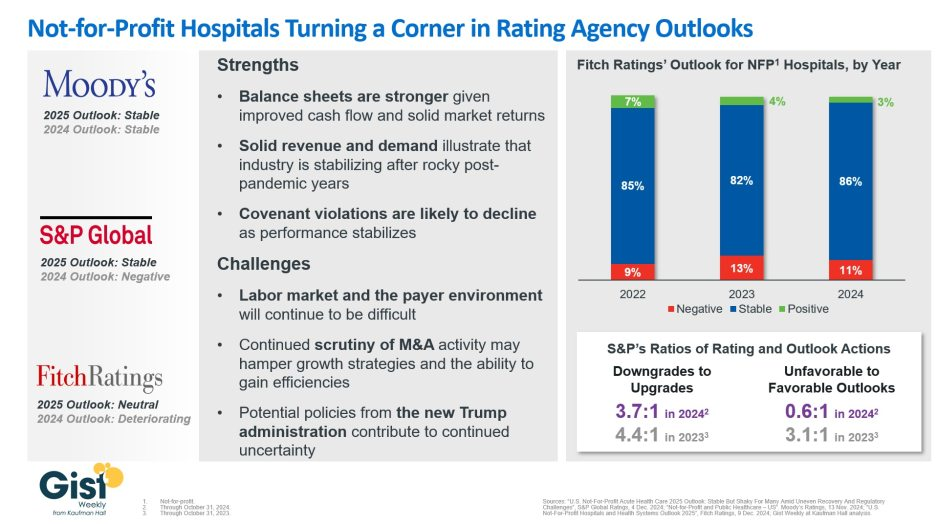

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

In mid-January, General Catalyst (GC) and Summa Health announced the signing of a non-binding LOI for GC to acquire Summa, which, if consummated, would be a groundbreaking transaction. Summa Health is a vertically integrated not-for-profit health system located in Akron, Ohio that operates acute care hospitals, a network of health care services, a physician group practice, and a health plan. Like much of the health system sector, Summa has found the operating environment for the past couple of years to be challenging.

GC is a venture capital firm that had approximately $25B in assets under management at the end of 2022, across a dozen fund families and a number of sectors, including its Health Assurance funds, that have a stated mission of “creating a more proactive, affordable & equitable system of care.”

Health Assurance has investments in more than 150 digital health companies worldwide and has implemented working relationships with more than a dozen of the country’s most noteworthy health systems and hospital operators.

In October, GC announced the formation of a new venture called the Health Assurance Transformation Corporation (HATCo), for the purpose of providing financial and operational advisory assistance to health systems, including using GC’s suite of digital health companies. At that time, HATCo announced plans to buy a health system in order to drive transformation in the delivery of care by leveraging technology, updating workforce/staffing models, and becoming more proactive in creating revenue streams for health systems.

Their plans included an intent to streamline operations and find efficiencies using technology, as well as implementing value-based payment models, including fully capitated risk contracts to incentivize better utilization management, an initiative that requires significant data analytics.

GC had been looking for a system with market relevance and a sweet spot in terms of size – big enough to have a full complement of services, but nimble enough to accept significant change. In Summa, it has also found a system that maintains its own health plan, which GC can use to help accelerate the shift to capitated models.

The transaction that Summa and GC are contemplating is a new and innovative attempt at addressing the underlying problems that plague the acute care industry.

In particular, 1) a continued reliance on fee-for-service revenue when reimbursement has been pressured from every angle and rate increases have failed to keep pace with the rising cost of providing care, 2) capital to fund a growing list of competing needs, and 3) the challenges of staffing for quality in a tight market for clinical labor. Summa appears to be banking on the idea that GC and the data- and technology driven solutions that reside within their portfolio companies can ease those pressures.

HATCo’s proposed purchase of Summa requires a conversion of the health system to for profit. The purchase price of the health system will contribute to the corpus for a large foundation that will address social determinants of health in the Akron community, and the operating entities would become subsidiaries of HATCo.

HATCo has stated publicly that it will continue Summa’s existing charity care commitment, that Summa’s existing management team will stay in place, and the health system Board will continue to have local community representation. HATCo has also emphasized that it plans to hold Summa for an extended period and have it serve as a digital innovation testing ground and incubation site for new healthcare IT, where it believes that aligning incentives will drive financial improvement and better care.

