponsoring payers may project in the absence of ACO arrangements or associated improvements in care patterns. Some model architects have advocated for this provider-market blended approach to benchmark development because they believe such an approach balances the need to reward providers who improve their own performance with a principle tenet of this model: That ACOs within a market should be held accountable to the same targets (at least in the long term).

The shared savings rate is the percentage of any estimated savings (compared with benchmark) that is paid to the ACO, subject to meeting any requirements for quality performance. For example, an ACO with a savings rate of 50 percent that outperforms its benchmark by 3 percent would keep 1.5 percent of benchmark spend. Under the array of Medicare ACO models, the shared savings rate percentage ranges anywhere from 40 percent to 100 percent.11

In some ACO models, particularly one-sided gain sharing models that do not introduce downside risk, payers impose a minimum savings rate (MSR), which is the savings threshold for an ACO to receive a payout, typically 2 percent, but can be higher or lower.12 For example, assume ACO Alpha has a savings rate of 60 percent and MSR of 1.5 percent. If Alpha overperforms the benchmark by 1 percent, there would be no bonus payout, because the total savings do not meet or exceed the MSR. If, however, Alpha overperforms the benchmark by 3 percent, Alpha would receive a bonus of 1.8 percent of benchmark (60 percent of 3 percent). An MSR is common in one-sided risk agreements to protect the payer from paying out the ACO if modest savings are a result of random variations. ACOs in two-sided risk arrangements may often choose whether to have an MSR.

Both factors impact the payout an ACO receives. Between 2012 and 2018, average earned shared savings for MSSP ACOs were between $1.0M and $1.6M per ACO (between $10 and $100 per beneficiary).13 However, while nearly two out of three MSSP ACOs in 2018 were under benchmark, only about half of them (37 percent of all MSSP ACOs) received a payout due to the MSR.14

1c. Risk corridors

In certain arrangements, payers include clauses that limit an ACO’s gains or losses to protect against extreme situations. Caps depend on the risk-sharing agreement (for example, one-sided or two-sided) as well as the shared savings/loss rate. For example, MSSP Track 1 ACOs (one-sided risk sharing) cap shared savings at the ACO’s share of 10 percent variance to the benchmark, while Track 3 ACOs (two-sided risk sharing) cap shared savings at the ACO’s share of 20 percent variance to the benchmark and cap shared losses at 15 percent variance to the benchmark.15 In contrast with these Medicare models, many Commercial and Medicaid ACO models have applied narrower risk corridors, with common ranges of 3 to 5 percent. In our experience, payers have elected to offer narrower risk corridors. Their choice is based on their desire to mitigate risk as well as the interest of some payers (and state Medicaid programs) to share in extraordinary savings that may be attributable in part to policy changes or other interventions undertaken by the payers themselves, whether in coordination with ACOs or independent of their efforts.

Payers also may vary the level of shared savings (and/or risk), between that which applies to the first dollar of savings (versus benchmark) compared with more significant savings. For example, by applying a 1 percent adjustment or “haircut” to the benchmark, a payer might keep 100 percent of the first 1 percent of savings and share any incremental savings with the ACO at a negotiated shared savings rate. Depending on what higher shared savings rate may be offered in trade for the “haircut,” such a structure has the potential to increase the incentive for ACOs to significantly outperform the benchmark. For example, an ACO that beats the benchmark by 4 percentage points and earns 100 percent of savings after 1 percentage point would net 75 percent of total estimated savings. However, under the same risk model, if the ACO were to beat the benchmark by 2 percentage points, they would only earn 50 percent of total savings. Such a structure could therefore be either more favorable or less favorable than 60 percent shared savings without a “haircut,” depending on the ACO’s anticipated performance.

