St. Francis Medical Center in Trenton, N.J., on Dec. 21 transitioned to a freestanding emergency room that offers various outpatient services after Capital Health acquired the hospital from Trinity Health, according to PBS affiliate WHYY.

The campus, renamed Capital Health – East Trenton, must feature a primary family health clinic and a women’s OB/GYN clinic, according to terms of the transaction.

Other services, such as cardiac surgery, are moving to Capital Health Regional Medical Center in Trenton, where “extensive capital projects” are being planned, the health system said in a Dec. 8 news release.

A St. Francis spokesperson told the news outlet that the hospital had been financially struggling for years.

“St. Francis has done many great things for the Trenton community, but the current healthcare landscape has made it unsustainable,” Capital Health President and CEO Al Maghazehe said. “Without these key approvals, Trenton would have lost desperately needed healthcare services, including emergency services, behavioral health and cardiac surgery.”

Capital Health said it has taken “a significant risk” to try and prevent a healthcare crisis for Trenton’s 90,000 residents, according to the report.

The majority of hospitals are predicted to have negative margins in 2022, marking the worst year financially for hospitals since the beginning of the Covid-19 pandemic.

In Part 1 of Radio Advisory’s Hospital of the Future series, host Rachel (Rae) Woods invites Advisory Board experts Monica Westhead, Colin Gelbaugh, and Aaron Mauck to discuss why factors like workforce shortages, post-acute financial instability, and growing competition are contributing to this troubling financial landscape and how hospitals are tackling these problems.

As we emerge from the global pandemic, health care is restructuring. What decisions should you be making, and what do you need to know to make them? Explore the state of the health care industry and its outlook for next year by visiting advisory.com/HealthCare2023.

Radio Advisory’s Rachel Woods sat down with Optum EVP Dr. Jim Bonnette to discuss the sustainability of modern-day hospitals and why scaling down might be the best strategy for a stable future.

Rachel Woods:When I talk about hospitals of the future, I think it’s very easy for folks to think about something that feels very futuristic, the Jetsons, Star Trek, pick your example here. But you have a very different take when it comes to the hospital, the future, and it’s one that’s perhaps a lot more streamlined than even the hospitals that we have today. Why is that your take?

Jim Bonnette: My concern about hospital future is that when people think about the technology side of it, they forget that there’s no technology that I can name that has lowered health care costs that’s been implemented in a hospital. Everything I can think of has increased costs and I don’t think that’s sustainable for the future.

And so looking at how hospitals have to function, I think the things that hospitals do that should no longer be in the hospital need to move out and they need to move out now. I think that there are a large number of procedures that could safely and easily be done in a lower cost setting, in an ASC for example, that is still done in hospitals because we still pay for them that way. I’m not sure that’s going to continue.

Woods: And to be honest, we’ve talked about that shift, I think about the outpatient shift. We’ve been talking about that for several years but you just said the change needs to happen now. Why is the impetus for this change very different today than maybe it was two, three, four, five years ago? Why is this change going to be frankly forced upon hospitals in the very near future, if not already?

Bonnette: Part of the explanation is regarding the issues that have been pushed regarding price transparency. So if employers can see the difference between the charges for an ASC and an HOPD department, which are often quite dramatic, they’re going to be looking to say to their brokers, “Well, what’s the network that involves ASCs and not hospitals?” And that data hasn’t been so easily available in the past, and I think economic times are different now.

We’re not in a hyper growth phase, we’re not where the economy’s performing super at the moment and if interest rates keep going up, things are going to slow down more. So I think employers are going to become more sensitized to prices that they haven’t been in the past. Regardless of the requirements under the Consolidated Appropriations Act, which require employers to know the costs, which they didn’t have to know before. They’re just going to more sensitive to price.

Woods: I completely agree with you by the way, that employers are a key catalyst here and we’ve certainly seen a few very active employers and some that are very passive and I too am interested to see what role they play or do they all take much more of an active role.

And I think some people would be surprised that it’s not necessarily consumers themselves that are the big catalyst for change on where they’re going to get care, how they want to receive care. It’s the employers that are going to be making those decisions as purchasers themselves.

Bonnette: I agree and they’re the ultimate payers. For most commercial insurance employers are the ultimate payers, not the insurance companies. And it’s a cost of care share for patients, but the majority of the money comes from the employers. So it’s basically cutting into their profits.

