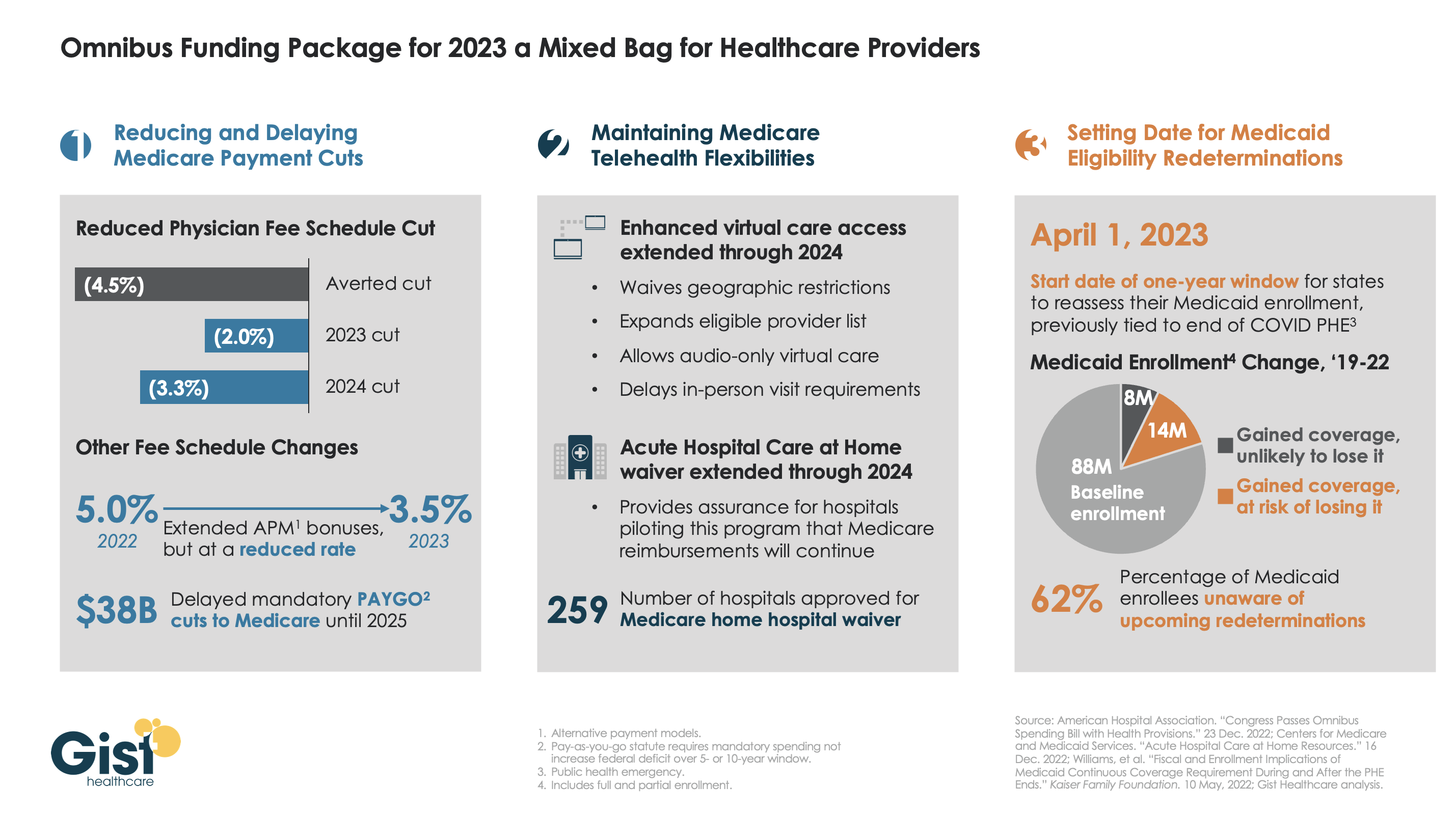

Late last week, President Biden signed a $1.7T spending package to fund the federal government through next September. While around half the funds are dedicated to defense, some important healthcare items made it into the bill, including a reduction in planned Medicare physician pay cuts and a two-year postponement of the $38B Medicare spending cut required by the PAYGO sequester.