1d. Frequency of rebasing

In most ACO models (including those adopted by CMS for the Medicare FFS program), the ACO’s benchmark is reset for each performance period based (at least in part) on the ACO’s performance in the immediate prior year. This approach is commonly referred to as “rebasing.” The main criticism of this approach toward ACO model design—which is also evident in capitation rate setting for Managed Care Organizations—is that ACOs become “victims of their own success”: Improvements made by the ACO in one year lead to a benchmark that is even harder to beat in the following year. The corollary is also true: An ACO with “excessive” costs in Year 1 may be setting themselves up for significant shared savings in Year 2 simply by bringing their performance back to “normal” levels.

Even in situations where ACOs show steady improvements in management of total cost of care over several years, the “ratchet” effect of rebasing can have significant implications for the share of estimated savings that flow to the ACO. Exhibit 2 illustrates the shared savings that would be captured by an ACO, if it were to mitigate trend by 2 percentage points consistently for 5 years (assumes linear growth), under a model that provides 50 percent shared savings against a benchmark that is set with annual rebasing. In this scenario, although the ACO would earn 50 percent of the savings estimated in any one year (against benchmark), the ACO would derive only 16 percent of total savings achieved relative to a “status quo” trend.

Exhibit 2

Some ACO model designs (including MSSP) have mitigated this “ratchet” effect, to some extent, by using multi-year baselines, whereby the benchmark for a given performance year is based not on the ACO’s baseline performance in the immediate prior year but over multiple prior years. This approach smooths out the effect of one-year fluctuations in performance on the benchmark for subsequent years; by implication, improvements made by an ACO in Year 1 and sustained in Year 2 create shared savings in both years. Under a three-year baseline, weighted toward the most recent year 60/30/10 percent (as applies to new contracts under the MSSP), the ACO in Exhibit 2 would capture 22 percent of total estimated savings over 5 years. If the model were instead to adopt an evenly weighted three-year baseline, that same ACO would capture 28 percent over 5 years.

In select cases, particularly in the Commercial market, payers and ACOs have agreed to multi-year prospective benchmarks. Under this approach, the benchmark for performance Years 1 to 5 (for example) are set prospectively in Year 0; the benchmarks for Years 2 and 3, for example, are not impacted by the ACO’s performance in Year 1. If this approach were to be applied to the ACO depicted in Exhibit 2, they would earn fully 50 percent of the total savings, assuming that the prospectively established 5-year benchmark was set at the “status quo” trend line. While prospective multi-year benchmarks may be more favorable to ACOs, they also increase the sensitivity of ACO performance to both the original baseline as well as the reasonableness of the prospectively applied trend rate.

Key takeaways

While in many cases healthcare organizations are highly focused on the percent of shared savings they will receive (shared savings rate), in our experience, the financial sustainability of ACO arrangements may be equally or more greatly affected by several other design parameters outlined here, among them: the inclusion of an MSR or a “haircut” to benchmark, either of which may dampen the incentive to perform; benchmark definitions including the use of provider-specific, market-specific, and/or national baseline and trend factors; and the frequency of rebasing, as implied by the use of a single-year or multi-year baseline, or the adoption of prospectively determined multi-year benchmarks.

2. Demand destruction

Although shared savings arrangements are meant to align providers’ incentives with curbing unnecessary utilization, the calculation of bonus payments based on avoided claims costs (as described in Section 1) does not account for the foregone provider revenue (and margins) attached to reductions in patient volume. The economic impact of this reduction in patient volume, sometimes referred to as “demand destruction,” is described in this section, which we address in two parts:

Foregone economic contribution based on reduced utilization in the ACO population; and,

Spillover effects from reduced utilization in the non-ACO population, based on clinical and operational changes that “spillover” from the ACO population to the non-ACO population.

2a. Foregone economic contribution

Claims paid to hospital systems for inpatient, outpatient, and post-acute facility utilization typically comprise 40 to 70 percent of total cost of care, with hospital systems that own a greater share of outpatient diagnostic lab and/or imaging and/or skilled nursing beds falling at the upper end of this range. These same categories of facility utilization may comprise 60 to 80 percent of reductions in utilization arising from improvements in population health management by an ACO. Given the high fixed costs (and correspondingly high gross margins) associated with inpatient, outpatient, and post-acute facilities, foregone facility volume could come at an opportunity cost of 30 to 70 percent of foregone revenue—that opportunity cost being the gross contribution margin associated with incremental patient volume, calculated as revenue less variable costs: Commercially insured ACO populations are more likely to fall into the upper end of this range and Medicaid populations into the lower end. This is the reason savings rates tend to be higher in the Commercial market, to offset the larger (negative) financial impact of “demand destruction.”