Woods: We are on the same page, but I’m going to be honest, I’m not sure that all of our listeners are right. We’re talking about why these changes could happen soon, but when I have conversations with folks, they still think about a future of a more consolidated hospital, a more outpatient focused practice is something that is coming but is still far enough in the future that there’s some time to prepare for.

I guess my question is what do you say to that pushback? And are there any inflection points that you’re watching for that would really need to hit for this kind of change to hit all hospitals, to be something that we see across the industry?

Bonnette: So when I look at hospitals in general, I don’t see them as much different than they were 20 years ago. We have talked about this movement for a long time, but hospitals are dragging their feet and realistically it’s because they still get paid the same way until we start thinking about how we pay differently or refuse to pay for certain kinds of things in a hospital setting, the inertia is such that they’re going to keep doing it.

Again, I think the push from employers and most likely the brokers are going to force this change sooner rather than later, but that’s still probably between three and five years because there’s so much inertia in health care.

On the other hand, we are hitting sort of an unsustainable phase of cost. The other thing that people don’t talk about very much that I think is important is there’s only so many dollars that are going to health care.

And if you look at the last 10 years, the growth in pharmaceutical spend has to eat into the dollars available for everybody else. So a pharmaceutical spend is growing much faster than anything else, the dollars are going to come out of somebody’s hide and then next logical target is the hospital.

Woods: And we talked last week about how slim hospital margins are, how many of them are actually negative. And what we didn’t mention that is top of mind for me after we just come out of this election is that there’s actually not a lot of appetite for the government to step in and shore up hospitals.

There’s a lot of feeling that they’ve done their due diligence, they stepped in when they needed to at the beginning of the Covid crisis and they shouldn’t need to again. That kind of savior is probably not their outside of very specific circumstances.

Bonnette: I agree. I think it’s highly unlikely that the government is going to step in to rescue hospitals. And part of that comes from the perception about pricing, which I’m sure Congress gets lots of complaints about the prices from hospitals.

And in addition, you’ll notice that the for-profit hospitals don’t have negative margins. They may not be quite as good as they were before, but they’re not negative, which tells me there’s an operational inefficiency in the not for-profit hospitals that doesn’t exist in the for-profits.

Woods: This is where I wanted to go next. So let’s say that a hospital, a health system decides the new path forward is to become smaller, to become cheaper, to become more streamlined, and to decide what specifically needs to happen in the hospital versus elsewhere in our organization.

Maybe I know where you’re going next, but do you have an example of an organization who has had this success already that we can learn from?

Bonnette: Not in the not-for-profit section, no. In the for-profits, yes, because they have already started moving into ambulatory surgery centers. So Tenet has a huge practice of ambulatory surgery centers. It generates high margins.

So, I used to run ambulatory surgery centers in a for-profit system. And so think about ASCs get paid half as much as a hospital for a procedure, and my margin on that business in those ASCs was 40% to 50%. Whereas in the hospital the margin was about 7% and so even though the total dollars were less, my margin was higher because it’s so much more efficient. And the for-profits already recognize this.

Woods: And I’m guessing you’re going to tell me you want to see not-for-profit hospitals make these moves too? Or is there a different move that they should be making?

Bonnette: No, I think they have to. I think there are things beyond just ASCs though, for example, medical patients who can be treated at home should not be in the hospital. Most not-for-profits lose money on every medical admission.

Now, when I worked for a for-profit, I didn’t lose money on every Medicare patient that was a medical patient. We had a 7% margin so it’s doable. Again, it’s efficiency of care delivery and it’s attention to detail, which sometimes in a not-for-profit friends, that just doesn’t happen.

One of COVID’s many effects on the health system business model has been the accelerated migration of care to outpatient settings, with orthopedic surgeries, such as knee and hip replacements, leading the way. For this week’s graphic, we partnered with Stratasan, a Syntellis-owned healthcare data analytics firm that provides market intelligence for strategic planning, to track how quickly joint replacements have shifted to hospital outpatient and ambulatory surgery centers (ASCs) over the last five years.

Using data from Stratasan’s proprietary All-Payer Claims Database, we found that by the end of 2021, only one in four knee replacements and one in three hip replacements were performed in inpatient facilities, down from over 95 percent in 2018. A major catalyst for the shift was the removal of the procedures from Medicare’s Inpatient Only list, first knee replacements in 2018, then hip replacements in 2020.

