This month, a panel of expert advisers recommended the Food and Drug Administration (FDA) grant full approval to Leqembi, a drug developed by Eisai and Biogen that targets amyloid plaques in the brain that are linked to the development of Alzheimer’s.

The drug was found to slow cognitive decline in patients by 27 percent over 18 months, though not without some serious side effects, including brain swelling and bleeding. While Leqembi received accelerated FDA approval in January 2023, it is now likely to become the first Alzheimer’s drug that slows the progression of the disease to secure full FDA approval. The Centers for Medicare and Medicaid Services (CMS) recently announced that it intends to cover this new class of Alzheimer’s drugs, as long as prescribing physicians participate in patient registries designed to continue collecting data about the drugs and their efficacy. The FDA is expected to make a final decision on Leqembi by early July.

The Gist: In addition to risks of patient harm, much of the controversy around Leqembi surrounds its $27K list price. Payers, especially Medicare, are worried that it will balloon spending while exposing patients to unaffordable cost-sharing.

With the number of Americans diagnosed annually with Alzheimer’s and other dementias projected to double by 2050, Leqembi has the potential both to help millions and to drive unsustainable spending patterns, and it will be difficult to achieve the former without the latter.

But with full approval likely, a coming frenzy of investor activity to launch memory treatment centers for drug infusion services, capitalizing on the expected huge demand for the drug, seems inevitable.

Billionaire investor Charlie Munger has been vocal in expressing his concerns about U.S. healthcare, stating that it is “shot through with rampant waste” and has become “immoral.”

Munger says there are substantial problems that need to be addressed, including the presence of unnecessary costs and inefficiencies that plague the medical field.

Drawing a vivid analogy at a Daily Journal Annual Meeting, Munger compared the experience of a dying old person in many American hospitals to that of a carcass on the plains of Africa. He painted a bleak picture, describing how vultures, jackals, hyenas and other scavengers swarm around the helpless creature.

In an attempt to address these issues, Berkshire Hathaway, Amazon.com Inc., and JPMorgan Chase joined forces to establish Haven Healthcare a venture that despite their combined efforts failed to achieve its objectives.

Some startups have seen success where they failed. iRemedy, for example, is a startup using artificial intelligence (AI) technology, that offers a solution to the healthcare system’s challenges through its large procurement marketplace. Its platform streamlines the supply chain, enabling faster and more affordable access to lifesaving supplies for doctors, hospitals and healthcare providers.

Munger, vice chairman of Berkshire Hathaway Inc., criticized the high costs and inefficiencies in medical care as both expensive and wrong. In a CNBC interview, he went on to claim that some medical providers artificially prolong death to increase their profits.

With over 35 years of experience as board chairman of Good Samaritan Hospital in Los Angeles, Munger expressed his belief that certain healthcare practices are absurd.

“A lot of the medical care we do deliver is wrong — so expensive and wrong. It’s ridiculous,” he said in a “Squawk Box” interview.

In 2018, Munger predicted that when Democrats gain control of all three branches of government, there will be a push for a single-payer healthcare system. He highlighted the need for a complete change forced by the government because of the severity of the issues in the current system. He suggested that a universal healthcare system with an opt-out option would be a reasonable solution.

Warren Buffett, Munger’s longtime investing partner, shares similar concerns regarding healthcare spending, referring to it as a “tapeworm on the economic system.” Buffett believes the private sector can make substantial contributions to cost-reduction efforts.

A recent investigation conducted by Kaiser Health News-NPR shed light on the alarming reality of medical debt in the United States. The study reveals that over 100 million Americans are burdened with medical debt, placing a significant financial strain on their lives. Further analysis of the data reveals that approximately one-fourth of American adults carrying this debt owe more than $5,000.

What makes this issue even more concerning is the fact that it is not primarily driven by a lack of insurance coverage. Contrary to popular belief, the majority of people grappling with medical debt are not uninsured. Instead, it is the problem of being underinsured that is prevalent.

Many people have health insurance plans that do not offer sufficient coverage, leaving them vulnerable to high out-of-pocket expenses and accumulating medical debt.

A majority of Americans with health insurance said they had encountered obstacles to coverage, including denied medical care, higher bills and a dearth of doctors in their plans, according to a new survey from KFF, a nonprofit health research group. As a result, some people delayed or skipped treatment.

Those who were most likely to need medical care — people who described themselves as in fair or poor health — reported more trouble; three-fourths of those receiving mental health treatment experienced problems.

“The consequences of care delayed and missed altogether because of the sheer complexity of the system are significant, especially for people who are sick,” said Drew Altman, the CEO of KFF, formerly known as the Kaiser Family Foundation.

The survey also underscored the persistent problem of affordability as people struggled to pay their share of health care costs. About 40% of those surveyed said they had delayed or gone without care in the last year because of the expense. People in fair or poor health were more than twice as likely to report problems with paying medical bills than those in better health, and Black adults were more likely than white adults to indicate they had trouble.