For example, a hospital-led ACO that mitigates total cost of care by 3 percent (or $300 based on a benchmark of $10,000 per capita) might forego $180 to $240 of revenue per patient (assuming 60 to 80 percent of savings derived from hospital services), which may represent $90 to $120 in foregone economic contribution, assuming 50 percent gross margins. As this example shows, this foregone economic contribution may represent a significant offset to any bonus paid under shared savings arrangements, unless the shared savings percentage is significantly greater than the gross margin percentage for foregone patient revenue.

For some hospitals that are capacity constrained, the lost patient volume may be replaced (that is, backfilled) with additional patient volume that may be more or less profitable depending on the payer (for example, an ACO that backfills with more profitable Commercial patients). However, the vast majority of hospitals are not traditionally capacity constrained and therefore must look to other methods (for example, growing market share) to be financially sustainable.

In contrast, physician-led ACOs have comparatively little need to consider the financial impact of “demand destruction,” given that they never benefitted from hospitalizations and thus do not lose profits from forgone care. Furthermore, primary care practices may actually experience an increase, rather than decrease, in patient revenue, based on more effective population health management. Even for multi-specialty physician practices that sponsor ACO formation, any reductions in patient volume arising from the ACO may have only modest impact on practice profitability due to narrow contribution margins attached to incremental patient volume. Physician-led ACOs may need to be concerned with “demand destruction” only to the extent that a disproportionate share of savings is derived from reductions in practice-owned diagnostics or other high-margin services; however, the savings derived from such sources are typically smaller than reductions in utilization for emergency department, inpatient, and post-acute facility utilization.

2b. Spillover effects

Though ACOs are not explicitly incentivized to reduce total cost of care of their non-ACO populations (including FFS), organizations often see increased efficiency across their full patient population after becoming an ACO. For example, research over the last decade has found reductions in spend for non-ACO lives between 1 and 3 percent (Exhibit 3).

Exhibit 3

The impact of spillover effects on an ACO’s profitability depends on the proportion of ACO and non-ACO lives that comprise a provider’s patient panel. Further, impact also depends on the ACO’s ability to implement differentiated processes for ACO and non-ACO lives to limit the spillover of the efficiencies. Although conventional wisdom implies that physicians will not discriminate their clinical practice patterns based on the type of payer (or payment), nonetheless many examples exist of hospitals and other providers with the ability to differentiate processes based on payer or payment type. For example, many hospitals deploy greater resources to discharge planning or initiate the process earlier for patients reimbursed under a Diagnosis Related Group (case rate) than for those reimbursed on a per diem or percent of charges model. Moreover, ACOs and other risk-bearing entities routinely direct care management activities disproportionately or exclusively toward patients for whom they have greater financial accountability for quality and/or efficiency. For physician-led ACOs, differentiating resource deployment between ACO- and non-ACO populations may be necessary to achieve a return on investment for new care management or other population health management activities. For hospital sponsors of ACOs that continue to derive the majority of their revenue from FFS populations outside the ACO, differentiating population health management efforts across ACO and FFS populations are of paramount importance to overall financial sustainability. To the extent that hospital-led ACOs are unable to do so, they may find total cost of care financial arrangements to be financially sustainable only if extended to the substantial majority of their patient populations in order to reduce the severity of any spillover effects.