This change triggered an outpatient shift across all payers; COVID’s dampening effect on inpatient demand only exacerbated the trends. Patients who undergo these surgeries in an inpatient hospital tend to be sicker, older, and more likely to be on Medicare. This translates to an altered payer mix for these procedures, with hospitals seeing a drop in lucrative commercial payment and an uptick in lower Medicare reimbursements.

Amid rising expenses and slow-to-return volumes across the board, this outpatient migration presents another significant challenge to health systems’ financial bottom lines, and they must either find ways to recapture revenues in ambulatory settings, or watch a once reliable source of revenue walk—gingerly—out their doors.

Adult inpatient volumes will recover to pre-pandemic numbers but grow only 2 percent over the next decade, a new report from Sg2 forecasts.

At the same time, adult inpatient days are expected to increase 8 percent and tertiary inpatient days are poised to increase 17 percent, fueled by an increase in chronic conditions.

“While case mix varies by hospital, it is likely this combination of increased inpatient volume, patient complexity and length of stay may require healthcare organizations to rethink service line prioritization, service distribution and investment in care at-home initiatives,” Maddie McDowell, MD, senior principal and medical director of quality and strategy for Sg2, said in a June 7 news release for the report.

Five other key takeaways from Sg2’s forecasts:

1. Outpatient volumes are projected to return to pre-pandemic levels in 2022 and then grow 16 percent through 2032, three percentage points above estimated population growth.

2. Surgical volumes are projected to grow 25 percent at ambulatory surgery centers and 18 percent at hospital outpatient departments and physician offices over the next decade.

3. The pandemic-driven decline in emergency department visits is expected to plateau with a decline in demand projected at -2 percent over the next 10 years.

4. Over the next five years, home care is expected to gain traction, with home evaluation and management visits seeing 19 percent growth, home hospice at 13 percent growth and home physical and occupational therapy at 10 percent growth.

5. Telehealth is expected to resume its climb and by 2032 account for 27 percent of all evaluation and management visits.

More than two years after the pandemic’s onset, some types of hospital volume still haven’t returned to pre-pandemic levels. The graphic above uses recent data from analytics firm Strata Decision Technology to track monthly hospital volume across various care settings.