Why It Matters: Delayed care can endanger health.

Nearly half of those who encountered a problem with their insurance said they could not satisfactorily resolve it. Some could not obtain the care they had sought, while others said they paid more than expected. Among the nearly 60% who reported difficulty with their insurance coverage, 15% said their health had declined.

“This survey shows it’s not enough to just get a card in your pocket — the insurance has to work or it’s not exactly coverage,” said Karen Pollitz, the co-director for KFF’s patient and consumer protections program.

People have a hard time understanding their coverage and benefits, with 30% or more reporting difficulty figuring out what they will be required to pay for care or what exactly their insurance will cover.

“Insurances are way more complicated than they should be,” said Amanda Parente, a 19-year-old college student in Nashville, Tennessee, who is covered under her mother’s employer plan. She was surprised to find that her out-of-pocket costs spiked recently when she sought treatment for strep throat. While she realized her copayments would be higher, “I guess we didn’t know how drastic it was going to be,” she said.

Background: Insurance coverage is confusing to everyone.

Navigating the intricacies of coverage and benefits were similar regardless of what kind of insurance people had. At least half of those surveyed with private coverage, through an employer, those with an “Obamacare” plan, or a government program like Medicare or Medicaid, said they experienced difficulties.

People might be unhappy with their coverage because they were already concerned about higher inflation and potential layoffs, said Christopher Lis, the managing director of global health care intelligence at J.D. Power, which found that consumer satisfaction with insurers had declined in a recent study. “We’ve got economic conditions that set the stage for concern around coverage and benefits,” he said.

Insurers say people generally report being happy with their plan, and 81% of those surveyed by KFF gave their insurance high ratings. “Health insurance providers are committed to improving access, affordability and convenience for all Americans and will continue to find innovative solutions to work toward this common goal,” said David Allen, a spokesperson for AHIP, a trade group that represents insurers.

What’s Next: How to haggle with insurers or appeal?

Also striking among the survey’s findings was how unaware people were about pursuing appeals of denied coverage and how to go about doing so.

“Most people don’t know who to call,” Pollitz said. Sixty percent of insured adults surveyed did not know they had a legal right to appeal, and about three-fourths said they did not know which government agency to contact for help, particularly respondents with private insurance.

State insurance regulators oversee fully insured policies sold to individuals and small businesses, and the federal Department of Labor has jurisdiction over employer-sponsored insurance.

Many of the problems people have with their insurance could be solved by enforcing existing rules, like federal regulations requiring private insurers to issue understandable explanations of benefits and to maintain accurate, current lists of doctors and hospitals within their networks.