The law also decoupled several measures from the end of the federal COVID public health emergency (PHE), setting April 1st as the start date for states to begin Medicaid eligibility redeterminations, and extending Medicare’s telehealth flexibilities and the Acute Hospital Care at Home waiver program through the end of 2024. For more details on these changes, see our graphic below.

The Gist: Medical groups were hoping for more of a reprieve from the Medicare physician fee schedule cuts, but Congress proved unwilling to address concerns over rising practice costs. We’re relieved that Medicare’s new telehealth and hospital at home policies will continue beyond the PHE, given the early interest we’ve seen from the provider community in embracing these new, more consumer-friendly care models.

Once the new Congress finally gets underway, we’re expecting this to be an uneventful two years for federal healthcare legislation, with the emphasis of health policy likely to shift toward states, federal agency rulemaking, and judicial activity.

Financial analysts have said that 2022 may have been the worst year for hospital finances in decades. This year looks like it will be yet another year of financial underperformance, with rural providers in especially dire circumstances.

What’s driving this bleak financial reality? It’s “primarily an expense story,” said Erik Swanson, a senior vice president at Kaufman Hall‘s data analytics practice.

“Growth in expenses has vastly outpaced growth in revenues — since pre-pandemic levels since last year, and even the year prior — such that margins are ultimately being pushed downward. And hospitals’ median operating margin is still below zero on a cumulative basis,” he declared, referring to 2021 and 2020.

Here’s some context about how dismal this situation is: Even in 2020, a year in which hospitals saw extraordinary losses during the first few months of the pandemic, they still reported operating margins of 2%.

What’s even more disconcerting is that hospitals are underperforming financially pretty much across the board, Swanson said.

Even Kaiser Permanente, one of the country’s largest health systems with an integrated delivery model, reported a $1.5 billion loss for the third quarter of 2022.

Rural hospitals are in even worse shape, but more on that below.

Other hospitals have been forced to shutter service lines to offset these financial losses. Some are also turning to integration and consolidation.

For example, Hermann Area District Hospital in Missouri said last month that it is seeking a “deeper affiliation” with Mercy Health or another provider. This announcement came after the hospital eliminated its home health agency as a cost-cutting measure. In December, the hospital projected a loss of $2 million for 2022.

We can also look at the mega-merger between Atrium Health and Advocate Aurora Health, which was completed last month. The deal, which is designed for cost synergy, creates the fifth-largest nonprofit integrated health system in the U.S.

The merger was finalized one day after North Carolina Attorney General Josh Stein expressed concern about how the deal could impact rural communities. He said that while he didn’t have a legal basis within his office’s limited statutory authority to block the deal, he was worried that it could further restrict access to healthcare in rural and underserved communities.

Stein brings up an extremely valid concern. Rural hospitals’ dismal financial circumstances are becoming more and more worrisome — in fact, about 30% of all rural hospitals are at risk of closing in the near future, according to a recent report from the Center for Healthcare Quality and Payment Reform (CHQPR).

A crucial reason for this is that it is more expensive to deliver healthcare in rural areas — usually because of smaller patient volumes and higher costs for attracting staff. Another factor is that payments rural hospitals receive from commercial health plans isn’t enough to cover the cost of delivering care to patients in rural areas, said Harold Miller, CEO of CHQPR.

“Many people assume that private commercial insurance plans pay more than Medicare and Medicaid. But for small rural hospitals, the exact opposite is true,” he said. “In many cases, Medicare is their best payer. And private health plans actually pay them well below their costs — well below what they pay their larger hospitals. One of the biggest drivers of rural hospital losses is the payments they receive from private health plans.”

In Miller’s view, rural hospitals perform two main functions: taking care of sick people in the hospital and being there for people in case they need to go to the hospital.

To fulfill the latter job, rural hospitals must operate 24/7 emergency rooms. These hospitals get paid when there’s an emergency, but not when there isn’t — even though the hospital is incurring costs by operating and staffing these units.

“Rural hospitals have a physician on duty 24/7 to be available for emergencies. But they don’t get paid for that by most payers. Medicare does pay them for that, but other payers don’t. If the hospital is doing two different things, we should be paying them for both of those things. Hospitals should be paid for what I refer to as ‘standby capacity,’” Miller said.

He bolstered his argument by pointing to these analogies: Do we only pay firefighters when there’s a fire? Do we only pay police officers when there’s a crime?