Innovative approaches to meaningful problems should be applauded but there is skepticism.

Will bottom line pressures affect the quality of care?

Will the typical investment horizon of venture capital align with the time frames needed to prove these solutions are taking hold?

Health system evolution has traditionally been measured in decades, rather than the 5-7 year hold periods that private capital prefers. There are also perceived conflicts to consider as Summa will be paying the GC-owned companies for their services. Acute care hospitals are central elements of their communities and their constituents are broader than most companies, often including large workforces, union leadership, politicians, government regulators, and of course patients and their families.

This transaction will receive significant scrutiny with any number of constituents taking issue with a health system’s purchase by a venture capital firm. One hurdle is the conversion process itself, which requires review and approval by the Ohio Attorney General and regulators may want to impose restrictions on GCs ability to operate that are incompatible with its plans. The hurdles to closing are daunting, but the challenges facing health systems are equally daunting.

And while this proposed combination may not come to fruition, the need for innovative solutions remains.

If you’re a U.S. health industry watcher, it would appear the $4.5 trillion system is under fire at every corner.

Pressures to lower costs, increase accessibility and affordability to all populations, disclose prices and demonstrate value are hitting every sector. Complicating matters, state and federal legislators are challenging ‘business as usual’ seeking ways to spend tax dollars more wisely with surprisingly strong bipartisan support on many issues. No sector faces these challenges more intensely than hospitals.

In 2022 (the latest year for NHE data from CMS), hospitals accounted for 30.4% of total spending ($1.35 trillion. While total healthcare spending increased 4.1% that year, hospital spending was up 2.2%–less than physician services (+2.7%), prescription drugs (+8.4%), private insurance (+5.9%) and the overall inflation rate (+6.5%) and only slightly less than the overall economy (GDP +1.9%). Operating margins were negative (-.3%) because operating costs increased more than revenues (+7.7% vs. 6.5%) creating deficits for most. Hardest hit: the safety net, rural hospitals and those that operate in markets with challenging economic conditions.

In 2023, the hospital outlook improved. Pre-Covid utilization levels were restored. Workforce tensions eased somewhat. And many not-for-profits and investor-owned operators who had invested their cash flows in equities saw their non-operating income hit record levels as the S&P 500 gained 26.29% for the year.

In 2024, the S&P is up 5.15% YTD but most hospital operators are uncertain about the future, even some that appear to have weathered the pandemic storm better than others. A sense of frustration and despair is felt widely across the sector, especially in critical access, rural, safety net, public and small community hospitals where long-term survival is in question.

The cynicism felt by hospitals is rooted in four conflicts in which many believe hospitals are losing ground:

Hospitals vs. Insurers:

Insurers believe hospitals are inefficient and wasteful, and their business models afford them the role of deciding how much they’ll pay hospitals and when based on data they keep private. They change their rules annually to meet their financial needs. Longer-term contracts are out of the question. They have the upper hand on hospitals.

Hospitals take financial risks for facilities, technologies, workforce and therapies necessary to care. Their direct costs are driven by inflationary pressures in their wage and supply chains outside their control and indirect costs from regulatory compliance and administrative overhead, Demand is soaring. Hospital balance sheets are eroding while insurers are doubling down on hospital reimbursement cuts to offset shortfalls they anticipate from Medicare Advantage. Their finances and long-term sustainability are primarily controlled by insurers. They have minimal latitude to modify workforces, technology and clinical practices annually in response to insurer requirements.

Hospitals vs. the Drug Procurement Establishment:

Drug manufacturers enjoy patent protections and regulatory apparatus that discourage competition and enable near-total price elasticity. They operate thru a labyrinth of manufacturers, wholesalers, distributors and dispensers in which their therapies gain market access through monopolies created to fend-off competition. They protect themselves in the U.S. market through well-funded advocacy and tight relationships with middlemen (GPOs, PBMs) and it’s understandable: the global market for prescription drugs is worth $1.6 trillion, the US represents 27% but only 4% of the world population.

And ownership of the 3 major PBMs that control 80% of drug benefits by insurers assures the drug establishment will be protected.