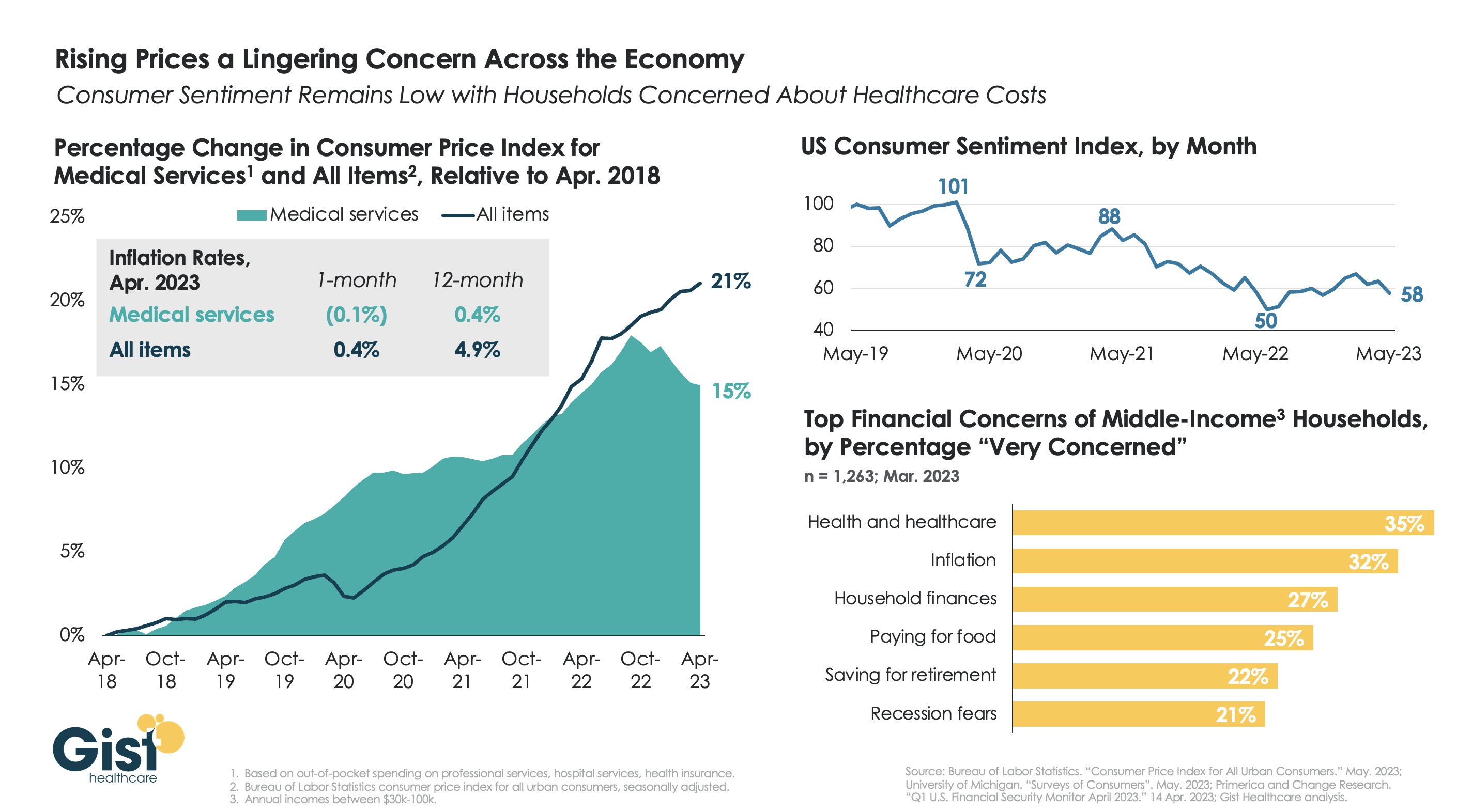

With the latest Bureau of Labor Statistics’ Consumer Price Index (CPI) report revealing the 12-month inflation rate in April 2023 rose again after hitting a recent low in March, we’re using this week’s graphic to show the cumulative picture on price and consumer sentiment changes across the last five years.

Since 2018, the CPI for all goods has risen 21 percent, while medical services have become 15 percent more expensive, in terms of consumer out-of-pocket spending. Leading into COVID, medical service prices were rising faster than general inflation, but the cumulative rise in the price of all goods caught up to medical services in early 2022.

Since December of last year, the price of medical services has actually experienced some deflation, partly due to a lagging decline in insurer profits. Reports of easing inflation had elicited a slight rebound in consumer sentiment, but last month’s 9 percent drop, the largest since June 2022, suggests this confidence is easily shaken.

Unfortunately for healthcare providers, according to a recent poll, fewer consumers worrying about elevated grocery and gas prices means that healthcare has reclaimed the top spot for household financial concerns.

In healthcare, as in life, people devote a lot of time and attention to the way things should be. They’d be better off focusing on what actually could be.

As an example, 57% to 70% of American voters believe our nation “should” adopt a single-payer healthcare system like Medicare For All. Likewise, public health advocates insist that more of the nation’s $4 trillion healthcare budget “should” be spent on combating the social determinants of health: things like housing insecurity, low-wage jobs and other socioeconomic stresses. Neither of these ideas will happen, nor will dozens of positive healthcare solutions that “should” happen.

When the things that should happen don’t, there’s always a reason. In healthcare, the biggest roadblock to change is what I call the conglomerate of monopolies, which includes hospitals, drug companies, private-equity-staked physicians and commercial health insurers. These powerful entities exert monopolistic control over the delivery and financing of the country’s medical care. And they remain fiercely opposed to any change in healthcare that would limit their influence or income.

This article concludes my five-part series on medical monopolies with an explanation of why (a) “should” won’t happen in healthcare but (b) industrywide disruption will.

Why government won’t lead the way

With the U.S. Senate split 51-49 and with virtually no chance of either party securing the 60 votes needed to avoid a filibuster, Congress will, at most, tinker with the medical system. That means no Medicare For All and no radical redistribution of healthcare funds.

Even if elected officials started down the path of major reform, healthcare’s incumbents would lobby, threaten to withhold campaign contributions (which have exceeded $700 million annually for the past three years) and swat down any legislative effort that might harm their interests.

In American politics, money talks. That won’t change soon, even if voters believe it should.

American employers won’t lead, either

Private payers wield significant power and influence of their own. In fact, the Fortune 500 represents two-thirds of the U.S. GDP, generating more than $16 trillion in revenue. And they provide health insurance to more than half the American population.

With all that clout, you’d think business executives would demand more from healthcare’s conglomerate of monopolies. You might assume they’d want to push back against the prevailing “fee for service” payment model, replacing it with a form of reimbursement that rewards doctors and hospitals for the quality (not quantity) of care they provide. You’d think they would insist that employees get their care through technologically advanced, multispecialty medical groups, which deliver superior outcomes when compared to solo physician practices.