It’s also important to remember that rural hospitals are in the midst of transitioning to a post-pandemic environment, now without the pandemic-era financial assistance they received from the government, said Brock Slabach, chief operations officer at the National Rural Health Association.

“Rural providers are looking to move into the future without the benefit of those extra payments. And they’re in an environment of really high inflation. It’s over 8%, and for some goods and services in the healthcare sector, that’s going to be over 20% in terms of increased prices. Wages and salaries have also gone up significantly. But patient volumes have maintained below average or average. That all presents a huge challenge,” Slabach said.

Rural providers across the country are dealing with the stressors Slabach described and clamoring for more government help. For example, the Michigan Health & Hospital Association sought more money from the state last month after having to take 1,700 beds offline.

Many rural hospitals can’t escape their fate. From 2010 to 2021, there were 136 rural hospital closures. There were only two closures in 2021, and Slabach said 2022 produced a similarly low number. But these low totals are due to government relief, he explained. Slabach said he’s expecting an increase in rural hospital closures in 2023.

When a rural hospital closes, it means community members have to travel far distances for emergency or inpatient care. Miller pointed out another problem: in many rural communities, the hospital is the only place people can go to get laboratory or imaging work done. The hospital might also be the only source of primary care for the community. Shuttering these hospitals would be a massive blow to rural Americans’ healthcare access.

In the face of these potentially devastating blows to patient access, financial analysts’ outlook is bleak.

Higher inflation and costly labor expenses will continue to have negative effects on hospitals — both rural and urban — in 2023, according to an analysis from Moody’s. Expenses will also continue to increase due to supply chain bottlenecks, the need for more robust cybersecurity investments and longer hospital stays due to higher levels of patient acuity.

All of this doom and gloom begs the question — are any hospitals doing well financially?

The answer is yes, a select few. Let’s look at the three largest for-profit health systems in the nation — Community Health Systems, HCA Healthcare and Tenet Healthcare. As of 2020, these three public health systems accounted for about 8% of hospital beds in the U.S.

These three systems all had positive operating margins for the majority of the pandemic, including most recently in the third quarter of 2022.

Large public health systems have shareholders to report to and stock prices to worry about. Does this mean they’re more likely to deny care to patients who can’t afford it while other hospitals pick up the slack?

Slabach said it’s tough to say.

“Obviously, hospitals try to mitigate their exposure to risk when it comes to taking care of patients. Most hospitals do a really good job of providing services and care to people who don’t have insurance or don’t have the means to pay. But that gets stressed in this current financial environment. So indeed, there may be instances where what you suggested might happen, but it’s not because they want to deny services or deny care. It’s because they have a bigger picture they have to maintain,” Slabach said.

And the big picture involving dollar signs for hospitals looks pretty bleak in 2023.

A number of health systems experienced downgrades to their financial ratings in recent weeks amid ongoing operating losses, declines in investment values and challenging work environments.

Here is a summary of recent ratings since Becker’s last roundup Nov. 15:

The following systems experienced downgrades:

Adventist Health (Roseville, Calif.): Saw a downgraded long-term credit rating on bonds it holds, declining from “A” (negative) to “A-” (stable) by S&P Global Ratings.

The December downgrade follows a 2021 downgrade from Fitch Ratings from “A+” to “A.” That downgrade reflected “a series of one-time events and the lingering deleterious impact from the novel coronavirus” which “resulted in lower than anticipated operating EBITDA margins,” Fitch said. In November, Fitch added to this assessment by downgrading Adventist’s outlook from stable to negative, reflecting “continued negative operational pressure.”

The group, which operates 23 hospitals in California, Hawaii and Oregon, was also assigned an “A” rating by Fitch to 2022 bonds and other outstanding debt.

Catholic Health (Buffalo, N.Y.): The group was downgraded on debt from “B1” to “Caa2” by Moody’s and is in danger of defaulting on its covenants.

The nonprofit health system, which serves residents in Western New York with four acute care hospitals and several other facilities, saw its rating drop in November on approximately $364 million of debt.

Duke University Health System (Durham, N.C.): Downgraded to an “AA-” credit rating by Fitch Ratings.

The December downgrade comes amid concern over Duke’s planned integration of the Private Diagnostic Clinic, a for-profit medical group with more than 1,800 physicians.