Prescription drugs are the third biggest expense in hospitals after payroll and med/surg supplies. They’re a major source of unexpected out-of-pocket cost to patients and unanticipated costs to hospitals, especially cancer therapies. And hospitals (other than academic hospitals that do applied research) are relegated to customers though every patient uses their products.

Prescription drug cost escalation is a threat to the solvency and affordability of hospital care in every community.

Hospitals vs. the FTC, DOJ and State Officials:

Hospital consolidation has been a staple in hospital sustainability and growth strategies. It’s a major focus of regulator attention. Horizontal consolidation has enabled hospitals to share operating costs thru shared services and concentrate clinical programs for better outcomes. Vertical consolidation has enabled hospitals to diversify as a hedge against declining inpatient demand: today, 200+ sponsor health insurance plans, 60% employ physicians directly and the majority offer long-term, senior care and/or post-acute services. But regulators like the FTC think hospital consolidation has been harmful to consumers and third-party data has shown promised cost-savings to consumers are not realized.

Federal regulators are also scrutinizing the tax exemptions afforded not-for-profit hospitals, their investment strategies, the roles of private equity in hospital prices and quality and executive compensation among other concerns. And in many states, elected officials are building their statewide campaigns around reining in “out of control” hospitals and so on.

Bottom line: Hospitals are prime targets for regulators.

Hospitals vs. Congress:

Influential members in key House and Senate Committees are now investigating regulatory changes that could protect rural and safety net hospitals while cutting payments to the rest. In key Committees (Senate HELP and Finance, House Energy and Commerce, Budget), hospitals are a target. Example: The Lower Cost, More Transparency Act passed in the the House December 11, 2023. It includes price transparency requirements for hospitals and PBMs, site-neutral payments, additional funding for rural and community health among more. The American Hospital Association objected noting “The AHA supports the elimination of the Medicaid disproportionate share hospital (DSH) reductions for two years. However, hospitals and health systems strongly oppose efforts to include permanent site-neutral payment cuts in this bill. In addition, the AHA has concerns about the added regulatory burdens on hospitals and health systems from the sections to codify the Hospital Price Transparency Rule and to establish unique identifiers for off-campus hospital outpatient departments (HOPDs).” Nonetheless, hospitals appear to be fighting an uphill battle in Congress.

Hospitals have other problems:

Threats from retail health mega-companies are disruptive. The public’s trust in hospitals has been fractured. Lenders are becoming more cautious in their term sheets. And the hospital workforce—especially its doctors and nurses—is disgruntled. But the four conflicts above seem most important to the future for hospitals.

However, conflict resolution on these is problematic because opinions about hospitals inside and outside the sector are strongly held and remedy proposals vary widely across hospital tribes—not-for profits, investor-owned, public, safety nets, rural, specialty and others.

Nonetheless, conflict resolution on these issues must be pursued if hospitals are to be effective, affordable and accessible contributors and/or hubs for community health systems in the future. The risks of inaction for society, the communities served and the 5.48 million (NAICS Bureau of Labor 622) employed in the sector cannot be overstated. The likelihood they can be resolved without the addition of new voices and fresh solutions is unlikely.

PS: In the sections that follow, citations illustrate the gist of today’s major message: hospitals are under attack—some deserved, some not. It’s a tough business climate for all of them requiring fresh ideas from a broad set of stakeholders.

PS If you’ve been following the travails of Mission Hospital, Asheville NC—its sale to HCA Healthcare in 2019 under a cloud of suspicion and now its “immediate jeopardy” warning from CMS alleging safety and quality concerns—accountability falls squarely on its Board of Directors. I read the asset purchase agreement between HCA and Mission: it sets forth the principles of operating post-acquisition but does not specify measurable ways patient safety, outcomes, staffing levels and program quality will be defined. It does not appear HCA is in violation with the terms of the APA, but irreparable damage has been done and the community has lost confidence in the new Mission to operate in its best interest. Sadly, evidence shows the process was flawed, disclosures by key parties were incomplete and the hospital’s Board is sworn to secrecy preventing a full investigation.

The lessons are 2 for every hospital:

Boards must be prepared vis a vis education, objective data and independent counsel to carry out their fiduciary responsibility to their communities and key stakeholders. And the business of running hospitals is complex, easily prone to over-simplification and misinformation but highly important and visible in communities where they operate.