Key takeaways

The adverse impact of “demand destruction” is what most distinguishes the math of hospital-led ACOs from that of physician-led ACOs. The structure of ACO-sponsoring hospitals—whether they own post-acute assets, for example—further shapes the severity of demand destruction, which then provides a point of reference for determining what shared savings percentage may be necessary to overcome the impact of demand destruction. Though in the long term, hospitals may be able to right size capacity, in the near term when deciding to become an ACO, there is often limited ability to alter the fixed-cost base. Finally, the extent of “spillover effects” from the ACO to the non-ACO population further impacts the financial sustainability of hospital-led ACOs. Hospital-led ACOs can seek to minimize the impact through 1) differentiating processes between the two populations, and/or 2) transitioning the substantial majority of their patient population into ACO arrangements.

3. Market share gains

Providers can further improve profitability through market share gains, specifically:

Reduced system leakage through improved alignment of referring physicians across both ACO and non-ACO patients; and,

Improved network status as an ACO.

3a. Reduced system leakage

ACOs can grow market share by coordinating patients within the system (that is, reduce leakage) to better manage total cost of care and quality. This coordination is often accomplished by improving the provider’s alignment with the referring physician; for example, ACOs can establish a comprehensive governance structure and process around network integrity, standardize the referral process between physicians and practices, and improve physician relationships within, and with awareness of, the network. Furthermore, ACOs can develop a process to ensure that a patient schedules follow-up appointments before leaving the physician’s office, optimizing the scheduling system and call center.

Stark Laws (anti-kickback regulations) have historically prevented systems from giving physicians financial incentives to reduce leakage. While maintaining high-quality standards, ACOs are given a waiver to this law and therefore are allowed to pursue initiatives that improve network integrity to better coordinate care for patients. In our experience, hospitals generally experience 30 to 50 percent leakage (Exhibit 4), but ACOs can improve leakage by 10 to 30 percent.

Exhibit 4

3b. Improved network status

In some instances for Commercial payers, an ACO may receive preferential status within a network by entering into a total cost of care arrangement with a payer. As a result, the ACO would see greater utilization, which will improve profitability. For example, in 2012, the Cooley Dickinson Hospital (CDH) and Cooley Dickinson Physician Hospital Organization, a health system in western Massachusetts with 66 primary care providers and 160 specialists, joined Blue Cross Blue Shield of Massachusetts’ (BCBSMA) Alternative Quality Contract (AQC), which established a per-patient global budget to cover all services and expenses for its Commercial population. As a result of joining the AQC, reducing the prices charged for services, and providing high quality of care, CDH was “designated as a high-value option in the Western Mass. Region,” which meant BCBSMA members with certain plans “[paid] less out-of-pocket when they [sought] care” at CDH.16 Other payers have also established similar mutually beneficial offerings to providers who assume more accountability for care.1718 An ACO can benefit from these arrangements up until most or all other provider systems in the same market join.

Key takeaways

These factors to improve market share (at lower cost and better quality) can help an ACO compensate for any lost profits from “demand destruction” (foregone profits and spillover effects) and increased operating costs. The opportunity from this factor, which requires initiatives that focus on reducing leakage, can be the difference between a net-neutral hospital-led ACO and a significantly profitable ACO. An example initiative would be performance management systems that analyze physician referral patterns.

4. Operating costs

Finally, profitability is impacted by operating costs or any additional expenses associated with running an ACO. These costs generally are lower for physician-led ACOs than for hospital-led ACOs (and also depend on buy-versus-build decisions). In our experience, operating costs to run an ACO vary widely depending on the provider’s operating model, cost structure (for example, existing personnel, IT capabilities), and ACO patient population (for example, number and percent of ACO lives). However, we will focus on three specific types of costs:

Care management costs, often variable, or a marginal expense for every life;

Data and analytics operating costs, which can vary widely depending on whether the ACO builds or buys this capability; and

Additional administrative costs, which are fixed or independent of the number of lives.