The rating, reduced from “AA,” applies both to specific bonds the group holds and to its overall issuer default rating. In addition to the integration of the Private Diagnostic Clinic, Fitch also cited concern over macro issues such as labor and inflationary pressures, which have helped to drag down operating results for the health group.

Main Line Health (Radnor Township, Pa.): – Had its bond rating downgraded to “A1” from “Aa3” by Moody’s.

The December downgrade reflects a multiyear trend of weak operating performance and expectations of tepid progress into 2023, Moody’s said.

In addition to Main Line’s revenue bond rating declining, its outlook has been revised to stable from negative at the lower rating. The hospital group has approximately $651 million in outstanding debt, Moody’s said.

Prime Healthcare (Ontario, Calif.): The group was downgraded on probability of default rating to “B2-PD” from “B1-PD” as well as its ratings of the system’s senior secured notes to “B3” from “B2” by Moody’s.

Moody’s also revised the outlook in November to negative from stable because it projects operating expenses will continue to pressure the 45-hospital system’s profitability in the near term, presenting challenges for “the company’s pace of deleveraging,” according to a Nov. 18 news release.

Westchester County Health Care Corp. and Charity Health System (Valhalla, N.Y): The group was downgraded from “Baa2” to “Baa3” by Moody’s.

The December downgrade for CHS is based on WCHCC’s legal guarantee to pay debt service on CHS’ Series 2015 bonds, if CHS is unable. The outlook for both systems remains negative with WCHCC and CHS having $773 million and $127 million of debt, respectively, at the end of fiscal year 2021, Moody’s said.

St. Francis Medical Center in Trenton, N.J., on Dec. 21 transitioned to a freestanding emergency room that offers various outpatient services after Capital Health acquired the hospital from Trinity Health, according to PBS affiliate WHYY.

The campus, renamed Capital Health – East Trenton, must feature a primary family health clinic and a women’s OB/GYN clinic, according to terms of the transaction.

Other services, such as cardiac surgery, are moving to Capital Health Regional Medical Center in Trenton, where “extensive capital projects” are being planned, the health system said in a Dec. 8 news release.

A St. Francis spokesperson told the news outlet that the hospital had been financially struggling for years.

“St. Francis has done many great things for the Trenton community, but the current healthcare landscape has made it unsustainable,” Capital Health President and CEO Al Maghazehe said. “Without these key approvals, Trenton would have lost desperately needed healthcare services, including emergency services, behavioral health and cardiac surgery.”

Capital Health said it has taken “a significant risk” to try and prevent a healthcare crisis for Trenton’s 90,000 residents, according to the report.

Healthcare added almost 45,000 jobs in November, but many hospitals and health systems will continue to struggle to meet staffing needs, retain top executives and providers, and foster long-term pipelines for talent, Ted Chien, president and CEO of independent consulting firm SullivanCotter, wrote in a Dec. 15 article for Nasdaq.

Hospitals and health systems are living “paycheck to paycheck” and unable to make long-term investments at the height of the current workforce crisis, Mr. Chien said.

The challenge boils down to a healthcare delivery problem, not a demand problem.

Baby Boomers are the greatest source of care demand on the healthcare system, but are unable to contribute to the provider workforce in the numbers needed to achieve balance, according to Mr. Chien. To compound that issue, burnout is a major factor why “too many” frontline workers have left or plan to exit healthcare, he said.

Last year, an estimated 333,942 healthcare providers dropped out of the workforce, including about 53,000 nurse practitioners, which has led hospitals to spend more on contract labor and feeling more pressure to consolidate, according to an October report published by Definitive Healthcare.

Long term, a continued lack of healthcare workers would force hospitals to operate in a heightened crisis mode, according to Mr. Chien, depriving non-critical patients of sufficient health prevention and demanding too much of providers who are already overly taxed.

Mr. Chien highlighted three key areas to tackle the workforce crisis: smarter technology, resilient teams and excellent leadership.

Technologies that alleviate providers’ administrative burdens will be critical to reduce burnout and keep caregivers focused on patient care, while smarter tech can also forge pipelines for future providers by streamlining clinical experience operations and aligning student placements with existing opportunities.

Building resilient teams begins with competitive pay and robust benefit packages, which fosters trust and demonstrates that a hospital values its staff, according to Mr. Chen. Supporting career growth, including upskilling and redeploying staff when appropriate, empowers employees.