Business relationships, price transparency, board performance, executive compensation et al can no longer to treated as private arrangements.

With input from stakeholders across the industry, Modern Healthcare outlines six challenges health care is likely to face in 2023—and what leaders can do about them.

1. Financial difficulties

In 2023, health systems will likely continue to face financial difficulties due to ongoing staffing problems, reduced patient volumes, and rising inflation.

According to Tina Wheeler, U.S. health care leader at Deloitte, hospitals can expect wage growth to continue to increase even as they try to contain labor costs. They can also expect expenses, including for supplies and pharmaceuticals, to remain elevated.

Health systems are also no longer able to rely on federal Covid-19 relief funding to offset some of these rising costs. Cuts to Medicare reimbursement rates could also negatively impact revenue.

“You’re going to have all these forces that are counterproductive that you’re going to have to navigate,” Wheeler said.

In addition, Erik Swanson, SVP of data and analytics at Kaufman Hall, said the continued shift to outpatient care will likely affect hospitals’ profit margins.

“The reality is … those sites of care in many cases tend to be lower-cost ways of delivering care, so ultimately it could be beneficial to health systems as a whole, but only for those systems that are able to offer those services and have that footprint,” he said.

2. Health system mergers

Although hospital transactions have slowed in the last few years, market watchers say mergers are expected to rebound as health systems aim to spread their growing expenses over larger organizations and increase their bargaining leverage with insurers.

“There is going to be some organizational soul-searching for some health systems that might force them to affiliate, even though they prefer not to,” said Patrick Cross, a partner at Faegre Drinker Biddle & Reath. “Health systems are soliciting partners, not because they are on the verge of bankruptcy, but because they are looking at their crystal ball and not seeing an easy road ahead.”

Financial challenges may also lead more physician practices to join health systems, private-equity groups, larger practices, or insurance companies.

“Many independent physicians are really struggling with their ability to maintain their independence,” said Joshua Kaye, chair of U.S. health care practice at DLA Piper. “There will be a fair amount of deal activity. The question will be more about the size and specialty of the practices that will be part of the next consolidation wave.”

3. Recruiting and retaining staff

According to data from Fitch Ratings, health care job openings reached an all-time high of 9.2% in September 2022—more than double the average rate of 4.2% between 2010 and 2019. With this trend likely to continue, organizations will need to find effective ways to recruit and retain workers.

Currently, some organizations are upgrading their processes and technology to hire people more quickly. They are also creating service-level agreements between recruiting and hiring teams to ensure interviews are scheduled within 48 hours or decisions are made within 24 hours.

Eric Burch, executive principal of operations and workforce services at Vizient, also predicted that there will be a continued need for contract labors, so health systems will need to consider travel nurses in their staffing plans.

“It’s really important to approach contract labor vendors as a strategic partner,” Burch said. “So when you need the staff, it’s a partnership and they’re able to help you get to your goals, versus suddenly reaching out to them and they don’t know your needs when you’re in crisis.”

When it comes to retention, Tochi Iroku-Malize, president of the American Academy of Family Physicians (AAFP), said health systems are adequately compensated for their work and have enough staff to alleviate potential burnout.

AAFP also supports legislation to streamline prior authorization in the Medicare Advantage program and avoid additional cuts to Medicare payments, which will help physicians provide care to patients with less stress.

4. Payer-provider contract disputes

A potential recession, along with the ensuing job cuts that typically follow, would limit insurers’ commercial business, which is their most profitable product line. Instead, many people who lose their jobs will likely sign up for Medicaid plans, which is much less profitable.

Because of increased labor, supply, and infrastructure costs, Brad Ellis, senior director at Fitch Ratings, said providers could pressure insurers into increasing the amount they pay for services. This will lead insurers to passing these increased costs onto members’ premiums.

Currently, Ellis said insurers are keeping an eye on how legislators finalize rules to implement the No Surprise Act’s independent resolution process. Regulators will also begin issuing fines for payers who are not in compliance with the law’s price transparency requirement.

5. Investment in digital health

Much like 2022, investment in digital health is likely to remain strong but subdued in 2023.