Instead, companies take a more passive position. In fact, employers are willing to shoulder 5% to 6% increases in insurance premiums each year (double their average rate of revenue growth) without putting up much or any resistance.

One reason they tolerate hefty rate hikes—rather than battling insurers, hospitals and doctors— involves a surprising truth about insurance premiums. Business leaders have figured out how to transfer much of their added premium costs to employees in the form of high-deductible health plans. A high deductible plan forces the beneficiary to pay “first dollar” for their medical care, which significantly reduces the premium cost paid by the employer.

Businesses also realize that high deductibles will only financially burden employees who experience an unexpected, catastrophic illness or accident. Meaning, most workers won’t feel the sting in a typical year. As for employees with ongoing, expensive medical problems, employers typically don’t mind watching them walk out the door over high out-of-pocket costs. Their departures only reduce the company’s medical spend in future years.

Finally, businesses know that employee medical costs are tax deductible, which cushions the impact of premium increases. So, what starts as a 6% annual increase ends up costing employees 3%, the government 1% and businesses only 2%. In today’s strong labor market, which boasts the lowest unemployment rate in 54 years, businesses are reluctant to demand changes from healthcare’s biggest players—regardless of whether they should.

Leading the healthcare transformation

If there were a job opening for “Leader of the American Healthcare Revolution,” the applicant pool would be shallow.

Elected officials would shy away, fearing the loss of campaign contributions. Businesses and top executives would pass on the opportunity, preferring to shift insurance costs to employees and the government. Patients would feel overwhelmed by the task and the power of the incumbents. Doctors, nurses and hospitals—despite their frustrations with the current system—would want to take small steps, fearful of the conglomerate of monopolies and the risks of disruptive change.

To revolutionize American medicine, a leader must possess three characteristics:

Sufficient size and financial reserves to disrupt the entire industry (not just a small piece of it).

Presence across the country to leverage economies of scale.

Willingness to accept the risks of radical change in exchange for the potential to generate massive profits.

Whoever leads the way won’t make these investments because it “should happen.” They will take the chance because the upside is dramatically better than sitting on the sidelines.

The likely winner: American retailers

Amazon, CVS, Walmart and other retail giants are the only entities that fit the revolutionary criteria above. In healthcare’s game of monopoly, they’re the ones willing to take high-stakes risks and capable of disrupting the industry.

For years, these retailers have been acquiring the necessary game pieces (including pharmacy services, health-insurance capabilities and innovative care-delivery organizations) to someday take over American healthcare.

CVS Health owns health insurer Aetna. It bought value-based care company Signify Health for $8 billion, along with national primary care provider OakStreet Health for $10.6 billion. Walmart recently entered into a 10-year partnership with the nation’s largest insurance company, UnitedHealth, gaining access to its 60,000 employed physicians. Walmart then acquired LHC, a massive home-health provider. Finally, Amazon recently purchased primary-care provider One Medical for $3.9 billion and maintains close ties with nearly all of the country’s self-funded businesses.

Harvard business professor Clay Christensen noted that disruptive change almost always comes from outsiders. That’s because incumbents cling to overly expensive and inefficient systems. The same holds true in American healthcare.

The retail giants can see that healthcare is exorbitantly priced, uncoordinated, inconvenient and technologically devoid. And they recognize the hundreds of billions of dollars of revenue and they could earn by offering a consumer-focused, highly efficient alternative.

How will the transformation happen?

Initially, I believe the retail giants will take a two-pronged approach. They’ll (a) continue to promote fee-for-service medical services through their pharmacies and retail clinics (in-store and virtual) while (b) embracing every opportunity to grow their market share in Medicare Advantage, the capitated option for people over age 65.

And within Medicare Advantage, they’ll look for ways to leverage sophisticated IT systems and economies of scale, thus providing care that is better coordinated, technologically supported and lower cost than what’s available now.

Rather than including all community doctors in their network, they’ll rely on their own clinicians, augmented by a limited cohort of the highest-performing medical groups in the area. And rather than including every hospital as an inpatient option, they’ll contract with highly respected centers of excellence for procedures like heart surgery, neurosurgery, total-joint replacement and transplants, trading high volume for low prices.

Over time, they’ll reach out to self-funded businesses to offer proven, superior clinical outcomes, plus guaranteed, lower total costs. Then they’ll make a capitated model their preferred insurance plan for all companies and individuals. Along the way, they’ll apply consumer-driven medical technologies, including next generations of ChatGPT, to empower patients, provide continuous care for people with chronic diseases and ensure the medical care provided is safe and most efficacious.

Tommy Lasorda, the long-time manager of the Los Angeles Dodgers, once remarked, “There are three types of people. Those who watch what happens, those that make it happen and those who wonder what just happened.”