Lastly, capable executive leadership teams, under intense scrutiny from industry stakeholders, must clearly outline their hospital or health system’s strategy and provide the change needed to support their staff. Lack of trust in leaders drives staff out of healthcare, so it is crucial to recruit and retain “modern, strategic thinkers with depth of experience who are prepared to lead,” Mr. Chien wrote.

The majority of hospitals are predicted to have negative margins in 2022, marking the worst year financially for hospitals since the beginning of the Covid-19 pandemic.

In Part 1 of Radio Advisory’s Hospital of the Future series, host Rachel (Rae) Woods invites Advisory Board experts Monica Westhead, Colin Gelbaugh, and Aaron Mauck to discuss why factors like workforce shortages, post-acute financial instability, and growing competition are contributing to this troubling financial landscape and how hospitals are tackling these problems.

As we emerge from the global pandemic, health care is restructuring. What decisions should you be making, and what do you need to know to make them? Explore the state of the health care industry and its outlook for next year by visiting advisory.com/HealthCare2023.

Radio Advisory’s Rachel Woods sat down with Optum EVP Dr. Jim Bonnette to discuss the sustainability of modern-day hospitals and why scaling down might be the best strategy for a stable future.

Rachel Woods:When I talk about hospitals of the future, I think it’s very easy for folks to think about something that feels very futuristic, the Jetsons, Star Trek, pick your example here. But you have a very different take when it comes to the hospital, the future, and it’s one that’s perhaps a lot more streamlined than even the hospitals that we have today. Why is that your take?

Jim Bonnette: My concern about hospital future is that when people think about the technology side of it, they forget that there’s no technology that I can name that has lowered health care costs that’s been implemented in a hospital. Everything I can think of has increased costs and I don’t think that’s sustainable for the future.

And so looking at how hospitals have to function, I think the things that hospitals do that should no longer be in the hospital need to move out and they need to move out now. I think that there are a large number of procedures that could safely and easily be done in a lower cost setting, in an ASC for example, that is still done in hospitals because we still pay for them that way. I’m not sure that’s going to continue.

Woods: And to be honest, we’ve talked about that shift, I think about the outpatient shift. We’ve been talking about that for several years but you just said the change needs to happen now. Why is the impetus for this change very different today than maybe it was two, three, four, five years ago? Why is this change going to be frankly forced upon hospitals in the very near future, if not already?

Bonnette: Part of the explanation is regarding the issues that have been pushed regarding price transparency. So if employers can see the difference between the charges for an ASC and an HOPD department, which are often quite dramatic, they’re going to be looking to say to their brokers, “Well, what’s the network that involves ASCs and not hospitals?” And that data hasn’t been so easily available in the past, and I think economic times are different now.

We’re not in a hyper growth phase, we’re not where the economy’s performing super at the moment and if interest rates keep going up, things are going to slow down more. So I think employers are going to become more sensitized to prices that they haven’t been in the past. Regardless of the requirements under the Consolidated Appropriations Act, which require employers to know the costs, which they didn’t have to know before. They’re just going to more sensitive to price.

Woods: I completely agree with you by the way, that employers are a key catalyst here and we’ve certainly seen a few very active employers and some that are very passive and I too am interested to see what role they play or do they all take much more of an active role.

And I think some people would be surprised that it’s not necessarily consumers themselves that are the big catalyst for change on where they’re going to get care, how they want to receive care. It’s the employers that are going to be making those decisions as purchasers themselves.

Bonnette: I agree and they’re the ultimate payers. For most commercial insurance employers are the ultimate payers, not the insurance companies. And it’s a cost of care share for patients, but the majority of the money comes from the employers. So it’s basically cutting into their profits.

Woods: We are on the same page, but I’m going to be honest, I’m not sure that all of our listeners are right. We’re talking about why these changes could happen soon, but when I have conversations with folks, they still think about a future of a more consolidated hospital, a more outpatient focused practice is something that is coming but is still far enough in the future that there’s some time to prepare for.

I guess my question is what do you say to that pushback? And are there any inflection points that you’re watching for that would really need to hit for this kind of change to hit all hospitals, to be something that we see across the industry?