“You’ll continue to see layoffs, and startup funding is going to be hard to come by,” said Russell Glass, CEO of Headspace Health.

However, investors and health care leaders say they expect a strong market for digital health technology, such as tools for revenue cycle management and hospital-at-home programs.

According to Julian Pham, founding and managing partner at Third Culture Capital, he expects corporations such as CVS Health to continue to invest in health tech companies and for there to be more digital health mergers and acquisitions overall.

In addition, he predicted that investors, pharmaceutical companies, and insurers will show more interest in digital therapeutics, which are software applications prescribed by clinicians.

“As a physician, I’ve always dreamed of a future where I could prescribe an app,” Pham said. “Is it the right time? Time will tell. A lot needs to happen in digital therapeutics and it’s going to be hard.”

6. Health equity efforts

This year, CMS will continue rolling out new health equity initiatives and quality measurements for providers and insurers who serve marketplace, Medicare, and Medicaid beneficiaries. Some new quality measures include maternal health, opioid related adverse events, and social need/risk factor screenings.

CMS, the Joint Commission, and the National Committee for Quality Assurance are also partnering together to establish standards for health equity and data collection.

In addition, HHS is slated to restore a rule under the Affordable Care Act that prohibits discrimination based on a person’s gender identity or sexual orientation. According to experts, this rule may conflict with recently passed state laws that ban gender-affirming care for minors.

“It’s something that’s going to bear out in the courts and will likely lack clarity. We’ll see differences in what different courts decide,” said Lindsey Dawson, associate director of HIV policy and director of LGBTQ health policy at the Kaiser Family Foundation. “The Supreme Court acknowledged that there was this tension. So it’s an important place to watch and understand better moving forward.”

Radio Advisory’s Rachel Woods sat down with Advisory Board‘s Aaron Mauck and Natalie Trebes to talk about where leaders need to focus their attention on longer-term industry challenges—like growing competition, behavioral health infrastructure, and finding success in value-based care.

Rachel Woods: So I’ve been thinking about the last conversation that we had about what executives need to know to be prepared to be successful in 2023, and I feel like my big takeaway is that the present feels aggressively urgent. The business climate today is extraordinarily tough, there are all these disruptive forces that are changing the competitive landscape, right? That’s where we focused most of our last conversation.

But we also agreed that those were still kind of near-term problems. My question is why, if things feel like they are in such a crisis, do we need to also focus our attention on longer term challenges?

Aaron Mauck: It’s pretty clear that the business environment really isn’t sustainable as it currently stands, and there’s a tendency, of course, for all businesses to focus on the urgent and important items at the expense of the non-urgent and important items. And we have a lot of non-urgent important things that are coming on the horizon that we have to address.

Obviously, you think about the aging population. We have the baby boom reaching an age where they’re going to have multiple care needs that have to be addressed that constitute pretty significant challenges. That aging population is a central concern for all of us.

Costly specialty therapeutics that are coming down the pipeline that are going to yield great results for certain patient segments, but are going to be very expensive. Unmanaged behavioral needs, disagreements around appropriate spending. So we have lots of challenges, myriad of challenges we’re going to have to address simultaneously.

Natalie Trebes: Yeah, that’s right. And I would add that all of those things are at threshold moments where they are pivoting into becoming our real big problems that are very soon going to be the near term problems. And the environment that we talked about last time, it’s competitive chaos that’s happening right now, is actually the perfect time to be making some changes because all the challenges we’re going to talk about require really significant restructuring of how we do business. That’s hard to do when things are stable.

Woods: Yes. But I still think you’re going to get some people who disagree. And let me tell you why. I think there’s two reasons why people are going to disagree. The first reason is, again, they are dealing with not just one massive fire in front of them, but what feels like countless massive fires in front of them that’s just demanding all of their strategic attention. That was the first thing you said every executive needs to know going into this year, and maybe not know, but accept, if I’m thinking about the stages of grief.

But the second reason why I think people are going to push back is the laundry list of things that Aaron just spoke of are areas where, I’m not saying the healthcare industry shouldn’t be focused on them, but we haven’t actually made meaningful progress so far.

Is 2023 actually the year where we should start chipping away at some of those huge industry challenges? That’s where I think you’re going to get disagreement. What do you say to that?