Lasorda’s quip describes healthcare today. The incumbents are watching closely but failing to see the big picture as retailer acquire medical groups and home health capabilities. The retail giants are making big moves, assembling the pieces needed to completely transform American medicine as we think of it today. Finally, tens of thousands of clinicians and thousands of hospital administrators are either ignoring or underestimating the retail giants. And, when they get left behind, they’ll wonder: What just happened?

The conglomerate of monopolies rule medicine today. Amazon, CVS and Walmart believe they should rule. And if I had to bet on who will win, I’d put my money on the retail giants.

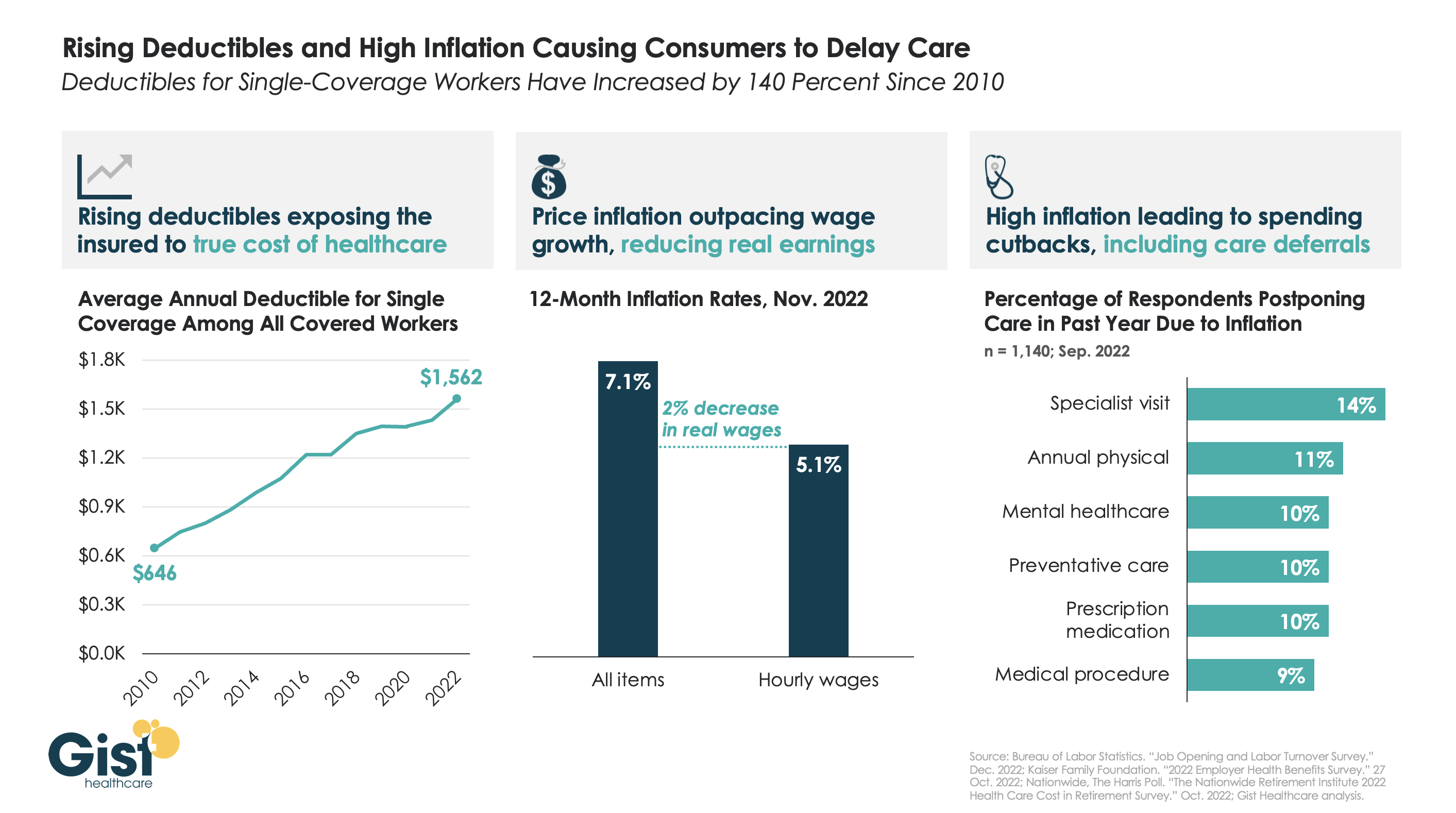

After COVID fears and shutdowns led consumers to delay care early in the pandemic, persistently high inflation over the past year has further suppressed volumes.

As the graphic above illustrates, the average deductible for individual coverage has grown by over 140 percent since 2010, exposing consumers to an increasing portion of healthcare costs, and prompting economists to reevaluate the adage that healthcare is “recession-proof”.