Bonnette: So when I look at hospitals in general, I don’t see them as much different than they were 20 years ago. We have talked about this movement for a long time, but hospitals are dragging their feet and realistically it’s because they still get paid the same way until we start thinking about how we pay differently or refuse to pay for certain kinds of things in a hospital setting, the inertia is such that they’re going to keep doing it.

Again, I think the push from employers and most likely the brokers are going to force this change sooner rather than later, but that’s still probably between three and five years because there’s so much inertia in health care.

On the other hand, we are hitting sort of an unsustainable phase of cost. The other thing that people don’t talk about very much that I think is important is there’s only so many dollars that are going to health care.

And if you look at the last 10 years, the growth in pharmaceutical spend has to eat into the dollars available for everybody else. So a pharmaceutical spend is growing much faster than anything else, the dollars are going to come out of somebody’s hide and then next logical target is the hospital.

Woods: And we talked last week about how slim hospital margins are, how many of them are actually negative. And what we didn’t mention that is top of mind for me after we just come out of this election is that there’s actually not a lot of appetite for the government to step in and shore up hospitals.

There’s a lot of feeling that they’ve done their due diligence, they stepped in when they needed to at the beginning of the Covid crisis and they shouldn’t need to again. That kind of savior is probably not their outside of very specific circumstances.

Bonnette: I agree. I think it’s highly unlikely that the government is going to step in to rescue hospitals. And part of that comes from the perception about pricing, which I’m sure Congress gets lots of complaints about the prices from hospitals.

And in addition, you’ll notice that the for-profit hospitals don’t have negative margins. They may not be quite as good as they were before, but they’re not negative, which tells me there’s an operational inefficiency in the not for-profit hospitals that doesn’t exist in the for-profits.

Woods: This is where I wanted to go next. So let’s say that a hospital, a health system decides the new path forward is to become smaller, to become cheaper, to become more streamlined, and to decide what specifically needs to happen in the hospital versus elsewhere in our organization.

Maybe I know where you’re going next, but do you have an example of an organization who has had this success already that we can learn from?

Bonnette: Not in the not-for-profit section, no. In the for-profits, yes, because they have already started moving into ambulatory surgery centers. So Tenet has a huge practice of ambulatory surgery centers. It generates high margins.

So, I used to run ambulatory surgery centers in a for-profit system. And so think about ASCs get paid half as much as a hospital for a procedure, and my margin on that business in those ASCs was 40% to 50%. Whereas in the hospital the margin was about 7% and so even though the total dollars were less, my margin was higher because it’s so much more efficient. And the for-profits already recognize this.

Woods: And I’m guessing you’re going to tell me you want to see not-for-profit hospitals make these moves too? Or is there a different move that they should be making?

Bonnette: No, I think they have to. I think there are things beyond just ASCs though, for example, medical patients who can be treated at home should not be in the hospital. Most not-for-profits lose money on every medical admission.

Now, when I worked for a for-profit, I didn’t lose money on every Medicare patient that was a medical patient. We had a 7% margin so it’s doable. Again, it’s efficiency of care delivery and it’s attention to detail, which sometimes in a not-for-profit friends, that just doesn’t happen.

Since the early days of the pandemic, the healthcare industry has faced seemingly insurmountable challenges to ensure access to high-quality care. While healthcare providers have performed admirably in the face of these challenges, patients are still seeing access challenges that are impacting their behaviors — which can lead to challenges in the long run.

In the 2022 BDO Patient Experience Survey, they sought to learn how patients feel about their providers and healthcare experience — from making appointments and interacting with care providers, to how patients access health insurance and who patients turn to for routine care.

From the survey of over 3,000 U.S. adults, they came across a few key takeaways:

1. Delaying routine care is the new norm

Americans face a troubling dilemma: While 92% have health insurance and 91% have a regular care provider, 58% admit to delaying routine medical care in the past 12 months.

For routine (non-emergency) care, 69% of respondents report seeing a primary care physician and 12% routinely visit primary care nurse/nurse practitioner or physician assistant. Just 9% do not have a provider for routine medical care. Our survey found that Americans use a wide variety of health insurance options with employer-sponsored insurance (32%) being the most popular, followed by Medicare (28%), Medicaid (14%) and individual private insurance (7%). While 8% report having no health insurance, even those with insurance faced significant barriers to care.