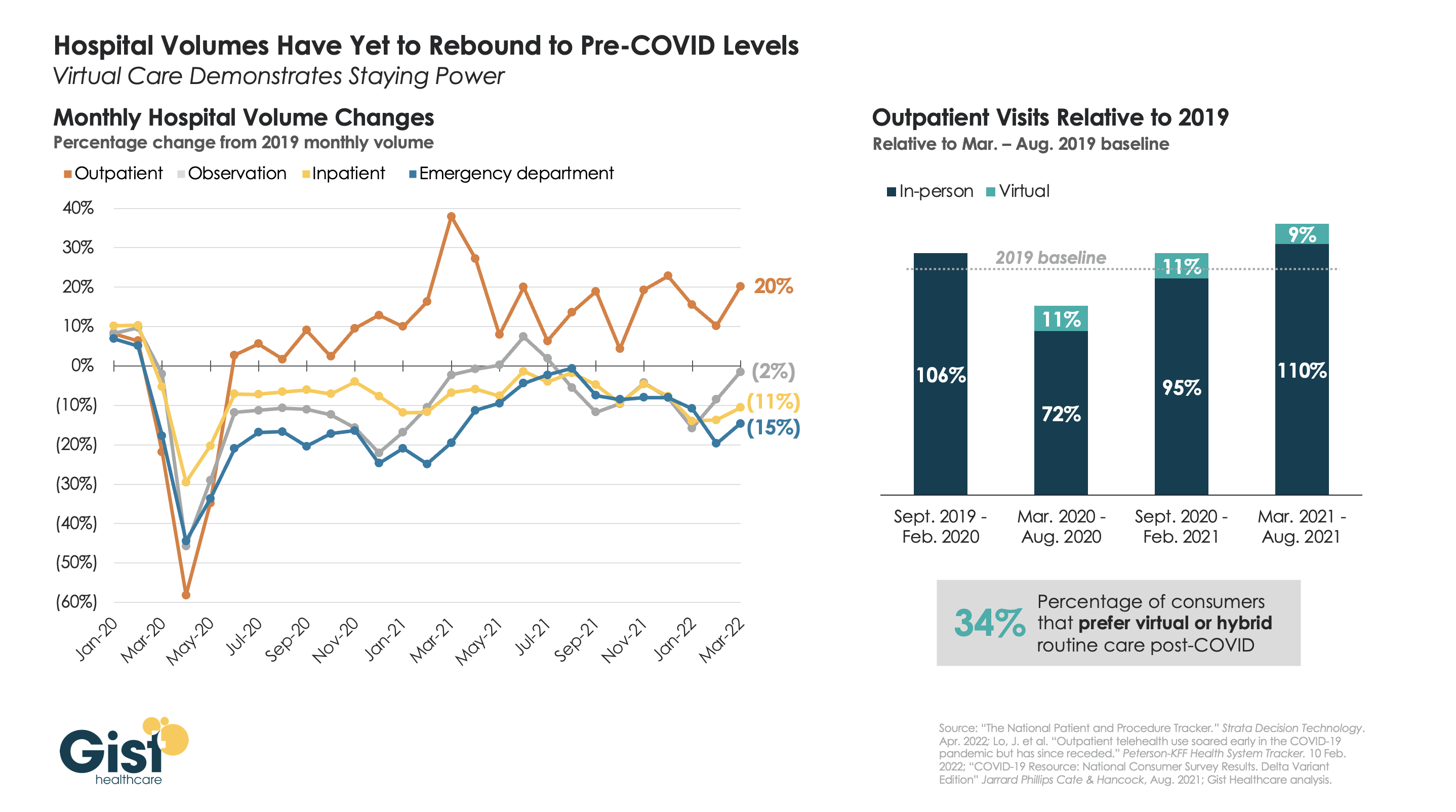

While outpatient volume continues to exceed pre-COVID levels, inpatient, emergency department (ED), and observation volume is still below the 2019 baseline.The unpredictability of volume trends is likely to continue, as COVID continues to ebb and flow regionally, and care continues to shift outpatient.

By contrast, the volume of virtual care visits has remained consistent, even as consumers return to in-person outpatient visits, driving up the overall level above the pre-pandemic baseline. Some of this increase in outpatient visit volume has been driven by consumers turning to urgent care clinics or doctors’ offices—either in-person or virtually—for their lower-acuity care needs.

While temporary reimbursement and licensing policies for telehealth have been the main stumbling blocks for many organizations’ longer-term planning for virtual visits, about half of states have now implemented permanent payment parity for telemedicine. As such, provider organizations that are still taking a “wait and see approach” must develop an economically sustainable virtual care model to reduce costs and meet evolving consumer demands.

Tampa, Fla.-based Shriners Hospitals for Children is transitioning its Springfield, Mass., campus into an outpatient clinic model, NBC/CW affiliate WWLP reported April 20.

Current outpatient services won’t be affected, except that ambulatory surgery will end.

The hospital gave the Massachusetts Department of Public Health a 120-day notice of the plan on March 31, Western Mass News reported April 20.

“The advancement of surgical procedures has resulted in very few patients requiring admission for inpatient pediatric services, which are the cornerstone of a hospital facility,” Shriners said in a letter obtained by Western Mass News. “Accordingly, after evaluating the needs of our patients, we have determined that Shriners Hospitals for Children may best serve our patients and fulfill our charitable mission by transitioning this location from a hospital to an outpatient clinic model.”

HCA has purchased MD Now Urgent Care, Florida’s largest urgent care chain, adding 59 urgent care centers to its existing 170. Meanwhile Tenet’s $1.1B deal to buy SurgCenter Development cements its position as the nation’s largest ambulatory surgery center (ASC) operator, eclipsing Envision-owned AMSURG and Optum-owned Surgical Care Affiliates.

The Gist: Healthcare services are increasingly moving outpatient and even virtual—a trend only accelerated by the pandemic. With this latest acquisition, Tenet will now own or operate nearly seven times as many ASCs as hospitals. Such national, for-profit systems are looking to add more non-acute assets to their portfolios, to capitalize on a shift fueled by both consumer preference for greater convenience, and purchaser pressure to reduce care costs.

Tenet and its subsidiary USPI have entered into a $1.2 billion deal to acquire ambulatory surgery center operator SurgCenter Development, expanding on a previous $1.1 billion cash deal inked with SCD last year.