This year, that trend collided with an inflation spike that outpaced wage gains by two percent. Faced with diminished purchasing power, households are making budget tradeoffs which explicitly pit healthcare against other essential household needs.

For some, this cost-cutting impulse even extends to preventative screenings—required to be covered without cost-sharing—when consumers’ financial concerns drive them to avoid healthcare altogether.

While the latest inflation report suggests price increases are moderating, fears of a broader recession persist, making it critical for health systems and physicians to communicate with patients, encouraging them to continue to access preventive care, educating them about lower cost care options, and helping them prioritize treatment that should not be put off.

The majority of hospitals are predicted to have negative margins in 2022, marking the worst year financially for hospitals since the beginning of the Covid-19 pandemic.

In Part 1 of Radio Advisory’s Hospital of the Future series, host Rachel (Rae) Woods invites Advisory Board experts Monica Westhead, Colin Gelbaugh, and Aaron Mauck to discuss why factors like workforce shortages, post-acute financial instability, and growing competition are contributing to this troubling financial landscape and how hospitals are tackling these problems.

As we emerge from the global pandemic, health care is restructuring. What decisions should you be making, and what do you need to know to make them? Explore the state of the health care industry and its outlook for next year by visiting advisory.com/HealthCare2023.

2022 has disproven the old trope that “healthcare is recession-proof”. With the average family deductible nearing $4,000, a significant portion of healthcare services are exposed to consumer concerns about affordability. Reflecting the impact of the recession, health systems nationwide have reported sluggish volumes, particularly for elective cases, in the second half of the year.

One COO recently shared, “We’re 15 percent off where we expected to be on elective cases…We didn’t see the usual pick-up in early fall, after summer vacation. I’m not sure if it’s related to the economy, or whether demand changed during COVID, but this decline has eroded any possibility of a positive margin for the quarter.” The recession hit just as providers mostly finished working through the backlog of cases delayed by COVID in 2020 and 2021.

To determine whether demand declines are related to the current economic environment, or signal real shifts in care patterns, health systems are looking closely to see if the usual end-of-year swell of demand for elective care materializes, as patients max out their deductibles. But even if the demand is there, some systems are worried about being able to accommodate it: “We’ve been so short-staffed for nurses and surgical techs, we’ve had to intermittently take some ORs and units offline…If we get a big December spike in elective care, I’m not sure we’ll have the staff to accommodate it.” Facing the triple threat of sky-high costs, sluggish demand, and a worsening payer environment, the ability to accommodate this demand will be critical to securing margins as providers move into 2023.

Driven by the steady progress of Medicaid expansion and pandemic-era policies to ensure access to health insurance coverage, the US uninsured rate hit an all-time low of 8 percent in early 2022. Since the Affordable Care Act passed in 2010, the US uninsured rate has been cut in half, with the largest gains coming from Medicaid expansion.

However, using data from Commonwealth Fund, the graphic below illustrates how this noteworthy achievement is undermined by widespread underinsurance, defined as coverage that fails to protect enrollees from significant healthcare cost burdens. A recent survey of working-age adults found that eleven percent of Americans experienced a coverage gap during the year, and nearly a quarter had continuous insurance, but with inadequate coverage.

High deductibles are a key driver of underinsurance, with average deductibles for employer-sponsored plans around $2,000 for individuals and $4,000 for families.

Roughly half of Americans are unable to afford a $1,000 unexpected medical bill. Americans’ healthcare affordability challenges will surely worsen once the federal COVID public health emergency ends, because between 5M and 14M Medicaid recipients could lose coverage once the federal government ends the program that has guaranteed continuous Medicaid eligibility.

The process of eligibility redeterminations is sure to be messy—while some Medicaid recipients will be able to turn to other coverage options, the ranks of uninsured and underinsured are likely to swell.

Patients at North Carolina-based Atrium Health get what looks like an enticing pitch when they go to the nonprofit hospital system’s website: a payment plan from lender AccessOne. The plans offer “easy ways to make monthly payments” on medical bills, the website says. You don’t need good credit to get a loan. Everyone is approved. Nothing is reported to credit agencies.

In Minnesota, Allina Health encourages its patients to sign up for an account with MedCredit Financial Services to “consolidate your health expenses.” In Southern California, Chino Valley Medical Center, part of the Prime Healthcare chain, touts “promotional financing options with the CareCredit credit card to help you get the care you need, when you need it.”

As Americans are overwhelmed with medical bills, patient financing is now a multibillion-dollar business, with private equity and big banks lined up to cash in when patients and their families can’t pay for care. By one estimate from research firm IBISWorld, profit margins top 29% in the patient financing industry, seven times what is considered a solid hospital margin.

Hospitals and other providers, which historically put their patients in interest-free payment plans, have welcomed the financing, signing contracts with lenders and enrolling patients in financing plans with rosy promises about convenient bills and easy payments.