Of those who delayed seeking medical care in the past 12 months, 30% cite unaffordability due to high out-of-pocket costs and 19% say they could not afford to seek care due to a lack of insurance. In addition to the high costs of medical care, many Americans struggle with a lack of cost transparency.

2. Cost transparency is a continuing problem

Nearly a third of Americans (31%) have never tried to obtain cost estimates for medical care. When patients do not know what healthcare will cost, many avoid seeking necessary care. A critical way we can improve patient access to healthcare is to understand how patients like to obtain cost estimates.

Of patients surveyed who have sought cost estimates, most prefer to reach out to a person, with 38% preferring to contact their insurance provider and 37% opting to ask the healthcare provider’s administrative staff. On the digital side, 31% say they obtained cost estimates by looking at online patient portals and 27% look to health provider or medical facility websites.

3. Most patients experience frustration when seeking and receiving care

We know that long appointments lead times and high costs cause patients to put off care — but how do patients feel about the actual care they receive? 69% of Americans experience frustration during routine medical appointments, with having to wait for a late provider (29%), not getting enough time with the provider (22%) and having too much paperwork to fill out (21%) being the most common frustrations.

When providers make it easier for patients to receive care, their efforts are noticed. Patients say providers make care more accessible by offering telehealth appointments (32%), reaching out to proactively schedule appointments (29%), offering walk-in appointments (27%) and implementing online/self-service scheduling (23%).

Patients are facing a challenging care environment — and so are providers. Fortunately, there are ways that providers can improve access and the care experience for their patients without breaking their budgets.

Hospitals across the country are being hit with a spike in respiratory syncytial virus (RSV) and influenza cases, while still dealing with a steady flow of COVID admissions, in what’s been dubbed a “tripledemic”. The graphic above uses hospitalization data from the Centers for Disease Control and Prevention (CDC) to show that each disease has been sending similar shares of the population to hospitals across late fall, with flu hospitalizations having just overtaken COVID admissions after Thanksgiving.

These numbers reflect that we’re experiencing the worst RSV season in at least five years, and we’re set to endure the worst flu season since 2009-10.As RSV is most severe in very young children, its recent surge has revealed another capacity shortage in our nation’s hospitals: pediatric beds. From 2008 to 2018, pediatric inpatient bed counts fell by 19 percent, as hospitals shifted resources to higher revenue services.

This strategy has now come to a head in many parts of the country, as RSV has driven pediatric bed usage rates to a recent high. (The Department of Health and Human Services’ pediatric capacity data only dates back to August 2020.) With three straight weeks of declining RSV hospitalizations, there is reason to hope that pediatric care units will soon feel a reprieve. However, flu season has yet to reach its peak, prompting calls for a return to widespread mask-wearing and a renewed emphasis on flu shots, given that more than half of Americans have not yet gotten vaccinated this season.

It’s been a difficult year for the hospital workforce, both here and around the world, as the effects of the pandemic, the economy, and the legacy of lean staffing models have combined to drive up vacancy rates and threaten the sustainability of hospital operations.

Everywhere we’ve gone in the past six months, workforce issues have overshadowed every other topic: how can hospitals attract and retain staff given the environment, how can they stabilize finances in the face of 15-20 percent increases in labor costs, how can they safeguard patient care with intense turbulence in the clinical workforce?

This week we heard yet another wrinkle to this problem, one that had not occurred to us but in retrospect is obvious. A system CFO was lamenting the fact that even with big salary increases, the hospital workforce remains unstable. “It’s like we’re not even getting credit for raising base salary 15 percent across the board and giving big retention bonuses.”

As to why—it’s a timing issue. Her system, like many, delivered pay raises back in the late winter and early spring, when staff were still recovering from the Omicron surge and the urgency of reducing reliance on expensive agency labor became clear. But economy-wide inflation had only then begun to spike, and has since continued to be stuck at high levels.

Staff don’t view the earlier salary increases as a response to inflation, but as predating it—and they’re asking for still more, to offset rising prices for food, transportation and housing. “I wish we’d waited to give the pay bump,” the CFO told us. “Even though our wage increases have outpaced inflation this year, the timing of events didn’t help us at all.”

With the hospitals operating near capacity, and a severe flu season impacting both patient volumes and staff availability, her sense is that the system is back to square one on staffing—and more difficult financial decisions lie ahead.