Trebes: I think that’s fair. I think it’s partly that we have to start transforming today and organizations are going to diverge from here in terms of how they are affected. So far, we’ve been really kind of sharing the pain of a lot of these challenges, it’s bits and pieces here. We’re all having to eat a little slice of this.

I think different organizations right now, if they are careful about understanding their vulnerabilities and thinking about where they’re exposed, are going to be setting themselves up to pass along some of that to other organizations. And so this is the moment to really understand how do we collectively want to address these challenges rather than continue to try to touch as little of it as we possibly can and scrape by?

Woods: That’s interesting because it’s also probably not just preparing for where you have vulnerabilities that are going to be exposed sooner rather than later, but also where might you have a first mover advantage? That gets back to what you were talking about when it comes to the kind of competitive landscape, and there’s probably people who can use these as an opportunity for the future.

Mauck: Crises are always opportunities and even for those players across the healthcare system who have really felt like they’re boxers in the later rounds covering up under a lot of blows, there’s opportunities for them to come back and devise strategies for the long term that really yield growth.

We shouldn’t treat this as a time just of contraction. There are major opportunities even for some of the traditional incumbents if they’re approaching these challenges in the right fashion. When we think about that in terms of things like labor or care delivery models, there’s huge opportunities and when I talk with C-suites from across the sector, they recognize those opportunities. They’re thinking in the long term, they need to think in the long term if they’re going to sustain themselves. It is a time of existential crisis, but also a time for existential opportunity.

Trebes: Yeah, let’s be real, there is a big risk of being a first mover, but there is a really big opportunity in being on the forefront of designing the infrastructure and setting the table of where we want to go and designing this to work for you. Because changes have to happen, you really want to be involved in that kind of decision making.

Woods: And in the vein of acceptance, we should all accept that this isn’t going to be easy. The challenges that I think we want to focus on for the rest of this conversation are challenges that up to this point have seemed unsolvable. What are the specific areas that you think should really demand executive attention in 2023?

Trebes: Well, I think they break into a few different categories. We are having real debates about how do we decide what are appropriate outcomes in healthcare? And so the concept of measuring value and paying for value. We have to make some decisions about what trade-offs we want to make there, and how do we build in health equity into our business model and do we want to make that a reality for everyone?

Another category is all of the expensive care that we have to figure out how to deliver and finance over the coming years. So we’re talking about the already inadequate behavioral health infrastructure that’s seen a huge influx in demand.

We’re talking about what Aaron mentioned, the growing senior population, especially with boomers getting older and requiring a lot more care, and the pipeline of high-cost therapies. All of this is not what we are ready as the healthcare system as it exists today to manage appropriately in a financially sustainable way. And that’s going to be really hard for purchasers who are financing all of this.

There is no shortage of challenges to confront in healthcare today, from workforce shortages and burnout to innovation and health equity (and so much more). We’re committed to giving industry leaders a platform for sharing best practices and exchanging ideas that can improve care, operations and patient outcomes.

Check out this podcast interview with Ketul J. Patel, CEO at Virginia Mason Franciscan Health and division president, Pacific Northwest at CommonSpirit Health, for his insights on where healthcare is headed in the future.

In this episode, we are joined by Ketul J. Patel, Division President, Pacific Northwest; Chief Executive Officer, CommonSpirit Health; Virginia Mason Franciscan Health, to discuss his background & what led him to executive healthcare leadership, challenges surrounding workforce shortages, the importance of having a strong workplace culture, and more.

Edward Karlovich serves as the executive vice president and CFO for UPMC, a $23 billion provider and insurer based in Pittsburgh.

Since joining UPMC in 1990, Mr. Karlovich has served in several financial leadership roles. Most recently, he was vice president, CFO and chief of staff for UPMC’s Health Services Division. He became CFO of the entire integrated system with 40 hospitals in October 2020, after serving on an interim basis for about a year.

Here, Mr. Karlovich shares with Becker’s the skills he thinks CFOs need to succeed today, some key capital projects in the works at UPMC and his organization’s top financial priorities.

Editor’s note: Responses were lightly edited for length and clarity.

Question: What is the most pressing issue facing hospital CFOs due to COVID-19?