4a. Care management costs

In our experience, care management costs to operate an ACO range from 0.5 to 2.0 percent of total cost of care for a given ACO population. These care management costs include ensuring patients with chronic conditions are continuously managing those conditions and coordinating with physician teams to improve efficacy and efficiency of care. A core lever of success involves reducing use of unnecessary care. ACOs that spend closer to 2 percent and/or those whose efforts focus on expanding care coordination for high-risk patients struggle to achieve enough economic contribution to break even. This is because care coordination (devoting more resources to testing and treating patients with chronic disease) often does not have a positive return on investment.19 ACOs that do this effectively and ultimately spend less on care management (around 0.5 percent of the total cost of care) tend to create value primarily through curbing unnecessary utilization and steering patients toward more efficient facilities rather than managing chronic conditions. This value creation is particularly true for Commercial ACO contracts, where there is greater price variation across providers compared with Medicare and Medicaid contracts, where pricing is standardized.

4b. Data and analytics operating costs

Data and analytics operating costs are critical to supporting ACO effectiveness. For example, high-performing ACOs prioritize data interoperability across physicians and hospitals and constantly analyze electronic health records and claims data to identify opportunities to better manage patient care and reduce system leakage. ACOs can either build or license data and analytics tools, a decision that often depends on the number of ACO lives. In our experience, an ACO that decides to build its own data and analytics solutions in-house will on average invest around $24M for upfront development, amortized over 8 years for $3M per year, plus $6M in annual costs (for example, using data scientists and analysts to generate insights from the data), for a total of $9M per year. Alternatively, ACOs can license analytics software on a per-patient basis, typically costing 0.5 to 1.5 percent of the total cost of care. Thus, we find the breakeven point at around 100,000 covered ACO lives; therefore, it often makes financial sense for ACOs with more than 100,000 lives to build in-house.

4c. Additional administrative costs

Organizations must also invest in personnel to operate an ACO, typically including an executive director, head of real estate, head of care management, and lawyers and actuaries. The ACO leadership team’s responsibilities often include setting the ACO’s strategy (for example, target markets, lines of business, services offered, through which physicians and hospitals) and developing, managing, and communicating with the physician network to support continuity of care.

Key takeaways

Operating costs to run an ACO are significant. Ability to find ways to invest in fixed costs that are more transformational in nature may result in lower near-term profitability but can provide a greater return on investment in the long term both for the ACO and the rest of the system. The decision to make these investments is dependent on the number of lives covered by an individual ACO.

ACO Archetypes

Drawing on the analysis outlined above, we conducted scenario modeling of “the math of ACOs” using five different ACO archetypes, which vary in structure and performance under a common set of rules. These five archetypes include:

Typical physician-led ACO

Hospital-led ACO with low ACO penetration and low leakage reduction

Hospital-led ACO with high ACO penetration

Hospital-led ACO with high leakage reduction

Hospital-led ACO with high leakage reduction and high ACO penetration

Subsequently, taking an ACO’s structure as a given, we describe for each ACO archetype the key model design parameters and other strategic and operational choices that ACOs might make to maximize their performance.

Comparision of archetypes based on scenario modeling

Summarizing the four factors, the profitability of each archetype reveals certain insights (Exhibit 5).

Earlier this year, when public schools in Kansas City, Missouri, shut down in-person instruction because of the COVID-19 pandemic, Nika Cotton quit her job in social work to start her own business. She has two young children — ages 8 and 10 — and no one to watch them if she were to continue working a traditional job.

It was a big decision, made weightier by the loss of her employer-sponsored health insurance. But on August 5, Cotton awoke to the news that Missouri voters had narrowly approved the expansion of the state’s Medicaid program via ballot initiative, making it the second politically right-leaning state to do so during the pandemic. The expansion opens Medicaid eligibility to individuals and families with incomes up to 138% of the federal poverty guidelines, which are $12,760 for an individual and $21,720 for a family of three, allowing Cotton’s family of three to qualify.

“It takes a lot of stress off of my shoulders with having to think about how I’m going to take care of myself, how I’m going to be able to go and see a doctor and get the health care I need while I’m starting my business,” she told Alex Smith of KCUR, the NPR affiliate in Kansas City.