For patients, the payment plans often mean something more ominous: yet more debt.

Millions of people are paying interest on these plans, on top of what they owe for medical or dental care, an investigation by KHN and NPR shows. Even with lower rates than a traditional credit card, the interest can add hundreds, even thousands of dollars to medical bills and ratchet up financial strains when patients are most vulnerable.

Robin Milcowitz, a Florida woman who found herself enrolled in an AccessOne loan at a Tampa hospital in 2018 after having a hysterectomy for ovarian cancer, said she was appalled by the financing arrangements.

“Hospitals have found yet another way to monetize our illnesses and our need for medical help,” said Milcowitz, a graphic designer. She was charged 11.5% interest — almost three times what she paid for a separate bank loan. “It’s immoral,” she said.

MedCredit’s loans to Allina patients come with 8% interest. Patients enrolled in a CareCredit card from Synchrony, the nation’s leading medical lender, face a nearly 27% interest rate if they fail to pay off their loan during a zero-interest promotional period. The high rate hits about 1 in 5 borrowers, according to the company.

For many patients, financing arrangements can be confusing, resulting in missed payments or higher interest rates than they anticipated. The loans can also deepen inequalities. Lower-income patients without the means to make large monthly payments can face higher interest rates, while wealthier patients able to shoulder bigger monthly bills can secure lower rates.

More fundamentally, pushing people into loans that threaten their financial health runs against medical providers’ first obligation to not harm their patients, said patient advocate Mark Rukavina, program director at the nonprofit Community Catalyst.

“We’re dealing with sick people, scared people, vulnerable people,” Rukavina said. “Dangling a financial services product in front of them when they’re concerned about their care doesn’t seem appropriate.”

Debt upon debt for patients, as finance firms get a cut of payments

Nationwide, about 50 million people — or 1 in 5 adults — are on a financing plan to pay off a medical or dental bill, according to a KFF poll conducted for this project. About a quarter of those borrowers are paying interest, the poll found.

Increasingly, those interest payments are going to financing companies that promise hospitals they will collect more of their medical bills in exchange for a cut.

Hospital officials defend these arrangements, citing the need to offset the cost of offering financing options to patients. Alan Wolf, a spokesperson for the University of North Carolina’s hospital system, said that the system, which reported $5.8 billion in patient revenue last year, had a “responsibility to remain financially stable to assure we can provide care to all regardless of ability to pay.” UNC Health, as it is known, has contracted since 2019 with AccessOne, a private equity-backed company that finances loans for scores of hospital systems across the country.

This partnership has had a substantial impact on patient debt, according to a KHN analysis of billing and contracting records obtained through public records requests.

Most patients in 2019 were in no-interest payment plans

UNC Health, which as a public university system touts its commitment “to serve the people of North Carolina,” had long offered payment plans without interest. And when AccessOne took over the loans in September 2019, most patients were in no-interest plans.

That has steadily shifted as new patients enrolled in one of AccessOne’s plans, several of which have variable interest rates that now charge 13%.

In February 2020, records show, just 9% of UNC patients in an AccessOne plan were in a loan with the highest interest rate. Two years later, 46% were in such a plan. Overall, at any given time more than 100,000 UNC Health patients finance through AccessOne.

The interest can pile on debt. Someone with a $7,000 hospital bill, for example, who enrolls in a five-year financing plan at 13% interest will pay at least $2,500 more to settle that debt.

How a short-term solution ‘leads to longer-term problems’

Rukavina, the patient advocate, said adding this burden on patients makes little sense when medical debt is already creating so much hardship. “It may seem like a short-term solution, but it leads to longer-term problems,” he said. Health care debt has forced millions of Americans to cut back on food, give up their homes, and make other sacrifices, KHN found.

UNC Health disavowed responsibility for the additional debt, saying patients signed up for the higher-interest loans. “Any payment plans above zero-interest terms/conditions in place with AccessOne are in place at the request of the patient,” Wolf said in an email. UNC Health would only provide answers to written questions.

UNC Health’s patients aren’t the only ones getting routed into financing plans that require substantial interest payments.

At Atrium Health, a nonprofit system with roots as Charlotte’s public hospital that reported more than $7.5 billion in revenues last year, as many as half of patients enrolled in an AccessOne loan were in one of the company’s highest-interest plans, according to 2021 billing records analyzed by KHN.

At AU Health, Georgia’s main public university hospital system, billing records obtained by KHN show that two-thirds of patients on an AccessOne plan were paying the highest interest rate as of January.

A finance firm calls such loans ’empathetic patient financing’

AccessOne chief executive Mark Spinner, who in an interview called his firm a “compassionate, empathetic patient financing company,” said the range of interest rates gives patients and medical systems valuable options. “By offering AccessOne, you’re creating a much safer, more mission-aligned way for consumers to pay and help them stay out of medical debt,” he said. “It’s an alternative to lawsuits, legal action, and things like that.”