Edward Karlovich: I would say the most pressing issue for me is disruption. COVID-19 has done many things to disrupt the way we think about our organization and business. Some disruptions we faced in the last year include staffing and supply chain challenges. UPMC did a great job weathering through the supply disruptions and labor challenges. We always had adequate personal protective equipment for our folks here. We also really made a conscientious decision last year to keep our workforce intact; we didn’t lay off workers, and we took care of people who needed time off because of COVID-19. We also made sure employees knew they had the support of our executive leadership team. In summary, COVID-19 has created a disruption, and we must think about how things are different now coming out of the disruption.

Q: What are some things you are doing to work through the change/disruption?

EK: From an organizational perspective, we embarked on what we call the “UPMC experience” a few years ago. We looked at the way we are doing things to understand the experience of our employees and patients. This prepared us to be more creative in our thinking as to how we address challenges and disruption. We also learned through this the importance of interdependencies. Our business, both provider and insurance side, discussed a need to tackle the disruptions in an integrated way and discussed a need to communicate changes effectively. This year, we provided about 40 news conferences to get the standard message out across all of our regions. We also have a 90,000-plus employee organization which allows you to move around resources to deal with some challenges and disruptions.

Q: What are UPMC’s top financial priorities for 2022?

EK: From a financial perspective, we want to maintain a positive margin to support our capital investments and employees. To do this, we are focused on a few things. First, supporting our operating employees to ensure they can perform to the best of their ability. They are the ones who make the difference each and every day. Second, we want to make sure we, as a finance team, can provide the things that the organization needs to be successful. This includes, but is not limited to, making sure supply chain folks can get all needed supplies and ensuring we have the cash collections needed to fund our organization. Another priority is making sure we provide the advice and guidance needed to invest our dollars effectively so we can prepare for the next challenge.

Q: What are a few key capital projects UPMC has in the works?

EK: UPMC is a premier provider in our community, and we operate a number of specialty hospitals in the area. We are the primary pediatric, psychiatric, women’s health and oncology provider in the region. Over the past couple of years, we’ve embarked on a journey to provide new facilities in western Pennsylvania for these major programs. We are also investing heavily in a vision and rehabilitation institute, which is a $500 million project that will put our clinicians, researchers and other providers together to drive breakthroughs in vision care and rehabilitation.

We also are going to embark on a new tower for UPMC Presbyterian Oakland Campus [in Pittsburgh]. It is going to be the largest capital project we’ve embarked on since I’ve been here. This project will be more than $1 billion and is so important to the community.

The third thing we are looking at is enhancing our oncology services and product at UPMC Shadyside [in Pittsburgh]. What we’ve recognized is that we are the provider and insurer of choice in western Pennsylvania, and we have to invest in this community for the next 50 to 100 years.

Q: What skills are essential for hospital and health system CFOs to thrive in today’s healthcare landscape?

EK: The technical skills are given as CFO. To get in that leadership position, you have to be able to perform the necessary tasks. However, to make your organization better, I could boil it down to four things. First, you have to be a partner to your other senior leaders. Finance doesn’t exist in a vacuum. You have to be in the room with those folks, helping them manage and drive the business. The second thing is flexibility. If you think about what we experienced as an industry over the last two years, if you weren’t flexible, you were going to be seriously challenged. Flexibility is such an important attribute because the pace of change is going to accelerate in our industry. Third, I’d say talent recognition is a key skill. It is important to be able to find talent as well as mentor and develop them as employees who can provide a great service to the organization. Fourth, you have to embody integrity. There is no doubt in my mind that integrity is a core value that is essential to everything you do as a finance leader. You have to maintain your integrity at all times. Those are essential skills. If you’re going to be a successful CFO now, you have to have those skills outside of the technical.

Q: What is one piece of advice you would offer to another healthcare CFO, and why?

EK: I’d say, look beyond the challenges of today. It’s not just about what you can actually see and envision in front of you. Try to look at the implications that are not necessarily top of mind. What the future holds is uncertain for all of us in healthcare now. You need to be thinking about what things might be coming down the road that will change our business and commitment to our communities dramatically. Try to brainstorm around that. Trying to think forward and speculate about what might happen is very valuable.