Nearly 1,264,000 voters weighed in on the measure, with 53% voting for it and 47% against it. Missouri’s Republican governor Mike Parson opposed it, arguing that the state could not afford the coverage expansion — even though the federal government pays 90% of the costs and a fiscal analysis (PDF) by the Center for Health Economics and Policy at Washington University estimated that the state would save $39 million if it implemented Medicaid expansion in 2020.

The ballot measure requires the state to expand Medicaid by July 2021, and an estimated 230,000 residents with low incomes will become eligible for affordable health coverage.

Voters Signal Support

In late June, Oklahoma voters also approved Medicaid expansion by ballot measure, eking out a victory by less than one percentage point.

“It is difficult to ignore that these ballot initiatives passed in right-leaning states in the middle of the coronavirus pandemic, when millions of Americans have lost their jobs and, with them, their employer-sponsored health insurance,”Dylan Scott wrote in Vox. “This is partly a coincidence — the signatures were collected to put the Medicaid expansion questions on the ballot long before COVID-19 ever arrived in the US — but the relatively narrow margins made me wonder if the pandemic and its economic and medical consequences proved decisive.”

Earlier this year, Scott spoke to Cynthia Cox, MPH, director of the Peterson-Kaiser Health System Tracker, about the potential impact of the pandemic on health care politics. “Many of the biggest coverage expansions both in the US and in similar countries happened in the context of wars and social upheavals, as well as financial crises,” Cox said. “One theory is that those circumstances redefine social solidarity, thus expanding views of the role of government.”

Between February and May, Missouri’s Medicaid program saw enrollment rise nearly 9%, one of the largest increases nationwide during the pandemic,Rachel Roubein reported in Politico. During that same period, Oklahoma’s Medicaid program saw enrollment increase by about 6%.

States that implemented Medicaid expansion are better positioned to respond to COVID-19, according to a report by the Center on Budget and Policy Priorities (CBPP). These states entered the health crisis and resulting economic downturn with lower uninsured rates, which is important for public health “because people who are uninsured may forgo testing or treatment for COVID-19 due to concerns that they cannot afford it, endangering their health while slowing detection of the virus’ spread,” the authors wrote.

CBPP and KFF estimate that 3.6 to 4.4 million uninsured adults would become eligible for Medicaid coverage if the 12 states that have not yet expanded the program did so. Those states are Alabama, Florida, Georgia, Kansas, Mississippi, North Carolina, South Carolina, South Dakota, Tennessee, Texas, Wisconsin, and Wyoming.

Coverage for Frontline Essential Workers

Medicaid is particularly important for frontline essential workers — such as those working in grocery stores, meat processing plants, and nursing homes — during the pandemic. Their jobs require them to report in person, increasing their risk of getting sick with the coronavirus as they interact with coworkers and, in many cases, with customers and patients. Essential workers are often paid low wages and not offered employer-sponsored health insurance or can’t afford the premiums for it.

About 5 million essential workers nationwide get health coverage through Medicaid, “including nearly 1.8 million people working in frontline health care services and 1.6 million in other frontline essential services including transportation, waste management, and child care,” Matt Broaddus, senior research analyst at CBPP, wrote on the center’s blog.

In California, over 950,000 essential workers are enrolled in Medi-Cal, the state’s Medicaid program. People of color are overrepresented in many categories of essential jobs. According to a UC Berkeley Labor Center analysis of the 15 largest frontline essential occupations, Latinx workers are overrepresented in agriculture, construction, and food preparation, among other occupations. Asian workers are overrepresented among registered nurses and personal care aides; and Black workers are overrepresented among personal care aides, laborers and material movers, and office clerks.

In addition to low-wage workers, Medi-Cal continues to bridge the coverage gap for other key populations amid the COVID-19 crisis, which is magnifying historical health inequities. (Medi-Cal covers nearly 40% of the state’s children, half of Californians with disabilities, and over one million seniors. For a refresher on the program, see CHCF’s Medi-Cal Explained series.)

Even though Missouri’s Medicaid expansion won’t take effect for another year, Nika Cotton remains excited. “It’s better late than never,” she said. “The fact that it’s coming is better than nothing” — perhaps a takeaway for the remaining 12 states.