Under the new deal announced Monday, Tenet will acquire SCD’s ownership interests in 92 ambulatory surgery centers and other support services in 21 states.

In addition to the acquisition, USPI and SCD plan to enter into a five-year partnership and development agreement in which SCD will help facilitate “continuity and support for SCD’s facilities and physician partners.” USPI will also have exclusivity on developing new projects with SCD during the five-year agreement.

Dive Insight:

Despite being a legacy hospital operator, Tenet’s outpatient surgery business is key to its long-term strategy.

After the latest deal closes, USPI will operate 440 surgery centers in 35 states, Tenet said Tuesday. The acquisition will boost USPI’s footprint in existing markets, such as Florida where it already operates 47 centers and will gain an additional 15. USPI will also enter new markets, such as Michigan, with a sizable footprint at the outset, executives said Tuesday.

The deal includes 65 mature centers and 27 that have opened in the past year or will soon open and start performing their first cases. Tenet may also spend an additional $250 million to acquire equity interests from physician owners.

Tenet leaders touted SCD’s service line mix, pointing out that a significant portion of the cases performed by these centers are for musculoskeletal care, which includes total joint and spine procedures.

The deal is expected to generate $175 million in EBITDA during the first year, executives said.

SVB Leerink analysts characterized the deal as savvy and said it will reshape the company’s earnings towards a “faster growing, higher margin, and improved capital return profile.”

Heading into 2021, Tenet had expected a greater share of its earnings power to come from its outpatient surgery business. This deal accelerates that aim over the long-term.

In 2014, Tenet’s ambulatory surgery business accounted for just 5% of the company’s overall earnings. Prior to this latest deal, Tenet expected the unit to account for 42% of its overall earnings in 2021.

This latest announcement follows Tenet’s deal in October with Compass Surgical Partners to acquire its ownership and management interests in nine ambulatory surgery centers located in Florida, North Carolina and Texas for an undisclosed sum.

Two major policy developments emerged from this week’s release by the Centers for Medicare & Medicaid Services (CMS) of the FY22 proposed rule governing payment for hospital outpatient services and ambulatory surgical centers.

First, CMS proposes todramatically increase the financial penalties assessed to hospitals that fail to adequately reveal prices for their services, a requirement first put in place by the Trump administration. According to a report by the consumer group Patient Rights Advocate, only 5.6 percent of a random sample of 500 hospitals were in full compliance with the transparency requirement six months after the regulation came into effect, with many instead choosing to pay the $300 per hospital per day penalty associated with noncompliance. The new CMS regulation proposes to scale the assessed penalties in accordance with hospital size, with larger hospitals liable for up to $2M in annual penalties, a substantial increase from the earlier $109,500 maximum annual fine. In a press release, the agency said it “takes seriously concerns it has heard from consumers that hospitals are not making clear, accessible pricing information available online, as they have been required to do since January 1, 2021.” In a statement, the AHA stated that it was “deeply concerned” about the proposal, “particularly in light of substantial uncertainty in the interpretation of the rules.” The penalty hike is a clear signal that the Biden administration plans to put teeth behind its new push for more competition in healthcare, which was a major focus of the President’s recent executive order. We’d expect to see most hospitals and health systems quickly move to comply with the transparency rule, given the size of potential penalties.

More heartening to hospitals was CMS’ proposal to roll back changes the Trump administration made, aimed at shifting certain surgical procedures into lower cost, ambulatory settings. The agency proposed halting the elimination of the Inpatient Only (IPO) list, which specifies surgeries CMS will only pay for if they are performed in an inpatient hospital. Citing patient safety concerns, CMS noted that the phased elimination of the IPO list, which began this year, was undertaken without evaluating whether individual procedures could be safely moved to an outpatient setting. Nearly 300 musculoskeletal procedures have already been eliminated from the list, and will now be added back to the list for 2022, keeping the rest of the list intact while CMS undertakes a formal process to review each procedure. Longer term, we’d anticipate that CMS will look to continue the elimination of inpatient-only restrictions on surgeries, as well as pursuing other policies (such as site-neutral payment) that level the playing field between hospitals and lower-cost outpatient providers.

For now, hospitals will enjoy a little more breathing room to plan for the financial consequences of that inevitable shift.