AccessOne, which doesn’t buy patient debt from hospitals, doesn’t run credit checks on patients to qualify them for loans. Nor will the company report patients who default to credit bureaus. The company also frequently markets the availability of zero-interest loans.

Some patients do qualify for no-interest plans, particularly if they have very low incomes. But the loans aren’t always as generous as company and hospital officials say.

AccessOne borrowers who miss payments can have their accounts returned to the hospital, which can sue them, report them to credit bureaus, or subject them to other collection actions. UNC Health refers unpaid bills to the state revenue department, which can garnish patients’ tax refunds. Atrium’s collections policy allows the hospital system to sue patients.

Because AccessOne borrowers can get low interest rates by making larger monthly payments, this financing system can also deepen inequalities. Someone who can pay $292 a month on a $7,000 hospital bill, for example, could qualify for a two-year, interest-free plan. But a patient who can pay only $159 a month would have to take a five-year plan with 13% interest, according to AccessOne.

“I see wealthier families benefiting,” said one former AccessOne employee, who asked not to be identified because she still works in the financing industry. “Lower-income families that have hardship are likely to end up with a higher overall balance due to the interest.”

Andy Talford, who oversees patient financial services at Moffitt Cancer Center in Tampa, said the hospital contracted with AccessOne to make it easier for patients to manage their medical bills. “Someone out there is helping them keep track of it,” he said.

But patients can get tripped up by the complexities of managing these plans, consumer advocates say. That’s what happened to Milcowitz, the graphic designer in Florida.

Milcowitz, 51, had set up a no-interest payment plan with Moffitt to pay off $3,000 she owed for her hysterectomy in 2017. When the medical center switched her account to AccessOne, however, she began receiving late notices, even as she kept making payments.

Only later did she figure out that AccessOne had set up two accounts, one for the cancer surgery and another for medical appointments. Her payments had been applied only to the surgery account, leaving the other past-due. She then got hit with higher interest rates. “It’s crazy,” she said.

Lenders see a growing business opportunity

While financing plans may mean more headaches and more debt for patients, they’re proving profitable for lenders.

That’s drawn the interest of private equity firms, which have bought several patient financing companies in recent years. Since 2017, AccessOne’s majority owner has been private equity investor Frontier Capital.

Synchrony, which historically marketed its CareCredit cards in patient waiting rooms, is now also inking deals with medical systems to enroll patients in loans when they go online to pay bills.

“They’re like pilot fish eating off the back of the shark,” said Jonathan Bush, a founder of Athenahealth, a health technology company that has developed electronic medical records and billing systems.

As patient bills skyrocket, hospitals face mounting pressure to collect more, which can make financing arrangements seem appealing, industry experts say. But as health systems go into business with lenders, many are reluctant to share details. Only a handful of hospitals contacted by KHN agreed to be interviewed about their contracts and what they mean for patients.

Several public systems, including Atrium and UNC Health, disclosed information only after KHN submitted public records requests. Even then, the two systems redacted key details, including how much they pay AccessOne.

AU Health, which did not redact its contract, pays AccessOne a 6% “servicing fee” on each patient loan the company administers. But like Atrium and UNC Health, AU Health refused to provide any on-the-record interviews.

Other hospital systems were even less transparent. Mercyhealth, a nonprofit with hospitals and clinics in Illinois and Wisconsin that routes its patients to CareCredit, would not discuss its lending practices. “We do not have anyone available for this,” spokesperson Therese Michels said. Allina Health and Prime Healthcare also wouldn’t talk about their patient financing deals.

Bush said there’s a reason so few hospitals want to discuss their financing deals: They’re embarrassed. “It’s like they quietly write someone’s name on a piece of paper and slide it across the table,” he said. “They don’t want to be a part of it because they have in their institutional memory that they are supposed to look after patients’ best interests.”

Some hospitals and banks still offer interest-free help

Not all hospitals expose their patients to extra costs to finance medical bills.

Lake Region Healthcare, a small nonprofit with hospitals and clinics in rural Minnesota that contracts with Missouri-based Commerce Bank, charges no interest or fees on payment plans. That’s a decision that spokesperson Katie Johnson said was made “for the benefit of our patients.”

Even some AccessOne clients such as the University of Kansas Health System shield patients from interest. But as providers look to boost their bottom lines, it’s unclear how long these protections will last. Colette Lasack, who oversees financing for the Kansas system, noted: “There’s a cost associated with that.”

Meanwhile, large national lenders such as Discover Financial Services are looking at the patient financing business.

“I’ve had to become more of a health care marketer,” said Matt Lattman, vice president for personal loans at Discover, which is pitching the loans to people with unexpected medical bills. “In a world where many people are ill prepared to cover their health care costs, the personal loan can provide an opportunity.”